DEFINITION OF FINANCIALSYSTEM

A financial system refers to a set of institutions, markets,

instruments, and services that facilitate the flow of funds between

savers (investors) and borrowers.

It plays a crucial role in mobilizing savings, allocating capital, and

enabling economic development.

3.

NATURE OF FINANCIALSYSTEM

Facilitates Fund Flow:

It ensures the smooth transfer of funds from surplus units (savers)

to deficit units (borrowers).

Intermediary-Based:

The system includes financial intermediaries such as banks,

insurance companies, and mutual funds which help bridge the gap

between investors and users of funds.

4.

Market-Oriented:

It comprises financialmarkets like the money market and capital market,

which allow for trading in financial instruments.

Regulated Structure:

It operates under a legal and regulatory framework set by authorities like

RBI, SEBI, and the Ministry of Finance.

Supports Economic Growth:

By allocating resources efficiently, it contributes to capital formation and

overall economic development.

5.

Dynamic in Nature:

Thefinancial system evolves over time with changes in economic

conditions, technology, and policies.

Includes Both Formal and Informal Sectors:

It encompasses organized institutions (like banks) and unorganized

sectors (like moneylenders in rural areas).

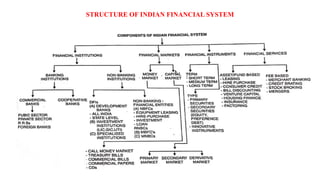

1. Financial Institutions

Theseare intermediaries that facilitate the flow of funds.

a. Banking Institutions (Organized Sector):

• Commercial Banks (Public, Private, Foreign)

• Cooperative Banks

• Regional Rural Banks (RRBs)

b. Non-Banking Financial Institutions (NBFIs):

• Insurance Companies (LIC, GIC)

• Development Financial Institutions (NABARD, SIDBI, EXIM Bank)

• Mutual Funds

• Pension Funds

8.

2. Financial Markets

Theseare platforms where financial assets are bought and sold.

a. Money Market (Short-term funds):

• Call Money Market

• Treasury Bills – debt securities-immediate financial needs

• Commercial Paper -unsecured short term –debt issued by corporations

• Certificates of Deposit – offered by banks and credit unions

b. Capital Market (Long-term funds):

• Primary Market (New issues of securities/ sale of securities to purchasers)

• Secondary Market (Stock Exchanges like BSE, NSE)

9.

Money Market

Money marketis a market for dealing with financial assets and securities

which have a maturity period of up to one year.

Capital Market

Capital market is a market for financial assets which havea long or

indefinite maturity. Generally, it deals with long –term securities which have

a maturity period of above one year.

10.

3. Financial Instruments

Theseare the tools used for raising funds or investment.

• Equity Shares

• Debentures/Bonds

• Treasury Bills

• Commercial Paper

• Derivatives (Options, Futures)-agreement set between 2 parties

11.

4. Financial Services

Theseinclude services that support financial transactions.

• Banking Services (Loans, Deposits)

• Insurance Services

• Investment Services

• Credit Rating

• Asset Management

• Leasing and Hire Purchase

12.

FUNCTIONS OF THEFINANCIAL SYSTEM

The financial system performs several crucial functions that support economic

development and financial stability in a country. Below are the main functions:

1. Mobilization of Savings

• Encourages individuals and businesses to save money.

• Converts idle savings into productive investments.

• Example: Banks collect savings through deposits and lend to borrowers.

13.

2. Facilitation ofInvestment

• Helps channel savings into profitable investment opportunities.

• Provides capital for business expansion and infrastructure.

• Example: Investors buy shares or bonds through the stock market.

3. Credit Allocation

• Distributes credit to various sectors of the economy (industry, agriculture,

services).

• Ensures balanced development by providing funds where needed.

14.

4. Financial Intermediation

•Acts as a link between savers and borrowers through intermediaries like banks,

NBFCs, mutual funds.

• Example: A bank collects deposits from the public and gives loans to industries.

5. Liquidity Provision

• Offers mechanisms to convert financial assets into cash quickly and easily.

• Example: Stocks can be sold on the stock exchange to generate instant liquidity.

15.

6. Risk Management

•Provides financial instruments (insurance, derivatives) to manage and spread risk.

• Example: Insurance policies protect against loss or damage.

7. Efficient Payment System

• Ensures smooth transactions via digital banking, online transfers, UPI, NEFT, RTGS, etc.

8. Price Discovery

• Helps determine the fair price of financial assets based on supply and demand in markets.

• Example: Share prices on NSE/BSE are decided through trading activity.

16.

9. Regulation andControl

• Regulated by authorities like RBI, SEBI to ensure transparency, investor

protection, and stability.

10. Promotes Economic Development

• By supporting investment, entrepreneurship, and employment generation, it

helps boost GDP and national progress.

17.

🌱EVOLUTION AND DEVELOPMENTOF INDIAN FINANCIAL SYSTEM

The Indian financial system has evolved gradually over time, adapting to economic

needs, policy changes, and global developments.

️

🏛️1. Pre-Independence Period (Before 1947)

• Primitive Financial System – Mainly unorganized moneylenders and indigenous

bankers (e.g., shroffs, sahukars).

• Few organized institutions – Presidency Banks (e.g., Bank of Bengal, 1806), Imperial

Bank of India (1921).

• Lack of regulation, poor outreach, and limited services.

18.

2. Post-Independence Phase(1947–1968)

• Formation of Reserve Bank of India (RBI) in 1935 became the backbone of

monetary regulation.

• Nationalization of Imperial Bank → State Bank of India (1955).

• Establishment of development banks:

• IFCI (1948)

• LIC (1956)

• UTI (1964)

• Focus on industrial and agricultural development.

19.

The Imperial Bankof India, which was a major banking institution during

British rule, was nationalized in 1955.

It was renamed as the State Bank of India (SBI).

This move was taken to expand banking services, especially in rural and

semi-urban areas, and to align banking operations with national economic

goals.

SBI became the largest public sector bank in India and played a vital role

in supporting agricultural, industrial, and rural development.

20.

Establishment of DevelopmentBanks

Development banks are financial institutions created to provide long-term

capital for the development of various sectors of the economy. Here's a brief

look at each:

a) IFCI (1948) – Industrial Finance Corporation of India

• Established as the first development bank in India.

• Its purpose was to provide medium and long-term finance to large-scale

industries.

• Played a key role in supporting industrial development after independence.

21.

LIC (1956) –Life Insurance Corporation of India

• Formed by nationalizing all private life insurance companies.

• LIC collects premiums from policyholders and invests in government

and industrial securities.

• It has been a major source of funds for national development projects

and public sector undertakings.

22.

UTI (1964) –Unit Trust of India

• First mutual fund organization in India.

• Established to encourage savings and investments among small

investors by pooling money and investing in capital markets.

• Played a key role in developing the Indian capital market.

23.

3. Nationalization andExpansion (1969–1990)

• 1969: 14 major commercial banks nationalized.

• 1980: 6 more banks nationalized → greater public sector presence.

• Establishment of:

• Regional Rural Banks (1975)

• NABARD (1982)

• SEBI (1988)

• Strong emphasis on financial inclusion and rural development.

24.

1. Nationalization ofBanks

• 1969: Nationalization of 14 Major Commercial Banks

• The Government of India nationalized 14 private sector banks on 19 July 1969.

• This step was taken under the leadership of Prime Minister Indira Gandhi.

• Objective: To ensure that banking services reach the rural and

underdeveloped areas and support agriculture, small industries, and exports.

• Outcome: Banks began focusing on priority sector lending such as agriculture,

small-scale industries, and education.

25.

1980: Nationalization of6 More Banks

• In April 1980, 6 more commercial banks were nationalized.

• This increased the public sector’s share in the banking industry.

• The aim was to strengthen the government's control over credit delivery

and financial planning.

26.

2. Establishment ofKey Financial Institutions

• Regional Rural Banks (RRBs) – 1975

• Introduced to bridge the gap between commercial banks and cooperative societies.

• RRBs were established to provide credit and financial services to the rural poor,

particularly farmers, agricultural laborers, and small entrepreneurs.

• Jointly owned by:

• Central Government (50%)

• State Government (15%)

• Sponsor Bank (35%)

27.

NABARD – NationalBank for Agriculture and Rural Development (1982)

• Apex development bank for agriculture and rural development.

• Formed by transferring the agricultural credit functions of RBI and refinance

functions of the Agricultural Refinance and Development Corporation (ARDC).

• Plays a crucial role in:

• Refinancing rural credit institutions

• Promoting rural infrastructure

• Supervising cooperative banks and RRBs

28.

SEBI – Securitiesand Exchange Board of India (1988, statutory in 1992)

• Established in 1988 (got statutory powers in 1992).

• Acts as the regulatory authority for capital markets in India.

• Main functions:

• Regulating stock exchanges and securities market

• Protecting investors' interests

• Preventing fraudulent activities in the market

29.

4. Liberalization andReforms Era (1991 Onwards)

• Major economic reforms under LPG Policy (Liberalization, Privatization,

Globalization).

• Entry of private and foreign banks.

• Establishment of NSE (1992), NSDL(National Securities Depository Limited),

Credit Rating Agencies.

• Capital market reforms and better regulatory structure via SEBI.

• Introduction of modern financial instruments (derivatives, mutual funds).

30.

5. Digital &Inclusive Finance (2000s–Present)

• Growth of digital banking: NEFT, RTGS, IMPS, UPI.

• Launch of Jan Dhan Yojana (2014): financial inclusion mission.

• Rise of Fintech companies, mobile wallets, digital lending.

• RBI promoting digital currency (CBDC) and tightening regulations for

NBFCs.

• Expansion of insurance, mutual fund penetration, and retail investors in

stock markets.

31.

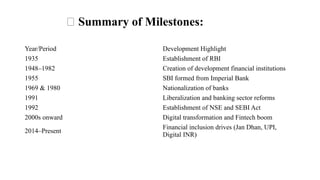

Year/Period Development Highlight

1935Establishment of RBI

1948–1982 Creation of development financial institutions

1955 SBI formed from Imperial Bank

1969 & 1980 Nationalization of banks

1991 Liberalization and banking sector reforms

1992 Establishment of NSE and SEBI Act

2000s onward Digital transformation and Fintech boom

2014–Present

Financial inclusion drives (Jan Dhan, UPI,

Digital INR)

📌 Summary of Milestones:

32.

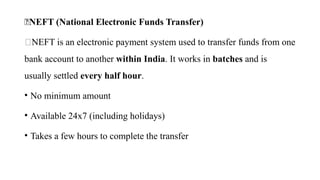

🏦NEFT (National ElectronicFunds Transfer)

🔹NEFT is an electronic payment system used to transfer funds from one

bank account to another within India. It works in batches and is

usually settled every half hour.

• No minimum amount

• Available 24x7 (including holidays)

• Takes a few hours to complete the transfer

33.

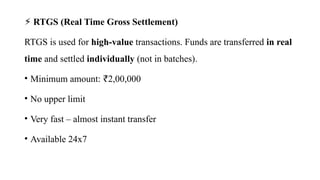

⚡ RTGS (RealTime Gross Settlement)

RTGS is used for high-value transactions. Funds are transferred in real

time and settled individually (not in batches).

• Minimum amount: 2,00,000

₹

• No upper limit

• Very fast – almost instant transfer

• Available 24x7

34.

FINANCIAL SYSTEM ANDECONOMIC DEVELOPMENT

Mobilization of Savings

Efficient Allocation of Resources

Capital Formation

Encourages Investment

Supports Trade and Commerce

Promotes Financial Inclusion

Stabilizes the Economy

Boosts Government Revenue

35.

MAJOR REFORMS SINCE1991: LPG

The Liberalization, Privatization, and Globalization (LPG) policy

initiated in 1991 transformed the Indian financial system significantly.

These reforms were introduced to overcome the balance of payment crisis

and promote economic growth.

36.

1. Liberalization

Removing governmentrestrictions to create a free and competitive market economy.

Key Reforms:

• Interest rate deregulation – Market-driven rates replaced fixed rates.

• Reduction of CRR and SLR – More funds for lending.

• Introduction of private sector banks – ICICI Bank, HDFC Bank, etc.

• Liberalization of capital markets – Free pricing of securities.

• Introduction of online trading – NSE, BSE modernization.

37.

🏢 2. Privatization

Encouragingprivate sector participation in economic activities.

Key Reforms:

• Disinvestment of public sector undertakings (PSUs).

• Entry of private players in banking, insurance, and mutual funds.

• Listing of PSUs in stock exchanges to improve accountability.

• Reduction in government monopoly in key sectors.

38.

🌍 3. Globalization

Integratingthe Indian economy with the global economy.

Key Reforms:

• Foreign Direct Investment (FDI) allowed in various sectors.

• Foreign Institutional Investors (FIIs) permitted in capital markets.

• Convertibility of Indian rupee (partial capital account convertibility).

• Improved forex management and liberal trade policies.

39.

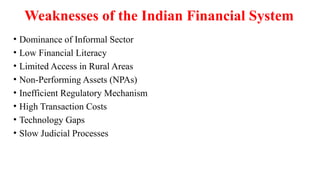

Weaknesses of theIndian Financial System

• Dominance of Informal Sector

• Low Financial Literacy

• Limited Access in Rural Areas

• Non-Performing Assets (NPAs)

• Inefficient Regulatory Mechanism

• High Transaction Costs

• Technology Gaps

• Slow Judicial Processes

40.

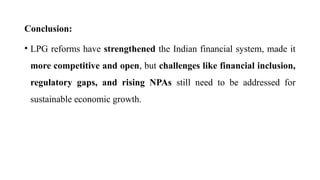

Conclusion:

• LPG reformshave strengthened the Indian financial system, made it

more competitive and open, but challenges like financial inclusion,

regulatory gaps, and rising NPAs still need to be addressed for

sustainable economic growth.