This document discusses private equity, including:

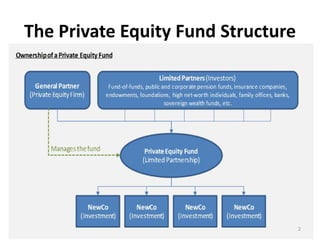

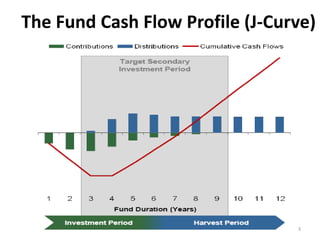

1. It outlines the private equity fund structure and cash flow profile known as the "J-curve".

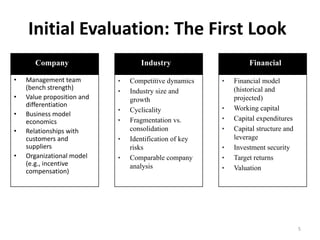

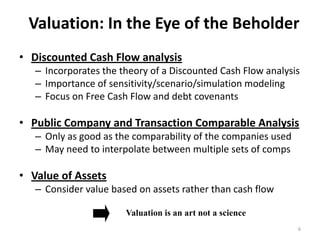

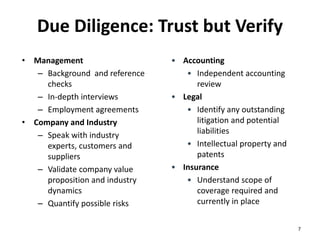

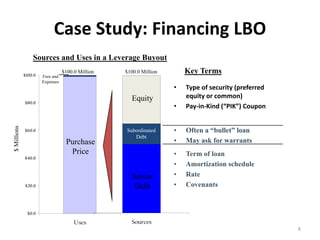

2. The investment process includes initial evaluation, valuation, due diligence, and case studies of financing leveraged buyouts.

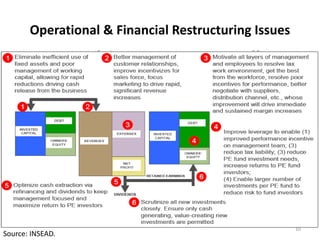

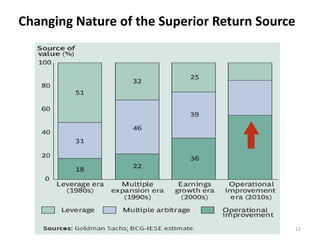

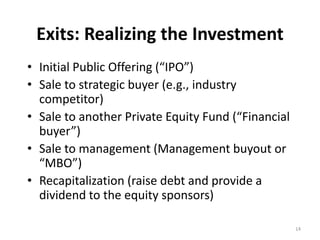

3. Value creation strategies are discussed like adding board members and management, acquisitions, and operational/financial restructuring. Exits like IPOs and sales are also covered.

![Contractual risks in pe invsts dr[1]. kishore - prmia](https://cdn.slidesharecdn.com/ss_thumbnails/contractualrisksinpeinvsts-dr1-kishore-prmia-130529155720-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)