In Sharjah ௵(+971)558539980 *_௵abortion pills now available.

How T-Mobile & Sprint will win Deal Approval

1. All rights reserved,InflectionCapital Management, LLC

Thesis:

Should T-Mobile merge with Sprint and their combined 5G service launch as we describe, the stock

should generate nearly an 80% annualized return through 2020.

Key Points:

1) We think that the DOJ/FCC will approve S+TMUS with conditions in the 1H’19 because the

DOJ/FCC will admit that they failed consumers in broadband and paid-TV competition.

2) The regulatory approval conditions will include: 1) the commitment to a specified 5G wireless

nationwide service, 2) the commitment to a fixed wireless service broadband alternative in

many single-provider markets, 3) a commitment to a 5G price cap that references the 4G

price, and 4) a limit to wireless price inflation in prepaid and potentially divestiture.

3) Excitement for 5G wireless will build in the 1H’19. We expect TMUS to launch in 30 markets with

a $78/mo price single-line Unlimited price point for 4G+5G.

4) As Wall Street gets comfortable with TMUS’ 5G momentum including a step-up in postpaid

share gains in the 2H’19, we expect substantial favorableconsensus revisions. Our 2020 EBITDA

estimate for TMUS is 14% higher than consensus.

5) We expect TMUS EV/EBITDA NTM valuation multiple to expand from6.5X to 8.5X based upon

faster top- and bottom-line growth, larger sharegains, and new TAMS.

Stating the obvious:

There are no sound 80% projected annualized returns for large cap stocks. Consequently, you are

missing something basic and just being stupid.

ICM’s Response:

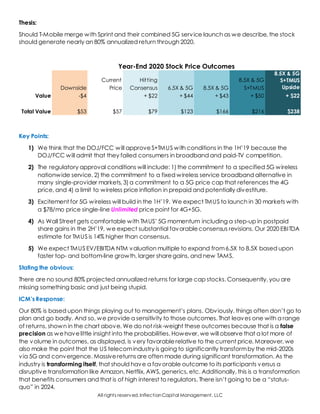

Our 80% is based upon things playing out to management’s plans. Obviously, things often don’t go to

plan and go badly. And so, we provide a sensitivity to those outcomes. That leaves one with a range

of returns, shown in the chart above. We do not risk-weight these outcomes because that is a false

precision as wehavelittle insight into the probabilities. However, we will observe that a lot more of

the volume in outcomes, as displayed, is very favorablerelative to the current price. Moreover, we

also make the point that the US telecomindustry is going to significantly transformby the mid-2020s

via 5G and convergence. Massivereturns are often made during significant transformation. As the

industry is transforming itself, that should have a favorable outcome to its participants versus a

disruptive transformation like Amazon, Netflix, AWS, generics, etc. Additionally, this is a transformation

that benefits consumers and that is of high interest to regulators. There isn’t going to be a “status-

quo” in 2024.

Year-End 2020 Stock Price Outcomes

Downside

Current

Price

Hitting

Consensus 6.5X & 5G 8.5X & 5G

8.5X & 5G

S+TMUS

8.5X & 5G

S+TMUS

Upside

Value -$4 + $22 + $44 + $43 + $50 + $22

Total Value $53 $57 $79 $123 $166 $216 $238

2. All rights reserved,InflectionCapital Management, LLC

Final point before weget into the details. People are highly dependent upon their phones; it’s their

lifeline to family, friends, work, and the community. They are using that device2-3 hours per day. It’s

like a “fifth appendage.” The utility of the appendage improves every year. 5G is going to be a

massive upgrade to that appendage (just like Steve Austin’s armin the Six Million Dollar Man). It will

unite the device and service with the cloud. The change is going to be as demonstrable as going

froma 32-bit desktop PC to the cloud, fromdial-up to 100 Gbps, fromlandline to mobile. The carriers

are going to pour $200B into upgrading the network. They are doing so because the ROI fromthis

investment is based upon a greatly expanded TAM. T-Mobile’s penetration of that larger TAM is not in

Wall Street estimates. If the reader believes that the TAM expansion is going to be zero and that T-

Mobile’s management won’t execute, then read no more. This piece isn’t going to convince any flat-

earth fanatic that the earth is spherical.

Below we address each of the five primary fears about buying TMUS here and now:

Fear-1: The wireless industry is mature and without pricing power. Eventually, margins and FCF are

going to decline. Cable entering the wireless market is just going to make matters worse.

Service revenue (as currentlydefined) for the industryis mature. That isn’t debated. Service revenue has been

down quarterlysince 2015. The move to “unlimited” undermined the industry’s abilityto get paid transparentlyfor

more data usage.

It is also not debatedthat the industryis without pricing power (for now). This is seen in the CPI index, especiallyin

2017 which Verizonand AT&T went unlimited.Pricing has now flattenedout and the industryparticipants generally

suggest that it will staythat way (i.e.not another decline).

However,the flipside of these falling prices is improving consumer satisfactionwiththe industryand the value

consumers get from the industry. This is shown in the table below from ACSI. In 2017,the wireless industry

acceleratedinits satisfactionimprovement.All other categories materiallydecelerated. Consumer affinityscores

(Net Promotor Scores)for the wireless companies are also on the rise and substantiallyabove cable and satellite

companies. These statistics suggest that the wireless industryhas “earned the right to price” when it brings

substantial new features to market. 5G is to allow for 15X-100X higher data speeds, better coverage,longer battery

life,push-to-talk,etc.(For reference,the 3G to 4G speed step was 3X.) 15X is a substantiallybetter product,like 6

seconds for a movie download. We have seen no evidence that the consumer will not be willing to pay more for

that product. For the industryto get a favorable ROI (11%) on its 5G investment, it willneed to price 5G at a

$7.50/mo premium to 4G (see 5G sectionbelow). We have seen no evidence that the industryis going to accept a

lower ROI. Consequently, +$7.50 is our base case assumptionfor 5G. Consumer demand for more data and the

umbrella of 5G should also foster +LSD 4Gpricing.

Series Title:

Area:

Item:

Year Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2011 60.572 60.437 60.351 60.353 60.341 60.340 59.902 59.889 59.860 59.895 59.895 59.931

2012 59.919 59.919 59.935 59.953 60.008 60.005 59.582 59.138 59.294 59.492 59.445 59.447

2013 59.357 59.202 59.139 58.577 58.577 58.566 58.430 58.363 58.332 58.331 58.276 58.249

2014 58.137 57.852 57.775 57.872 57.709 57.677 57.677 57.653 57.599 56.507 56.179 55.894

2015 55.614 55.406 54.975 54.902 54.537 54.555 54.711 55.194 55.388 55.514 55.908 55.883

2016 55.850 55.267 55.280 55.294 54.967 54.989 54.848 54.786 54.033 53.739 53.578 53.522

2017 53.435 52.679 49.002 48.153 48.118 47.735 47.580 47.550 47.730 47.944 48.090 48.066

2018 47.972 47.712 47.822 47.835

2016 0% 0% 1% 1% 1% 1% 0% -1% -2% -3% -4% -4%

2017 -4% -5% -11% -13% -12% -13% -13% -13% -12% -11% -10% -10%

2018 -10% -9% -2% -1%

Wireless telephone services in U.S. city

average, all urban consumers, not seasonallyU.S. city average

Wireless telephone services

CPI-All Urban Consumers (Current Series)

3. All rights reserved,InflectionCapital Management, LLC

Margins

Are there costs rising inthe business that are outgrowing revenue resulting inmargin compression? There are some

transitoryfactors,but we can find no evidence of structural marginerosion,outside of the negative effect from the

move to Unlimited. Cost to serve remains relativelystable as shown in Verizon’s results inthe table below. There is

likelysome expense inflationfor marketing and retail,but those do not show through. (We use Verizon’s report

because AT&T doesn’t disclose the numbers and T-Mobile’s and Sprint’s numbers have noise.)

The second table shown below is an aggregationof Verizonand AT&T wireless results.We focus on the underlying

service marginby stripping-awaythe impact of equipment and adding back the impact to revenue and EBIT from

their 1-time moves to Unlimited.This analysis shows that margins have climbedeach of the past five quarters

excluding Unlimited. Consequently, for one to argue that industrymargins are going down from here, one needs to

argue that pricing is going lower.We argue the contraryabove,i.e. that pricing is going to rise.

Verizon Communications Inc.

2018

Unaudited 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q

Operating Expenses

Cost of services 1,942 1,984 2,006 2,056 1,958 1,997 2,052 1,983 2,215

Total Pre- & Postpaid Connections 113 113 114 114 114 115 115 116 116

(millions)

Monthly Cost per Connection 5.75$ 5.84$ 5.88$ 6.00$ 5.73$ 5.81$ 5.93$ 5.69$ 6.35$

YoY % Ch 0% -1% 1% -5% -1%

Note: Q1'18 costs are reported under a new accounting treatment. We show the YoY change normalized for this.

Wireless - Selected Financial

2016 2017

Verizon & AT&T's Wireless Results

2016 2017 2018

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q

Non-Equipment Revenue 32,800$ 32,856$ 32,879$ 32,288$ 31,582$ 31,455$ 31,703$ 31,578$ 31,078$

Non-Equipment EBIT 14,930 14,979 14,925 13,662 13,999 13,945 13,877 12,814 13,907

Margin 45.5% 45.6% 45.4% 42.3% 44.3% 44.3% 43.8% 40.6% 44.7%

Unlimited 's impact on Revenue & EBIT 1,476$ 1,479$ 1,480$ 1,453$ 1,421$

Adjusted Revenue 32,800$ 32,856$ 32,879$ 32,288$ 33,058$ 32,934$ 33,183$ 33,031$ 32,499$

Adjusted EBIT 14,930 14,979 14,925 13,662 15,475 15,424 15,356 14,267 15,328

Margin 45.5% 45.6% 45.4% 42.3% 46.8% 46.8% 46.3% 43.2% 47.2%

YoY Change 129 bps 124 bps 89 bps 88 bps 35 bps

4. All rights reserved,InflectionCapital Management, LLC

Cable’s Entrance

Comcast has enteredthe market, bundling wireless along withtheir other services.Charter is also expectedsoon.

Comcast/Charter’s primary objective is to reduce video/broadband churn and improve customer life-time-value

versus to earn significant profits from a wireless offering. Whenever a new entrant has a different economic

incentive fromthe incumbents,there is higher risk that the incumbents’and industry’s economics get disrupted.

Xfinity-Mobile’s offer is free voice andtiereddata at a price of $12-$45/mo (bundled withXfinity-TV & internet)per

line; the $45/mo- price is for unlimited.A subscriber can start at the lower price-tier for less monthlydata and if they

exceedtheir data limit choose to upgrade to a higher tier (and be charged a pro-rata amount). An industryprice

comparisonis shown below. Giventhat the Xfinityoffering is solelytargetedat its subscriber base,which are

families,its pricing plan is curious to us. Assuming 3.5 lines per HH, its service wouldcost ~$157/mo.which is higher

than Sprint,Verizon,and T-Mobile.Thus, their strategymust be to pick-off families that are interestedin saving

money and restraining their data usage. The researchthat we have seen suggests that this is a small part of the

market. User reviews of Xfinity-Mobile are generallyveryfavorable. But as currentlypriced,we don’t view Xfinity-

Mobile as disruptive to the market.

Xfinity-Mobile now has 577K service lines,including an added 196K in Q1. Giventhat Xfinity-Mobile is marketed only

to Xfinitycustomers,one needs to adjust for the footprint to compare to the other wireless operators. Xfinityhas

27.4m residential customers,meaning that they are only marketing to ~25% of US households. Consequently, their

comparative gross adds for Q1 were 784K (196K/.25). Shownin the table below is how Xfinity’s gross adds

compared to the incumbents. On a relative basis,theyare doing about half as well as Sprint whichwe would

characterize as “solid” giventhat Comcast is new to the market.

Price Comparison For Unlimited

5.25.18

Xfinity Sprint Verizon AT&T T-Mobile

1-Line $45 $60 $75 $80 $70

2-Lines $90 $100 $130 $150 $100

3-Lines $135 $130 $150 $170 $140

4-Lines $180 $160 $160 $190 $160

Unlimted Limit 20 GB 10 GB 22 GB 22 GB 50 GB

Bundling Free HBO Netflix

Required w/ 2 Lines Included

Postpaid Gross Additions

In thousands 1Q17 2Q17 3Q17 4Q17 1Q18

Postpaid

AT&T Mobility (connections) 2,563 2,446 2,577 2,914 2,413

Sprint (phone) 1,296 1,279 1,546 1,563 1,563

T-Mobile (phone) 1,920 1,854 2,032 2,086 1,722

Verizon (connections) 3,490 3,702 3,808 4,498 3,755

Charter (Grossed-up) 0 0

Xfinity (Grossed-up) 524 784

Total 9,269 9,281 9,963 11,584 10,237

5. All rights reserved,InflectionCapital Management, LLC

The Disconnects table shows that incumbent disconnects are below the level experiencedinQ1’16 despite the

intrusionof Xfinity. (Note the YoY decline reportedinQ1’18 is against a verydisruptive periodinQ1’17 when Verizon

and AT&T launched their own unlimitedplans.) The total WirelessSubscribers table shows that the entire industry

grew by 2.6% lines and +4% in post-paidphone subs. These examples suggest that the industry’s growthis able to

absorb Xfinity’s entry without disrupting the incumbents. Additionally,all the incumbents have recently stated that

their ARPUs should trendhigher and that they are pleased withthe trajectoryof their top-line.

Disconnects

Postpaid (thousands) 1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17 4Q17 1Q18

AT&T Mobility 2,560 2,257 2,425 2,687 2,629 2,355 2,475 2,594 2,491

Sprint 1,596 1,448 1,419 1,578 1,661 1,573 1,541 1,526 1,364

T-Mobile 1,285 1,264 1,324 1,299 1,235 1,263 1,313 1,367 1,107

Verizon 3,098 3,051 3,398 3,611 3,797 3,088 3,205 3,324 3,495

Total 8,539 8,020 8,566 9,175 9,321 8,280 8,534 8,810 8,457

YoY Change % 9.2% 3.2% -0.4% -4.0% -9.3%

6. All rights reserved,InflectionCapital Management, LLC

Fear-2: AT&T is getting Time Warner and they will give away HBO to its wireless subscribers.

AT&T has been doing this since September 2017. As shown in the table below, the gross adds are worse during

Q4’17 and Q1’18 than when they didn’t offer HBO for free. Thus, free HBO appears to not be an effective strategy

for gaining more gross adds.

Fear-3: The 5G build-out is going to cost TMUS more than it expects, resulting in a FCF shortfall and a

decline in its enterprise value, whacking equity ownershard.

Giventhat TMUS’management has provided a budget and plan, having such a fear is like being of the opinion

that management is incompetent inthese types of projections.There is no such basis for such an opinion, but if

that’s one’s view, we would expect that one to have no interest inTMUS as an investment.

Fear-4: The stock is in deal-limbo and that deal is not likely to gain regulatory approval, so why

bother? It’s dead money at best and a likely underperformer in a robust economy where earnings

and estimates are rising for the S&P 500.

This is the equivalent of saying, “I can foresee what President Trump will do and he never surprises me.” We

ourselves have no such ability.We have also observedthat since the 2H’16, the unexpected oftenhappens and

that the conventional wisdom is frequentlywrong. Should President Trump implode, explode,or just die one day,

then we would be more willing to embrace the conventional regulatoryopinions about the deal probability.Until

that implosion/explosion,we are going to be rational and acknowledge that we have no basis for judging what

chances a TMUS+Sprint merger has,or its timing.Based upon our conversations withsell-side analysts,most of Wall

Street thinks the deal doesn’t have a chance. The sell-off post the deal announcement also supports that view.

Consequently, there is no optionvalue in TMUS’ stock for deal approval or synergies. Saiddifferently,that very

valuable outcome/option($55-$95/share)is currentlybeing offeredfor $0.00. If the deal doesn’t happen, the

optioninvestor doesn’t loose capital.If the deal does, they quickly make a lot.We like these situations.If you don’t,

go chase earnings momentum and revisions elsewhere.Also, would you please tell us if President Trump is going to

be re-electedin2020?

Fear-5: It’s too early to play 5G. Consumer adoption isn’t really going to start until 2020-2021 and so

we aren’t going to see strong 5G use cases or applications until 2021-2022. Thus, there are no real 5G

catalysts in 2018-2019.

This is a common naysayer complaint. If you believe our modeling, the end-value is there.Investors are going to

accrue that value.An investor couldbe there for the entire journey, or just the front, middle or rear. If the accrued

value potential is attractive,whycomplicate it and risk it,versus putting the time understanding and

dimensionalizing the end-value.If you put the opportunityaside, you are likelyto loose sight of the path and before

you turn your sight back on it,TMUS will be moving and you will have “missedit.” If the opportunityis as large as we

model, Wall Street is likelyto view it as a “sky-high opportunity” which typicallyresults inmaterial multiple expansion.

That higher valuationmultiple willmake a “miss-er” say, “Well I’mnot going to chase and buy at these levels.I’ll

wait for it to come back in.” They seldom do. Catching S-curve opportunities inthe front-endis where most of the

money is made. In the Catalyst Calendar sectionbelow,we project whenmaterial data points are likelyto appear.

In creating that section,it was clear to us that the catalysts are quicklyapproaching. Moreover,there are too many

events going on in the industryfor a generalist investor to keep track of.If you are a TMT specialist,totallyfocused

on 5G, then “God bless you.” If you are a generalist,like the end-point and our arguments, just make your life easier

by buying now. Then spend your time affirming and confirming that the industry and TMUS are traveling to our

projected end-points.

Volumes in thousands

3/31/16 6/30/16 9/30/16 12/31/16 3/31/17 6/30/17 9/30/17 12/31/17 3/31/18

Wireless Subscribers and Connections

Postpaid 65,739 65,772 65,767 66,100 65,692 65,570 65,388 65,683 65,489

Postpaid Net Adds 15 115 60 424 (282) (28) (46) 371 (64)

Postpaid Phone Churn 0.96% 0.84% 0.90% 0.98% 0.90% 0.79% 0.84% 0.89% 0.84%

Estimated Consumer Postpaid Disconnects 1,911 1,671 1,792 1,953 1,801 1,569 1,666 1,761 1,669

Estimated Gross Adds 1,926 2,377 2,132 1,605

AT&T Consumer Mobility

Three Months Ended

7. All rights reserved,InflectionCapital Management, LLC

In the above section,we review the five primaryfears or push-backs to buying TMUS today and at these levels. We argue

that these fears draw too much from the past, are reliant onthe unlikely scenario that T-Mobile management’s is

incompetent,and miss-caste the odds of outcomes.We acknowledge that the wireless industryand 5G are incredibly

complicatedand that the 5G transitionincreases uncertaintyas to the outcomes.However,all of this is what creates the

hugely favorable reward-to-risk at TMUS of $212 to $52. This is a potential “career making” opportunityof an investment.

TMUS’ Stand-alone 5G Plan

T-Mobile expects to have 30 cities live with5Gin 2019 and be nationwide before 2020.First adopters will needa

5G/4G phone, have to accept the partial 5G coverage and pass on the 5G battery-life savings.Giventhat these

phones will work withboth networks,that will allow a more secure QOS should there be initial 5Gservice issues.Such

a strategywill emboldenearlyadopters in 1H’19. Giventhat the launch cities are large metros like NY, LA, & LV,one

should expect that the press and Wall Street will quicklybe writing,analyzing, and valuing the service.Thus, the Q1

citylaunch is going to be a material catalyst.

T-Mobile is using its new 600 MHz spectrum and its millimeter wave (mmW)spectrum (30-300 GHz)for its 5G network.

The 600 spectrumis unencumbered by other uses (i.e. it’s not taking capacity froma network currentlyin use) and

it’s nationwide. (A good summary of the 600 MHz is attached below.) The more capital-intensive,higher capacity

mmW is for major metros where T-Mobile is now installing equipment.

Source:https://www.rcrwireless.com/20160406/analyst-angle/analyst-angle-600-mhz-spectrum-will-good-will-not-tag9

By Iain Gillott, President and Founder,iGR on APRIL 6, 2016

The 600 MHz auction is importantfor several reasons,notleastof which is that this is likely to be the lastauction in the U.S.

for some time and certainlythe last low band auction.The next auction will likely be for high band spectrum for “5G” services,

such as the 3.5 GHz band.Note that no such auctions are scheduled and no spectrum has been finalized;itis therefore likely

to be years before the next auctions.Chances to acquire licensed spectrum do notcome along very often, and for this reason,

operators usuallyjump atthe chance to acquire it (lastyear’s AWS-3 auctions being a good example).

Obviously, at this pointwe have no idea which operators will be successful acquiring spectrum,how much they will have to

pay or which regions theywill get licenses for.The only certainty is that those not participating (notablySprint) will not win

anything. You have to play to win.

So a little bit of physics.The higher the frequency of the radio signal,the less distance itcan travel through the air. Conversely,

the lower the frequency, the further it goes.This also applies to buildings,windows,trees,etc.; lower frequency signals g o

through more stuff. As an example,think aboutyour favorite radio station (mine is 90.5 MHz). You can more than likely get

that station miles from the transmitter,inside a building or in an underground garage.Now compare thatto your Wi -Fi at home

or in the office that is either 2.4 GHz or 5 GHz. Your Wi-Fi probablygoes a few hundred yards at best.(In our case,it barely

goes outside the house due to the type of windows we have.)

For small cells,mobile operators generallylike higher frequencies because itis easier to control the propagation and keep the

cell “small.” More small cells over a given area means more capacitythan a single cell.So when an operator needs to

increase the capacity in a given area, they usuallywill firstadd sectors to the macrocells and then try and put in small ce lls of

one type or another.

The original cellular systems in the U.S. used 850 MHz spectrum.LTE was originallylaunched with 700 MHz spectrum.

(AT&T, Verizon Wireless and T-Mobile all have 700 MHz bands in use.) These lower bands are greatfor covering wide areas

with signals and they will generallygo into buildings well.But,the fact the signals propagate well also means theyare harder

to control; deploying small cells with 700 MHz is very difficultand is the reason mostoperators are using 1.9 GHz or 1.7/2.1

GHz bands for this.Sprint uses its 2.5 GHz band.

Consider a macrocell using the 700 MHz band.To cover the same area with 1.9 GHz cells takes about2.5 cells.At 2.5 GHz,

about3.7 cells are required to cover the same area.This means 3.7 more infrastructure,towers/locations,etc. And of course ,

3.7-times as much capacityif the same amountofspectrum is used.

600 MHz is likely to need about0.8 cells to cover the same area as a 700 MHz cell. So 600 MHz will be excellent for providin g

coverage over a given area. And, as we said,the 600 MHz signal is likelyto penetrate mostbuildings – greatfor indoor

coverage. So providing mobile video over a given area or in-building will suit600 MHz well.

But, 600 MHz will not be good for small cells,as operators need higher bands for this.So 600 MHz will not enable the

operators to increase the capacity densityof their networks.

Ideally, an operator will have a selection oflow band (600 MHz, 700 MHz and 850 MHz) spectrum to provide wide coverage

and in-building coverage together with higher bands (1.9 GHz, 1.7/2.1 GHz, etc.) to provide capacity at given locations with

small cells,including in-building distributed antenna systems.The trick is in deploying the bands efficientlyand economicallyto

meetthe marketneeds.

Much has been said about5G networks being used to provide higher bandwidth and network speeds and this will take more

small cells.So 600 MHz should notbe thoughtof as “5G” spectrum – it is not. It will be used for LTE-Advanced networks (and

subsequentreleases),while the new 5G IMT-2020 networks will likelyuse higher bands,such as 3.5 GHz. But, 600 MHz still

8. All rights reserved,InflectionCapital Management, LLC

has value – all licensed spectrum has value.The mobile operators should never turn down the opportunity to acquire new

spectrum.600 MHz will be great for providing bandwidth over a wide area and in hard-to-reach places.

Map of TMUS 600 MHz spectrumacquired for $8B

9. All rights reserved,InflectionCapital Management, LLC

T-Mobile’s and Sprint’s Joint 5G Plan

The merger and 5G are intimatelyintertwined. The merger allows the companies to create a 5G network that is

significantlymore spectrum efficient,that significantlylowers the deployment expense, that allows a significantly

faster deployment speed, and that allows for a more compelling regulatoryapproval argument. Strategically,it

allows the companies to deploy nationwide significantly earlier thanAT&T and Verizon.It allows them to get a

significantlybetter service into the market before cable builds a significant wireless business. It allows themthe

credibilityto argue that they are bring 450 Mbps data speeds to the 50%of the US that has only one broadband

optionand that brings broadband to regions without it.

T-Mobile’s 600 MHz is going to be the nationwide 5G network. (600 MHz is a lower frequency, so long propagation

and strong penetration.) They will use the mmW spectrum(30 – 300 GHz) to builda high-capacity, high-speed

networks in urban geographies. mmW can penetrate rain, leaves,windows,and walls.But it can’t travel far,and

thus, its veryexpensive to deploygiventhe need for a lot of antennas.

QCOM Slide (May 2018)

Sprint’s mid-band (2.5 GHz) spectrum offers good propagation

characteristics andsupports wide-coverage with fewer base

stations.Sprint’s 2.5 is also the backbone for supporting their

current LTE service andso there is a challenge to redirecting

capacityfrom its 4G service for new 5G service. Consequently,

a merger allows Sprint’s 4G customers to obtaincoverage on T-

Mobile’s network and to transitionmore of the 2.5 faster to 5G.

This means getting to 450 Mps speeds for the entire customer

base by 2024.As a stand-alone,T-Mobile’s projected5G data

speeds are a slower 100-200 Mbps.

The merged companies will also deploy fixed-wireless

broadband at over 1Gps speeds as a cable replacement

(similar to Verizon’s and AT&T’s plans). The mergers also allows

them to do fixed-wireless onnationwide (market-by-market)

leveraging network assets that theyhave for wireless. (Both

companies have not discusseddoing so as stand-alones.)

Small mmW antennas

t hat need t o be

added all over in cit y

10. All rights reserved,InflectionCapital Management, LLC

FCC and DOJ Approval

As mentionedearlier,we believe that anapproval is viewed as extremelyunlikelyby Wall Street. The two reviewing

agencies are the FCC and the DOJ. We touchon the FCC and then the DOJ.

TMUS/S management is sticking to a 1H’19 approval based above three criteria:1)the FCC will rule that the US

“wireless market” is an antiquateddefinition and will transitionto define the market as “communicationand video

services,” 2)aggressivelydeploying 5G mobile broadband on a nationwide basis and that in turn fosters

technologyand business innovationwhichsolidifies the US as a 5G leader, and 3) the merger stimulates job

creation,investment,and GDP growth. Below, we address point-1.

Wall Street analyst primary reasonfor stating that the deal has a slimchance is that the FCC is quite proud of the US

wireless industry’s consumer value,service, and coverage.Those attributes are the consequence of the industry’s

high competitive intensity.US consumers generallyhave four choices for nationwide service. That intensityunleased

strong investment inLTEand 4G, unlimited service packaging,and little price inflation. As a consequence, analysts

argue that the FCC is unlikelyto disrupt an industry structure that achievedthat win.

TMUS/S is likelyto argue that while the FCC did secure a consumer-friendlywireless industry,it has been far less

successful instimulating competition andinnovationin broadband and paid-video services.TMUS/S will argue that

should the FCC define the market as to be inclusive of a combinationof these markets (complements of 5G) that

the merger will leadto a material increase in competition.It wouldaccelerate the deployment of 5G and bring

competitionto a cable broadband monopoly and a lethargic paid-TV industry. More specifically,TMUS/S will make

the case that the merger would moderate Comcast’s grip on its consumers. While video competitionand

innovation are unquestionablyimproving (YouTube-TV, Hulu-TV, Sling,etc.), no such improvement is happening in

broadband. Google Fiber has stopped. AT&T is laying new fiber only because they were forced to by the FCC to

get the DirecTV deal approved. AT&T and Verizonare building a fixedwireless broadband service,but that is going

to be market-by-market,avoiding regions that are remote or economicallystrained.

In exchange for granting a TMUS+S approval,FCC can make it conditional upon setting a price limit inflator to

wireless and a cap on the premium for 5G wireless service. They will also know that should TMUS+S be approved,

Verizonand AT&T will rapidly increase their 5G nationwide wireless plans.That would be pro-consumer, good for the

economy, and good for US industrial policy.

The prepaid market is a special considerationgiventhat Sprint andT-Mobile dominant this segment (54%combined

share), including brands such as MetroPCS,Boost Mobile,and VirginMobile.To win regulatoryapproval,TMUS/S

would likelyneed to spin-off or sell one or more of those brands. A sale would likelybe slightlydilutive to earnings.

The DOJ will relyon the Clayton Act.Section-7 of the Clayton Act is prettyclear and well understood. Section-7

states:If competition mightbe lessened in any line of commerce inany section of the country, the merger is

unlawful. That a merger might produce beneficial effects isnot a defense. We are not lawyers and do not have any

insight into TMUS/S’legal strategy.Consequently, we do not have a view onDOJ approval. However,we do ask

ourselves whyis TMUS/S willing to spend$100m+ on legal fees and change their capital returnstory(thus

undermining their stock price for 12 months+)if it is so clear cut? We trust this management and believe that they

think their DOJ approval chances are more than a zero.

AT&T & TWX Case

The Government argued that the merger would lessencompetitioninvideo programming and distribution.Thus, we

know that theyare concerned about competitioninthese markets.TMUS+S are going to bring new national

competitioninto the video market wholesaling Sling,Hulu-TV,or Google-TV over the merged company’s

distribution.This puts the Government in the uncomfortable positionof saying that they were concerned about

reduced competitioninthe case of AT&T+TWX,but not interestedin the increasedcompetitionthat TMUS+S would

bring to the consumer.

Also of note is that Judge Leon focused on AT&T+TWXbeing a vertical merger.TMUS+S is a horizontal merger which

limits drawing conclusions fromthe ruling to inform about the statutes onTMUS+S.

11. All rights reserved,InflectionCapital Management, LLC

5G Use Cases & TAMS

No, we are not going to opine about telemedicine,IoT,smart cities,autonomous vehicles andthe like. We are

going to focus on the two things that consumer care about--latencyand speed, especiallyin the context of the

cloud. This is because 5G is going to allow processing and storage to move to the cloud from the handset. This will

be particularlyacute in the mid-tier of the handset market as 5G will allow these phones will have significantlyless

commentary and cost.Offsetting some of that cost will be cloud service costs paidto the service provider bythe

subscriber.Saiddifferently,the economic rents for mobile service willmove to the provider fromthe handset and

componentry manufacturers. There will still be a $1K iPhone (and above) but the iPhone will likelylose the middle-

range of the market.5G should also be a large opportunityfor Google and Android as there will be significantly

more in cloud services.At the moment, there isn’t enough informationto sort out how the economic rent winnings

get split betweenthe service providers,Google,and others. However,it’s clear to us that the providers will be net

benefiters and iPhone and Samsung will be net losers.Notable is that we wrote “iPhone” and not “Apple.”

We didn’t write Apple, because 5G is likelyto yield Tony Stark Toys for Everyone. Apple is likelyto sell a lot of those

toys. There are going to be a lot of toys (watches,eyewear, etc.) because there isn’t going to be a lot of weight,

volume and componentry in those devices because the large memory and processing will be done in the cloud.

Those toys are going to have a service fee of $5-$10/mo along withother associated cloudusage costs. 5G devices

also have significantlylower power requirements (the current iWatchbattery-life goes up by 4,900x) which allows for

much smaller,lighter,and cheaper batteries. These toys’prices are going to be substantiallylower thanwhat these

heavier,clunker,slower toys currentlysell at. That is going to result insubstantiallyhigher adoptionof Tony Stark Toys.

12. All rights reserved,InflectionCapital Management, LLC

Return of Investment from the 5G Deployment

Below we model the industry’s returnfor its $200B 5Ginvestment (the various estimates center aroundthe $200B,but

those predate the TMUS+S news).In their announcement, TMUS+S saidthat theywould spend $40B. We have no

reason to be believe that AT&T’s or Verizon’s individual investments shouldnot be of similar magnitude;this sums to

$120B.We have no way to compare the plans of $40B to the assumptions behind the $200B. Consequently, we go

withthe more conservative $200B.

The minimum IRR that the industry should be willing to accept on such an investment is 11%.That is the plug that we

use to resolve what the industry’s assumptions are for the incremental profits fromthe 5-G investment.We model

out three:1) an incremental $7.50/mo service charge for 5G, 2) $5.00/mo in service revenue for Tony Stark Toys, and

3) fixed wireless residential broadbandfor $50/mo. The fixedwireless product is AT&T and Verizon’s 5G introduction

into the market. For this service,theylay fiber into high-prospect neighborhoods and then provide 1Gspeed

broadband to households via a 5G network antenna that works withina 2K foot radius. As such, it’s reallylike super-

charged Wi-Fi.There is no trenching unto homes and there is no truck-roll to deliver andinstall equipment.

Obviously,the cable incumbents are going to fight back. However,Comcasts reportedbroadband ARPU is $50/mo

and its unbundled price is $75+.Xfinitybroadband continues to be plagued by service outages,slow upload

speeds, and shared-line slowdowns. And so, Xfinitybroadband (as is)will likelybe an inferior product.What

happens if Comcast plays the price card and drops its price to $40/mo? If the wireless fixedwireless price is only

$40/mo. and keeping all the other assumptions consistent,the IRRfalls to 10.0%. That’s a significant reduction,but

not a thesis changer.

2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

5G Mobile

Total Postpaid Wireless Subs 260,100 265,302 270,608 276,020 281,541 287,171 292,915 298,773 304,749 310,844 317,060 323,402

5G Subscribers 3,000 15,000 30,000 45,000 70,000 130,000 190,000 250,000 304,749 310,844 317,060 323,402

Penetration 1.2% 5.7% 11.1% 16.3% 24.9% 45.3% 64.9% 83.7% 100.0% 100.0% 100.0% 100.0%

ARPU lift $7.50 $7.65 $7.80 $7.96 $8.12 $8.28 $8.45 $8.62 $8.79 $8.96 $9.14 $9.33

Revenue $135 $826 $2,107 $3,582 $5,602 $9,937 $16,217 $22,744 $29,249 $33,106 $34,444 $35,835

NOPAT $85 $522 $1,332 $2,264 $3,540 $6,280 $10,249 $14,374 $18,485 $20,923 $21,768 $22,648

5G Wireless Accessories

Penetration of 5G Subs 50.0% 50.0% 50.0% 50.0% 50.0% 50.0% 50.0% 50.0% 50.0% 50.0% 50.0% 50.0%

5G Subscribers 1,500 7,500 15,000 22,500 35,000 65,000 95,000 125,000 152,374 155,422 158,530 161,701

ARPU lift $5.00 $5.25 $5.51 $5.79 $6.08 $6.38 $6.70 $7.04 $7.39 $7.76 $8.14 $8.55

Revenue $45 $284 $744 $1,302 $2,097 $3,829 $6,432 $9,287 $12,294 $14,325 $15,342 $16,431

NOPAT $36 $224 $588 $1,029 $1,656 $3,025 $5,082 $7,337 $9,712 $11,317 $12,120 $12,981

Fixed Broadband

Total Broadband Subscribers 97,000 98,940 100,919 102,937 104,996 107,096 109,238 111,423 113,651 115,924 118,242 120,607

5G Subscribers 1,000 5,000 10,000 15,000 17,400 19,890 21,848 22,285 22,730 23,185 23,648 24,121

Penetration 1.0% 5.1% 9.9% 14.6% 16.6% 18.6% 20.0% 20.0% 20.0% 20.0% 20.0% 20.0%

ARPU lift $50.00 $50.00 $50.00 $50.00 $50.00 $50.00 $50.00 $50.00 $50.00 $50.00 $50.00 $50.00

Revenue $300 $1,800 $4,500 $7,500 $9,720 $11,187 $12,521 $13,240 $13,504 $13,774 $14,050 $14,331

NOPAT $166 $995 $2,489 $4,148 $5,375 $6,186 $6,924 $7,322 $7,468 $7,617 $7,770 $7,925

New Revenue Pools

Revenue $50 $100 $200 $400 $800 $1,600 $3,200 $6,400 $12,800 $25,600 $35,000 $45,000

NOPAT $28 $55 $111 $221 $442 $885 $1,770 $3,539 $7,078 $14,157 $19,355 $24,885

Operator Investment -$20,000 -$25,000 -$30,000 -$30,000 -$30,000 -$30,000 -$15,000 -$10,000

Sum -$190,000

Cash Flow -$19,686 -$23,203 -$25,481 -$22,339 -$18,986 -$13,624 $9,024 $22,572 $42,744 $54,014 $61,013 $68,438

Discount Factor 0.90 0.81 0.72 0.65 0.58 0.52 0.47 0.42 0.38 0.34 0.34

Discounted Cash Flow -$19,686 -$20,820 -$20,515 -$16,138 -$12,307 -$7,924 $4,710 $10,570 $17,960 $20,364 $20,640 $23,151

Sum $4

IRR 11.4%

13. All rights reserved,InflectionCapital Management, LLC

Impact from Use Cases on TMUS’ Financials

Below we layer in the industry5G storyonto T-Mobile’s financials.The subscriber estimates shownin the first line are

ICM’s estimates basedupon the company’s and the industry’s current momentum, i.e. steady-state.We then

assume that T-Mobile’s lead in 5G allows it to take increasing share from the industry. This is shown in the middle

section.We do not assume anything for fixed-wireless as T-Mobile as a stand-alone company has articulatedno

plan for a fixedresidential. While 5Gwill spur a significant increase indata consumption (secondfigure), the

technologyalso lowers the cost by 10X. And so, on an unlimitedplan with usage going up 10X-20X, cost follow will a

lower trajectory.

TMUS Stand-Alone 2018E 2019E 2020E 2021E 2022E 2023E 2024E Comment

Postpaid

Subscribers 41,293 45,391 49,079 52,398 55,386 58,074 60,494 This is our base forecast based upon current momentum

% yoy growth 8.3% 9.9% 8.1% 6.8% 5.7% 4.9% 4.2%

5G Subs

Converted 908 3,177 6,288 9,969 16,261 27,222 This is the conversion of TMUS' current customer-base

% of Base 2% 7% 12% 18% 28% 45%

Non-TMUS Post Paid 214,957 219,256 223,641 228,114 232,676 237,330 242,076 This is the industry ex-TMUS

New 5G Subs 1.0% 3.0% 5.0% 5.5% 6.0% 6.5%

New 5G Subs to TMUS 2,193 6,709 11,406 12,797 14,240 15,735 This is additional share gains for being 1st to market nation-wide

Non-5G TMUS Subs 41,293 44,483 45,902 46,110 45,416 41,813 33,272

5G Subs 0 3,100 9,887 17,693 22,767 30,501 42,957

Total Postpaid Subs 41,293 47,584 55,788 63,804 68,183 72,314 76,229

Non-5G ARPU $43.96 $44.40 $44.84 $45.29 $45.74 $46.20 $46.66 Guidance is for flat. We assume slightly more

5G ARPU $51.46 $51.90 $52.34 $52.79 $53.24 $53.70 $54.16 We assume that 5G gets a $5/mo premium

Non-5G Service Revenue $20,948 $22,850 $24,318 $25,003 $25,120 $24,180 $21,022

5G Service Revenue $0 $965 $4,079 $8,736 $12,925 $17,163 $23,872

Phone Postpaid Service Revenue $20,948 $23,815 $28,396 $33,739 $38,045 $41,343 $44,893

Other Devices

Watch/Eyewear/etc. 5G Subs 4,943 8,847 11,383 15,250 21,479

Other Device Gross Profit/mo $5.00 $5.00 $5.00 $5.00 $5.00

Other Device Postpaid Rev/Profits $148 $414 $607 $799 $1,102

14. All rights reserved,InflectionCapital Management, LLC

TMUS & Sprint Synergies

Shown below is TMUS/S’slide on the projected cost synergies.Of the $6B/year total,$4B of that comes from lower

expense to tower companies, equipment providers,and back-hall providers.$1B comes out of marketing and

competing retail stores.The final $1B comes from redundant IT, billing,and corporate spend. The $43B NPV figure

incorporates a 8% WACC, little innear-term taxes,and a 21% long-termtax rate.

We have no basis to challenge any of TMUS/S’ synergy and NPV estimates.Moreover,T-Mobile was able to exceed

its synergy target fromMetroPCS by 40% and T-Mobile’s management guides to exceed. Consequently, we provide

a second scenario of $8.5/year in annual synergies, which has an NPV of $69B. Currently,the $43B number is now

only slightlyless than TMUS’$4pB market cap. That tells us that Wall Street sees no chance of a deal.

TMUS+Sprint Synergies

Shares Pre Post

TMUS 862 862

Sprint 4011 411

Conversion Ratio 9.75

Total Shares 1,273

Stated Synergy $43,000

Modeled Synergy $68,800

Per Share $54

$8.5B in annual $76

synergies vs. $6B

15. All rights reserved,InflectionCapital Management, LLC

TMUS/S Integration Risks

Without question,TMUS+S is a big merger and there is integrationrisk.Whenasked about how they will execute the

integration,T-Mobile’s management answers, “one bite at a time.” This means that they will do one market at a

time.And so, on a metro-basis,the New York and LA migrations withMetroPCS and T-Mobile are comparable to

TMUS+S.Also, the MetroPCS requiredmerging two different network technologies (CDMA & GSM) into one. With

Sprint,T-Mobile is going to push Sprint subscribers onto T-Mobile network and thenre-positionSprint’s network for 5G.

Additionally,two-thirds of Sprint’s customer handsets (iPhone & Samsung) are already compatible withT-Mobile’s

network.A significant portionof the remaining one-thirdcan be made compatible witha remote software update.

TMUS’ Stand-alone Business, Financials, & Value

Shown below is ICM’s estimates for T-Mobile stand-alone.One critical assumptionof this model is that service

revenue can grow from $32B to $58B withequipment subsidies only growing from $1.5B to $2.3B. The basis for that

view is the lower 5G handset costs and collecting a portionof the associatedoffsetting cloudrevenue.The

summation of the assumptions is a WAG;consequently, this is an expense line that has a wide range of possible

outcomes.Additionally, our estimated start-up (op-ex)costs for 5G are a WAG.

TMUS Stand-Alone 2018E 2019E 2020E 2021E 2022E 2023E 2024E Comment

Total Postpaid Service Revenue $20,948 $23,768 $28,350 $33,739 $38,045 $41,343 $44,893

Prepaid revenues $9,857 $10,157 $10,457 $10,757 $11,057 $11,357 $11,657 FactSet Consensus

Wholesale $1,048 $1,048 $1,048 $1,048 $1,048 $1,048 $1,048

Roaming and other $351 $351 $351 $351 $351 $351 $351

Service revenues $32,205 $35,325 $40,206 $45,895 $50,501 $54,099 $57,950

Other Revenue $1,182 $1,267 $1,271 $1,284 $1,297 $1,310 $1,323 FactSet Consensus

Equipment Revenue $9,803 $11,296 $13,244 $14,390 $14,608 $14,719 $14,740

2018E 2019E 2020E 2021E 2022E 2023E 2024E

Total Revenues $42,008 $46,621 $53,450 $60,285 $65,110 $68,818 $72,689

Equipment Expense $11,303 $13,025 $15,271 $16,591 $16,844 $16,971 $16,995 Expense per device comes down due to cloud transition

Equipment EBIT -$1,500 -$1,728 -$2,027 -$2,202 -$2,235 -$2,252 -$2,255

Total Subs 76,868 83,805 92,527 100,956 105,666 110,062 114,188

Non-5G Cost of Service $7.08 $7.08 $7.08 $7.08 $7.08 $7.08 $7.08

5G Cost of Service $8.08 $7.88 $7.69 $7.49 $7.31 $7.12 $6.94 At scale 5G is to be 10X cheeper per bit

Non-5G Cost of Service $6,535 $6,829 $7,495 $8,224 $8,782 $9,170 $9,532

5G Cost of Service $0 $147 $599 $1,240 $1,774 $2,277 $3,061

Total Cost of Service $6,535 $6,976 $8,094 $9,464 $10,556 $11,446 $12,593

SG&A % of Service Revenue 38.4% 37.0% 36.0% 35.0% 34.0% 33.0% 32.0%

Service SG&A $12,354 $13,070 $14,474 $16,063 $17,170 $17,853 $18,544

per sub/mo $13.39 $13.56 $13.68 $13.84 $13.85 $13.79 $13.78 Assume modest efficiencies

Service EBITDA $13,316 $15,278 $17,638 $20,368 $22,775 $24,800 $26,813

5G Start-up Costs $250 $750 $1,000 $1,000 WAG

Total EBITDA $12,998 $14,567 $16,132 $18,450 $20,836 $23,857 $25,880

16. All rights reserved,InflectionCapital Management, LLC

Next,we layer our EBITDA estimates into a cash-flow and valuation model.(T-Mobile has no cash tax expense until

2025.) We assume that 75%of the FCF is used to de-lever.The analysis outputs prospective stock prices,one for 6.5X

EBITDA and a second for 8.5X. The stock currentlytrades at 6.5X NTM. However,should the company execute on

the 5G plan that we describe above, 8.5X is more appropriate givenfaster growthand larger TAMS.

TMUS Stand-Alone 2018E 2019E 2020E 2021E 2022E 2023E

Total EBITDA $12,998 $14,583 $16,187 $18,538 $20,926 $23,926

YoY $ Ch $1,585 $1,604 $2,351 $2,388 $3,000

Interest Costs $1,700 $1,600 $1,500 $1,400 $1,300 $1,200

Cash Taxes $0 $0 $0 $0 $0 $0

Cap Ex $5,300 $5,400 $7,700 $7,700 $7,700 $6,200

Working Capital -$900 -$990 -$1,089 -$1,198 -$1,318 -$1,449

Free Cash Flow $5,098 $6,593 $5,898 $8,240 $10,609 $15,076

Debt Paydown $1,500 $4,945 $4,424 $6,180 $7,956 $11,307

Net Debt $29,000 $24,055 $19,632 $13,452 $5,495 -$5,812

Leverage 2.2 x 1.6 x 1.2 x 0.7 x 0.3 x

EV/EBITDA 6.5 x 6.5 x 6.5 x 6.5 x 6.5 x 6.5 x

Enterprise Value $84,487 $94,790 $105,216 $120,497 $136,021 $155,518

Equity Value $55,487 $70,735 $85,584 $107,046 $130,526 $161,330

Per Share $64 $81 $98 $123 $150 $185

EV/EBITDA 8.5 x 8.5 x 8.5 x 8.5 x 8.5 x 8.5 x

Per Share $94 $115 $136 $166 $198 $240

17. All rights reserved,InflectionCapital Management, LLC

2018, ’19, & ’20 Catalyst Calendar

5G Road Map

Q3'18

QCOM, Huawei, Samsung, Ericsson, and Nokia news

Q4'18

VZ & AT&T Updates on 5G fixed-broadband roll-out

TMUS Announces 30 cities for 2019 5G launch

Huawei starts to sell 5G chips and phones

Huawei and China mobile start 5G trials in 5 cities

Q1'19

5G Handset Annoucements

KT nationwide 5G mobile launch in Korea

World Radio Congress confirms 5G standards

CES and Mobile World Congress

Q2'19

TMUS starts 30 deployment: NYC, Dallas, SF, LA, LV

Media and Wall Street reviews

VZ & AT&T roll-out of 5G fixed broadband

Sprint launches 5G mobile service

Q3'19

Q4'19

TMUS nationwide mobile 5G launch

VZ & AT&T annouce nationalwide 5G launch date

China Mobile launch

1H'20

VZ & AT&T nationwide 5G mobile launch

18. All rights reserved,InflectionCapital Management, LLC

Catalyst Calendar + Enterprise Expansion + Stock Price Outcome

The first table below uses FactSet consensus at 6.5Xto projectedexpectedTMUS stock prices shouldthe company

hit current expectations.This is shown in the blue-highlight.Below that are rows of values for each of the

incremental wins discussedabove. These are summed and presented in the green-highlight along withthe

annualized returnfrom6.2.2018. The circled 78%figure is the annualized returnfrom 6.2.2018 to 12.30.2020 should

the 5G plan work, the stock trade at 8.5X, TMUS+S be approvedand the synergy guidance be increased to $8.5B.

Based upon the timeline above,we would expect most of the upside from the 5G and merger stories to be

reflectedinTMUS price by the end of 2020.

The subsequent table show price outcomes for less favorable events.These include:

✓ Negative consensus revisions of -7.5%.

✓ The valuationcompressing to 5.5X.

✓ Only 50% of the 5G scenario

✓ And no merger.

12/31/2018 12/31/2019 12/30/2020 12/30/2021 12/30/2022 12/30/2023

Hitting Consensus

EBITDA-NTM $12,780 $13,418 $14,123 $14,823 $15,523 $16,223

EV/EBITDA 6.5 x 6.5 x 6.5 x 6.5 x 6.5 x 6.5 x

Enterprise Value $83,070 $87,217 $91,800 $96,350 $100,900 $105,450

Net Debt $29,000 $26,212 $22,841 $18,919 $14,407 $9,679

FCF $3,718 $4,494 $5,230 $6,016 $6,304 $6,704

Debt Paydown $2,789 $3,371 $3,923 $4,512 $4,728 $5,028

Equity Value $54,070 $61,006 $68,959 $77,431 $86,493 $95,771

per Share $62 $70 $79 $89 $99 $110

6X 5G Scenario $98 $123 $150 $185 $215

8X 5G Scenario $136 $166 $198 $240 $274

$6B Sprint Synergies $54 $54 $54 $54 $54

$8.5B in Synergies $76 $76 $76 $76 $76

8X + Synergies $212 $242 $274 $316 $350

Annualized 140% 78% 57% 46% 39%

return from $56.87

on 6.2.2018

19. All rights reserved,InflectionCapital Management, LLC

Other Risk Factors

Amazon: Does Amazon buy DISH’s spectrumand launch its own competing mobile network?

12/31/2018 12/31/2019 12/30/2020 12/30/2021 12/30/2022 12/30/2023

Consensus high by 7.5%

EBITDA-NTM $11,822 $12,412 $13,064 $13,711 $14,359 $15,006

EV/EBITDA 5.5 x 5.5 x 5.5 x 5.5 x 5.5 x 5.5 x

Enterprise Value $65,018 $68,264 $71,851 $75,412 $78,973 $82,535

Net Debt $29,000 $26,769 $24,073 $20,935 $17,325 $13,543

FCF (80% of Ce) $2,974 $3,595 $4,184 $4,813 $5,043 $5,363

Debt Paydown $2,231 $2,696 $3,138 $3,610 $3,782 $4,022

Equity Value $36,018 $41,495 $47,778 $54,477 $61,648 $68,992

per Share $41 $48 $55 $63 $71 $79

50% of 5G Scenario $1 $6 $10 $18 $27 $39

8X 5G Scenario $0 $0 $0 $0 $0 $0

Sprint Synergies $0 $0 $0 $0 $0 $0

Total $42 $53 $65 $81 $98 $119

Annualized -4% 6% 11% 13% 14%

return from $56.87

on 6.2.2018