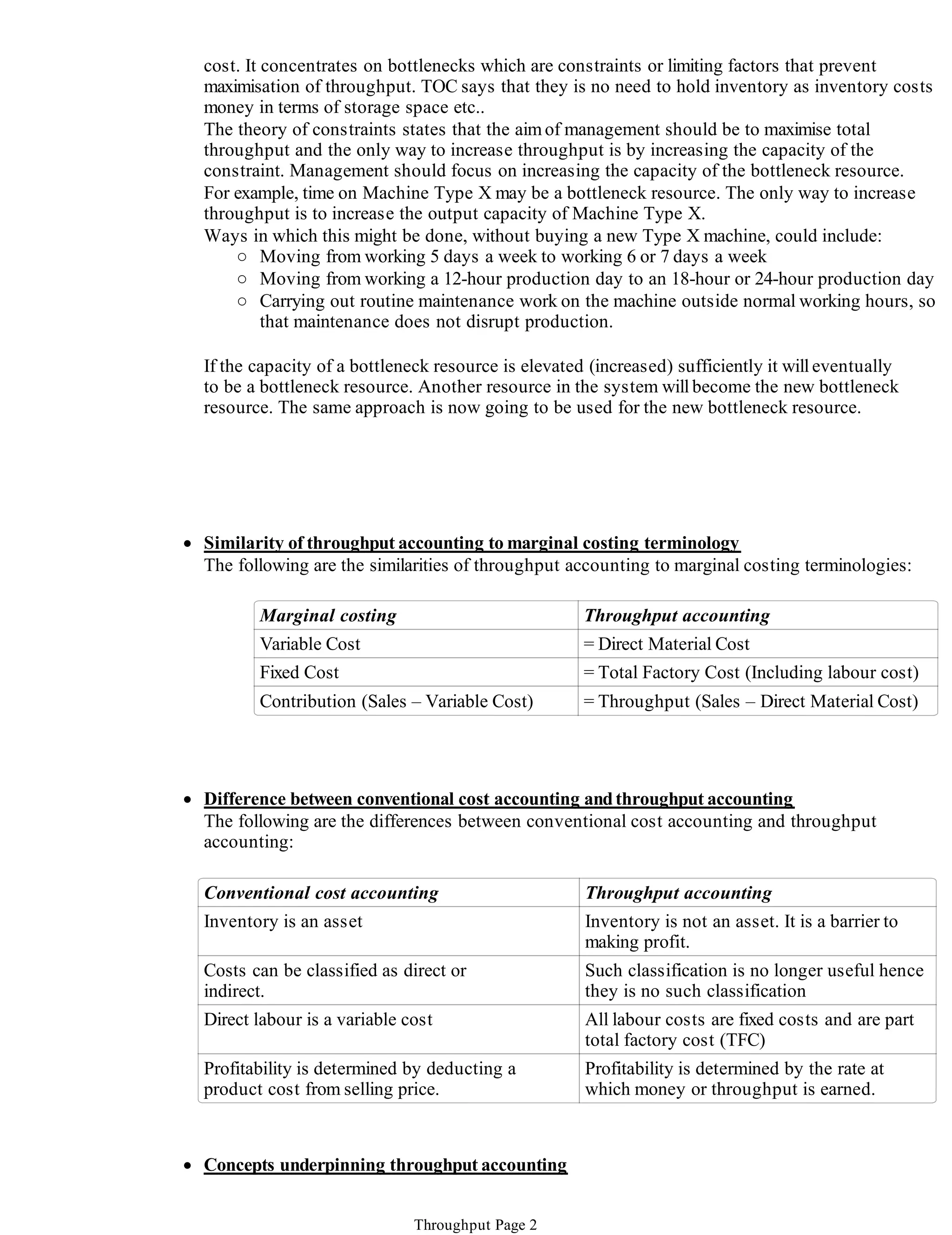

Throughput accounting focuses on maximizing throughput, which is defined as sales minus material costs. It recognizes direct materials as the only variable cost, and classifies all other direct costs like labor as fixed costs. A key concept is the bottleneck resource, which is the limiting factor that prevents higher output. The objective is to maximize throughput by fully utilizing the bottleneck resource. The theory of constraints states that management should focus on increasing the capacity of the bottleneck to improve throughput. Throughput accounting calculates ratios to evaluate productivity and identify ways to increase throughput, such as by raising prices, improving efficiency, or reducing costs.