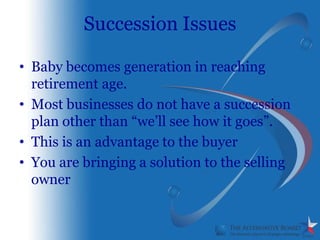

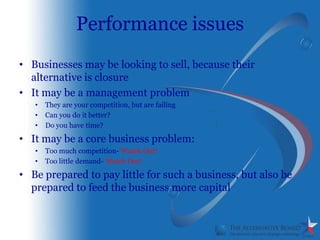

This document provides guidance on acquiring businesses through little or no cash outlay. It discusses evaluating if acquisition fits your strategy, acquiring businesses with succession, performance, or strategic issues, determining a fair price based on cash flows, negotiating a seller-financed deal structure, conducting thorough due diligence, and avoiding common traps in acquisitions. The key steps are evaluating acquisition opportunities, building a financial model, making a non-binding offer, performing due diligence, and structuring a seller-financed deal to acquire the business with little upfront cash.