Downloaded 2,249 times

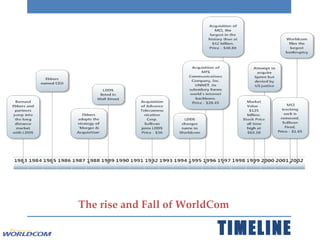

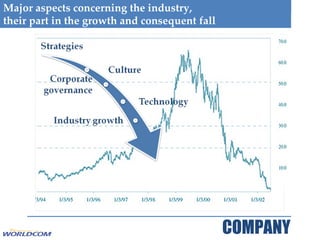

The document discusses the rise and fall of WorldCom, including its aggressive acquisition strategy, risky loans to executives, fraudulent accounting practices to inflate revenues and hide debts, and eventual bankruptcy. It analyzes WorldCom's financial ratios, z-score, and industry factors like the dot-com bubble burst that contributed to its decline. A whistleblower uncovered $3.8 billion in fraudulent line-cost accounting adjustments that hid expenses and misled investors.