Download to read offline

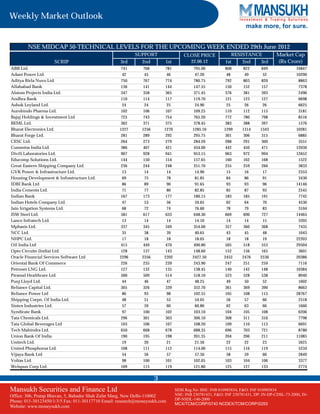

The weekly market outlook document provided a summary of market performance for the week ending June 22, 2012. Some key points: - Indian stock markets ended the week flat after gaining over 6% in the previous two weeks. Frontline indices saw marginal gains but extended their gaining streak to three weeks. - Sentiment was dampened after the RBI maintained interest rates, defying expectations of a cut. Inflation also rose slightly to 10.36% in May. - Technical support and resistance levels were provided for 30 Sensex stocks and 50 Nifty Midcap stocks to gauge the market outlook and inclination for the upcoming week.