Download to read offline

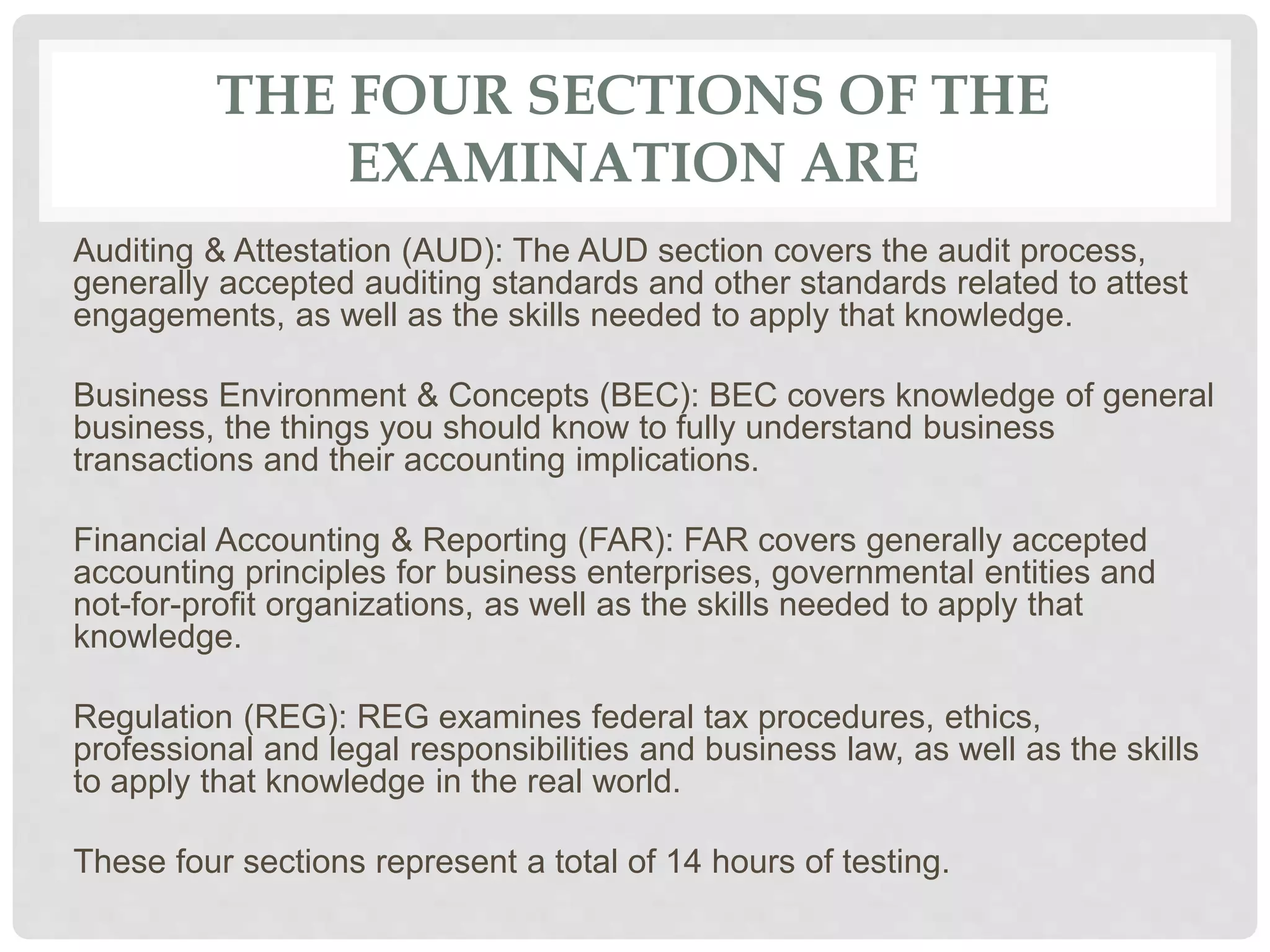

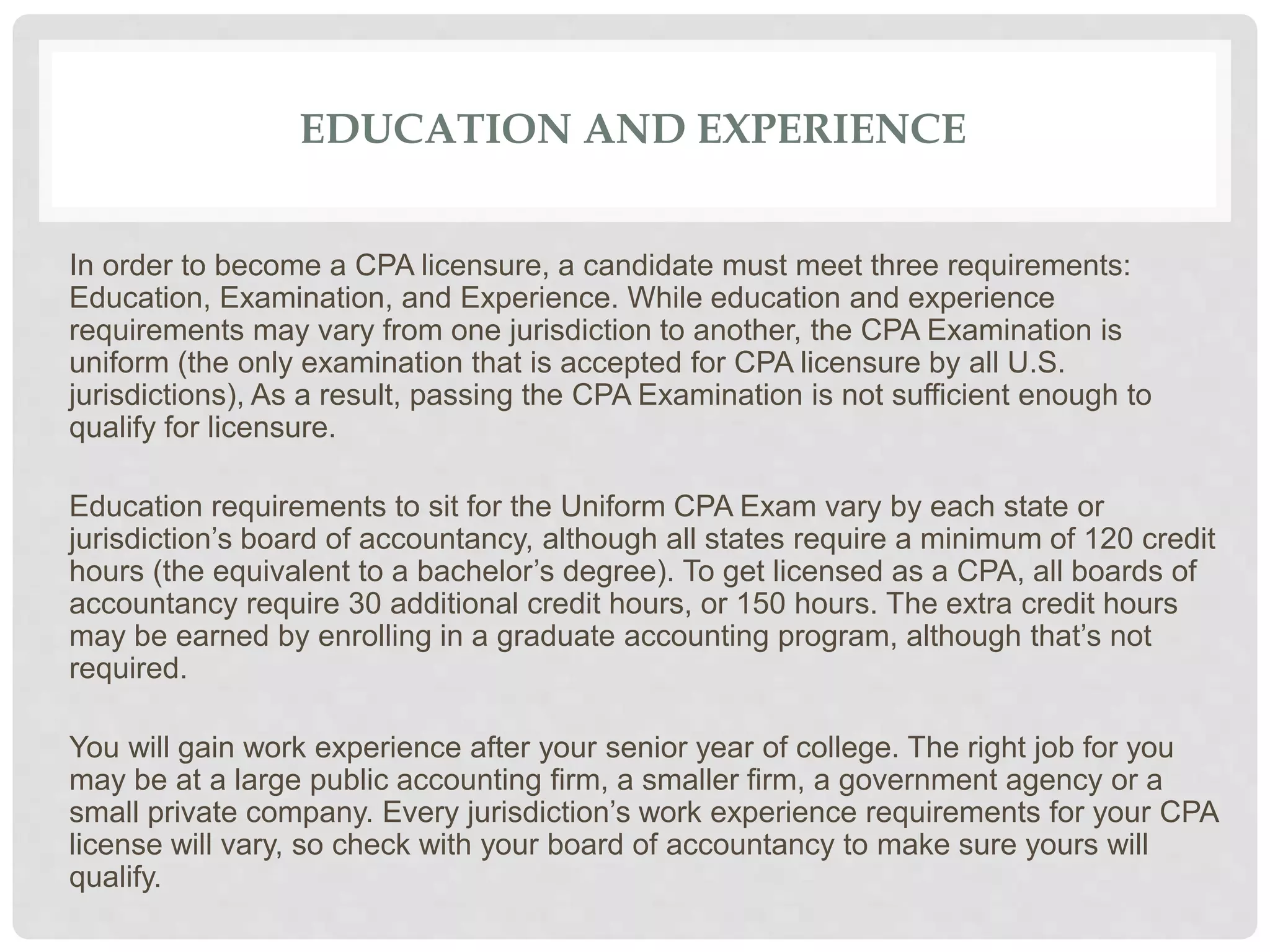

The Uniform CPA Examination is a standardized test used for licensure as a Certified Public Accountant in the U.S., ensuring candidates have necessary technical knowledge and skills for public protection. Established in 1917 and transitioning to a computer-based format in 2004, the exam consists of four sections covering auditing, business concepts, financial reporting, and regulation. Candidates must meet education and experience requirements, with varying criteria per state, before qualifying for the CPA license.