Xi test-brs+boe

•Download as DOCX, PDF•

0 likes•476 views

Class test for CBSE class XI Accountancy.

Recommended

More Related Content

Viewers also liked

Viewers also liked (15)

Similar to Xi test-brs+boe

Similar to Xi test-brs+boe (20)

Recently uploaded

Recently uploaded (20)

Xi test-brs+boe

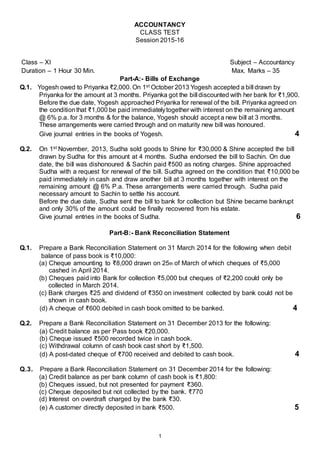

- 1. 1 ACCOUNTANCY CLASS TEST Session 2015-16 Class – XI Subject – Accountancy Duration – 1 Hour 30 Min. Max. Marks – 35 Part-A:- Bills of Exchange Q.1. Yogesh owed to Priyanka ₹2,000. On 1st October 2013 Yogesh accepted a bill drawn by Priyanka for the amount at 3 months. Priyanka got the bill discounted with her bank for ₹1,900. Before the due date, Yogesh approached Priyanka for renewal of the bill. Priyanka agreed on the conditionthat ₹1,000 be paid immediatelytogether with interest on the remaining amount @ 6% p.a. for 3 months & for the balance, Yogesh should accept a new bill at 3 months. These arrangements were carried through and on maturity new bill was honoured. Give journal entries in the books of Yogesh. 4 Q.2. On 1st November, 2013, Sudha sold goods to Shine for ₹30,000 & Shine accepted the bill drawn by Sudha for this amount at 4 months. Sudha endorsed the bill to Sachin. On due date, the bill was dishonoured & Sachin paid ₹500 as noting charges. Shine approached Sudha with a request for renewal of the bill. Sudha agreed on the condition that ₹10,000 be paid immediately in cash and draw another bill at 3 months together with interest on the remaining amount @ 6% P.a. These arrangements were carried through. Sudha paid necessary amount to Sachin to settle his account. Before the due date, Sudha sent the bill to bank for collection but Shine became bankrupt and only 30% of the amount could be finally recovered from his estate. Give journal entries in the books of Sudha. 6 Part-B:- Bank Reconciliation Statement Q.1. Prepare a Bank Reconciliation Statement on 31 March 2014 for the following when debit balance of pass book is ₹10,000: (a) Cheque amounting to ₹8,000 drawn on 25th of March of which cheques of ₹5,000 cashed in April 2014. (b) Cheques paid into Bank for collection ₹5,000 but cheques of ₹2,200 could only be collected in March 2014. (c) Bank charges ₹25 and dividend of ₹350 on investment collected by bank could not be shown in cash book. (d) A cheque of ₹600 debited in cash book omitted to be banked. 4 Q.2. Prepare a Bank Reconciliation Statement on 31 December 2013 for the following: (a) Credit balance as per Pass book ₹20,000. (b) Cheque issued ₹500 recorded twice in cash book. (c) Withdrawal column of cash book cast short by ₹1,500. (d) A post-dated cheque of ₹700 received and debited to cash book. 4 Q.3. Prepare a Bank Reconciliation Statement on 31 December 2014 for the following: (a) Credit balance as per bank column of cash book is ₹1,800: (b) Cheques issued, but not presented for payment ₹360. (c) Cheque deposited but not collected by the bank. ₹770 (d) Interest on overdraft charged by the bank ₹30. (e) A customer directly deposited in bank ₹500. 5

- 2. 2 Q.4 From the following particulars prepare a Bank Reconciliation Statement in the books of Sh. J.P. Kansal as on 30th June 2014: I. Balance as per Pass Book on 30th June 2014 was ₹6,000 II. Out of total cheques amounting to ₹37,500 drawn by Sh. Kansal, Cheques aggregating ₹5,000 were encashed in June 2014, Cheques aggregating ₹4,000 were encashed in July 2014 and the rest have not been presented at all. III. Out of total Cheques amounting to ₹12,000 deposited, Cheques aggregating ₹7,500 were credited in June 2014, cheques aggregating ₹2,000 were credited in July 2014 and the rest have not been collected at all. IV. Bank has charged ₹27 as its commission for collecting outstation cheques and has Debited wrongly ₹2,400. V. A cheque of ₹1,200 was entered in the Cash Book in June 2014, but was sent to the Bank in July 2014. VI. A cheque of ₹13,300 paid into the bank was returned dishonoured but no intimation was received from the bank till June 2014. 6 Q.5 Credit Balance of ₹40,000 showed by the cash book of Atul on 31 Dec. 2014. (a) It was found that three cheques of ₹2,000, ₹5,000 and ₹8,000 deposited during the month of December, out of which ₹8000 were credited in the Pass Book on January 02, 2015. (b) Two cheques of ₹7,000 and ₹8,000 issued on December 28, were not presented for payment till January 03, 2015. (c) Bank had credited Atul for ₹325 as interest and had debited him with ₹50 as bank charges for which there were no corresponding entries in the Cash Book. (d) A cheque of ₹400 drawn on his saving account has been shown on current account. (e) One cheque issued by Mr. Atul of ₹500 on December 25, but it was not presented for payment whereas it was recorded twice in the Cash Book. (f) A Cheque of ₹780 credited in the passbook on March 28 being dishonoured is debited again in the passbook on Jan 01, 2015. There was no entry in the cash book about the dishonour of the cheque until 12 January 2015. Prepare a Bank Reconciliation Statement as on December 31, 2004. 6