Recommended

Recommended

More Related Content

Similar to Levis at Wal-Mart DARDEN叁 UVA-M-0711 BUSINESS PUBLISHI.docx

Similar to Levis at Wal-Mart DARDEN叁 UVA-M-0711 BUSINESS PUBLISHI.docx (12)

More from smile790243

More from smile790243 (20)

Recently uploaded

Recently uploaded (20)

Levis at Wal-Mart DARDEN叁 UVA-M-0711 BUSINESS PUBLISHI.docx

- 1. Levi's at Wal-Mart? DARDEN叁 UVA-M-0711 BUSINESS PUBLISHING Rev. Oct. 12, 2010 UNIVERSITY: 矿VIRGINIA LEVI'S AT WAL-MART? Introduction In early 2002, Phil Marineau, CEO of Levi Strauss & Co., was thinking about whether he should direct his company to sell its product in the world's largest retail store, Wal-Mart. Levi Strauss had posted a decrease in sales for the past five years, and Marineau was eager to stem the decline. Since joining the company in 1999, Marineau had embarked on an aggressive plan to tum the company around by implementing new business strategies that included shuttering 16 North American manufacturing plants and moving the production to cheaper offshore sources. In the marketing area, Marineau had worked to revive the brand image by launching a series of new advertisements and product placements to broaden the appeal beyond the 15-to-19-year-old segment. Marineau and his management team sensed that the Levi's brand was being challenged at all points along the spectrum. The high-end segment was

- 2. dominated by trendy brands such as Tommy Hilfiger, Calvin Klein, Ralph Lauren Polo, and Diesel. In the middle segment, Levi Strauss competed with vertically integrated retailers such as the Gap, American Eagle Outfitters, and Abercrombie & Fitch. Meanwhile, retailers such as Wal- Mart, Target, JCPenney, and Sears had built their own private-label brands, offering comparable designs at significantly reduced prices. With Levi's selling in several chain and department stores, the company often found itself being used as a loss leader , with Levi's heavily discounted to the end consumer. Now Marineau and his management team had to decide whether to sell Levi's in Wal-Mart and, if so, what approach to use. The company had maintained a 10-year relationship with Wal- Mart during the 1980s and 1990s by selling them a value brand called Britannia. Wal-Mart stopped dealing with Levi Strauss in 1994, however, after a dispute in Canada, when Levi Strauss executives refused to maintain a supply of Levi's Orange Tab jeans in Wal-Mart's newly purchased Canadian stores (previously Woolco stores).'With sales of Britannia dropping drastically thereafter, Levi Strauss sold the Britannia brand to a competitor, VF Corporation, in the mid- l 990s. 1 Louis Trager, "Wal-Mart, Levi's in Battle Over Jeans," Los Angeles Daily News, September 9, 1994, B2. This case was prepared by Jordan Mitchell under the supervision of Paul W. Farris, Landmark Communications Professor of Business Administration, and Ervin Shames,

- 3. Instructor. It was written as a basis for class discussion rather than to illustrate effective or ineffective handling of an administrative situation. Copyright © 2005 by the University of Virginia Darden School Foundation, Charlottesville, VA. All rights reserved. To order cop比s, send an e-mail to sales(aldardebusinesspublishing.com. No part of this publication may be reproduced, stored in a retrieval system, used in a spreadsheet, or transmitted in any form or by any means—electronic, mechanical, photocopying, recording, or otherwise—without the permission of the Darden School Foundation. 0 Business Policy and Strategic Management -2- UVA-M-0711 As of early 2002, Levi Strauss was considering rekindling the Wal-Mart relationship by offering it a new value brand. Marineau and his management team had one central question: How should the brand be developed to preserve sales with existing customers in other channels? "There are 50 million pairs of jeans sold in discount stores," Marineau said, "and we are in the business of making pants. We would be crazy not to be looking at other Levi's brands that could be sold in those channels."2 Apparel and Jeans Market in the United States Approximately 569 million pairs of all types of jeans were sold in the United States in 2001, throughout all consumer segments, which represented an

- 4. increase of 2.7% over 2000.3 Total jeans sales were estimated to be $1 1. 7 billion4 out of a total apparel market of $166 billion. The apparel market had been steadily growing since 1998, but experienced its first decline in 2001, dropping 5.7% in dollars from the prior year.5 As an expert tracking the apparel industry stated, "2002 will be a very interesting year for the apparel industry and will see a slow road to recovery. Certain categories and consumer segments are expected to see slight increases, while most categories are expected to remain flat or decline in dollar sales."6 Exhibit 1 shows the market size of the entire apparel market and the breakdown of apparel sales by retail channel. Within the apparel market, several categories of pants existed with casual pants, dress pants, and jeans being the largest. During the late 1990s,jean sales had leveled off as consumers' tastes shifted to khaki, cargo, and other types of techno-fabric pants. By 2001, however, denim sales were rising as consumers migrated back to jeans. They were attracted by several innovations in fabric and in style. The jeans market was expected to grow by 2% to 3% in 2002. The average price for a pair of jeans hovered around the $20 mark for both men and women, with over 40% being sold (either as original or marked- down price) below $20.7 The average price of jeans had dropped over the previous 10 years due to the proliferation of off- pricing and private-label brands. One study by Cotton Incorporated showed that none of the top- 19 brands of jeans in both the women's and men's segments was

- 5. able to increase its brand premium when compared to the average price of j eans in an eight-year period. In the men's jeans segment, 11 of the 19 brands lost their premiums, and in the women's segment, 14 of the 19 brands lost their premiums over the market's average.8 The same study suggested the following to avoid losing price premiums: 2 Sarah Butler, "Levi's Rules Out Red Tab Sales to Value Sector," Drapers Record, March 30, 2002, 3. VF Corporation annual report, 2001. VF Corporation annual report, 2003. 5 "Reports 2001 U.S. Apparel Industry Down for First Time in Three Years," April 29, 2002, http://www.fashionworld.com (accessed March 3, 2005). 6 "Reports 2001 U.S. Apparel Industry Down for First Time in Three Years." 7 Scott Malone, "Retail Revolution—Levi's Considers Selling to Wal-Mart as Sales Slump," Women 's Wear Daily, January 17, 2002, I. 8 "Does Branding Combat Price Deflation?" Cotton Incorporated, Winter 2003, http://www.cottoninc.com rrextileConsumerffextileConsumerVolume31/?Pg=2 (accessed February 2, 2010). Levi's at Wal-Mart? -3- UVA-M-0711

- 6. One [solution] is for a brand to resist diluting its premium through discounting or marketing in too many different retail channels. Once consumers see a brand offered simultaneously at different channels, such as department stores and mass merchants, the ability to maintain a positive brand premium may be fatally compromised. A better strategy is to introduce a different brand name, perhaps affiliated with the original brand, but with enough independent brand identity so that consumers and retailers can differentiate products. Without differentiation, apparel products will compete largely on the basis of price. Another strategy for preserving brand premium focuses on emphasizing the non-price attributes of the brand. Attributes such as packaging, labeling, and customer service can enhance a brand image without compromising the brand's retail price.9 The largest and fastest-growing retail channel for jeans and apparel was the mass merchants channel made up of Wal-Mart, Target, Kmart, and several other smaller retailers. In January 2002, Kmart filed for bankruptcy protection after a soft holiday season and intense competition left it in a precarious financial situation.10 An industry analyst talked about the increasingly blurred lines separating the channels: Retailers will be challenged in 2002 with the need to distinguish themselves from one another. With the melding of channels, department, chain, specialty, and mass

- 7. merchant, retailers are looking for more of the same with similar merchandise. This allows the consumer to be able to switch channels for apparel shopping and seek the value experience, and fmd fashion value at lower prices. Department and specialty stores will really need to work hard to make themselves what they once were: special and different.11 Jeans Consumers Jeans were garments worn in a variety of settings—by people as diverse as manual laborers and models on the haute couture catwalks in London, Paris, and Milan. Denim jeans were considered truly egalitarian. As one academic wrote, "Jeans have the ability to conceal class distinction. When a person wears blue jeans—be it President Bill Clinton or a truck driver—the viewer is nebulous about the beholder's status."12 Styles varied as much as settings. Jeans were inextricably linked with music, given that certain styles of jeans were often part of a group's costume— tight black jeans were an essential wardrobe item for Goth dressers, no-nonsense straight-leg blue j eans were worn by country and western musicians, and oversized, baggy styles were adopted by hip-hop artists. In younger age 9 "Does Branding Combat Price Deflation?" 10 "VF Corp. sees no material impact from Kmart," Reuters, January 22, 2002. 11 "Reports 2001 U.S. Apparel Industry Down for First Time in Three Years," April 29, 2002.

- 8. 12 C. Magocsi, "The Gentrification of Blue Jeans," University of Toronto, http://www.chass.utoronto.ca 加story/material_culture/cynth/index.html (accessed February 2, 2010). Business Policy and Strategic Management -4- UVA-M-0711 groups such as 15- to-19-year-olds, it was normal to own between five and eig?t pairs of jeans of a variety of brands. Men and women over 35 had between three and five pairs of two to three brands卫 In general, men and women over 35 spent half as much on jeans each year as members of the 15-to-19-year-old group. The over-35 group purchased fewer pairs per year, and they spent less on these purchases. The 15-to-19-year-old set purchased the more expensive brand names, while consumers over 35 preferred inexpensive brands and the availability oflarger sizes and private labels. Levi Strauss & Co. History Levi Strauss was born in Buttenheim, Bavaria (modem-day Germany), in 1829, and moved to the United States in the 1847. After initially teaming up with his two half-brothers to run a dry goods business in New York, he relocated to San Francisco and started his own dry goods business in 1853. Nineteen years later, Strauss received a letter from Jacob Davis

- 9. proposing that the two of them apply for a patent on a new invention: riveted denim pants. On May 20, 1873, the two men received U.S. patent no. 139,121 for men's riveted work pants and immediately started producing what were at that time called "waist overalls." They soon realized that they were filling an important niche with their sturdy, durable garment. By around 1890, "lot number 501" was being used to designate the copper-riveted overalls later known as jeans. After the death of Levi Strauss in 1902, family members continued to run the business and developed Koveralls, one-piece play suits for children, in 1912, and Freedom-Alls, one-piece work suits for women. Around this time, the company established a relationship with Cone Mills to supply denim for key products—a relationship that still existed in 2002. During the Great Depression of the 1930s, Levi Strauss avoided layoffs by giving workers shorter workweeks or assigning nonmanufacturing activities such as maintenance and improvement of the facilities to employees. Near the end of the decade, Levi 's jeans were popularized by actor John Wayne's appearance in the movie Stagecoach—the jeans were a vital component of his wardrobe—and they became a common sight at dude ranches throughout the country. In the 1940s, Levi Strauss & Co. took the leadership position on social issues by being one of the first companies in the United States to promote integrated factories, with individuals from several cultures working side by side. The company also advertised in a number of

- 10. languages to reach the burgeoning immigrant market within the United States. Levi's took another marketing turn in the 1950s, when teenagers became the central focus in advertising for the brand. With movies such as The Wild One, featuring Marlon Brando in Levi's 501 jeans, the brand became associated with the rebellious "Beat Generation," the precursor of the 1960s countercultural revolution. Levi's jeans were becoming branded with the key attributes of rebellion and originality. (The "Right for School" campaign, however, drew responses to the contrary.) When Marilyn Monroe appeared in Levi's jeans in a photo shoot, the brand became sexier and appealing an alternative to skirts and other types of pants for women. 13 "Does Branding Combat Price Deflation?" Levi's at Wal-Mart? -5- UVA-M-0711 The company worked to expand the Levi's brand by moving into product lines such as Lighter Blues, Denim Family, and Casuals, the latter of which was adapted to meet the style of the 1960s with polyester blends and greater color variety. Levi's expanded into international markets in the 1950s. In 1969, the brand received further recognition through a famous photograph of the jeans being worn at the legendary

- 11. Woodstock music festival. The company set up a European division in 1965 and during the next decade expanded throughout the world and into Asia, with Japan becoming the fi订st Asian affiliate in 1971. The company's ability to create relevant and "cool" products for the teenage set as well as its progressive working conditions—such as being the fi江st to offer benefits to the unmarried partners of their employees and one of the first companies to offer support to AIDS victims— made Levi Strauss a heralded and well-respected Fortune 500 enterprise. By the 1980s, the company had several diverse interests ranging from dress-suit production to owning part of a hat manufacturer. In 1984, the company went through a major refocusing when it shed many of its noncore subsidiaries and based its marketing efforts on its star product—501 Levi' s. The timing was ideal—the company rode the wave of Bruce Springsteen's multiplatinum album "Born in the USA," the cover of which showed Springsteen' s backside clad in a trusty pair of 501s. The refocusing effort led by Strauss descendent Robert Haas put the company back on track as a profitable and focused organization. Seeing an opportunity to open up a new segment in the pants market, the company launched Dockers pants in 1986, as a casual alternative to dress pants and jeans. The success of Dockers was unabated. From its launch in 1986 to 2002, when Dockers introduced a line of pants

- 12. for women, the overall brand grew to over $1 billion in annual sales卫 The company decided to offer styles for the discerning young consumer and launched its Silvertab jeans in 1988. By 1996, Levi Strauss was at the top of its game~ it had built a truly global brand with efforts such as "Clayman," the company's fi江st global commercial, and its iconic 501 jeans continued to grow. The company had become the world's largest apparel manufacturer, with sales reaching a record $7.1 billion. Exhibit 2 shows a sample of Levi Strauss & Co.'s historical advertising 1.tnages. Levi Strauss & Co.: 1997 to 2002 Coming off a record year of sales in 1996, the company's sales began to decline from $7.1 billion and net income of $465 million in 1996, to $5.1 billion and net income of $5 million in 1999. By the close of the 2001 fiscal year, the company's sales had eroded further to $4.3 billion. During the same period, Levi Strauss restored net income to $151 million. The company was carrying debt of $2 billion, with some of the notes being graded as one category 14 Levi Strauss annual report, 2002. Business Policy and Strategic Management -6- UVA-M-0711 away from junk status as of early 2002.15 Exhibit 3 shows

- 13. financial highlights from 1997 through 2001. Levi's brand market share in men's and women's jeans fell from 18.7% in 1997 to 12.1 % in early 2002.16 In the men's jeans market, the company's mainstay category, the brand held 48% market share in 1990, but had decreased to approximately 20% by 2002.17 Levi Strauss's decline was attributed to several factors, such as increased competition in both the high- and low-end segments of the market. On the high end, image-conscious consumers were reaching for designer brands such as Tommy Hilfiger, Ralph Lauren Polo, and Calvin Klein. Other smaller premium brands such as Miss Sixty, Diesel, and Guess were all gaining momentum by offering fashion-foiward designs, finishes, fabrics, and fits. On the opposite end of the spectrum, major retailers such as JCPenney, Sears, Wal-Mart, Target, and Kmart were all realizing major market-share gains offering private-label jeans at under $20 apa江. Competing head-to-head in the same price category with Levi's jeans were vertical retailers such as the Gap, American Eagle Outfitters, Abercrombie & Fitch, J. Crew, and Eddie Bauer. These vertically integrated specialty stores controlled all aspects of product design, store design, and store operation. The Gap even had an in-house advertising department. These chains were credited with offering a consistent image across all formats and having the advantage of

- 14. placing products directly in the stores instead of having to sell to independently owned retailers. After being criticized for not being up to date with the shop- within-shop concept, the company invested heavily in education to learn more about in- store merchandising. One outcome was more than a dozen stores owned and operated by Levi Strauss & Co. in high-profile locations such as New York City. The company had a total of 3,300 retail customers at more than 20,000 locations. Observers felt that the Levi ' s brand was caught in the middle. Priced between $30 and $50 a pair, the jeans did not offer the same image or design as the high-end brands or the complete wardrobe selection of the vertically integrated retailers. Also, they did not offer the inexpensive alternatives found through private labels. To offer the lower price points, pundits suggested that the company eliminate its costly overhead of maintaining its North American- based production sources. In 1997, the company started closing its North American production facilities and further developed offshore sources of production with third parties in Asia, the Caribbean basin, and Latin America. 18 While it provided lower cost per unit, the company struggled to cover the costs of its restructuring charges for both manufacturing and non- 15 Levi Strauss annual report, 2002. 16 Lo山se Lee, "Why Levi's Still Look Faded," Business Week, July 22, 2002. 17 Ralph T. 灼ng Jr., "Infighting 沁ses, Productivity Falls,

- 15. Employees Miss Piecework System," Wall Street Journal, May 20, 1998. Note: The 2002 share derives from a case writer estimate. 18 The company had used offshore suppliers since the 1980s and had created a groundbreaking Supplier Code of Conduct in 1991. Levi's at Wal-Mart? -7- UVA-M-0711 manufacturing staff. From 1996, the company reduced headcount by 33%, moving from a worldwide total of over 25,000 employees to 16,700 by the end of the 2001 fiscal year.19 In 1999 Robert Haas stepped down from the CEO post, handing control over to the second nonfamily leader in the company's history—Phil Marineau. Marineau had over 25 years of experience in consumer packaged goods companies, working for 23 years and later holding the president and COO positions at Quaker Oats. There, he was credited with leading the global growth of Gatorade. Later, Marineau worked for a short time at Dean Foods and then moved to Pepsi-Cola North America for two years before being recruited to head Levi Strauss & Co. Levi's Product Lines In 2002, Levi's brand represented 74% of the company's

- 16. worldwide sales and 65% of sales in the Americas, with the remaining 9% derived from the Dockers brand and other smaller offshoots四 The brand comprised several product lines for men and women (see Table 1). Industry observers frequently talked about Levi's product lines being arranged in a pyramid, with fashion-forward designs such as Levi's Vintage Line, Levi's Red, and Levi's Premium at the top, followed in order by Levi's Engineered Jeans, Levi's Silvertab, and Levi's Red Tab. The product lines at the top of the pyramid were intended to create a halo effect on the overall brand, enhancing its image and fashion relevance. The company did not allow all its retailers access to higher-image brands. For examples JCPenney was not offered Levi's Vintage or Levi's Red, but was instead presented with the full range of Levi's Red Tab and Silvertab products. Each product line had a target consumer—the higher- end brands were aimed at trend- conscious buyers in the 15- to 24-year-old range, whereas the Levi' s Red Tab line had jeans suitable for more than 10 to 12 different body shapes and styles that included straight-leg, relaxed, baggy, boot cut, and slim. The company used the combination of fit, fabric , and finish as key differentiators for its target consumer and price point. Prices for Levi's Red Tab line had historically been double the price of the average jean. In the past five years, the average price paid at retail for Levi's jeans had been dropping, and was approximately 1.5 to 1.75 times the market average. 21

- 17. 19 Levi Strauss annual report, 200 I . 20 Levi Strauss annual report, 2002. 21 C -ase wnter estimates. Business Policy and Strategic Management -8- Table 1. Levi's product lines.22 Product line Description Levi's Vintage Clothing Small group of premium tops and and Levi's Red bottoms that were based on key heritage styles with premium fabncs. Levi's Engineered Jeans Group of tops and bottoms that were engineered for special mobility Levi's Premium Red Tab Variations of Levi's Red Tab products with changes to fabrics and finishes Levi's Red Tab The core of the Levi's brand including Levi's Silvertab the classic 501 button-fly jean, as well as a series of models from the 505 through 579, featuring shm, baggy, straight-leg, boot-cut and superlow fits. The line also included tops and jackets. Urban-inspired denim fits and techno- fabrics such as slick cotton and nylon- blends

- 18. Other Levi's products Included all other products such as additional tops, jackets, outwear and licensed products such as hats, bags, belts, socks, underwear, and footwear Source: Created by case writer. Distribution Channel High-end specialty stores Independent shops Specialty stores Independent shops Original Levi's stores Specialty stores Independent shops Original Levi's stores Department stores Chain stores Independent shops Original Levi's stores Department stores Chain stores Original Levi's stores Department stores Chain stores Independent shops Original Levi's stores UVA-M-0711 Retail Price Point

- 19. Bottoms: over $100 Bottoms: between $50 and $80 Bottoms: between $50 and $100 Bottoms: between $30 and $50 Bottoms: between $25 and $50 All price ranges depending on product category Levi Strauss & Co. was constantly releasing new products that fell somewhere within the pyramid structure. For example, a r efreshed design of Levi' s 501 jeans was in process with a release date p lanned for 2003. Also scheduled to h i t stores in 2003 was Levi's Type 1, a new product line, which accentuated the trademark Arcuate23 stitching design. Levi's new product releases had mixed results. For example, the release of Levi's Engineered Jeans in 2000 was highly successful in Europe and Asia but failed to prove v iable in the United States. The design direction for Levi's Engineered

- 20. Jeans was to start from zero and recreate a new jeans blueprint. The result of the new design was a reconstructed and re- engineered jean that had a twisted and bent pant leg for greater mobility . Fashion commentators believed that it was a breakthrough and soon many top-end brands such as G-Star and Diesel began their own designs based loosely on the Levi's pattern for Engineered Jeans. Despite this success with high-end brands, however , consumers of U.S. jeans did not adopt the innovation en masse. 22 Compiled by case writer based on information at retail locations and Levi Strauss annual report, 2001 . 23 Arcuate was the name given by Levi Strauss to the Levi's trademarked "V-like" stitching on the back pockets of a pair of Levi's jeans. Levi's at Wal-Mart? -9- UVA-M-0711 Advertising and Promotion The Levi's brand was rated as the number-one apparel brand for brand awareness and

- 21. brand retention.24 U .S. advertising and marketing for the Levi's brand in 2002 was estimated at $139 million. This budget included outlays for television advertising, billboard, print, and other media events and sponsorships.25 By comparison, Nike, a company more than double the size of Levi Strauss & Co., invested $998.2 million (10.5% in revenues) in advertising in 2001, and $974.1 million (10.8% ofrevenues) in 2000.26 As part of an integrated marketing approach, the company frequently promoted music and theatrical productions in exchange for brand advertising at the venue as well as product placement on the artists. Sponsored artists included tours by Lauryn Hill, Massive Attack, Jamiroquai, Christina Aguilera, Mariah Carey, De La Soul, Ben Folds Five, and the White Stripes. It used star talent such as Christina Aguilera and Mariah Carey in coordination with the release of Levi's Superlow jeans. For 2002, the brand was planning to tie in product with the World Cup soccer event in Korea by sponsoring Korean soccer star Song Chong Gug.27 To augment traditional approaches, the Levi's brand also worked to get product placement on television shows, feature films, music videos, and on the pages of top fashion magazines. Channels of Distribution Jeans channels could be grouped into six main categories within the U.S. denim landscape: 1. Chain and department stores such as JCPenney, Macy's,

- 22. Sears, May Department Stores Co., and Kohl's 2. Image department stores such as Bloomingdale's, Nordstrom, Neiman Marcus, and Saks International 3. Independent shops or "jeaneries" 4. Specialty stores such as the Gap, Old Navy, Abercrombie & Fitch, American Eagle Outfitters, and Original Levi's Stores (the only one of these to stock Levi's) 5. Mass merchants such as Wal-Mart, Target, and Kmart 6. Off-price channels such as Costco, Levi's Outlets, and TJ Maxx 24 Levi Strauss annual report, 2002. Note: Brand retention was defmed as the percentage of all past-12-month purchasers who planned on buying the brand in the future. 25 The 2001 annual report indicated approximately 7% of sales was spent on various media. This figure was derived by multiplying 7.4% times $4.1 billion in sales times 65% domestic sales times 74% of domestic sales for Levi's brand. 26 Nike, Inc., annual report, 2002. 27 Levi Strauss annual report, 200 I. Business Policy and Strategic Management

- 23. -10- UVA-M-0711 The mass channel sold an estimated 31 % of all jeans in the United States.28 The breakdown of total jean sales and Levi's brand sales by channel is shown in Tables 2 and 3. Table 2. Jean sales in the United States by channel (percent). Mass 31 Specialty 二 23 Chain 18 Department stores 16 Other 12 Total 100 Data source: Levi Strauss annual report, 2001. Table 3. Levi's brand sales in the United States by channel (percent). Chain and department stores 58 Independent 8 Specialty 3 —-Image department stores 2 Mass 0 Other 29 Total 100 Data source: Levi Strauss annual report, 2001. The Levi's brand was not present in the mass merchant channel in the United States. The single largest customer for Levi's brand sales was JCPenney, which accounted for over 10% of

- 24. the company's overall sales.29 In 2002, along with JCPenney, the top 10 customers in alphabetical order were Costco, Casual Male Retail Group (formerly Designs, Inc.), Dillard's, Federated Department Stores (owners of Macy's and Bloomingdales), Goody's, JCPenney, Kohl's, May Department Stores Co., the Mervyn's unit of Target Corporation, and Sears.30 Competition Given the fragmented nature of the fashion industry and the jeans market, the Levi's brand competed across a wide spectrum of brands. Competitors chose to either fight for market share based on price or sought consumers willing to pay a premium for image, design, fit, and finish. The frrst category was dominated by mass-market private labels from Wal-Mart, Target, Kmart, Sears, JCPenney, and Macy's. The second category was rife with examples from high- 28 Levi Strauss annual report, 200 I . 29 Levi Strauss annual report, 200 I . 30 Levi Strauss annual report, 200 I . Levi's at Wal-Mart? -11- UVA-M-0711 end brands such as Ralph Lauren Polo, Calvin Klein, and Guess, through to fashion-forward styles such as Fubu, L.E.I., Mudd, and Diesel. One consistent competitor in the last 50 years had

- 25. been Wrangler and Lee Jeans, both of which were owned by VF Corporation. VF Corporation: Wrangler, Lee, and Rustler VF Corporation, established in 1899, produced and marketed a large portfolio of brands including outdoor names such as JanSport, The North Face, and Eastpak as well as intimates labels such as Vanity Fair, Vassarette, and Bestform. VF's largest customer was Wal-Mart, which made up 15.1 % of VF's total sales in 2001 and 14.8% of VF's sales in 2000.31 Total advertising for all VF brands was $244 million (4.4% of sales) in 2001, $252 million (4.4% of sales) in 2000, and $258 million (4.6% of sales) in 1999.32 VF Corporation jeanswear brands included Riders, Chic, Britannia, and Rustler, and a number of product-line offshoots from the江 stable of Wrangler and Lee offerings. Riders, Chic, Britannia, and Rustler were sold in the mass channel at stores like Wal-Mart, Target, and Kmart and were typically priced between $9.99 and $19.99. All three of the brands were targeted largely at value-conscious mothers who made buying decisions for the rest of the family. Wrangler jeans were also available at the mass-merchant channel with some product extensions being available at chain and department stores. Wrangler jeans retailed between $14.99 and $24.99, and were designed for durability, reliability, and fit. Wrangler imaging revolved around western-inspired themes and the spirit of the American cowboy. Its consumer

- 26. base was mostly males ages 25 to 50 and appealed largely to men seeking comfortable jeans for work or pleasure activities. Lee Jeans were largely a chain and department store brand, commanding price points between $29.99 and $49.99, depending on the style, cut, and finish. In promotions, Lee Jeans used a character called Buddy Lee, a miniature cowboy doll that had gained a cult following in the United States. Lee Jeans were targeted toward the 15-to-25 age group, although the company did offer the Lee brand to children. The brand image projected original fits with up-to-date variations on vintage offerings. Designer and fashion-forward jeans Hundreds of brands competed in the designer and fashion- forward denim market. While the majority of brands commanded small market share, each attempted to find a niche with its style. The larger designer labels such as Ralph Lauren Polo, Calvin Klein, and Tommy Hilfiger were supported by ready-to-wear collections shown regularl~in fashion havens such as New York, London, Paris, and Milan. All three brands had distinct Jean collections, which they sold at high-end and regular department stores. All three brands invested heavily in in-store displays at 31 VF Corporation annual report, 2003. 32 VF Corporation annual report, 1999 through 2001 (see Exhibit 13).

- 27. Business Policy and Strategic Management -12- UVA-M-0711 department stores, refreshing the design and refurbishing every three years. The average price of jeans for these three labels was between $49.99 and $99.99. Other brands such as Guess ($49.99 to $79.99) and Diesel ($69.99 to over $100) had built a strong image using provocative out-of-home advertising. Guess chose to sell at a combination of department, independent, and Guess stores. Diesel products were found at higher-end department stores, image-conscious independents, and a small worldwide network of corporate- owned locations in select urban centers. Guess chose to control all of its advertising efforts in- house and spent $17.5 million (2.6% of total revenues) in 2001, $29.7 million (3.8% of total revenues) in 2000, and $24.5 million (4.0% of total revenues) on advertising in 1999.33 A number of other brands such as LE.I. (Life Energy Intelligence), Mudd, FUBU, and Lucky all attempted to establish a niche in the jean marketplace whether it be with quirky designs or baggy fits that responded to America's rap idiom. These brands were located at a combination of department stores and independent shops at price points ranging from $39.99 to $89.99. Vertically integrated specialty-store brands

- 28. The Gap sprung up in 1969 in San Francisco and carried Levi's jeans until the company began focusing on building its own jeans brand in the late 1980s and early 1990s. The Gap offered a wide range of casual products with a penchant for offering fashion-relevant basics supplemented by seasonal changes in colors, fits, and fabrics. An average pair of Gap jeans cost between $35.99 and $59.99, although the Gap frequently discounted its seasonal line of goods every eight weeks as new products were released into the stores. The Gap controlled all aspects of product and store design as well as consumer communications, which in recent years had featured a mix of well-known and unknown individuals involved in either music or dance. Notable TV spots for the 2001 holiday season included musical stars such as Dwight Yoakum, Macy Gray, Sheryl Crow, Shaggy, and Alanis Morissette. The Gap's target audience was fairly broad, although industry observers generally felt that the store was targeted to individuals in their 20s. The Gap also owned and operated Old Navy, which offered lower price points aimed at teenagers. An average pair of jeans at Old Navy cost between $19.99 and $29.99. Abercrombie & Fitch, American Eagle Outfitters, and J. Crew all competed for wardrobe dollars, offering a complete line of casual clothing for men, women, and children. They targeted consumers between 15 and 25 years of age, with each brand saluting the American classic styles frequently associated with campus and country club images. Prices points for a pair of jeans varied between $39.99 and $69.99.

- 29. Private-label brands Private labels were developed by retailers to offer consumers a similar product to branded alternatives at 50% to 60% of the retail price. JCPenney had developed the Arizona brand, which 33 Guess Inc. annual report, 200 I . Levi's at Wal-Mart? -13- UVA-M-0711 commanded about 7% of the men's jeans market, and Sears had a similar share of the market with their Canyon River Blues private label. Mass merchants had realized tremendous growth in private-label sales. Wal-Mart ,with its Faded Glory and No Boundaries private labels, had gained nearly 6% of the overall jeans market, while Kmart retained approximately 5% of the overall market. Target had taken a different approach by licensing the Cherokee brand, which became its captive label. With Cherokee jeans, Target had posted yearly growth to command nearly 8% of the overall jeans market in units. All private-label offerings by mass merchants were priced below $20. Wal-Mart Founded in 1962 in Arkansas, Wal-Mart became the world's

- 30. largest retailer. For the year ending January 31 , 2002, Wal-Mart posted revenues of $220 billion and net income of $6.7 billion.34 Exhibit 5 shows Wal-Mart's financials. It had over 2,700 U.S. outlets, split between its regular discount stores and supercenters that sold groceries and offered additional services. The company also operated another 500 discount outlets under the Sam's Club name and controlled nearly 1,200 outlets on international soil under names such as ASDA in the United Kingdom. Exhibit 6 indicates the growth of Wal-Mart' s discount stores and supercenters. Wal-Mart's average store size ranged from 90,000 square feet to over 200,000 square feet for supercenters. The company's slogan was, "Everyday low prices," and it guaranteed maximum selection at the lowest prices. Wal-Mart carried a mix of both private-label and branded merchandise with private-label sales accounting for approximately 20% of overall sales (in contrast, Target's private-label sales represented 50%).35 34 Table 4. Wal-Mart sales categories (percent). 22 Grocery, candy, and tobacco 21 Hard goods 18 Soft goods/ domestics 9 Pharmaceuticals 9 Electronics 7 Sporting goods and toys 7 Health and beauty aids 3 Stationery

- 31. 2 One-hour photo 1 Jewehy 1 Shoes 100 Total Data source: Wal-Mart annual report, 2002. Wal-Mart annual report, 2002. 35 Pankaj Ghemawat, Ken A. Mark, and Stephen P. Bradley, "Wal-Mart Stores in 2003," 9-704-430 (Cambridge, MA: Harvard Business School Publishing, 2004). Business Policy and Strategic Management -14- UVA-M-0711 Apparel sales were included in soft goods/domestics and represented approximately $23 billion in sales, or 11 % of Wal-Mart's total revenues.36 It was estimated that Wal-Mart held 12.6% of the entire apparel market compared with the 3.6% held by rival Target.37 Wal-Mart's most successful apparel categories were in the ladies'plus sizes and men's work wear with both consumer sets typically being 35 to 60 years old. Unlike higher- end designer brands that did not come in large sizes, Wal-Mart offered a range of sizes in men's pants with waist sizes that went as large as 48 inches. The predominant positioning for the Wal- Mart private labels was a focus on offering the basics at everyday low prices. As one analyst commented, "The only thing Wal-

- 32. Mart really develops is low prices."38 Another analyst explained that Wal-Mart used a low-risk strategy in its apparel division by playing down disposable fashion. "They can usually hold pricing at fairly stable and comfortable levels. They do some markdowns, but you won't see a whole category on sale," he said. 39 Some onlookers believed that Wal-Mart had substantial room in which to grow their apparel line and cited the retailer's attempt to develop one of its star brands, George, as well as other fashion-forward brands such as No Boundaries, Organize Your Life, and Mary-Kate & Ashley that were aimed at junior customers.40 As a Wal-Mart spokesperson said, "Over the past five years we've stepped up our efforts to focus on apparel, in terms of fashion and quality. George demonstrates that commitment. It offers high quality, great value and styling at everyday low prices."41 While looking to grow its own brands, Wal-Mart also purchased a specially designed assortment from work wear marketer Dickies, which developed a line specifically for Wal-Mart. Other branded apparel manufacturers such as VF Corporation sold Wal-Mart multiple lines, including the Wrangler, Riders, and Rustler brands. The president of VF Jeanswear, Mass Market, said: The potential for Wal-Mart's apparel is endless. They already turn merchandise well, but the numbers of people who walk into stores and don't buy apparel or

- 33. only buy a small percentage is huge. It comes back to what products they showcase and how they customize the assortment.42 Wal-Mart organized its offerings along the good, better, and best spectrum, with private labels filling the good position and national brands occupying the best spot. VF's Wrangler jeans were priced from $14.99 to $24.99, while Wal-Mart' s Faded Glory brand was priced regularly at 36 Debby Garbato Stankevich, "Expanding Upon a Basic Appeal: 汕cromarketing and Other Initiatives Are Likely to Drive Wal-Mart's Clothing Sales to New Heights," Retail Merchandiser, March 1, 2002: 34. 37 Emily Scardino, "Is Target's Wardrobe in Wal-Mart's Sights? The Mossimoization of Mass Catches On," Discount Store News, April 7, 2003, Sl. 38 Stankevich. 39 Stankevich. 40 Stankevich. 41 A. Scott Walton, "Low-Cost, High-Fashion," Cox News Service, November 25, 2002. 42 Stankevich. Levi's at Wal-Mart? -15- UVA-M-0711 $10.77.43 In women's jeans, the main national brand was Riders jeans, which sold between $14.99 and $24.99; No Boundaries, Faded Glory, and White

- 34. Stag carrying price tags between $9 and $20. Wal-Mart's No Boundaries brand offered greater variation in styles and coloring. The collection was largely based on prevailing fashions such as capri pants and low-rise jeans for girls, as well as carpenter pants and baggy fit for boys. Faded Glory offered customers a sturdy and relaxed basic jean. One fashion source even claimed that Faded Glory jeans were one of the most comfortable jeans in the U.S. market.44 Exhibit 7 shows a list of Wal-Mart's main brands by consumer category. The central incident involving the weakening of the Levi Strauss & Co. and Wal-Mart relationship was the dispute over selling Levi's Orange Tab jeans (a line of products that was phased out in the United States but still existed in Canada) to Wal-Mart stores in 1994, when it purchased the Woolco chain in Canada. Levi's decision to not sell Orange Tab at Wal-Mart in Canada cost the U.S. business the entire Wal-Mart sales of the Britannia brand—approximately 1.2 million units, or $10 million in revenue, for the Levi's brand.45 The Question for Levi's: What to Do and How to Do It? Levi Strauss & Co. management believed that its competitive advantage was based on the worldwide recognition of the Levi's brand name, its commitment to ethical conduct and social responsibility, and its focus on product innovation, quality, and value. Management thought that the Levi's brand was able to work across several channels of distribution because of its long-

- 35. standing relationships with top retailers.46 To remain competitive, Phil Marineau realized the company needed to continue innovating fits, fmishes, fabrics, and other product features. The necessity of maintaining strong brand imaging and advertising was believed to help Levi's maintain the number-one position as the most recognized jeans brand in the world. To strengthen retail partnerships, Marineau had to provide products for retailers to reach their overall blended margin, while backing up all brand extensions with strong consumer messaging and the necessary investment to create an in-store experience complementary to the brand and the retail space. In mid-January 2002, Marineau told the press: One point where we don't sell is obviously the mass merchants: Wal-Mart, Kmart, Target. We'd be crazy not to be studying that and trying to understand what the opportunities are in the marketplace. We've talked to these people, we've tried to understand how they do business, what they do. We have studies 43 "Retail Industry Update," Credit Suisse F江st Boston, July 18, 2003, I. 44 "Cheap Jeans Beat Designer Once Again," http://www.fashionunited.eo.uk/news/archive/jeansl.htm (accessed February 2, 2010). 45 Trager. 46 Levi Strauss annual report, 200 I.

- 36. Business Policy and Strategic Management -16- UVA-M-0711 going on about what their consumers want. But we have no announcement to make about any plans or any approach that we have fmalized or decided on. The first person we will tell ifwe do this is our current customers.47 Marineau was well aware of the P?tential reaction from customers. In its past, Levi's had upset existing customers on a few occas10ns when it made the decision to withdraw a product line or to sell to other customers. One such incident was in 1982, when Levi' s made the decision to sell to chain stores JC Penney and Sears, which caused a dearth of orders from department stores such as Macy' s.48 Eleven years later, Macy's began purchasing Levi' s jeans again. The Decision While some insiders were convinced that selling a brand to Wal- Mart was necessary, many executives within the company were divided on the subject. One article from an apparel industry magazine read: According to sources, there are intense disagreements within Levi's as to whether the company should make a move toward the mass market. In particular, the executives who have worked to build the company's profile in

- 37. the premium jeans market---on the strength of directional lines including Levi's Red Tab and Levi's Vintage Clothing, which carry triple-digit price tags—are said to be reluctant to see the brand sold in Wal-Mart.49 Marineau and his executive team needed to decide on whether— and if so, how—to sell to Wal-Mart. Levi's formidable competitor VF maintained the top spot among national competitors at Wal-Mart—Wrangler in men's jeans and Riders in women's jeans. One analyst said Levi Strauss & Co. was going to have "a tough time taking on the presence that Wrangler has in this niche."50 The other main pressure was explaining the rationale to existing customers. 47 An industry insider said: [Selling to Wal-Mart] creates more pressure for the Kohl's and Penney 's of the world. What are they going to do—just roll over and play dead? [Some retailers may say] "You have mass distribution now, we can't make money on you, you're gone." [Levi Strauss & Co. has not] had one effective strategy yet. This one will prop up short-term earnings, but it's a bad long-term strategy.51 Scott Malone, "Retail Revolution—Levi's Considers Selling Wal-Mart as Sales Slump," Women's Wear Daily, January 17, 2002, I.

- 38. 48 Malone. 49 Malone. 50 Thomas Cunningham, "Levi Strauss Rolls the Dice ... ," Daily News Record, November 4, 2002. 51 Cunningham. Levi's at Wal-Mart? -17- UVA-M-0711 On the other hand, another analyst said, "The total volume of traditional department stores is so insufficient right now that if Levi Strauss was totally dependent on department stores, they would go out ofbusiness."52 Marineau wondered about how he could leverage the celebrated Levi's brand name while remaining competitive and not affecting consumers' propensity to purchase other Levi's product lines at higher price points. "Around the world," Marineau said, "we' re making sure we have the opportunity to sell at the right price point, from the $250 level to the $25 level. That' s a unique opportunity for the Levi's brand, and it's one we' ll continue to explore as we move forward." 53 52 Cunningham. 53 Malone. Business Policy and Strategic Management

- 39. -1 8- Exhibit 1 LEVI'S AT WAL-MART? Apparel M arket Information U.S. Annual Apparel Dollar Sales (1998-2001) 1998 168 1999 173 3.0% 2000 176 1.7% 2001 166 -5.7% 2001 U.S. Apparel Sales by Market Segment (billions) Total Apparel Men's Women's Boys' Girls' Infants'& Toddlers'

- 40. Dollar Volume % Chg 00/01 Dollar Share % 166 -5.9% 100.0% 51 -7.0% 30.7% 89.3 -6.7% 53.9% 7.3 -5.6% 4.4% 7.5 -4.1 % 4.5% 10.6 5.7% 6.4% 2001 U.S. Apparel Sales by Channel Distribution (billions) Channel All Channels Department Stores National Chain Mass Merchants Specialty Stores All Other Dollar Volume 2 % Chg 00/01 Dollar Share % 166 -5.9% 100.0% 32.7 -6.3% 19.7% 22.4 -10.2% 13.5% 34.9 -0.6% 21.0% 41.2 -6.4% 24.9% 34.5 -7.0% 20.8% Data source: "Reports 2001 U.S. Apparel Industry Down for First Time in Three Years," April 29, 2002, http://www.npdfashionworld.com (accessed March 3, 2005).

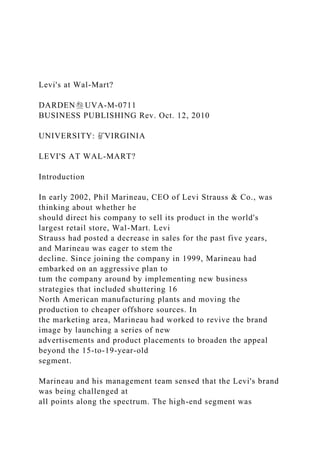

- 41. UVA-M-0711 -19- Exhibit 2 LEVI'S AT WAL-MART? Images of Levi's throughout the Ages UVA-M-0711 t •• 身,·······~ 等........ w ••• uvrrs鳍伊HS/Im, 主王幸圭幸宝宝兰 1J k叩妇片est'slacksand fashion _______ ,. 需 己志已于莘辛廷兰王之- Levi's Ad: 1966 Levi's Sta-Prest Ad: 1970 Levi' s for Women: 1992 Source: Levi Strauss and Co. Used with permission. Levi ' s at Wa l,M

- 42. art? Business Po licy and Strategic Management -20- Exhib it 3 LEVI'S AT WAL-MART? L evi Strauss & Co. Financial Hig hlights Nov30 Nov29 Nov28 1997 1998 1999 Statement of Income Data : Net Sales 6,861,482 5,958,635 5,139,458 Cost of goods sold 3,962,719 3,433,081 3,180,845 Gross profit 2,898,763 2,525,554 1,958,613 Marketing, general and administ「ativ1 2,045,938 1,834,058 1,629,845 Other operating (income) (26,769) (25,310) (24,387) Excess capacity/restructuring charge 386,792 250,658 497,683 Global Success Sharing Plan 114,833 90,564 (343,873) Operating income 377,969 375,584 199,345 Interest expense 212,358 178,035 182,978 Other (income) expense, net (18,670) 34,849 7,868 Income before taxes 184,281 162,700 8,499 Income tax expense 46,070 60,198 3,144 Net income 138,211 102,502 5,355

- 43. Statement of cash flow: Cash flows from operating activities 573,890 223,769 (173,772) Cash flows from investing activities (76,895) (82,707) 62,357 Cash flows from financing activities (530,302) (194,489) 224,219 Balance Sheet Data: Cash and cash equivalents 144,484 84,565 192,816 Working capital 701,535 637,801 770,130 Total assets 4,012,314 3,867,757 3,670,014 Total debt 2,631 ,696 2,415,330 2,664,609 Stockholders'deficit (1,370,262) (1,313,747) (1,288,562) Data source: Levi Strauss & Co. annual report, 2001. UVA-M-0711 Nov26 Nov25 2000 2001 4,645,126 4,258,67• 2,690,170 2,461,191 1,954,956 1,797,471 1,481,718 1,355,88! (32,380) (33,421 (33,144) (4,281 538,762 479,29 234,098 230,77: (39,016) 8,831 343,680 239,68° 120,288 88,68!

- 44. 223,392 151,00· 305,926 141,901 154,223 (17,231 (527,062) (139,891 117,058 102,83 555,062 651,251 3,205,728 2,983,481 2,126,430 1,958,43: (1,098,573) (935,94 Explanation of Stockholders' Deficit from annual report: "The stockholders'deficit resulted from a 1996 transaction in which the company' s stockholders created new long-term governance arrangements, including a voting trust and stockholders'agreement. As a result, sh ares of stock of a former parent company, Levi Strauss Associates Inc., including shares held under several employee benefit and compensation plans, were converted into the right to receive cash. Th e funding for the cash payments in this transaction was provided in part by cash on hand and in part from proceeds of approximately $3.3 billion of borrowings under bank credit facilities. The company's ability to satisfy its obligations and to reduce its total debt depends on the company's future operating performance and on economic, fmancial, competitive, and other factors, many of which are b eyond the company's control."1 1 Levi Strauss annual report, 200 I.

- 45. Levi's at Wal-Mart? -21- Exhibit4 LEVI'S AT WAL-MART? Pictures of Lev i 's Product L in es UVA-M-0711 Levi's Superlow: 2002 Levi's Silvertab: 2002 Levi's Red Tab Cords: 2000 LEVI ·S ENGINEERED JEANS /Sf Pllr AUX YOLONT(S l1J COR~

- 46. iA - Levi's Engineered Jeans: 2002 Source: Levi Strauss and Co. Used with permission. Business Policy and Strategic Management -22- Exhibit 5 LEVI'S AT WAL-MART? Wal-Mart Financials (dollars in billions) 2000 Net Sales Net sales increase Domestic comparative store sales increase Other income net Cost of sales Operating, selling and general and admin expenses Interest costs: Debt Capital Leases Provision for income taxes Mino「ity interest and equity in unconsolidate subsidiam

- 47. Cumulative effect of accounting change, net of tax Net income Per share of common stock: Basic net income Diluted net income Dividends Current Assets Inventories at replacement cost Less LIFO reserve Inventories at LIFO cost Net property, plant and equipment and capital leases Total assets Current liabilities Long-term debt Long-term obligations under capital leases Shareholders'equity Current ratio Inventories/working capital Return on assets• Return on shareholde「s'equity•• Number of U.S. Wal-Mart stores Number of U.S. Supercentres Number of U.S. SAM'S CLUBS Number of U.S. Neighborhood Markets International Units Number of Associates Number of Shareholders of reco「d (as of Ma「ch 31) 165,013 20.0% 8.0%

- 50. 202 21,442 40,934 78,130 28,949 12,501 3,154 31 ,343 0.9 -9 8.7% 22.0% 1,736 888 475 19 1,071 1,244,000 317,000 * Net income before mino「ity interest, equity in unconsolidated subsidiaries and cumulative effect of accounting change/average assets ** Net income/average shareholders•'equity *** Calculated giving effect to the amount by which a lawsuit settlement exceeded UVA-M-0711

- 52. 23.~ 8.5o/c 20.1 o/c 1,647 1,066 500 31 1,170 1,383,000 324,000 established reserves. If this settlement were not considered, the return would have been 9.8% for 2000 Return on Assets. Levi's at Wal-Mart? -23- Exhibit 6 LEVI'S AT WAL-MART? Wal-Mart Number of Doors UVA-M-0711 STORE COUNT Year Ending January 31 Wal-Mart Discount Stores

- 53. Opened Closed Conversions Balance Forward 1997 1998 1999 2000 2001 2002 59 37 37 29 41 33 2 lll 2l 92 75 88 96 104 121 tal95602169013647 T o-1 尥 尥

- 54. 凶 顶 口 顶 Wal-Mart Supercenters Opened Total 239 344 441 564 721 888 1,066 105 97 123 157 167 178 Source: Wal-Mart annual report, 2002. Business Policy and Strategic Management -24- Exhib it 7 LEVI'S AT WAL-M ART?

- 55. Wal-Mart Jeans Selection in 2002 (retail price in dollars) Wal-Mart's private label/ National brands captive brands available Men No Boundaries $15- 20 Wrangler $15- 20 Faded Glory 9- 11 Rustler 9- 15 George 15- 20 Dickies 15- 25 Women White Stag 15- 20 Riders 15- 20 Faded Glory 9- 11 George 15- 25 Juniors No Boundaries 10-20 Jordache 15- 20 Girls Faded Glory 8- 11 mary-kate and 15- 25 ashley No Boundaries 15- 20 Riders 15- 20 Boys Faded Glory 8- 11 Wrangler $15- 20 No Boundaries 15- 20 George $15- 25 Source: Created by case w巾er. UVA-M -07 11

- 56. Walt Disney Co.: The Entertainment King 帘 HARVARD I sus1NEssiscHOOL 9-701-035 REV, JANU ARY 5, 2009 MICHAEL G. RUKSTAD DAVID COLLIS The Walt Disney Company: The Entertainment King I only hope that we never lose sight of one thing—that it was all started by a mouse. - Walt Disney The Walt Disney Company's rebirth under Michael Eisner was w idely considered to be one of the great turnaround stories of the late twentieth century. When Eisner arrived in 1984, Disney was languishing and had narrowly avoided takeover and dismemberment. By the end of 2000, however, revenues had climbed from $1.65 billion to $25 billion, while net earnings had risen from $0.1 billion to $1.2 billion (see Exhibit 1). During those 15 years, Disney generated a 27% annual total return to shareholders.1 Analysts gave Eisner much of the credit for Disney's resurrection. Described as "more hands on than Mother Teresa," Eisner had a reputation for toughness.2 "If you aren' t tough," he said, "you just

- 57. don't get quality. If you're soft and fuzzy, like our characters, you become the skinny kid on the beach, and people in this business don't mind kicking sand in your face."3 Disney's later performance, however, had been well below Eisner's 20% growth target. Return on equity which had averaged 20% through the first 10 years of the Eisner era began dropping after the ABC merger in 1996 and fell below 10% in 1999. Analysts attributed the decline to heavy investment in n ew enterprises (such as cruise ships and a new Anaheim theme park) and the third-place performance of the ABC television network. W血e profits in 2000 had rebounded from a 28% d ecline in 1999, this increase was largely due to the turnaround at ABC, which itself stemmed from the success of a single show: Who Wants To Be a Millionaire. Analysts were starting to ask: Had the Disney magic begun to fade? The Walt Disney Years, 1923-1966 At 16, the Missouri farm boy, Walter Elias Disney, falsified the age on his p assport so he could serve in the Red Cross during World War I. He returned at war's end, age 17, determined to be an artist. When his Kansas City-based cartoon business failed after only one year,4 Walt moved to Hollywood in 1923 w here he founded Disney Brothers Studio5 with his older brother Roy (see Exhibit 2). Walt was the creative force, while Roy handled the money . Quickly concluding that he would never be a great animator, Walt focused on overseeing the story work.6

- 58. A series of shorts starring "Oswald, the Lucky Rabbit" became Disney Brothers'first m ajor hit in 1927. But within a year, Walt was outmaneuvered by his distributor, which hired away most of Professor Michael G. Rukstad, Professor David Collis of the Yale School of Management, and Research Associate Tyrrell Levine prepared this case. This case was developed from published sources. HBS cases are developed solely as the basis for class 如cussion. Cases are not intended to serve as endorsements, sources of primary data, or illustrations of effective or ineffective management. Copyright ©2001, 2005, 2009 President and Fellows of Harvard College. To order copies or request per皿ssion to reproduce materials, call 1- 800-545-7685, write Harvard Business School Publis血g, Boston, MA 02163, or go to http:/ / www.hbsp.harvard.edu. No part of this publication may be reproduced, stored in a retrieval system, used in a spreadsheet, or transmitted in any form or by any mea沁- €lectronic, mechanical, photocopying, recording, or otherwise-without the permission of Harvard Business School. Business Policy and Strategic Management 701-035 The Walt Disney Company: The Entertainment King Disney's animators in a bid to shut Disney out of the Oswald franchise.7 Walt initially thought he could continue making Oswald shorts with new animators and a new distributor, but after reading

- 59. the fine print of his contract, he was devastated to learn that his distributor owned the copyright. Desperate to create a new character, Walt modified Oswald's ears and made some additional minor changes to the rabbit's appearance. The result was Mickey Mouse. When Mickey failed to elic廿 much interest, Walt tried to attract a distributor by adding synchronized sound—something that had never been attempted in a cartoon砂 His gamble paid off handsomely with the release of Steamboat Willie in 1928.10 Overnight, Mickey Mouse became an international sensation known variously as "Topolino" (Italy), "Raton Mickey" (Spain), and "Musse Pigg" (Sweden). However, the company was still strapped for cash, so it licensed Mickey Mouse for the cover of a pencil tablet—the first of many such licensing agreements. Over time, as short-term cash problems subsided, Disney began to worry about brand equity and thus licensed its name only to "the best companies."11 The Disney brothers ran their company as a flat, nonhierarchical organization, in which everyone, including Walt, used their first names and no one had titles. "You don't have to have a title," said Walt. "If you're important to the company, you'll know 让卢 Although a taskmaster driven to achieve creativity and quality, Walt emphasized teamwork, communication, and cooperation. He pushed himself and his staff so hard that he suffered a nervous breakdown in 1931.13 However, many workers were fiercely committed to the company. Despite winning six Academy Awards and successfully introducing new characters such as Goofy

- 60. and Donald Duck, Walt realized that cartoon shorts could not sustain the studio indefinitely . The real money, he felt, lay in full-length feature films.14 In 1937, Disney released Snow White and the Seven Dwarfs, the world's first full-length, full-color animated feature and the highest-grossing animated movie of all time.15 In a move that would later become a Disney trademark, a few Snow White products stocked the shelves of Sears and Woolworth's the day of the release. With the success of Snow White, the company set a goal of releasing two feature films per year, plus a large number of shorts. Next, the company scaled up. The employee base grew sevenfold, a new studio was built in Burbank, and the company went public in 1940 to finance the strategy. Disney survived the lean years of World War II and the failure of costly films like Fantasia (1940) by producing training and educational cartoons for the government, such as How Disease Travels.16 Disney made no new full-length features during the war, but re- released Snow White for the first time in 1944, accounting for a substantial portion of that year's income.17 Subsequently, reissuing cartoon classics to new generations of children became an important source of profits for Disney. After the war, the company was again in difficult financial straits. It would take several years to make the next full-length animated film18 (Cinderella, 1950), so Walt decided to generate some quick income by making movies such as Song of the South (1946) that mixed live action with animation.19 Further diversification included the creation of the Walt Disney

- 61. Music Company to control Disney' s music copyrights and recruit top artists. In 1950, Disney's first TV special, One Hour in Wonderland, reached 20 million viewers at a time when there were only 10.5 million TV sets in the U.S.20 With the release of Treasure Island in 1950, Disney entered live-action movie production and, by 1965, was averaging three films per year. Most were live-action titles, such as the hits Old Yeller (1957), Swiss Family Robinson (1960), and Mary P叩pins (1964), but a few animated films like 101 Dalmatians (1961) were also made. To bolster the fihn business, Disney created Buena Vista Distribution in 1953, ending a 16-year-old distribution agreement with RKO. By eliminating distribution fees, Disney could save one-third of a film's gross revenues. And to further improve the bottom line, Disney avoided paying exorbitant salaries by developing the studio's own pool of talent. 2 Walt Disney Co.: The Entertainment King The Walt Disney Company: The Entertainment King 701-035 Observed one writer: "Disney himself became the box office attraction—as a producer of a predictable family style and the father of a family of lovable animals."21 Disney expanded its television presence in 1954 with the ABC- produced television program

- 62. 肋sneyland (followed the next year by the very popular Mickey Mouse Club, a show featuring pre-teen "Mouseketeers" as hosts). Walt hoped Disneyland would both generate financing and stimulate public interest in the huge outdoor entertainment park of the same name, which he had started designing two years earlier at WED Enterprises (WED being Walt's initials). This was kept separate from Disney Productions to provide an environment where Walt and his "Imagineers" could design and build the park free of pressure from film unions and stockholders. The park was a huge risk for the company, as Disney had taken out millions of dollars in bank loans to build it. But the bet paid off. The enormous success of Disneyland, which opened in 1955, was a product of both technically advanced attractions and Walt's commitment to excellence in all facets of park operation. His goal had been to build a park for the entire family, since he believed that traditional parks were "neither amusing nor clean, and offered nothing for Daddy心 Corporate sponsorship was exploited to minimize the cost of upgrading attractions and adding exhibits.23 To conserve capital, Disney also licensed the food and merchandising concessions. Once the park had generated sufficient revenue, the company bought back v江tually all operations within the park.24 Disneyland's success finally put the company on solid 加ancial footing.25 With Disneyland still in its infancy, Walt dreamed of starting another theme park. In 1965, he secretly purchased over 27,000 acres of land near Orlando, Florida on which he planned to build Walt

- 63. Disney World and EPCOT—an "experimental prototype community of tomorrow." However, Walt was never able to see his dream come to fruition; he died just before Christmas 1966. "He touched a common chord in all humanity," said former President Dwight Eise咄ower. "We shall not soon see his like again."26 Walt Disney's philosophy was to create universal timeless family entertainment. A strong believer in the importance of family life, the company was always oriented to fostering an experience that fam认ies could enjoy together. As Walt Disney said, "You 're dead if you aim only for kids. Adults are only kids grown up, anyway." The huge number of "firsts" that the company could claim were a tribute to the success of this philosophy, but Disney recognized that they were not without risk. "We cannot hit a home run with the bases loaded every time we go to the plate. We also know the only way we can ever get to first base is by constantly going to bat and continuing to swing." Disney attempted to retain control over the complete entertainment experience. Cartoon characters, unlike actors, could be perfectly controlled to avoid any negative imagery. Disneyland had been constructed so that once inside, visitors could never see anything but Disneyland. According to Walt, "The one thing I learned from Disneyland [is] to control the environment. Without that we get blamed for 如ngs that someone else does. I feel a responsibility to the public that we must control this so-called world and take blame for what goes on."27

- 64. The Post-Walt Disney Years, 1967-1984 The realization of Walt Disney World and EPCOT consumed Roy 0. Disney, who succeeded his brother as chairman and lived just long enough to witness the opening of Walt Disney World in 1971. The theme park almost instantly became the top-grossing park in the world, pulling in $139 million from nearly 11 million visitors in its first year. Its two on-site resort hotels were the first hotels operated by Disney. To generate traffic in the park, Disney opened an in-house travel company to 3 Business Policy and Strategic Management 701-035 The Walt Disney Company: The Entertainment King work with travel agencies, airlines, and tours. Disney also started bringing live shows, such as "Disney on Parade" and "Disney on Ice," to major cities all over the world. The next major expansion was Tokyo Disneyland, announced in 1976. Although wholly owned by its Japanese partner, it was designed by WED Enterprises to look just like the U.S. parks. Disney received 10% of the gate receipts, 5% of other sales, and ongoing consulting fees. Film output during the years of theme park construction declined substantially. Creativity in the

- 65. film division seemed stifled. Rather than push new ideas, managers were often heard asking, "What would Walt have done?" The result was more sequels rather than new productions. To help stem the decline in its filin division in the late 1970s and early 1980s, Disney introduced a new label, Touchstone, to target the teen/adult market, where film-going remained strong. From 1980 to 1983, the company's financial performance deteriorated. Disney was incurring heavy costs at the time in order to finish EPCOT, which opened in 1982. It was also investing in the development of a new cable venture, The Disney Channel, launched in 1983. Filin division performance remained erratic. As corporate earnings stagnated, Roy E. Disney (son of Roy 0. Disney) resigned from the board of directors in March 1984. In the following months, corporate raiders Saul Steinberg and Irwin Jacobs each made tender offers for Disney with the intention of selling off the separate assets. However, oil tycoon Sid Bass invested $365 million, rescuing the company, reinstating Roy E. Disney to the board, and ending all hostile takeover attempts.28 Eisner's Turnaround, 1984-1993 Eisner takes the helm Backed by the Bass group, Eisner, 42, was named Disney's chairman and chief executive officer, and Frank Wells was named president and chief operating officer in October 1984.29 Eisner, a former president and chief operating officer of Paramount Pictures, had been associated with such successful films and television shows as Raiders of the Lost Ark and Happy

- 66. Days. Wells, a former entertainment lawyer and vice chairman of Warner Brothers, was known for his business acumen and operating management skills. Roy E. Disney was named vice chairman. Eisner subsequently recruited Paramount executives Jeffrey Katzenberg and Rich Frank to be chairman and president, respectively, of Disney's motion pictures and television division. Eisner committed himself to maximizing shareholder wealth through an annual revenue growth target and return on stockholder equity exceeding 20%. His plan was to build the Disney brand while preserving the corporate values of quality, creativity, entrepreneurship, and teamwork. Concerns that the new managers would neither understand nor maintain Disney's culture faded rapidly. The history and culture of the company and the legacy of Walt Disney were inculcated in a three-day training program at Disney's corporate university. As part of the training, all new employees, including executives, were required to spend a day dressed as characters at the theme parks as a way to develop pride in the Disney tradition. Eisner viewed "managing creativity" as Disney's most distinctive corporate skill. He deliberately fostered tension between creative and financial forces as each business aggressively developed its market position. On the one hand, he encouraged expansive and innovative ideas and was protective of creative efforts in the concept-generation phase of a project. On the other hand, businesses were expected to deliver against well-defined strategic and financial objectives. All businesses (see Exhibit 3), including individual 出ms and TV shows, were expected to

- 67. have the potential for long-run profitability. Nevertheless, spending was readily approved if necessary to achieve creativity. Revitalizing TV and movies One of the new management's top priorities was to rebuild Disney's TV and movie business. Disney had stopped producing shows for network television out of 4 Walt Disney Co.: The Entertainment King The Walt Disney Company: The Entertainment King 701-035 concern that it would reduce demand for the recently launched Disney Channel. But Eisner and Wells believed that a network show would help create demand by highlighting Disney's renewed commitment to quality programming. In early 1986, The Disney Sunday Movie premiered on ABC. According to Eisner, the show "helped to demonstrate that Disney could be inventive and contemporary. . . . It put us back on the map空 During this time, Disney produced the NBC hit sitcom Golden Girls and the syndicated non-network shows Siske/ & Ebert at the Movies and Live with R~ 炉s & Kathie Lee. Eisner also created a syndication operation to sell to independent TV stations some of the TV programming that Disney had accumulated over 30 years. Disney's movie division was nearly as moribund when Eisner and Wells took over. Disney's share

- 68. of box office had fallen to 4% in 1984, lowest among the major studios, and Eisner contended that not one of the live-action movies that Disney had in development seemed worth making. However, in Eisner's first week at Disney, an agent called him with the script to what would become Down and Out in Beverly Hills, Touchstone's first R-rated movie. While Disney had risked alienating its core audience with the film, no backlash materialized. Beginning with that movie, 27 of Disney's next 33 movies were profitable, and six earned more than $50 million each, including Three Men and a Baby and Good Morning Vietnam. For the industry as a whole, an estimated 60% of all movies lost money. By 1988, Disney Studios'film division held a 19% share of the total U.S. box office, making it the market leader. "Nearly overnight," said Eisner, "Disney went from nerdy outcast to leader of the popular crowd."31 During this run, Disney began releasing 15 to 18 new films per year, up from two new releases in 1984. Releases under the Touchstone label were primarily comedies, with sex and violence kept to a minimum. Live-action releases under the Walt Disney label were designed for a contemporary audience but had to be wholesome and well plotted. Katzenberg, who was known for h is ability to identify good scripts, for his grueling work ethic (scheduling staff meetings for 10 p.m.), and for his dogged pursuit of actors and directors for Disney projects, convinced some of Hollywood's best talent to sign multideal contracts with Disney. Under Katzenberg, Disney pursued strong scripts from less established writers and well-known actors in

- 69. career slumps and TV actors rather than the highest-paid movie stars. The emphasis was on producing moderately budgeted films rather than big-budget, special effects-laden blockbusters. Management held movie budgets to certain target ranges that acted as a "financial box" within which the creative talent had to operate. Films were closely managed to ensure that they would come in on time and near their target budgets, which were set below the industry average.32 Disney's animation division was slower to tum around, in part because animated movies took so long to produce. Disney decided to expand its an订nation staff and to accelerate production by releasing a new animated feature every 12 to 18 months, instead of every 4 to 5 years. Disney also invested $30 m曲on in a computer animated production system (CAPS) that digitized the animation process, dramatically reducing the need for animators to draw each frame by hand. In 1988, Disney spent $45 million on Who Framed Roger Rabbit, a technically dazzling movie that combined animation w ith live action. The movie was uncharacteristically expensive for Disney, but the gamble paid off with the top earnings at the box office in 1988 ($220 million). Additional profits came from the merchandise, as the movie was Disney's first major effort at cross-promotion. By the time of the premiere, Disney had licensing agreements for over 500 Roger Rabbit products, ranging from jewelry to dolls to computer games. McDonald's and Coca-Cola also did promotional tie-ins. Maximizing theme park profitability Unlike Disney's television and movie business,

- 70. Disney's theme parks had remained popular and profitable after the deaths of Walt and Roy Disney. However, the new management team updated and expanded attractions at the parks. Disney spent tens of millions of dollars on new attractions such as "Captain EO" (1986) starring Michael Jackson. 5 Business Policy and Strategic Management 701-035 The Walt Disney Company: The Entertainment King Investments in the parks were offset by attendance-building strategies designed to generate rapid revenue and profit growth (see Exhibit 4). These included for the first time national television ads, as well as special events, retail tie-ins, and media broadcast events. Disney also lifted restrictions on the numbers of visitors permitted into its parks, opened Disneyland on Mondays when it had previously been closed for maintenance, and raised ticket prices (see Exhibits 5 and 6). Despite the ticket hikes, market research showed that guests felt they received value for their money. The Disney Development Company was established to develop Disney's unused acreage, primarily in Orlando, where only 15% of the 43 square miles had been exploited. It proceeded to aggressively expand its activities, which included a several- thousand-room hotel expansion at Disney World (and the company's first moderately priced hotel) and a $375 million convention center.

- 71. Coordination among businesses As the business units expanded after 1984, overlaps among them began to emerge. Promotional campaigns with corporate sponsors in one business needed to be coordinated with similar initiatives by other Disney businesses. It was also unclear how, for example, to allocate the minute of free advertising granted to Disney during The Disney Sunday Movie. Like many diversified companies, Disney employed negotiated internal transfer prices for any activity performed by one division for another. Transfer prices were charged, for example, on the use of any Disney film library material by the various divisions. W血e Eisner and Wells encouraged division executives to resolve conflicts among themselves, they made it clear that they were available to arbitrate difficult issues. Senior management's position was that disputes should be settled quickly and decisively so that business unit management could get on with their jobs. Nevertheless, in 1987, a corporate marketing function was installed to stimulate and coordinate companywide marketing activities. A marketing calendar was introduced listing the next six months of planned promotional activities by every U.S. division. A monthly meeting of 20 divisional marketing and promotion executives was initiated to discuss interdivisional issues. A library committee was set up that met quarterly to allocate the Disney film library among the theatrical, video, Disney Channel, and TV syndication groups. An in-house media buying group was also established to coordinate media buying for the entire company.

- 72. Management also jointly coordinated important events, such as Snow Wh亚s 50th anniversary in 1987 and Mickey's 60th birthday the following year. A meeting of all divisions generated novel ideas, coordinated schedules, and built commitment and excitement for the year's theme. Plans were then coordinated by the five-person corporate events department. "I think our biggest achievement to date," said Eisner in 1987, "has been bringing back to life an inherent Disney synergy that enables each part of our business to draw from, build upon, and bolster the others."33 Expanding into new businesses, regions, and audiences In the consumer products division, the Disney Stores (launched in 1987) pioneered the "retail-as- entertairunent" concept, generating sales per square foot at twice the average rate for retail. The stores were designed to evoke a sense of having stepped onto a Disney soundstage. W血e children were the target consumers, the stores' merchandise mix of toys and apparel also included high-end collectors'items for Disney's grown-up fans. The consumer products division also entered book, magazine, and record publishing. Hollywood Records, a pop music label, was founded in 1989 for less than $20 million, the cost of making a single Hollywood movie. In 1990, Disney established Disney Press, which published children's books, and in 1991, the company launched Hyperion Books, an adult publishing label that printed, among others, Ross Perot's biography. Disney also established new channels of distribution through direct-mail and catalog marketing.