Download as PPSX, PPTX

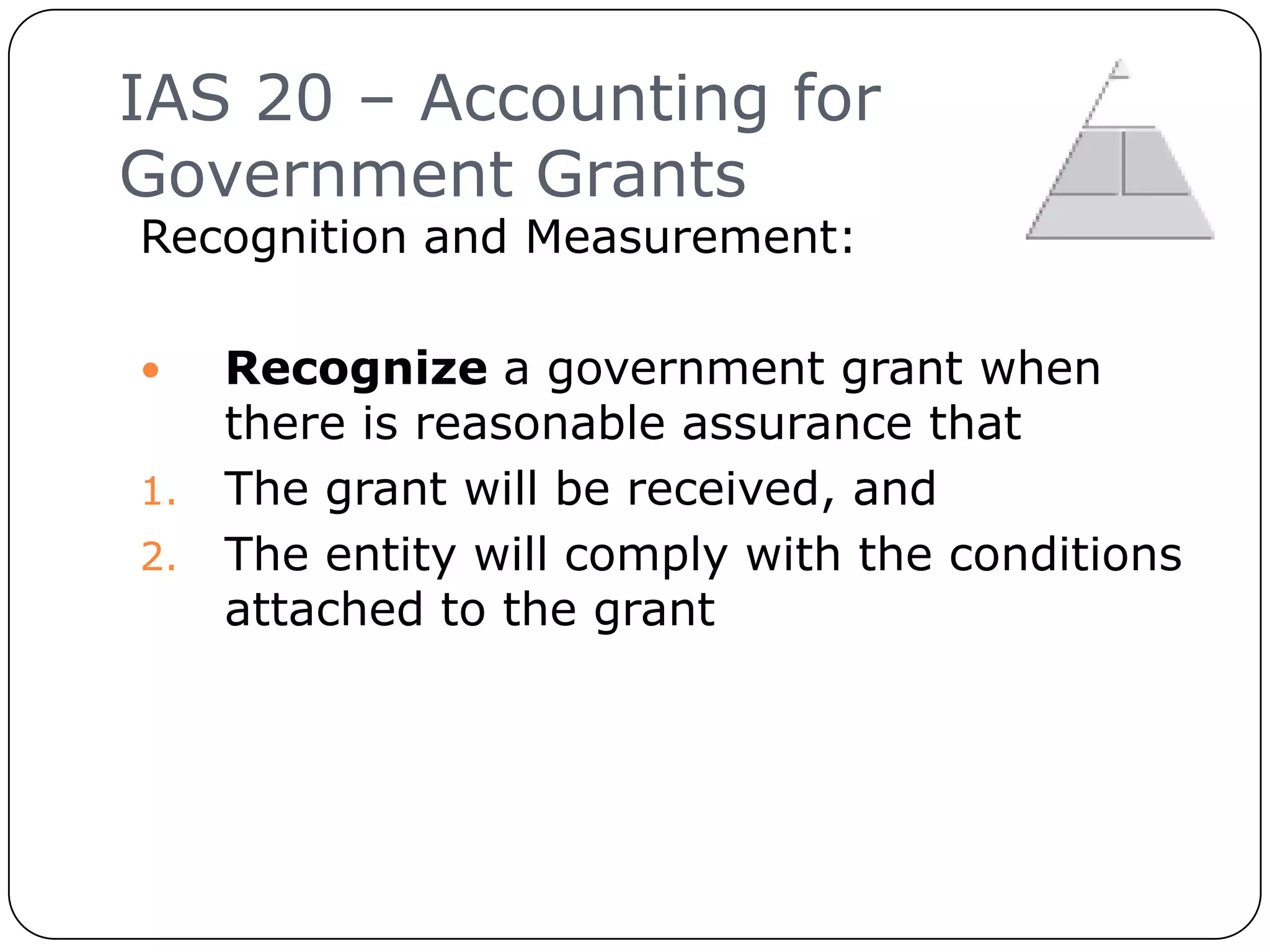

This document provides an overview of IAS 20, which establishes the accounting requirements for government grants and disclosure of government assistance. It discusses how government grants should be recognized as income or deferred income depending on whether they are related to assets or income. It also covers repayment of grants if conditions are not met and disclosure requirements. The end of chapter practice problems provide examples of accounting for government grants and assistance related to assets, income, and contingencies.