Download to read offline

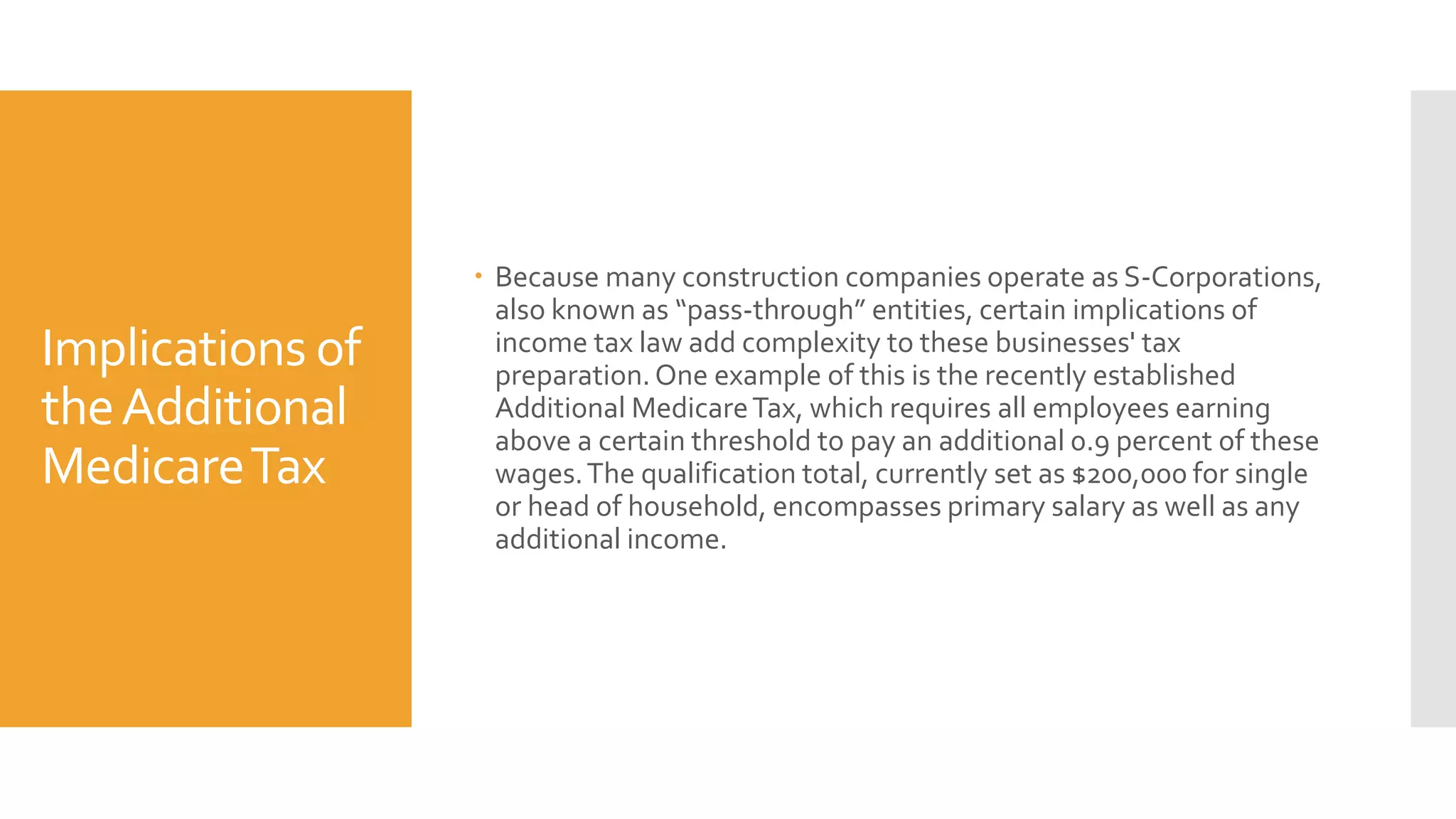

The document discusses the implications of the Additional Medicare Tax for construction companies that operate as S-corporations or partnerships. It notes that the tax requires employees earning over $200,000 to pay an additional 0.9% tax on wages. For partnerships and companies taxed as partnerships, all partners must now pay the 0.9% tax on all net taxable income earned by the company. However, income distributions from an S-corporation are not considered investment income and are not subject to the tax, though an owner-employee may owe it if other income sources exceed the limit.