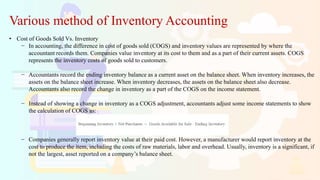

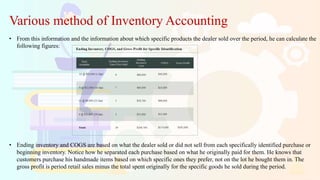

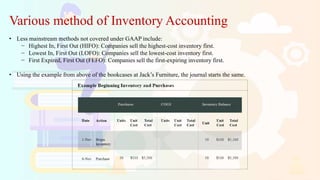

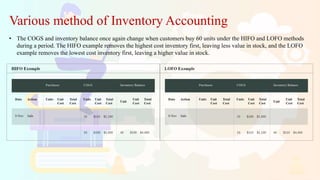

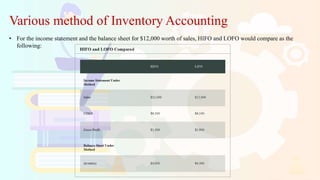

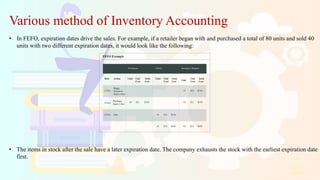

The document discusses various methods of inventory accounting, particularly inventory costing, which assigns costs to products and includes incidental fees. It explains key terms such as cost of goods sold (COGS) and identifies different accounting methods like FIFO, LIFO, and weighted average cost (WAC), along with their implications on financial statements. Additionally, it introduces less common methods like HIFO, LOFO, and FEFO that are not covered by GAAP.