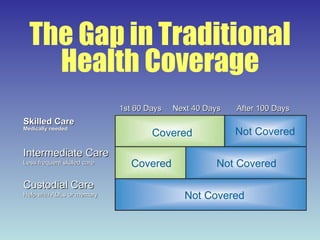

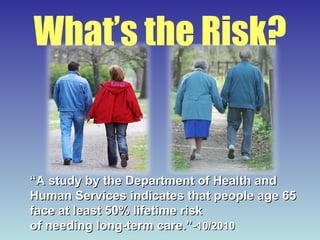

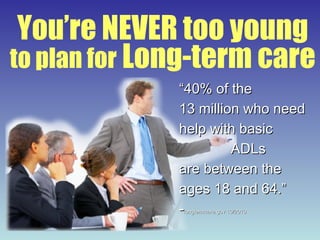

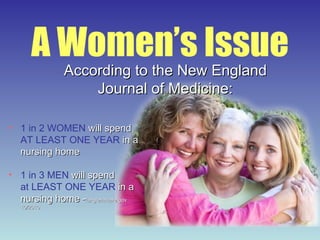

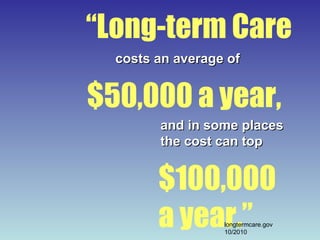

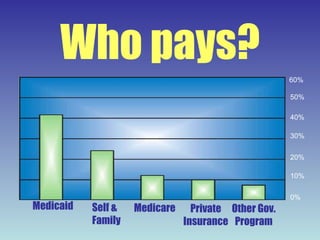

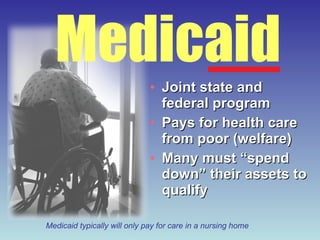

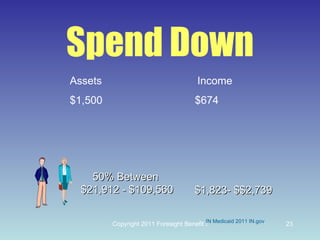

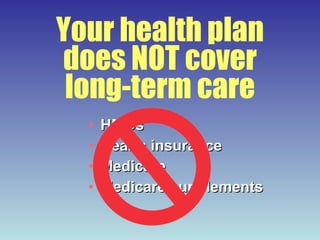

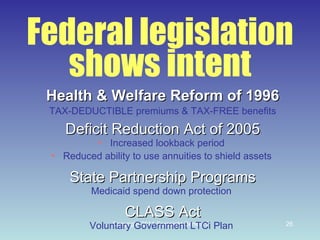

The document discusses long-term care planning and insurance. It notes that about half of people will need long-term care services, which can cost $50,000-$100,000 per year. However, traditional health insurance like Medicare does not cover long-term custodial care. Purchasing long-term care insurance can help cover these costs and close a gap in many retirement plans. The document provides an overview of long-term care insurance benefits and costs.

![A National Challenge… Long-Term Care A gap in health insurance exposes a hole in retirement planning... Michael E. Wright, CFP Wright Financial Advisors, LLC [email_address] Registered Representative of and securities offered through OneAmerica Securities, Inc., Advisor.9229 Delegates Row #190, Indianapolis, IN 46240,(317)573-3838, Member FINRA, SIPC, a Registered Investment Advisor. Insurance Representative of American United Life Insurance Company, AUL and other insurance companies. Wright Financial Advisors is not an affiliate of OneAmerica Securities or AUL and is not a Broker/Dealer or Registered InvestmentAdvisor .](https://image.slidesharecdn.com/wfa-ltc-employeeedworkshop-share-110502222348-phpapp01/85/Wfa-ltc-employee-ed-workshop-share-1-320.jpg)

![A National Challenge… Long-Term Care A gap in health insurance exposes a hole in retirement planning... Michael E. Wright, CFP Wright Financial Advisors, LLC [email_address] Registered Representative of and securities offered through OneAmerica Securities, Inc., Advisor.9229 Delegates Row #190, Indianapolis, IN 46240,(317)573-3838, Member FINRA, SIPC, a Registered Investment Advisor. Insurance Representative of American United Life Insurance Company, AUL and other insurance companies. Wright Financial Advisors is not an affiliate of OneAmerica Securities or AUL and is not a Broker/Dealer or Registered InvestmentAdvisor .](https://image.slidesharecdn.com/wfa-ltc-employeeedworkshop-share-110502222348-phpapp01/75/Wfa-ltc-employee-ed-workshop-share-1-2048.jpg)