Drug Store Cap Rates Fall to Record Lows in Q3 2013

•

0 likes•435 views

net lease drug store research report

Recommended

Recommended

More Related Content

What's hot

What's hot (20)

Similar to Drug Store Cap Rates Fall to Record Lows in Q3 2013

Similar to Drug Store Cap Rates Fall to Record Lows in Q3 2013 (20)

More from The Boulder Group

More from The Boulder Group (20)

Recently uploaded

Recently uploaded (20)

Drug Store Cap Rates Fall to Record Lows in Q3 2013

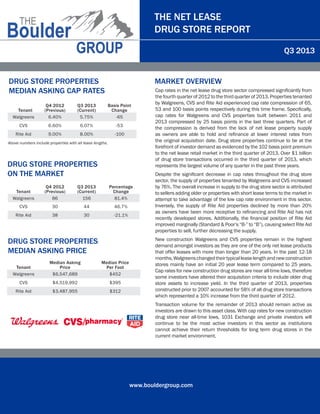

- 1. THE NET LEASE DRUG STORE REPORT Q3 2013 DRUG STORE PROPERTIES MEDIAN ASKING CAP RATES MARKET OVERVIEW Tenant Walgreens Q4 2012 (Previous) 6.40% Q3 2013 (Current) 5.75% Basis Point Change -65 CVS 6.60% 6.07% -53 Rite Aid 9.00% 8.00% -100 Above numbers include properties with all lease lengths. DRUG STORE PROPERTIES ON THE MARKET Tenant Walgreens Q4 2012 (Previous) 86 Q3 2013 (Current) 156 Percentage Change 81.4% CVS 30 44 46.7% Rite Aid 38 30 -21.1% DRUG STORE PROPERTIES MEDIAN ASKING PRICE Tenant Walgreens Median Asking Price $6,547,689 Median Price Per Foot $452 CVS $4,519,992 $395 Rite Aid $3,487,955 $312 Cap rates in the net lease drug store sector compressed significantly from the fourth quarter of 2012 to the third quarter of 2013. Properties tenanted by Walgreens, CVS and Rite Aid experienced cap rate compression of 65, 53 and 100 basis points respectively during this time frame. Specifically, cap rates for Walgreens and CVS properties built between 2011 and 2013 compressed by 25 basis points in the last three quarters. Part of the compression is derived from the lack of net lease property supply as owners are able to hold and refinance at lower interest rates from the original acquisition date. Drug store properties continue to be at the forefront of investor demand as evidenced by the 102 basis point premium to the net lease retail market in the third quarter of 2013. Over $1 billion of drug store transactions occurred in the third quarter of 2013, which represents the largest volume of any quarter in the past three years. Despite the significant decrease in cap rates throughout the drug store sector, the supply of properties tenanted by Walgreens and CVS increased by 76%. The overall increase in supply to the drug store sector is attributed to sellers adding older or properties with short lease terms to the market in attempt to take advantage of the low cap rate environment in this sector. Inversely, the supply of Rite Aid properties declined by more than 20% as owners have been more receptive to refinancing and Rite Aid has not recently developed stores. Additionally, the financial position of Rite Aid improved marginally (Standard & Poor’s “B-” to “B”), causing select Rite Aid properties to sell, further decreasing the supply. New construction Walgreens and CVS properties remain in the highest demand amongst investors as they are one of the only net lease products that offer leases with more than longer than 20 years. In the past 12-18 months, Walgreens changed their typical lease length and new construction stores mainly have an initial 20 year lease term compared to 25 years. Cap rates for new construction drug stores are near all-time lows, therefore some investors have altered their acquisition criteria to include older drug store assets to increase yield. In the third quarter of 2013, properties constructed prior to 2007 accounted for 58% of all drug store transactions which represented a 10% increase from the third quarter of 2012. Transaction volume for the remainder of 2013 should remain active as investors are drawn to this asset class. With cap rates for new construction drug store near all-time lows, 1031 Exchange and private investors will continue to be the most active investors in this sector as institutions cannot achieve their return thresholds for long term drug stores in the current market environment. www.bouldergroup.com

- 2. THE NET LEASE DRUG STORE REPORT Q3 2013 MEDIAN ASKING CAP RATE BY BUILDING AGE Year Built Walgreens CVS Rite Aid 2011-2013 5.50% 5.75% N/A 2005-2010 5.75% 6.00% 7.58% 2000-2004 6.20% 6.45% 8.00% 1995-1999 7.25% 7.64% 8.72% Before 1994 7.70% 8.00% 9.90% CVS Rite Aid MEDIAN ASKING CAP RATE BY PROPERTY TYPE Property Type Walgreens Ground Lease 5.00% 5.00% 6.50% Fee Simple 5.75% 6.07% 8.00% MEDIAN NATIONAL ASKING VS. CLOSED CAP RATE SPREAD DRUG STORE VS. RETAIL NET LEASE MARKET CAP RATE Tenant Walgreens Closed 6.20% Asking 6.13% CVS 6.20% 6.00% 20 Rite Aid 8.36% 8.10% 26 Q4 2012 (Previous) 6.93% Q3 2013 (Current) 6.00% Retail Net Lease Market 7.25% 7.02% Drug Store Premium (bps) Spread (bps) 7 32 102 Tenant Drug Store www.bouldergroup.com

- 3. THE NET LEASE DRUG STORE REPORT Q3 2013 COMPANY AND LEASE OVERVIEW Walgreens CVS Rite Aid Credit Rating BBB (Stable) BBB+ (Stable) B (Stable) Market Cap $56 billion $76 billion $4 billion Revenue $72 billion $123 billion $25 billion 2014 Stores Planned (Company estimates) 150 150 N/A Number of Stores 8,582 7,553 4,623 Typical Lease Term 20 or 25 year primary term with fifty years of options 25 year primary term with six 5-year options 20 year primary term with six 5-year options Typical Rent Increases None None in primary 10% increases in option periods Increases every 10 years of 10% FOR MORE INFORMATION AUTHOR John Feeney | Research Director john@bouldergroup.com CONTRIBUTORS Randy Blankstein | President rblank@bouldergroup.com Jimmy Goodman | Partner jimmy@bouldergroup.com Zach Wright | Research Analyst zach@bouldergroup.com © 2013. The Boulder Group. Information herein has been obtained from databases owned and maintained by The Boulder Group as well as third party sources. We have not verified the information and we make no guarantee, warranty or representation about it. This information is provided for general illustrative purposes and not for any specific recommendation or purpose nor under any circumstances shall any of the above information be deemed legal advice or counsel. Reliance on this information is at the risk of the reader and The Boulder Group expressly disclaims any liability arising from the use of such information. This information is designed exclusively for use by The Boulder Group clients and cannot be reproduced, retransmitted or distributed without the express written consent of The Boulder Group. www.bouldergroup.com