Downloaded 43 times

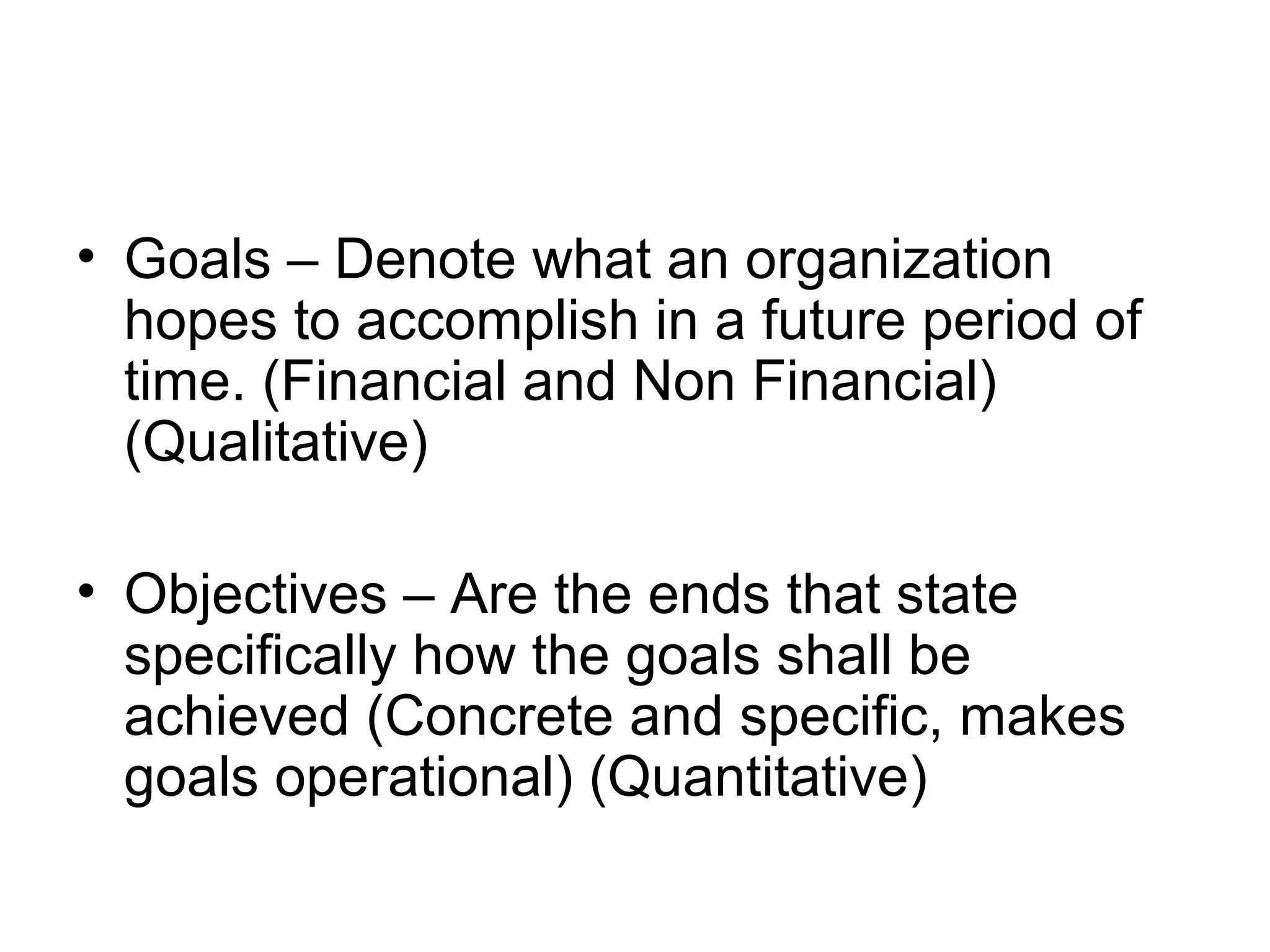

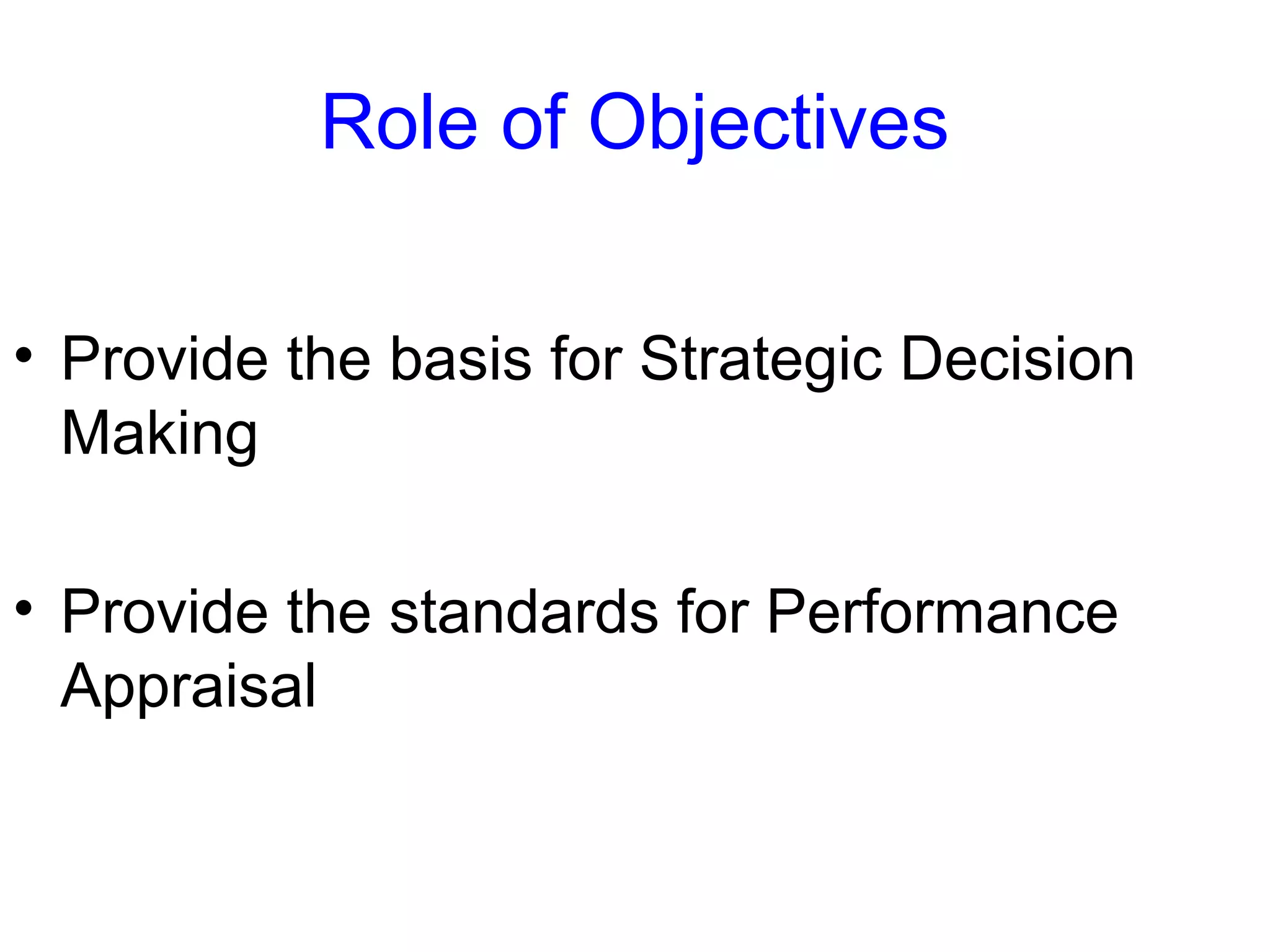

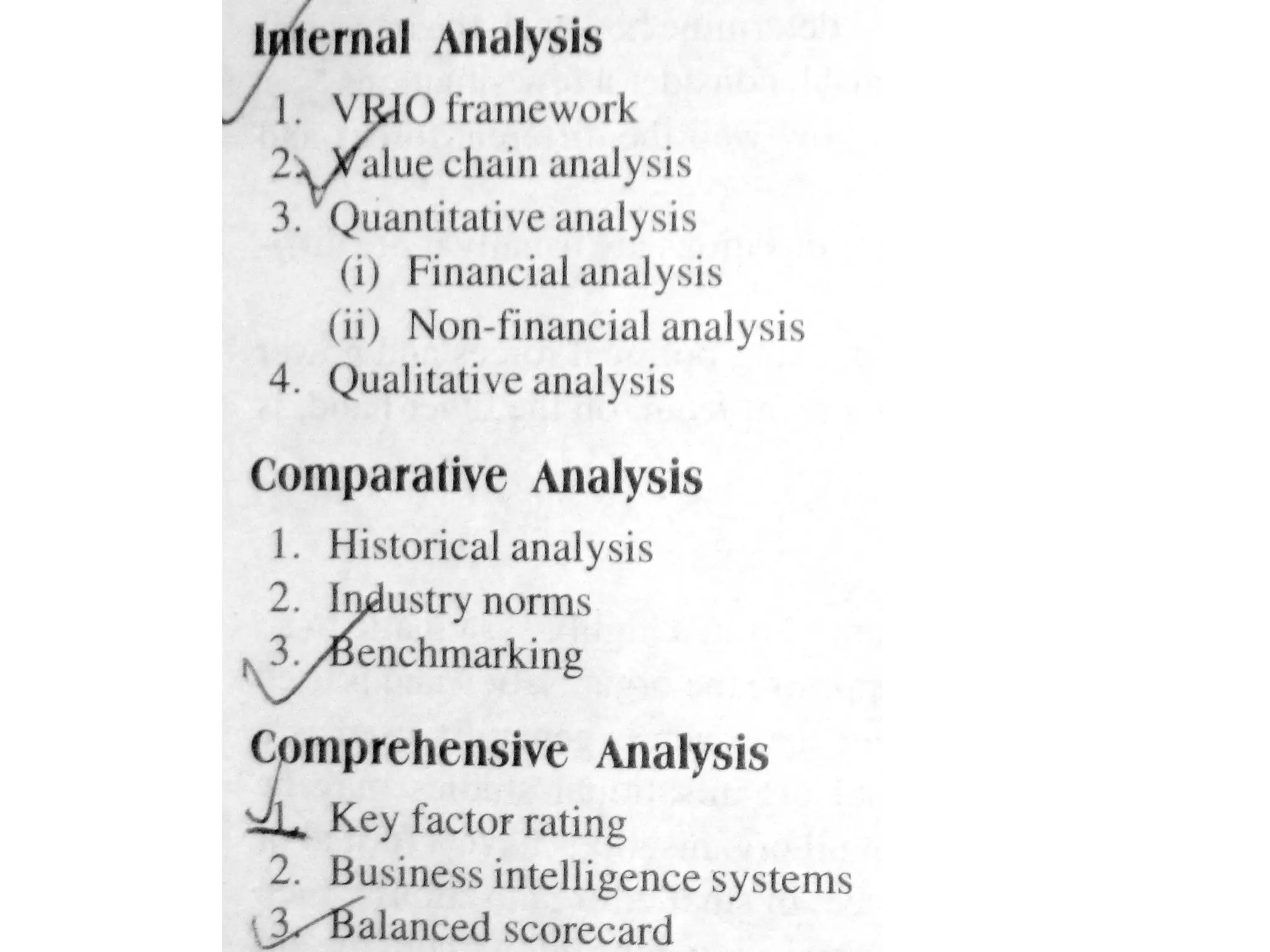

The document discusses goals, objectives, and organizational capabilities for strategic planning. It defines goals as qualitative and objectives as quantitative and specific. Objectives provide the basis for strategic decision making and performance appraisal. Organizational capabilities include financial, marketing, operations, personnel, information management, and general management factors. Methods for assessing capabilities include internal analysis using the VRIO framework, value chain analysis, quantitative analysis like ratios and benchmarks, and comprehensive analysis using tools like the balanced scorecard.

Explains the distinction between goals (future aspirations) and objectives (specific means). Highlights the role of objectives in strategic decision-making.

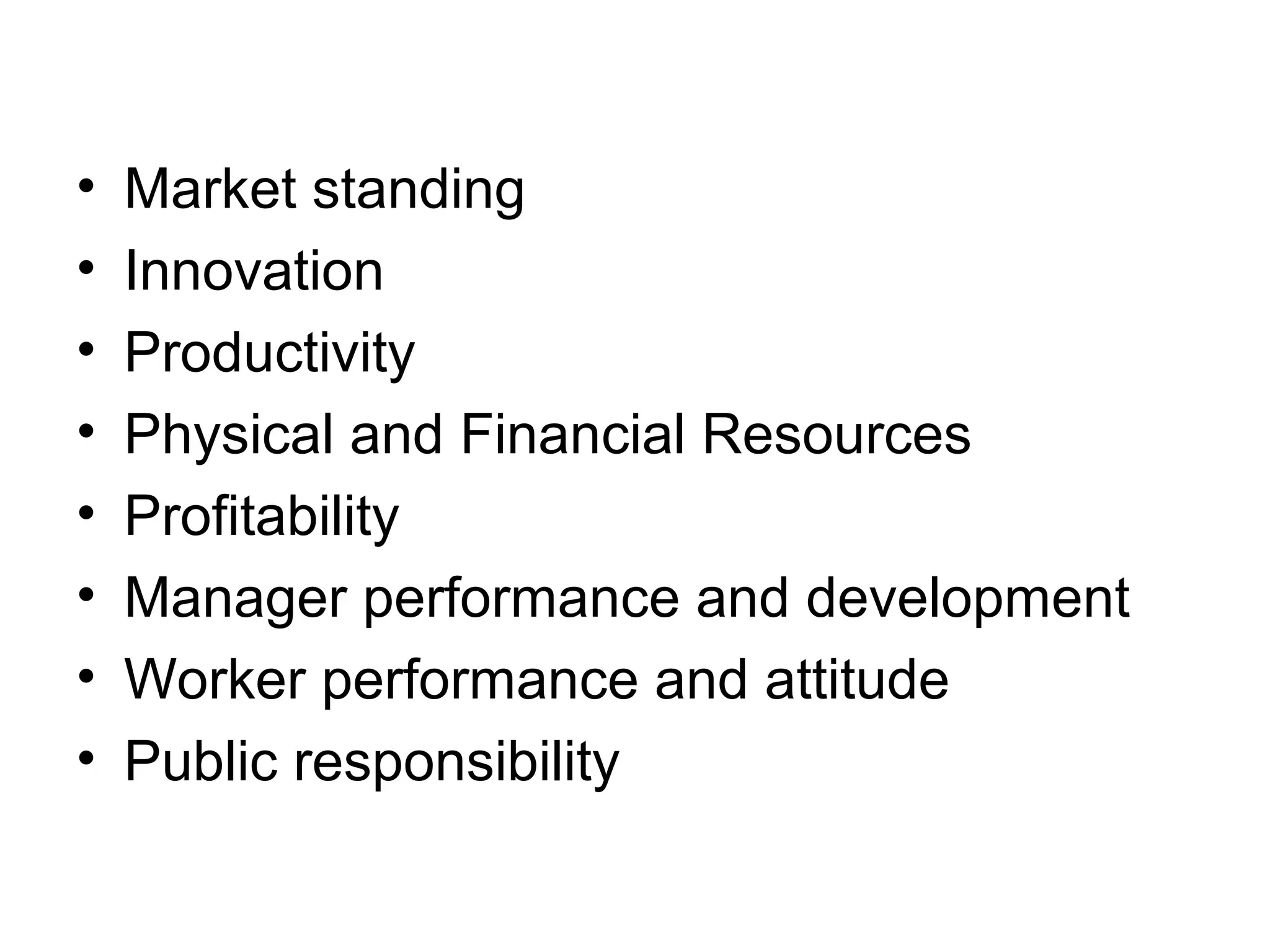

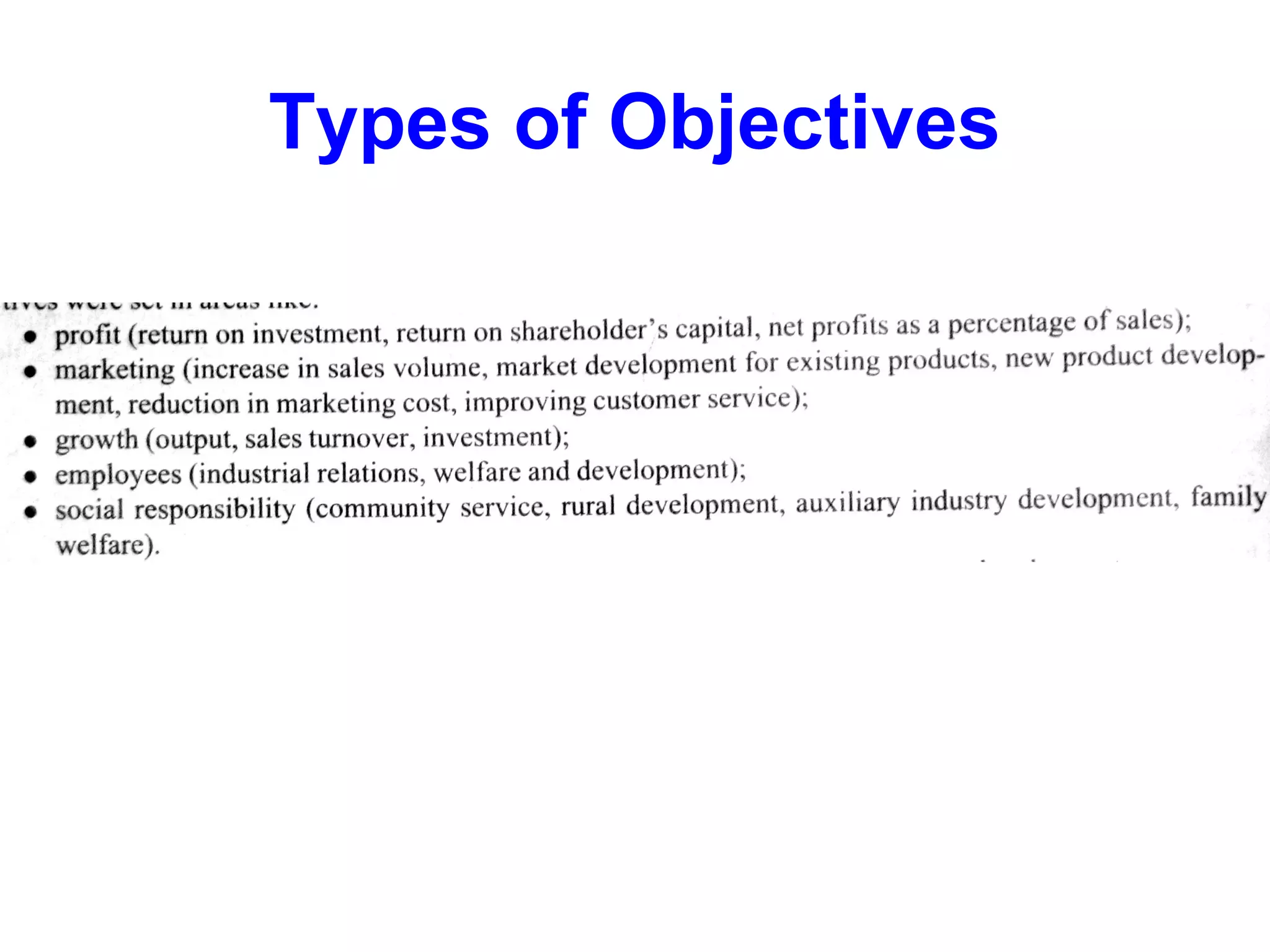

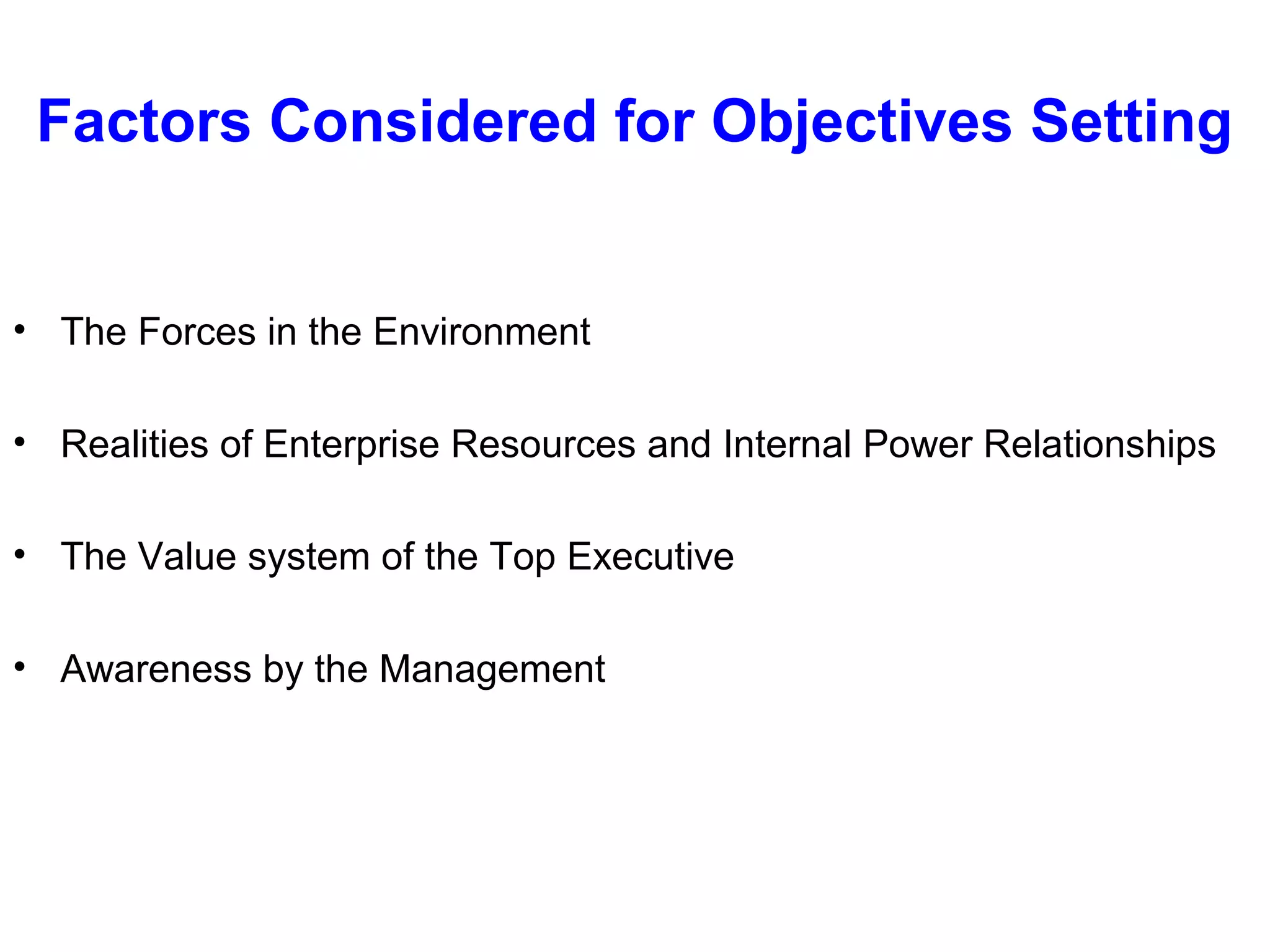

Discusses key areas for setting objectives: market standing, innovation, productivity, and resource management. Outlines environmental and internal factors influencing objectives.

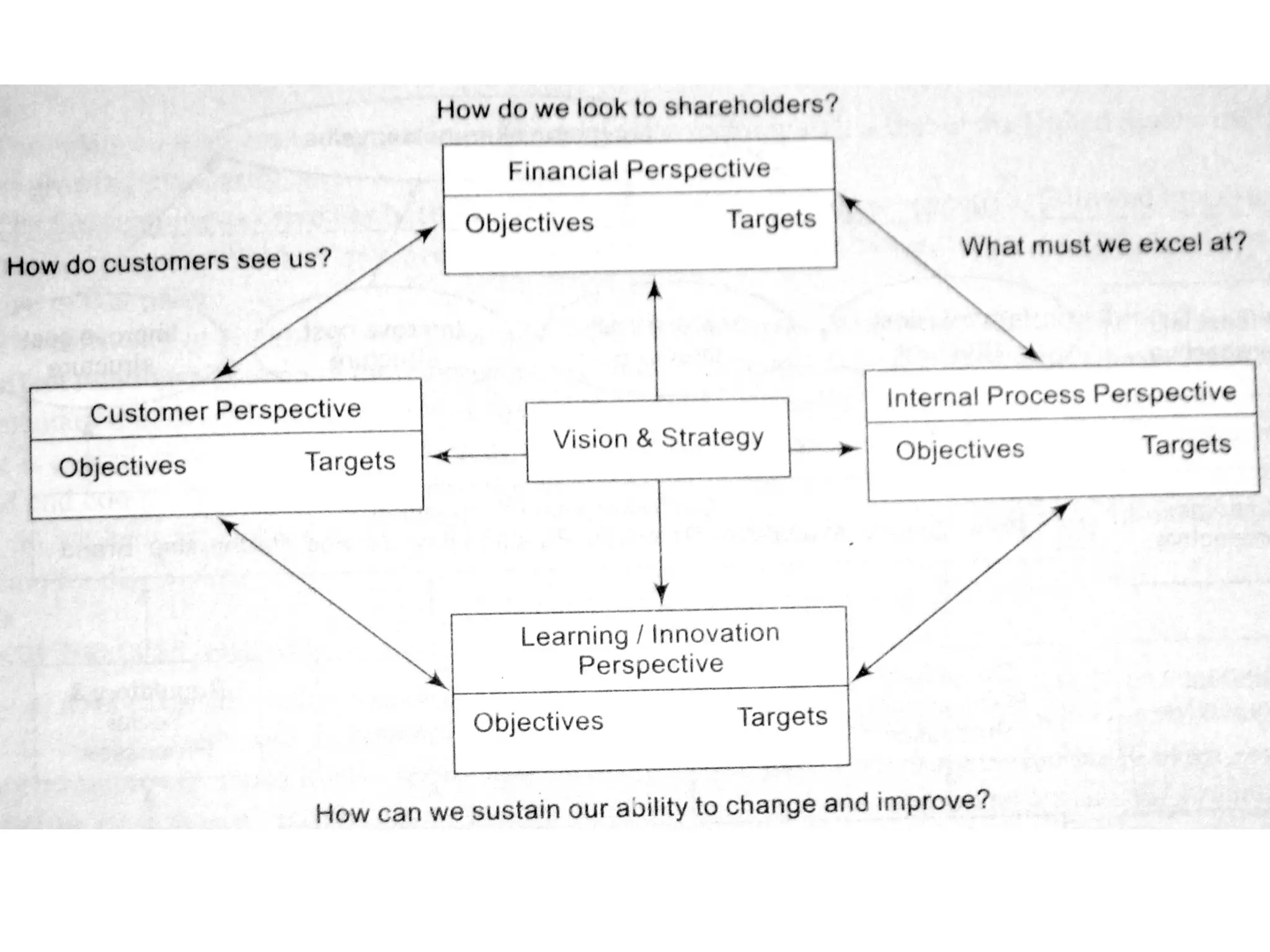

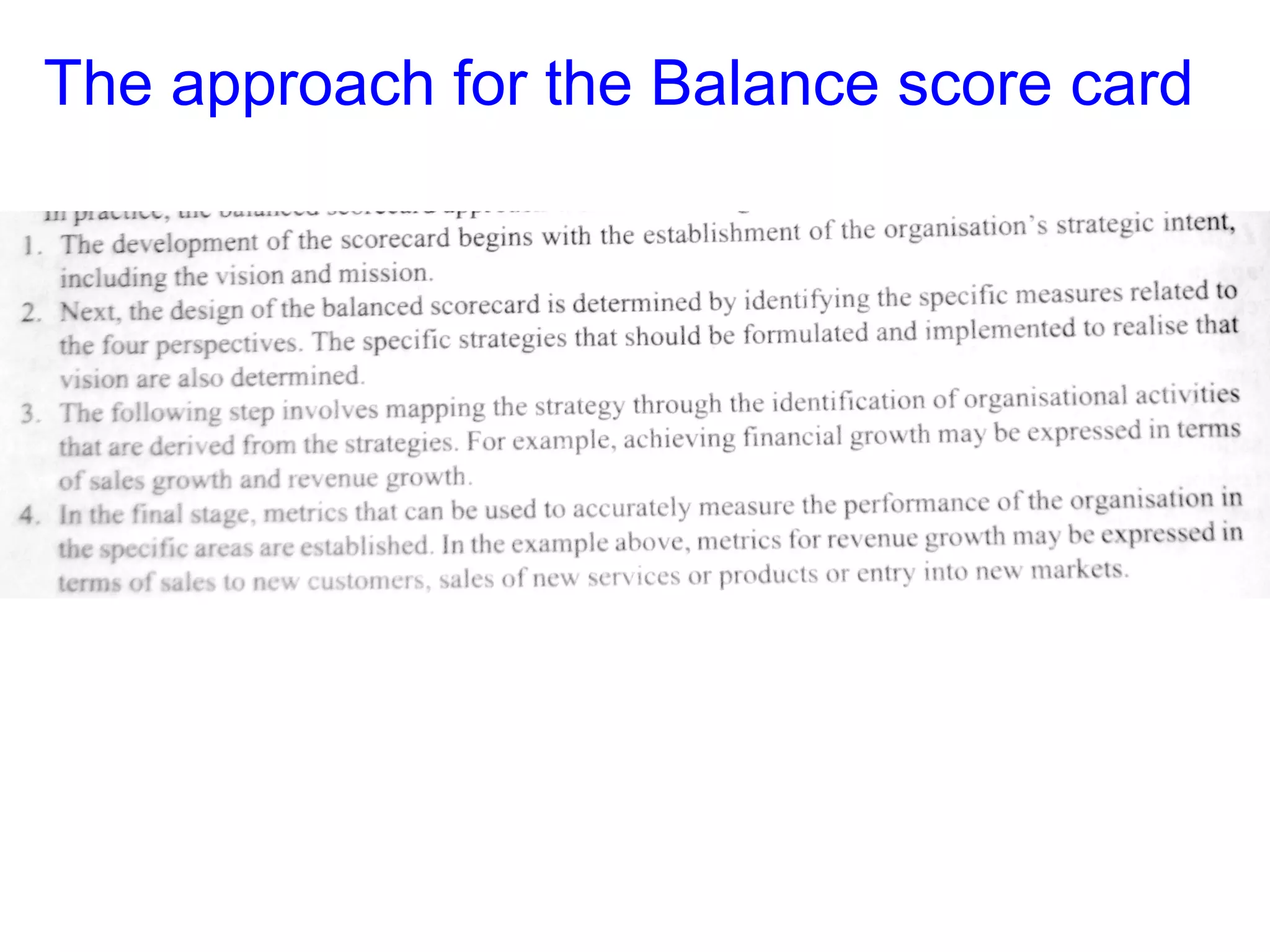

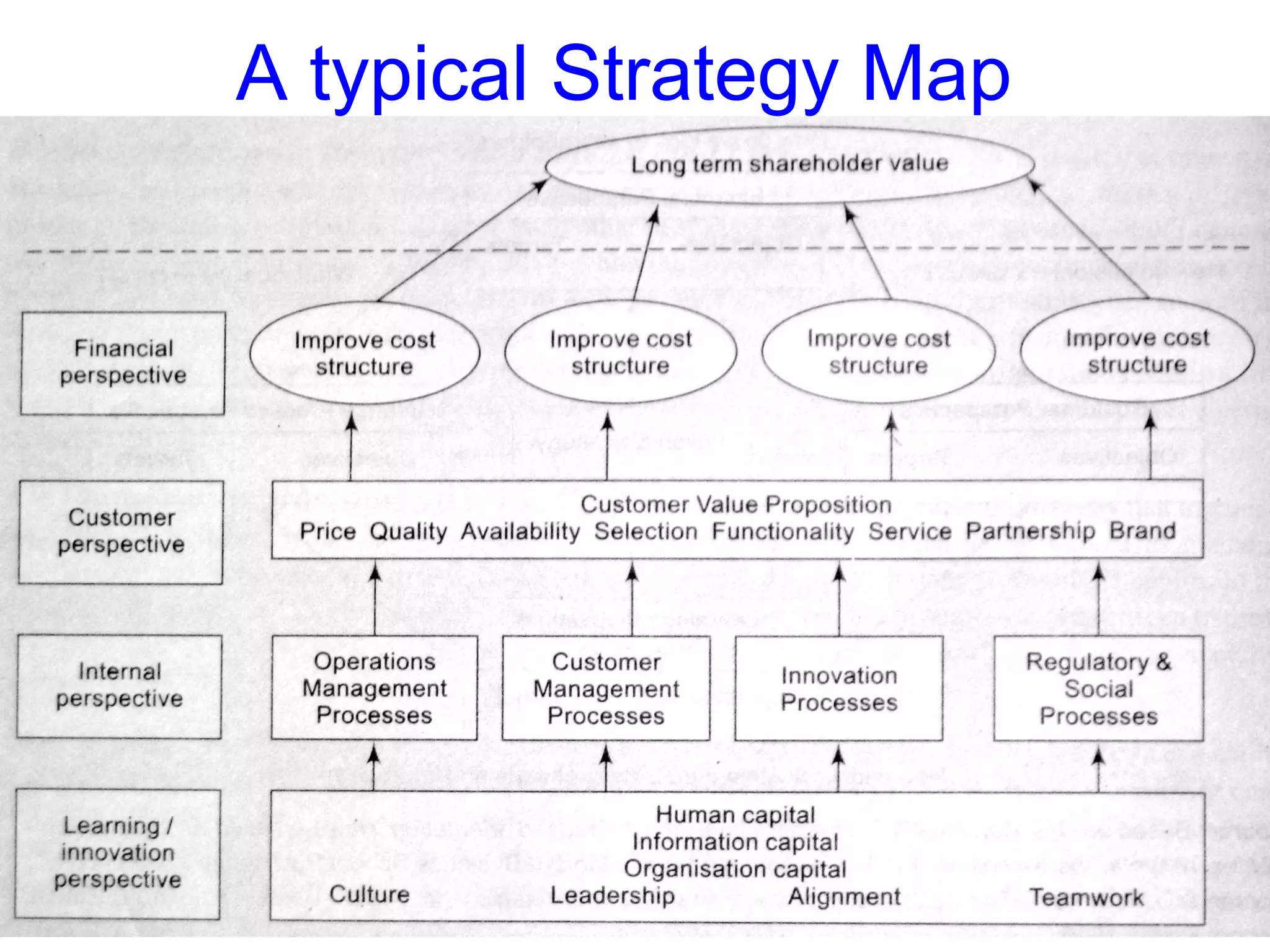

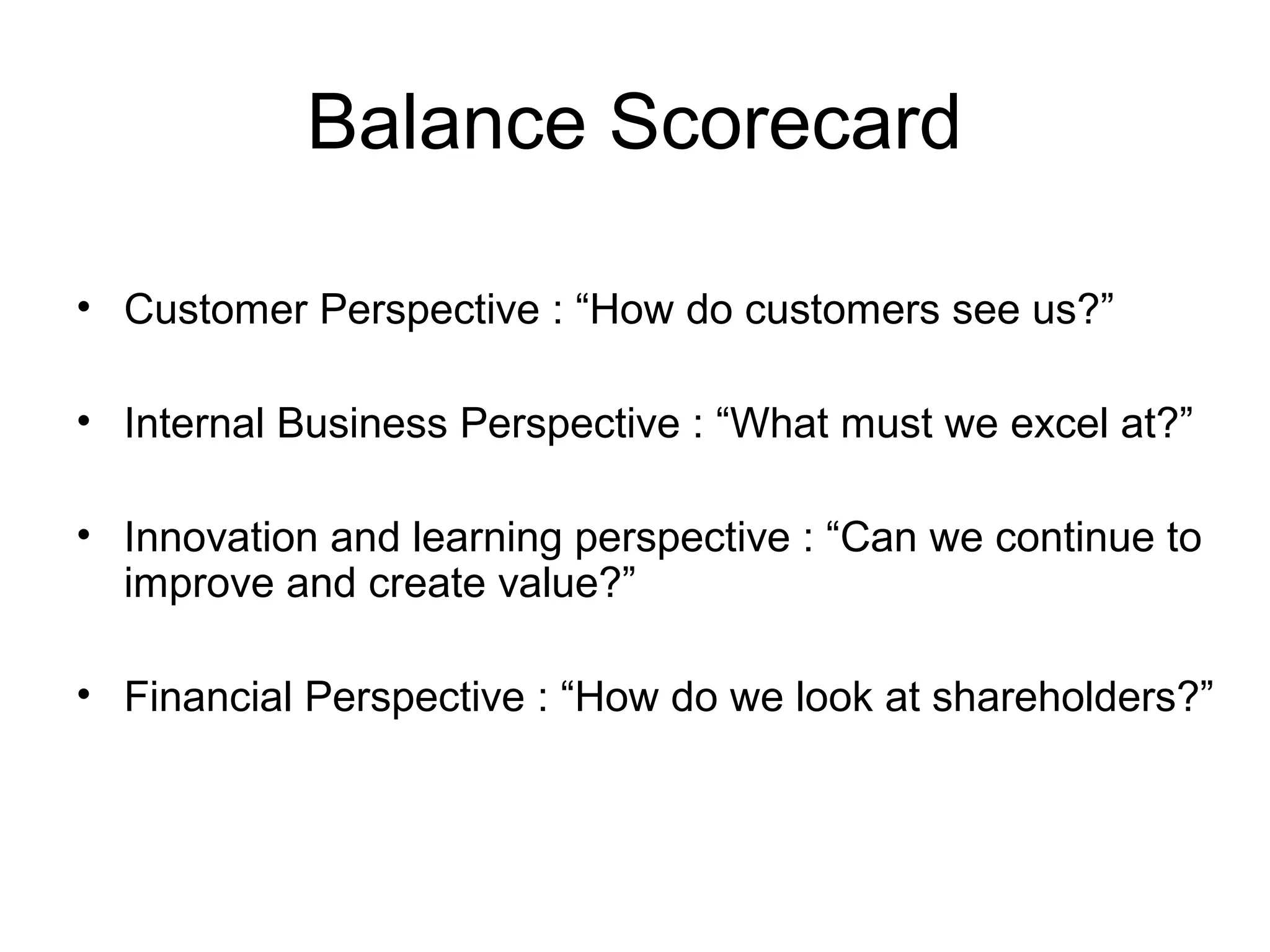

Introduces the Balanced Scorecard as a strategic planning tool and the approach to building a strategy map.

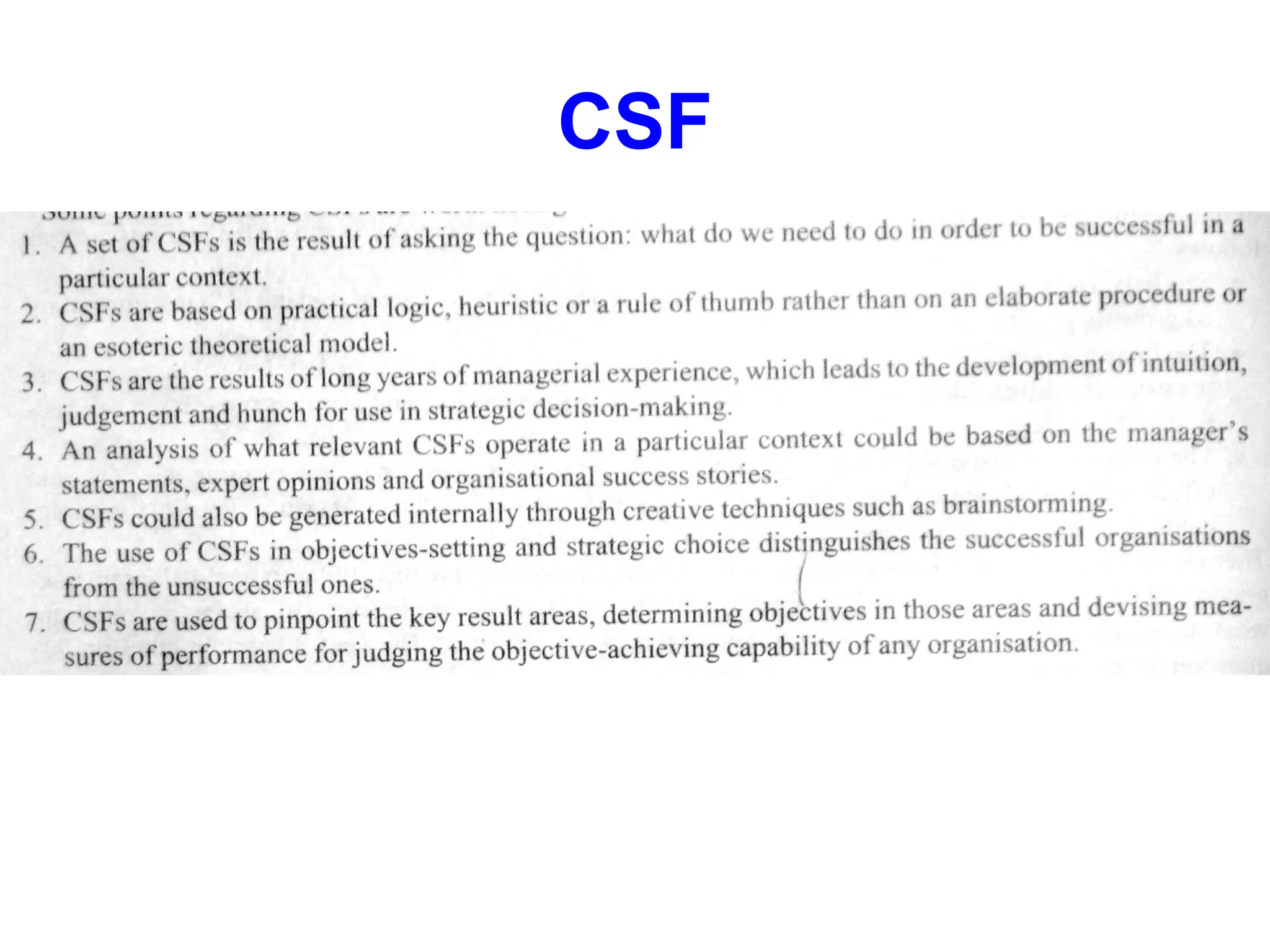

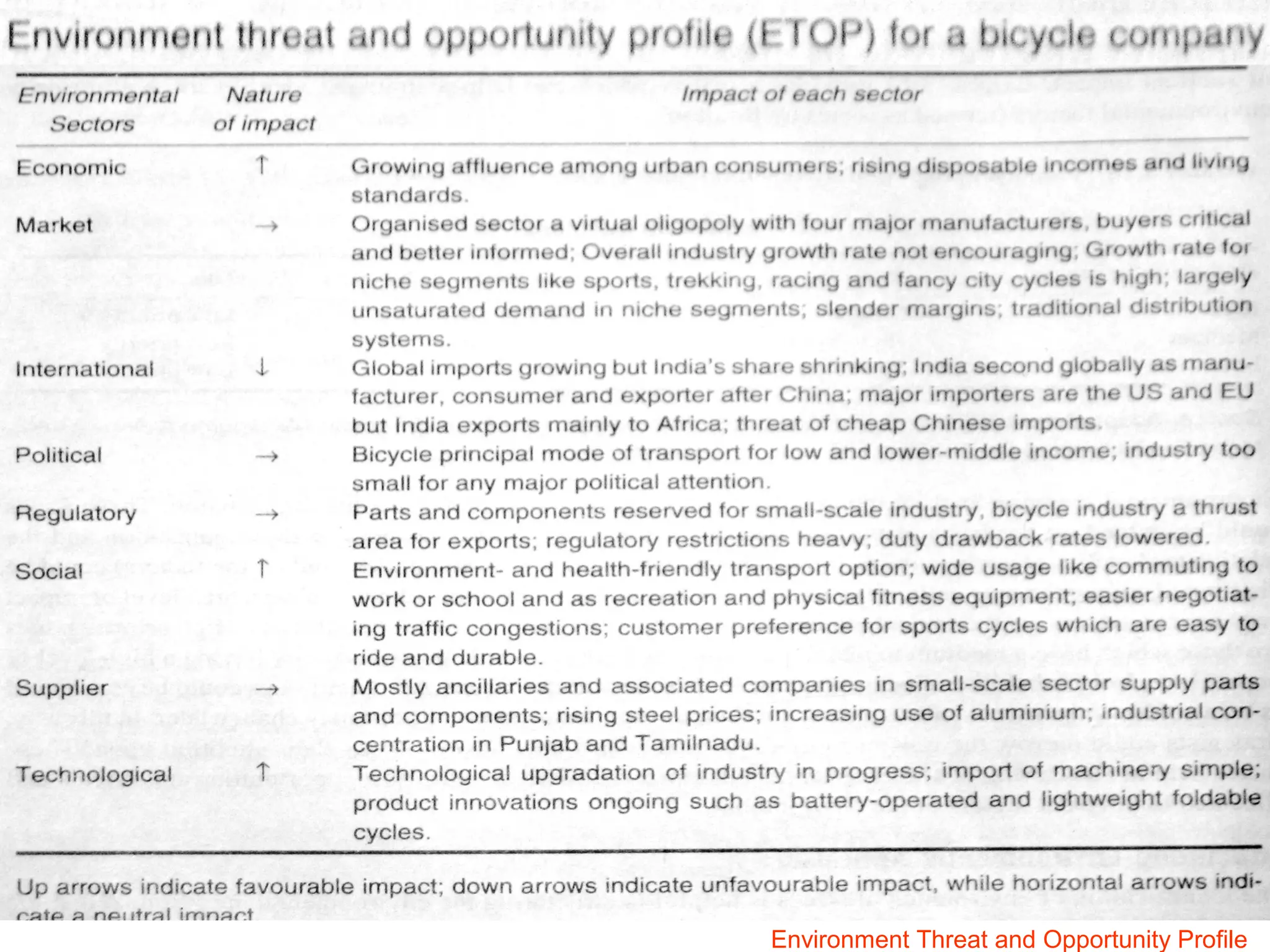

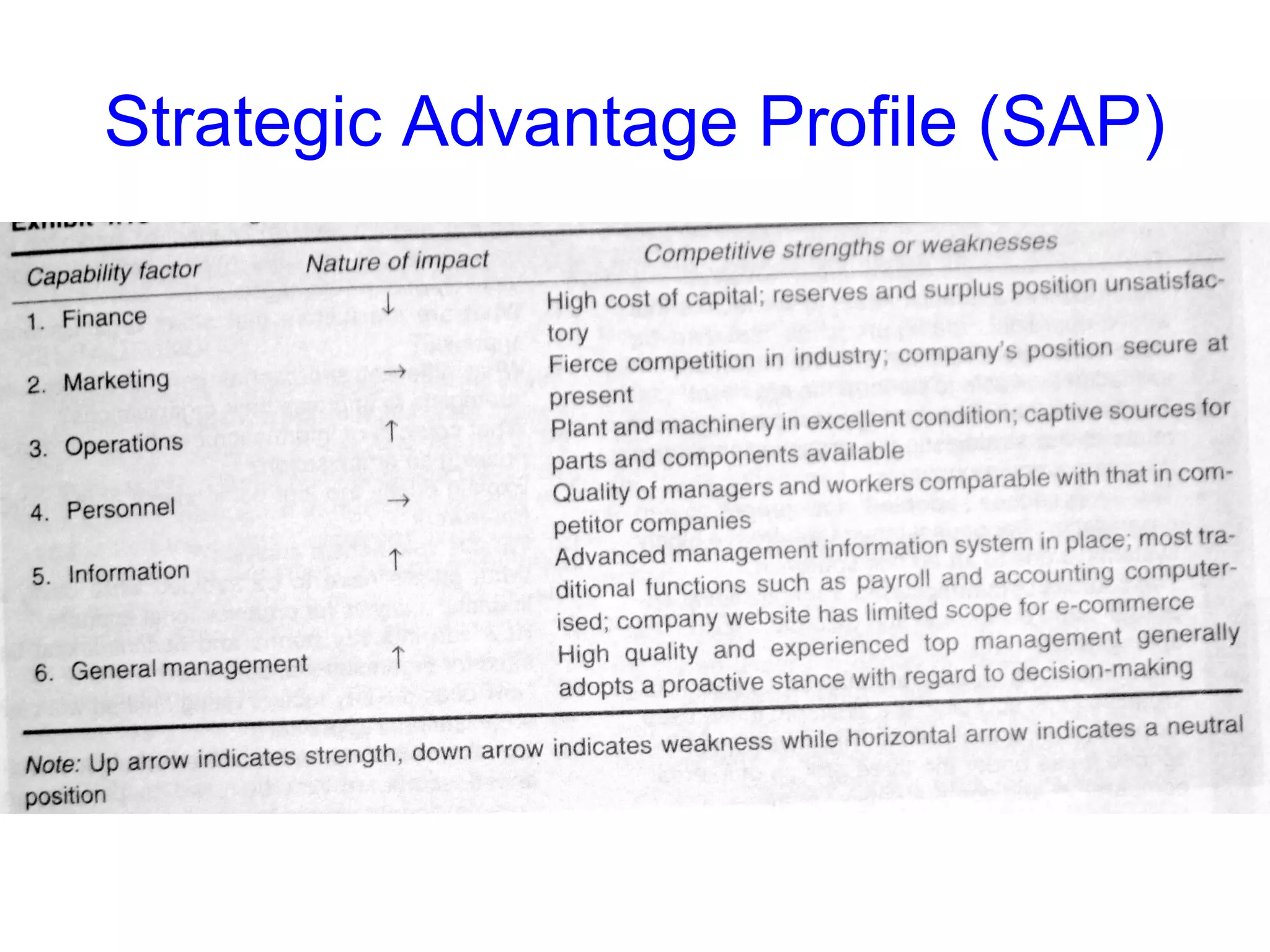

Explains critical success factors (CSFs) necessary for achieving objectives and explores the framework for organizational appraisal.

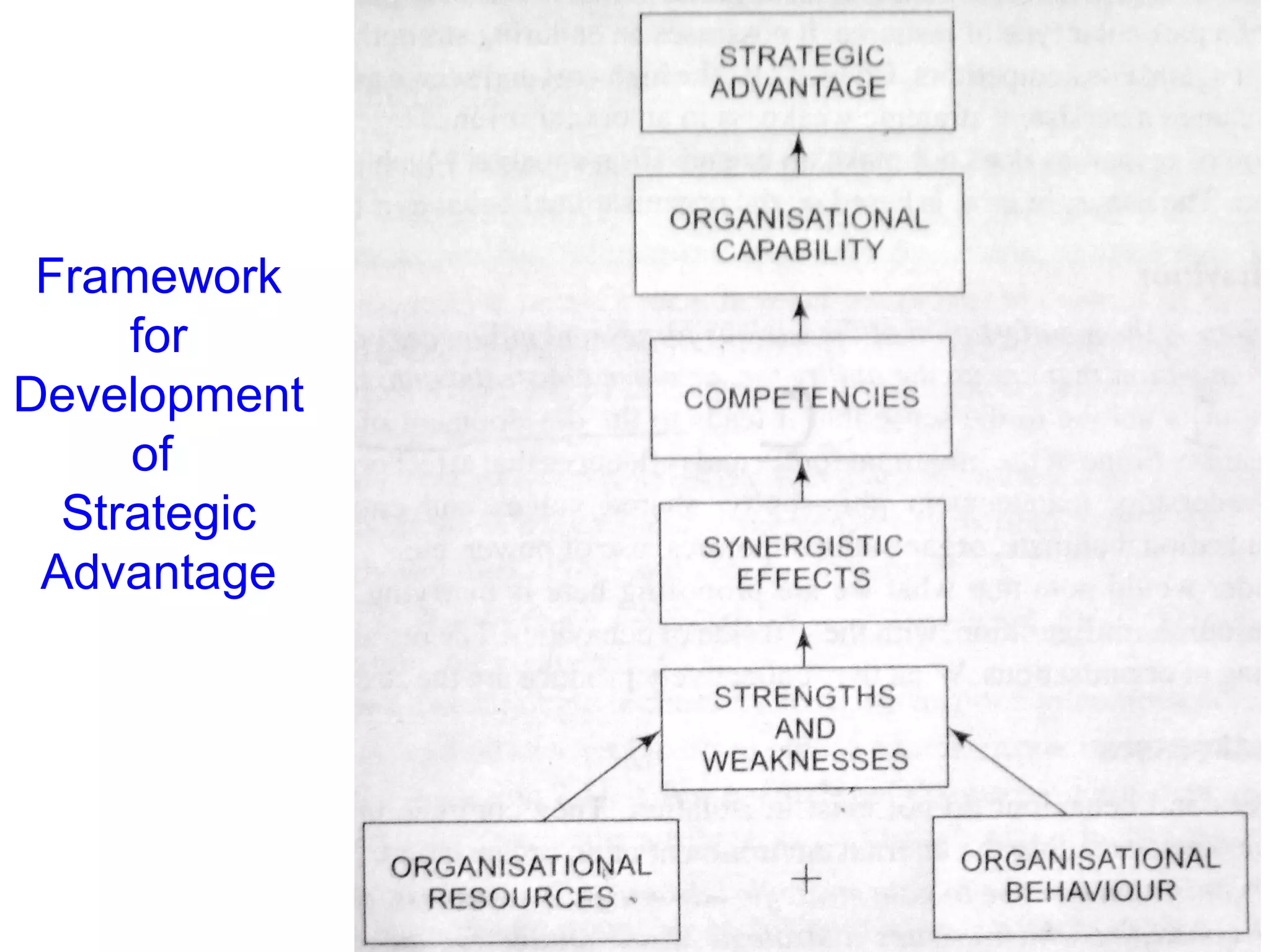

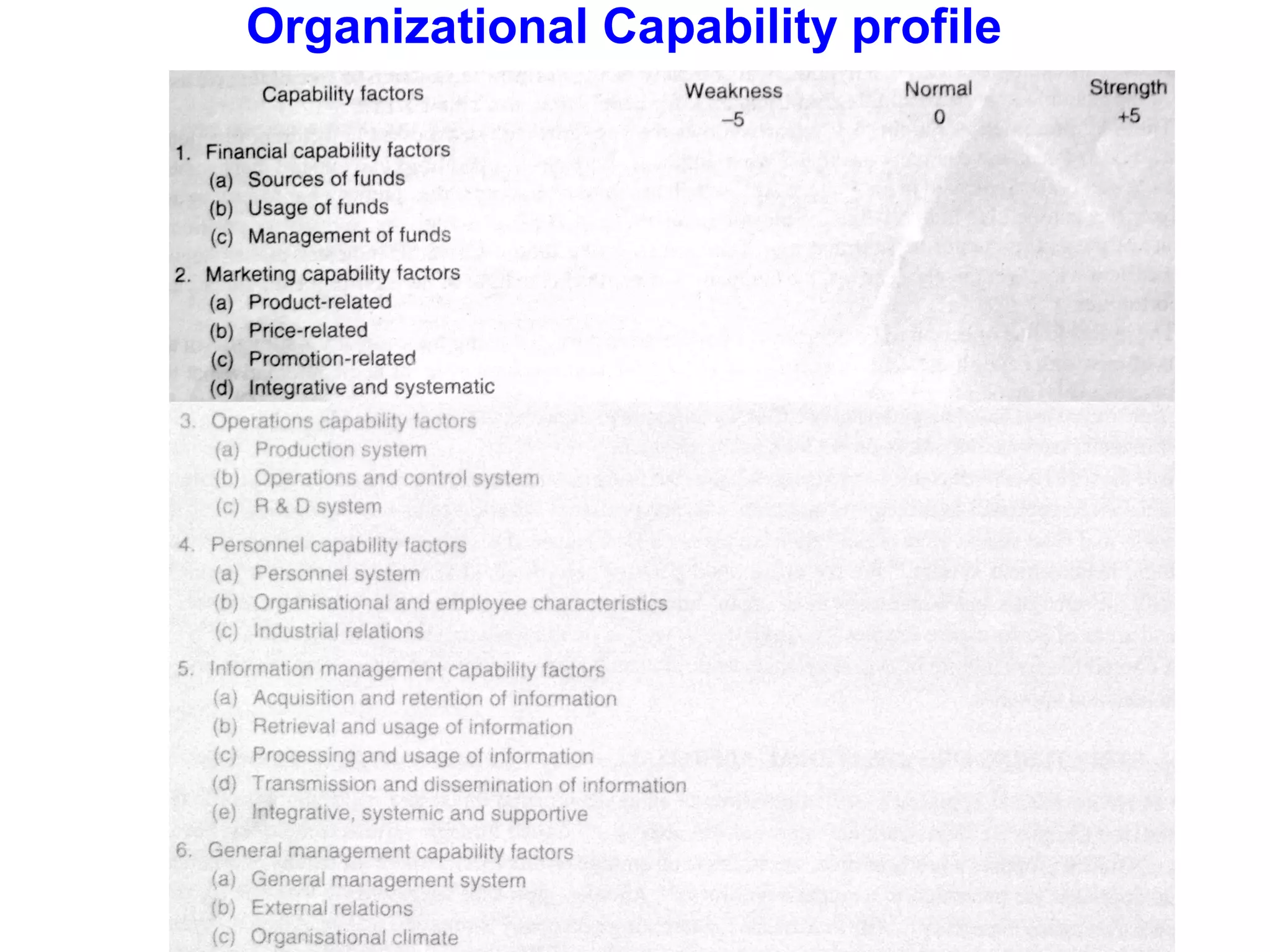

Focuses on organizational capability factors crucial for strategy formulation, highlighting strengths and weaknesses across functional areas.

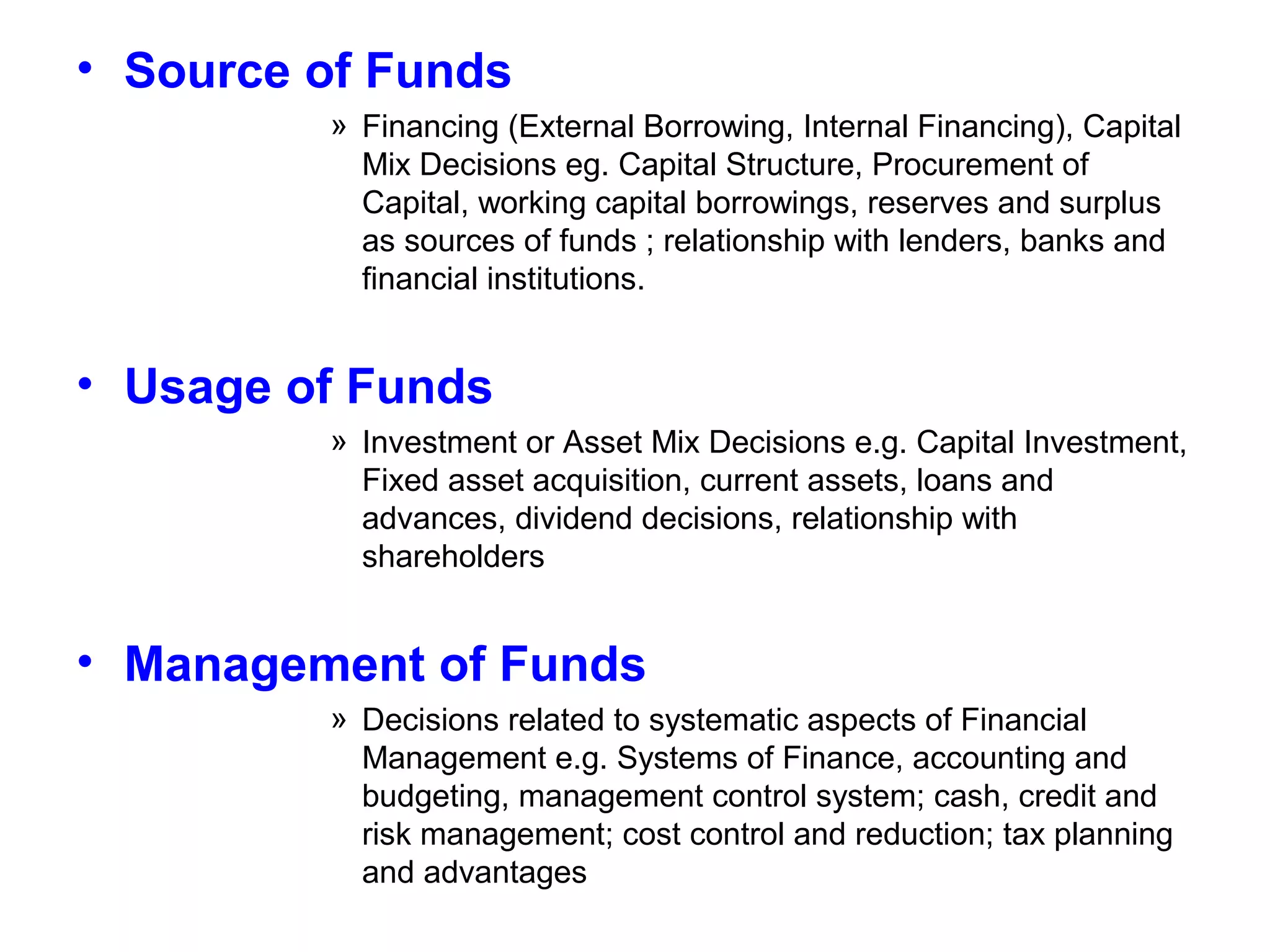

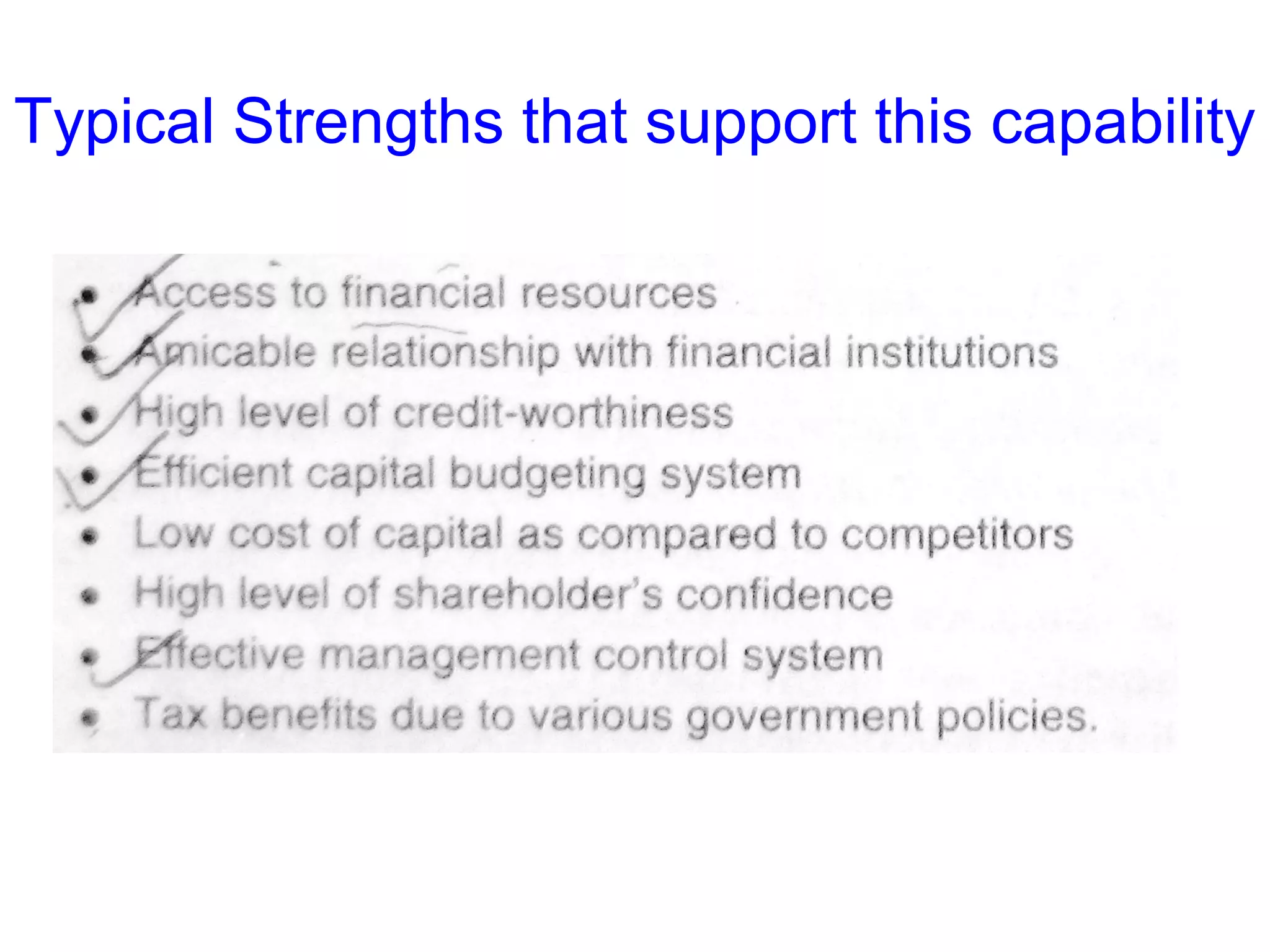

Details financial capability factors, including sources, usage, and management of funds essential for strategic planning.

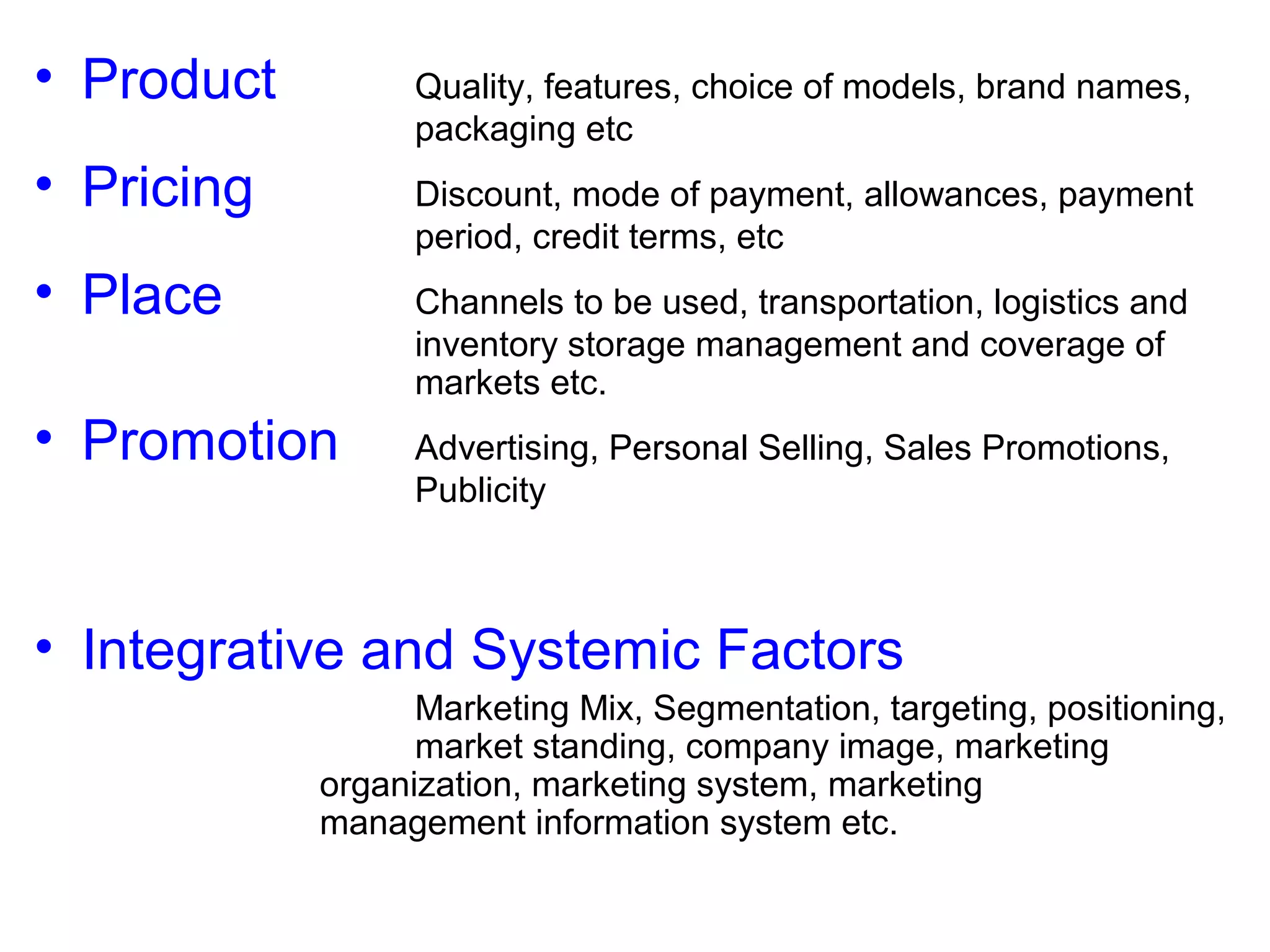

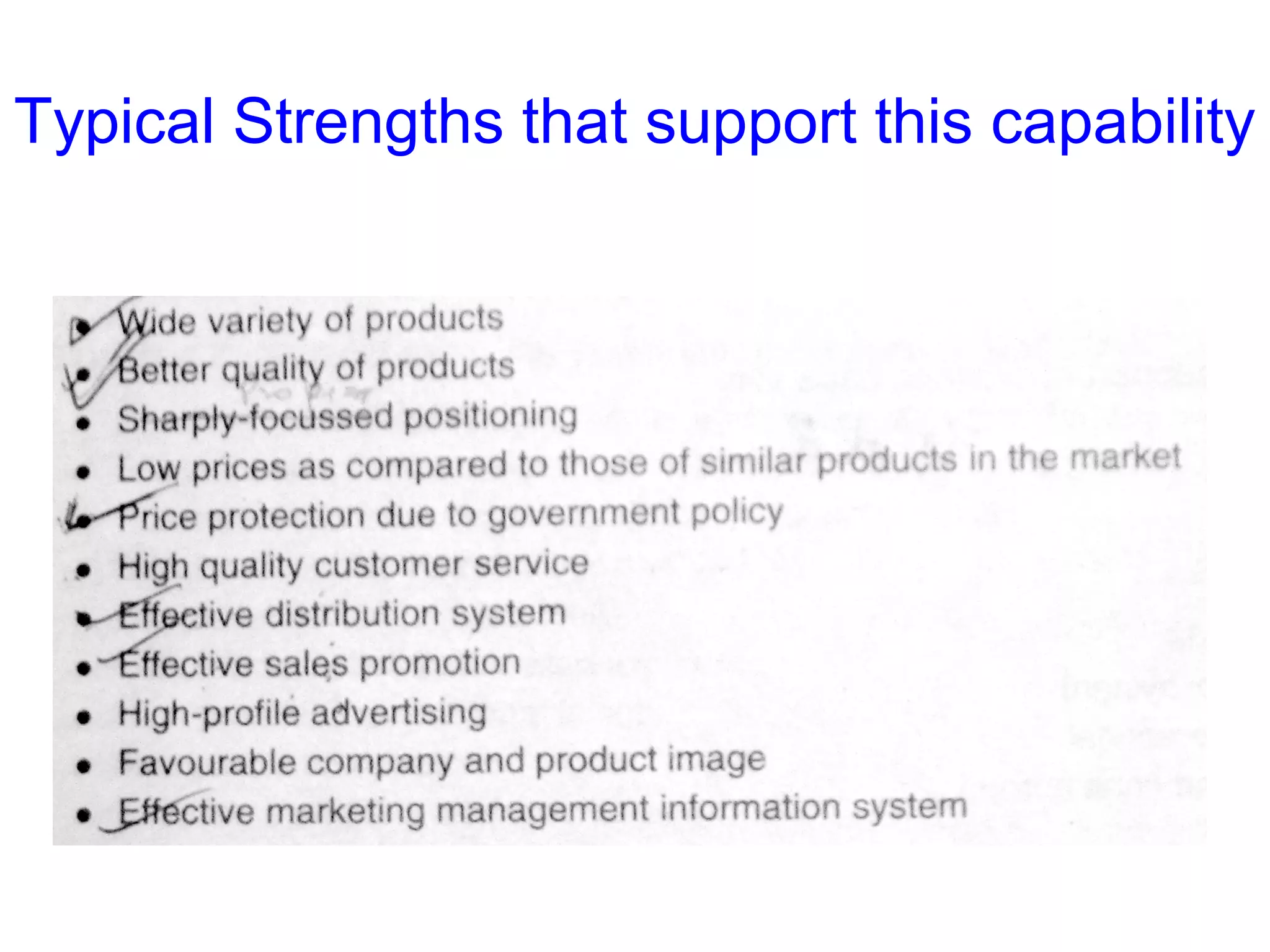

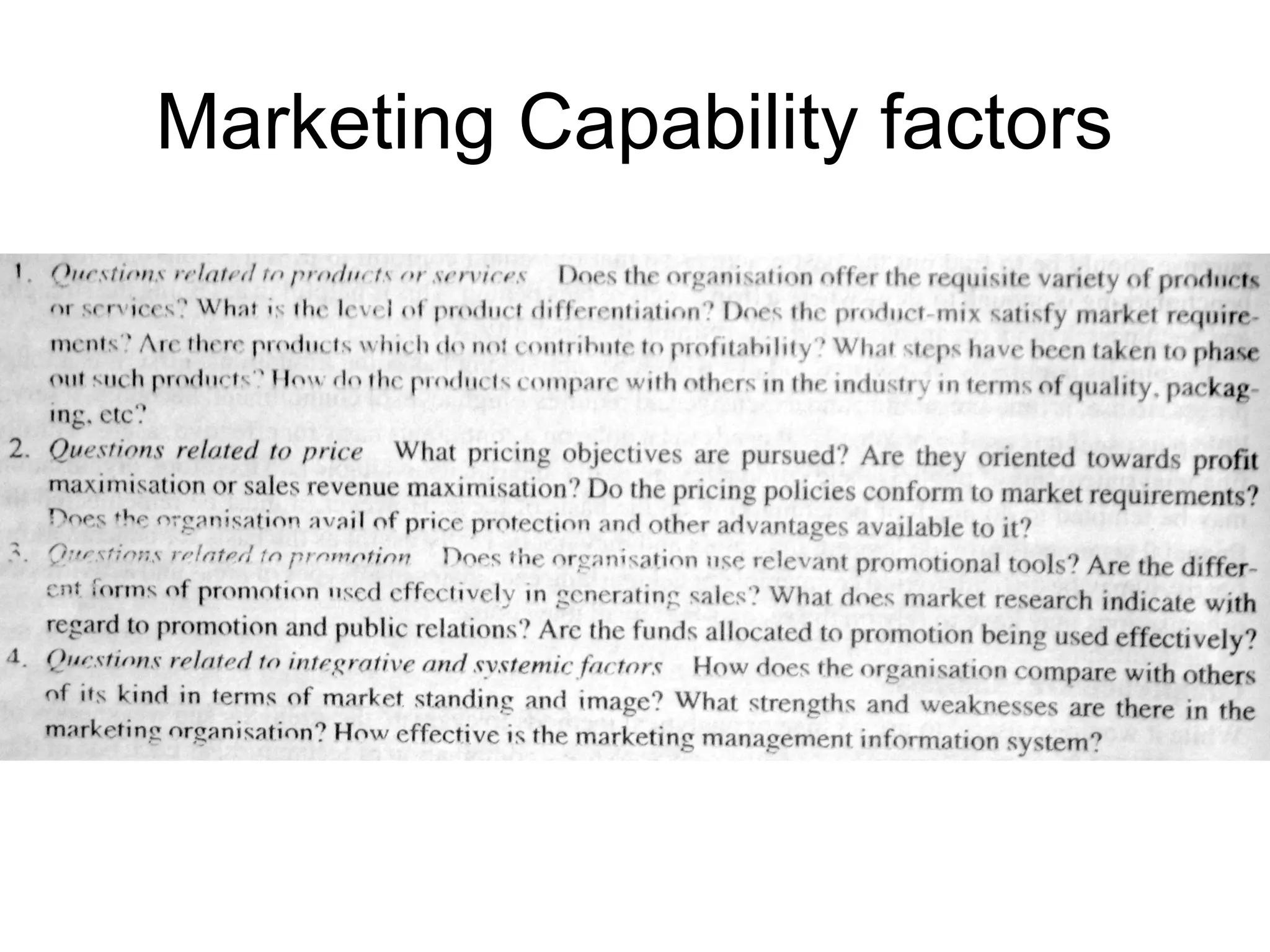

Examines marketing capabilities covering product, pricing, place, and promotion strategies with typical strengths.

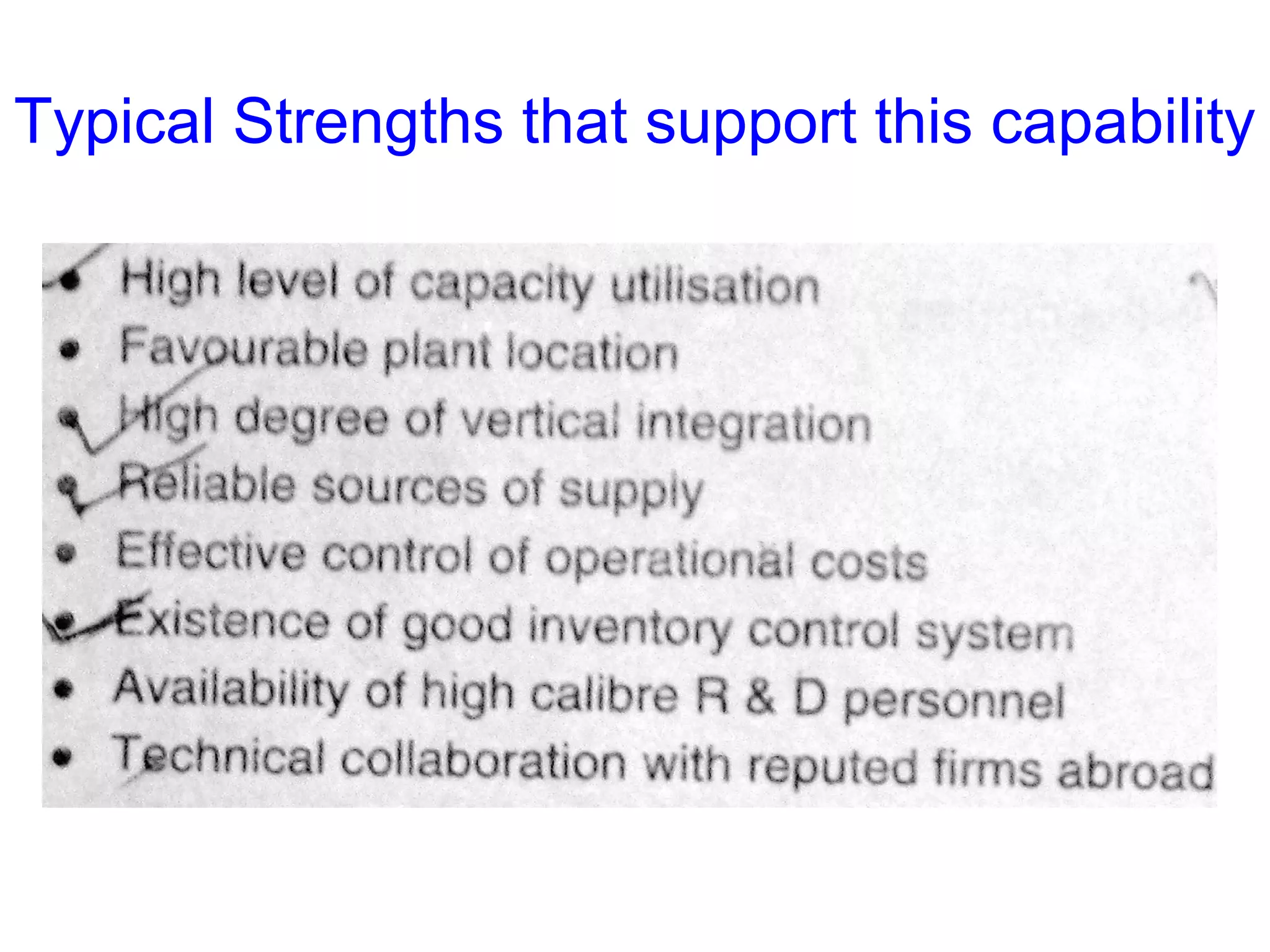

Overviews operational capabilities, including production systems, planning, and R&D with focus on strengths supporting operations.

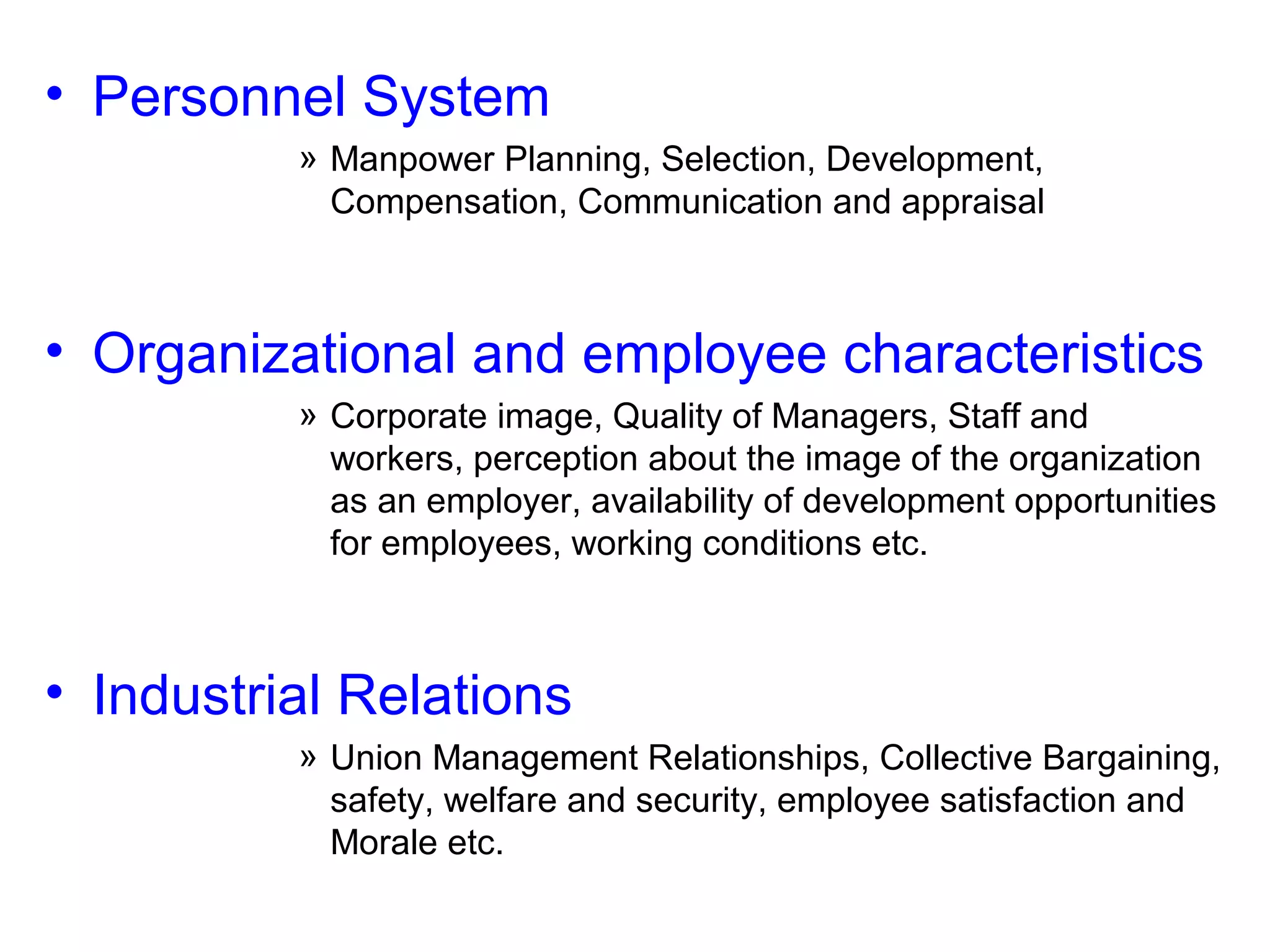

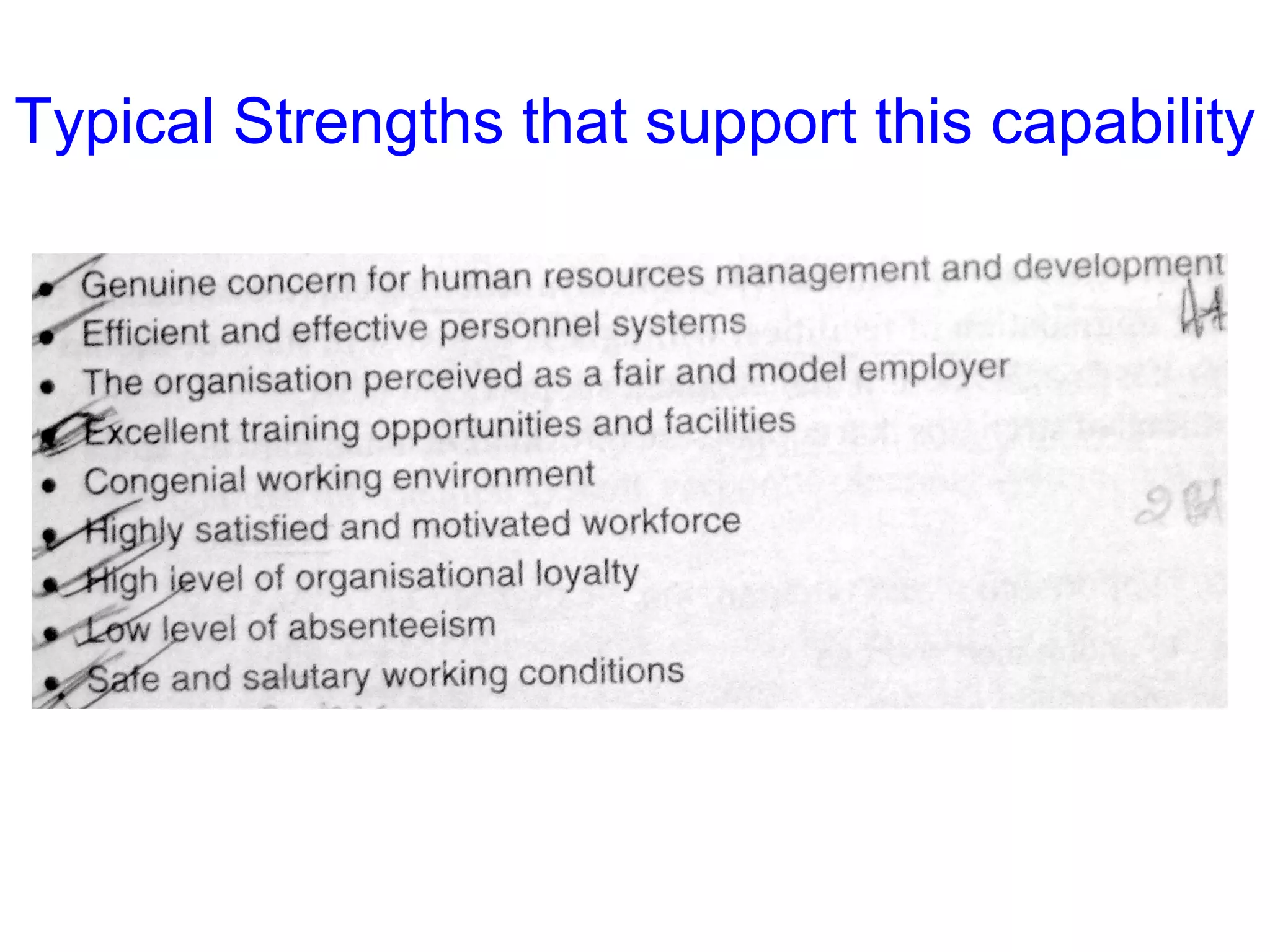

Discusses elements of personnel capability, including manpower planning, organizational characteristics, and industrial relations.

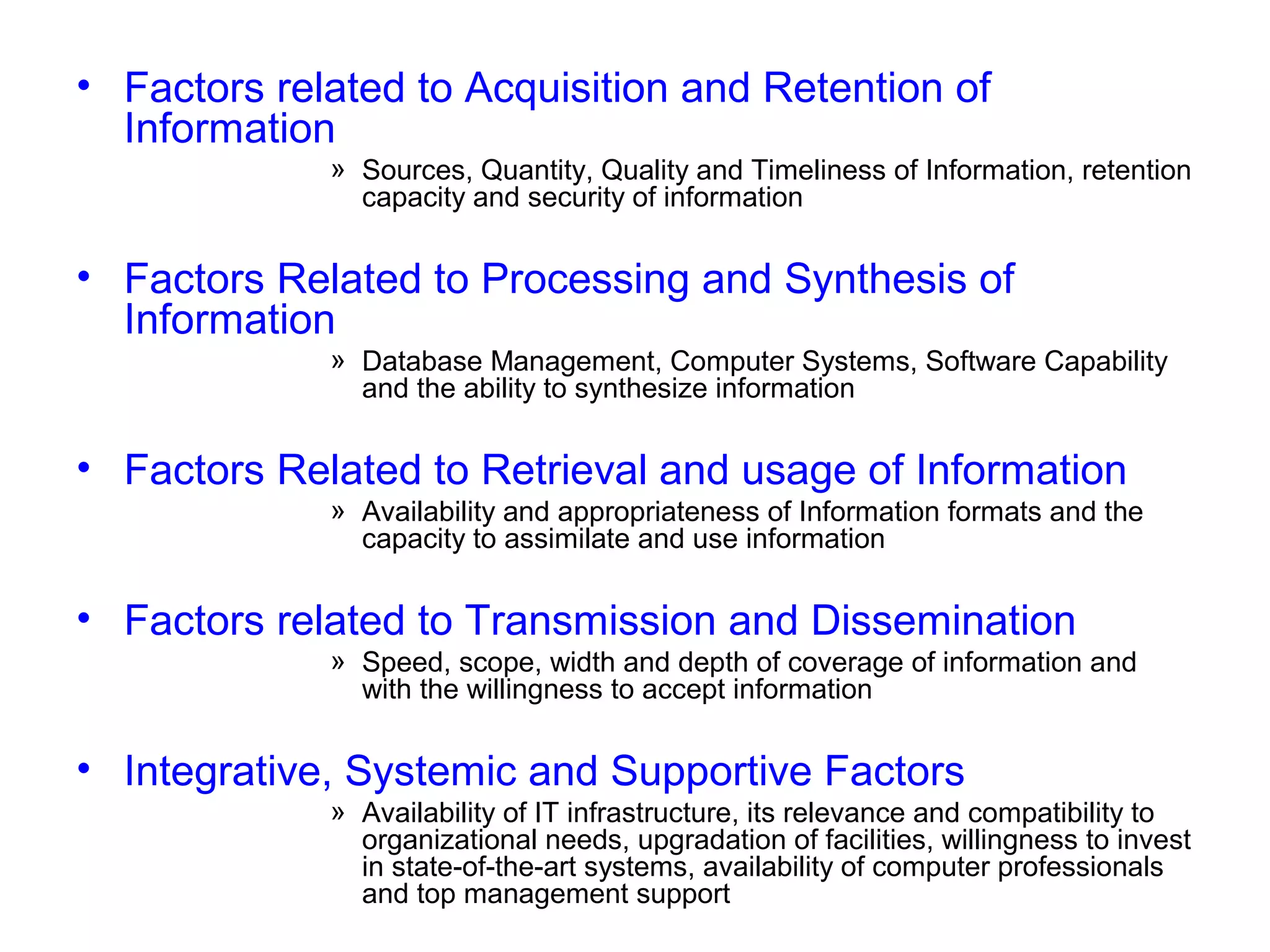

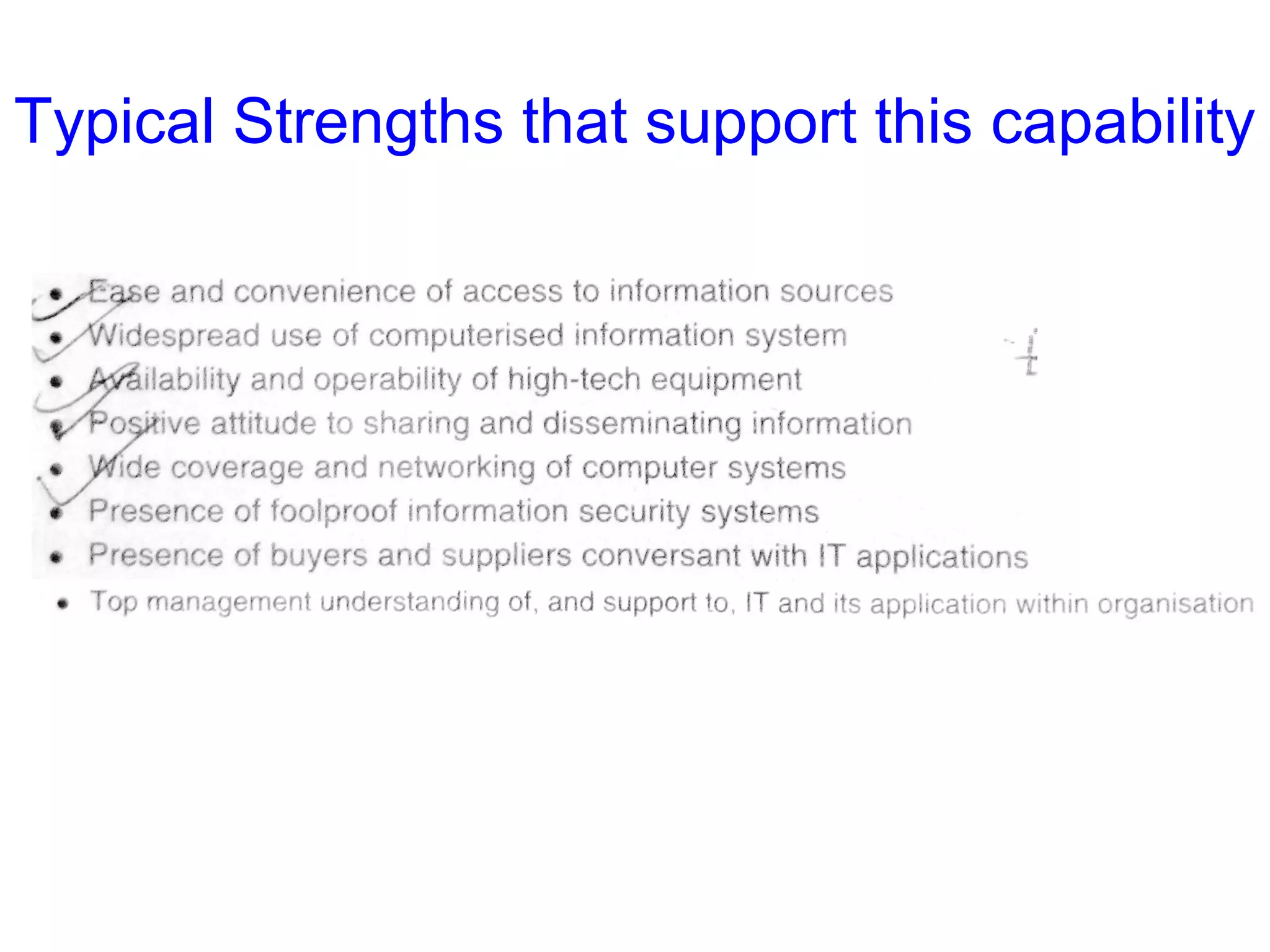

Outlines factors involved in information management including acquisition, processing, retrieval, and dissemination of information.

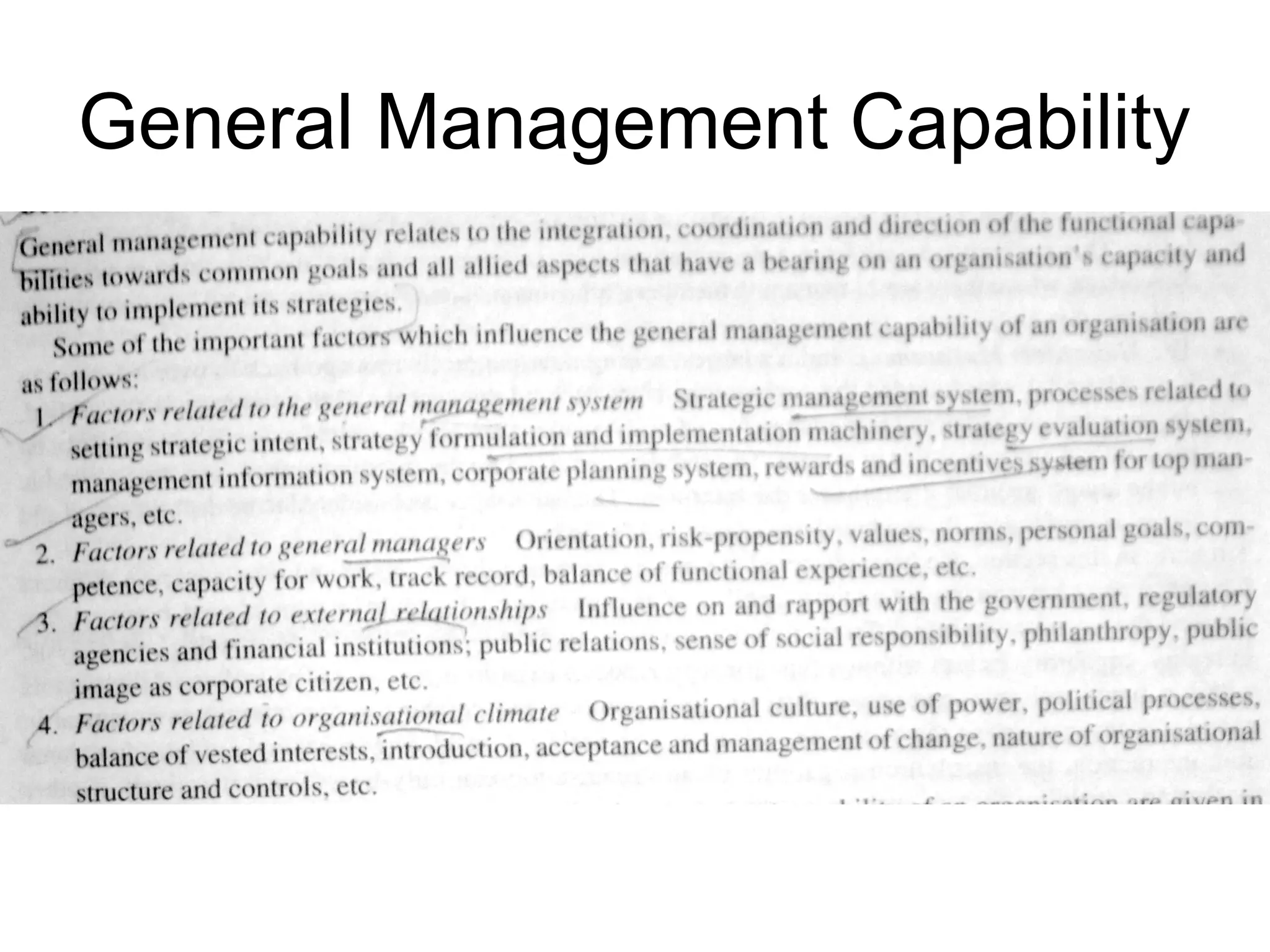

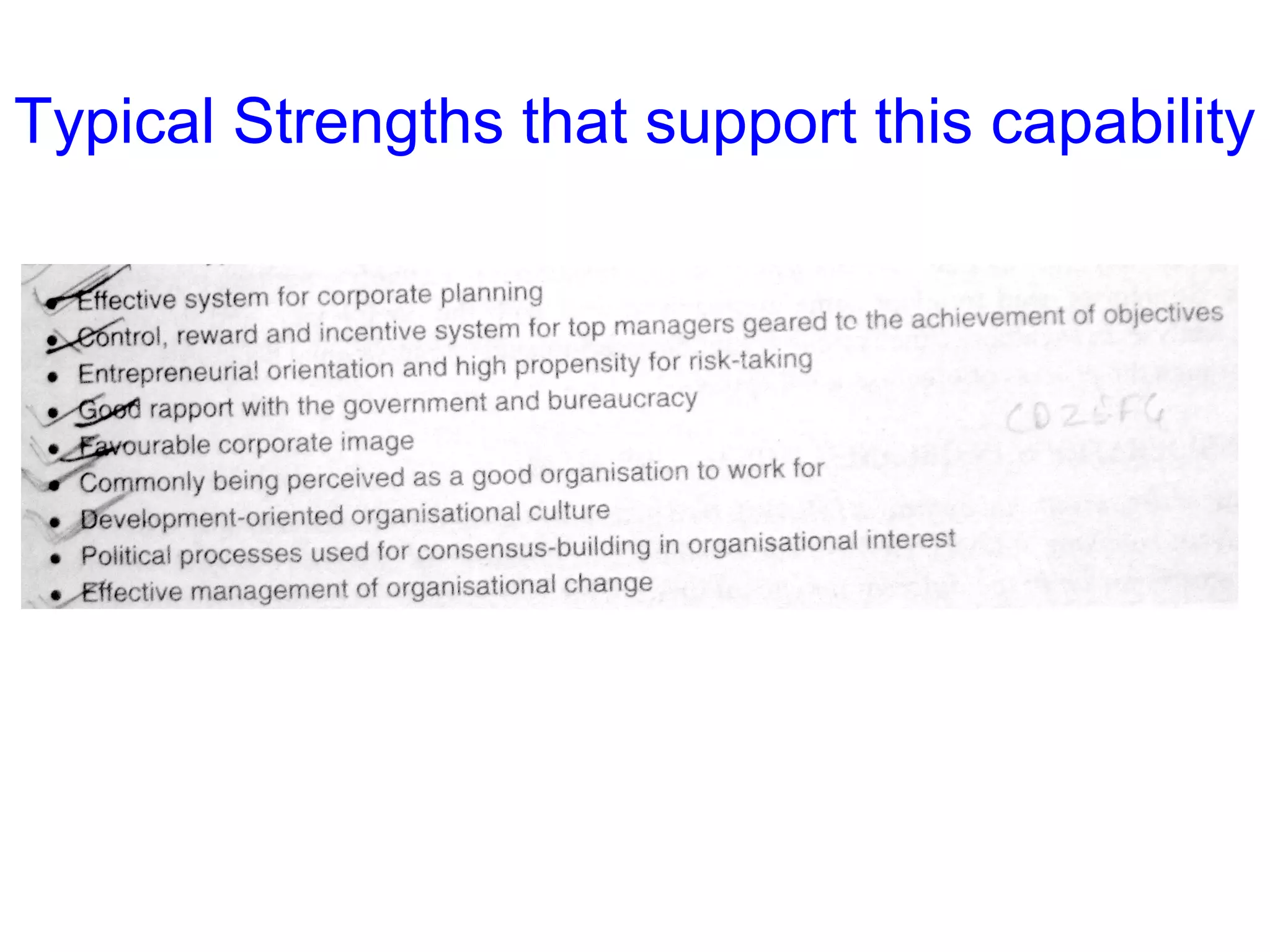

Focuses on general management capabilities and various methods for organizational appraisal including internal analysis.

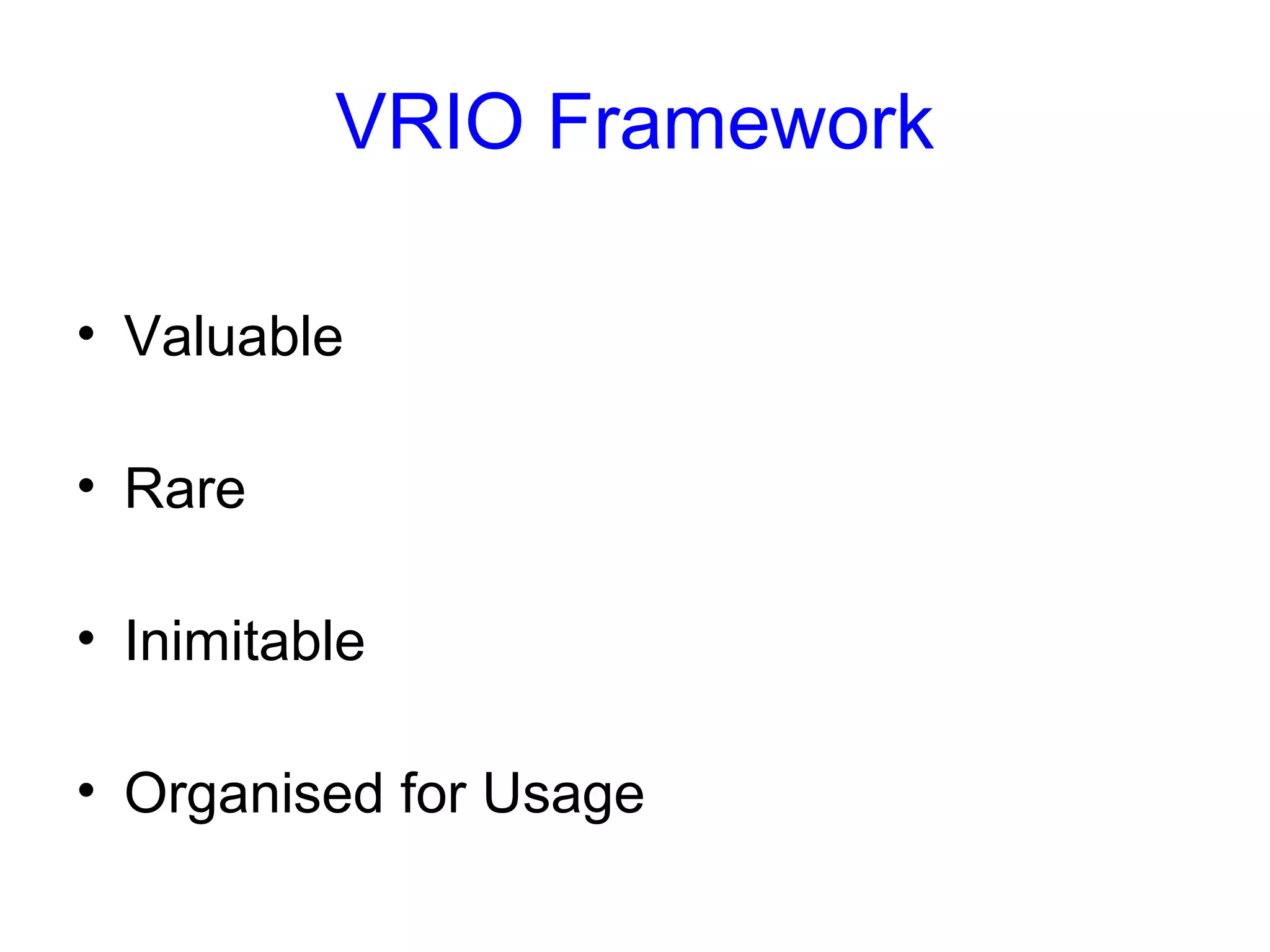

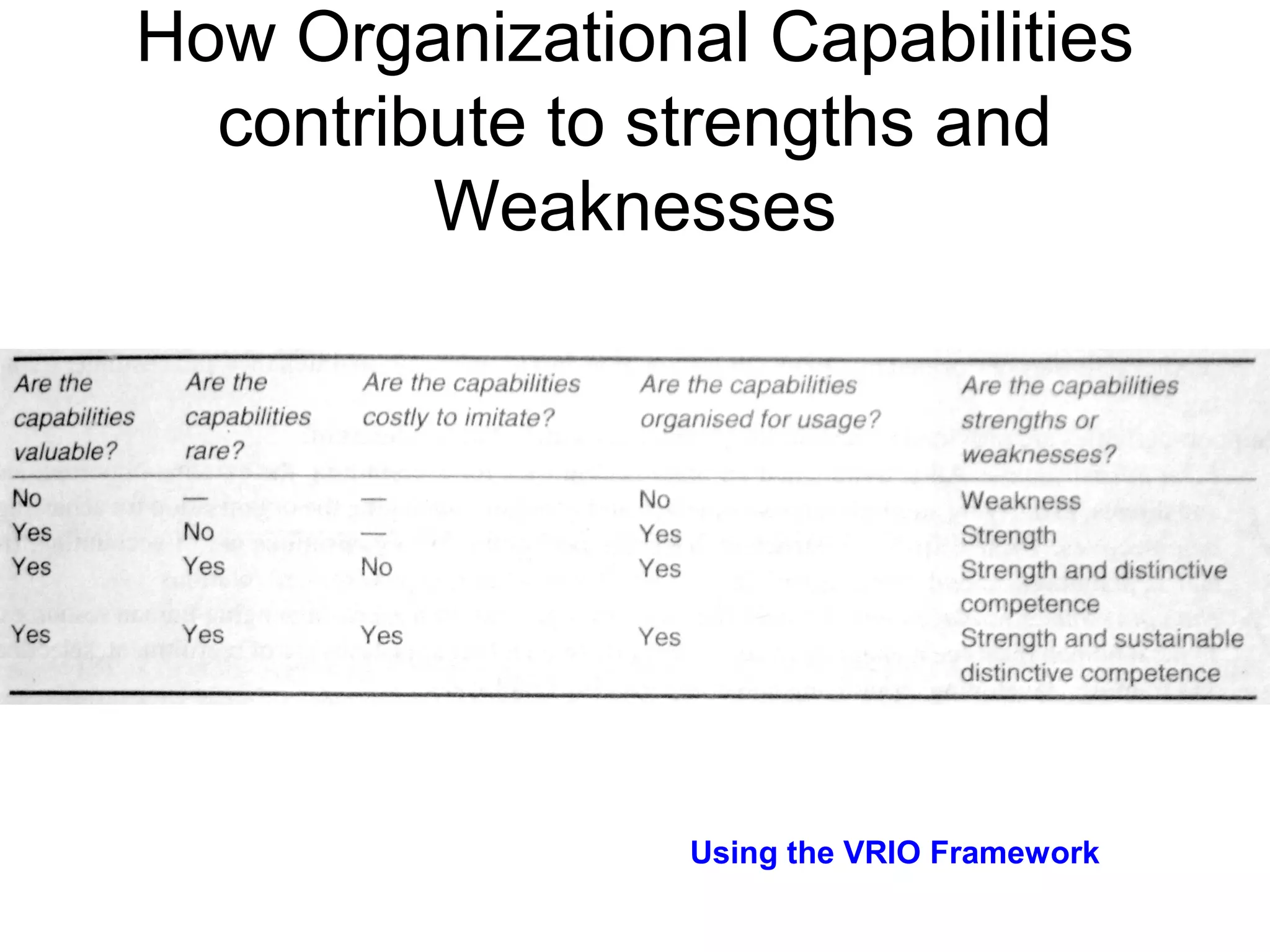

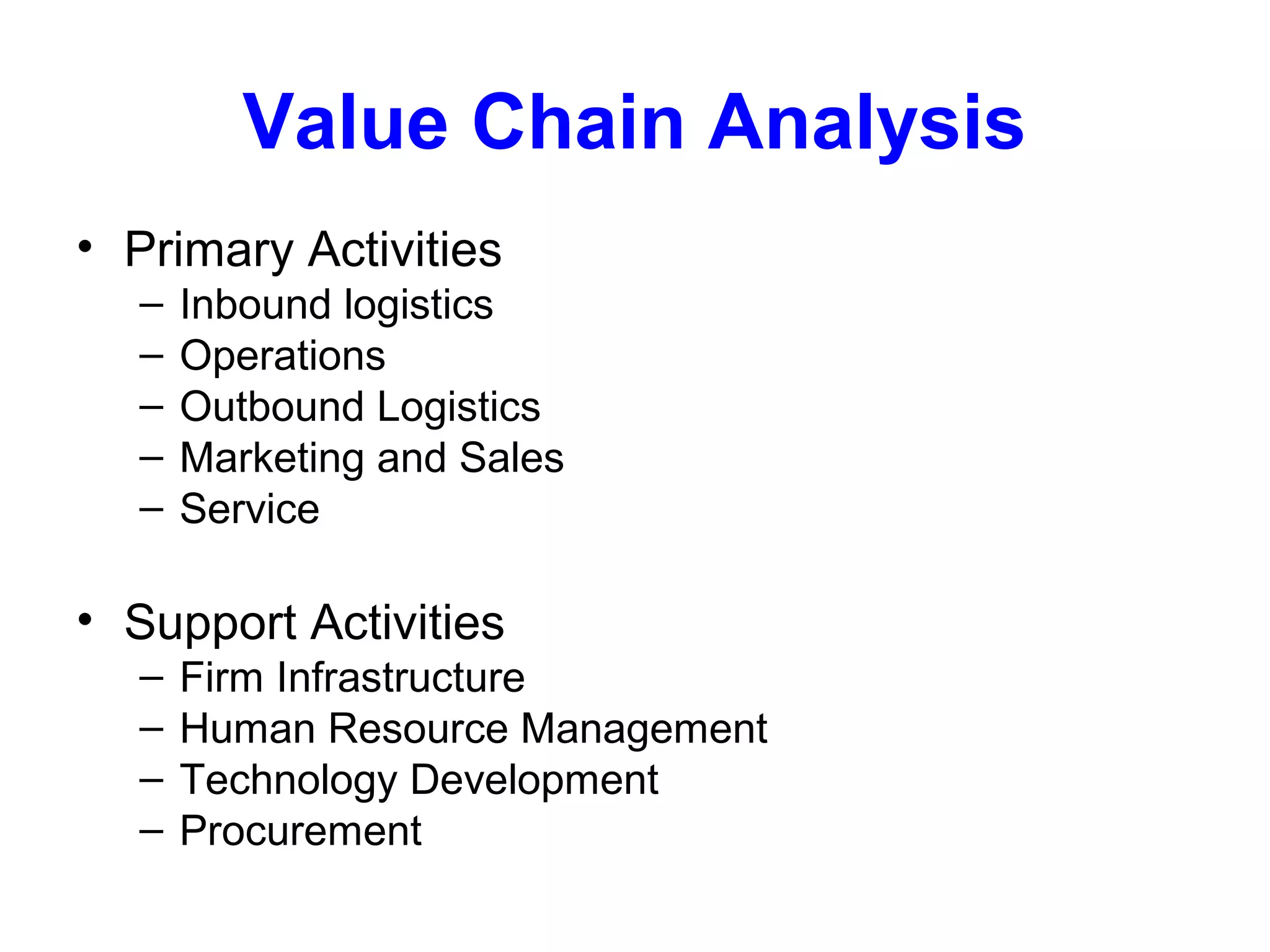

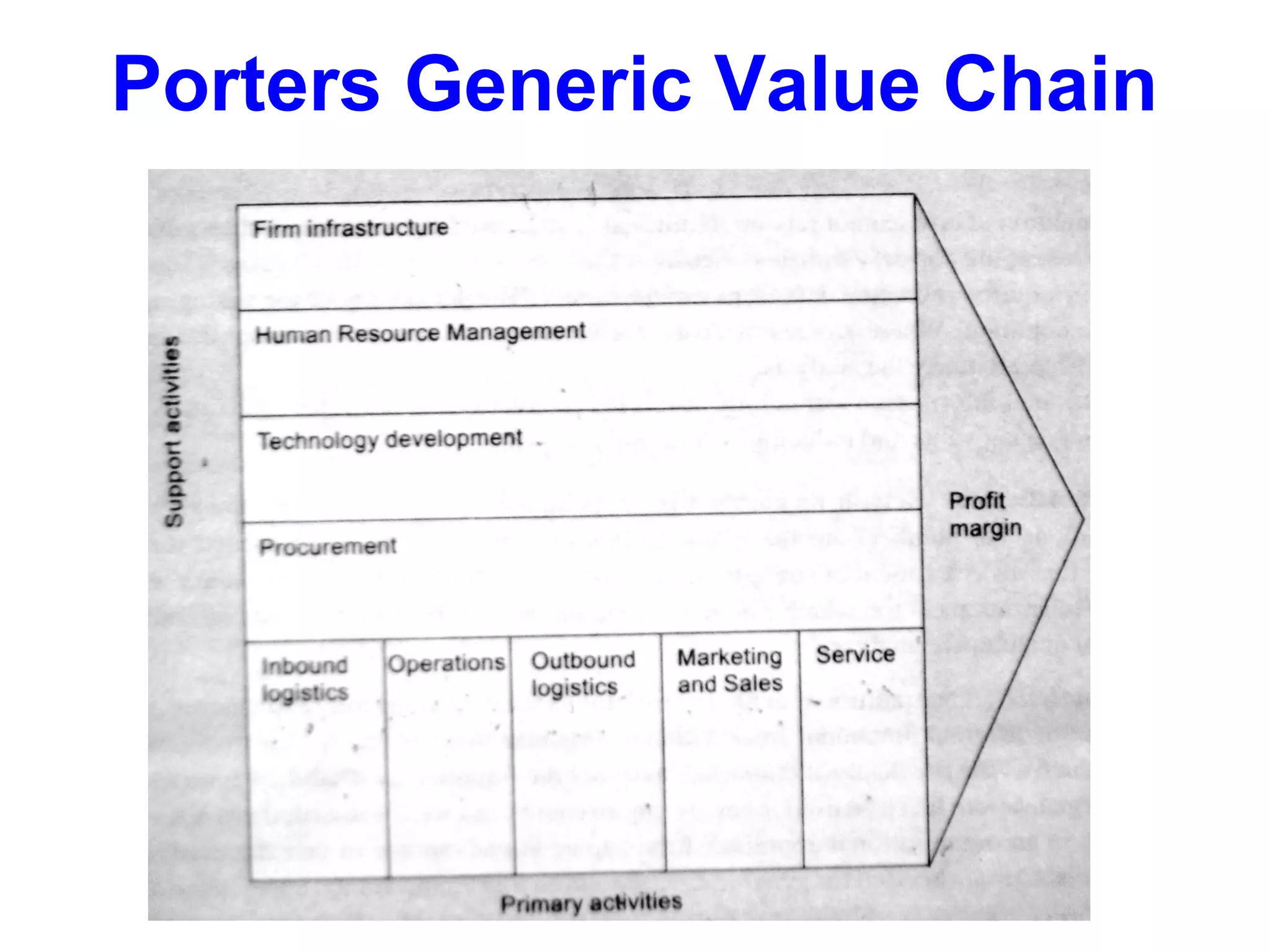

Explains VRIO framework and value chain analysis, emphasizing primary and support activities for assessing organizational capabilities.

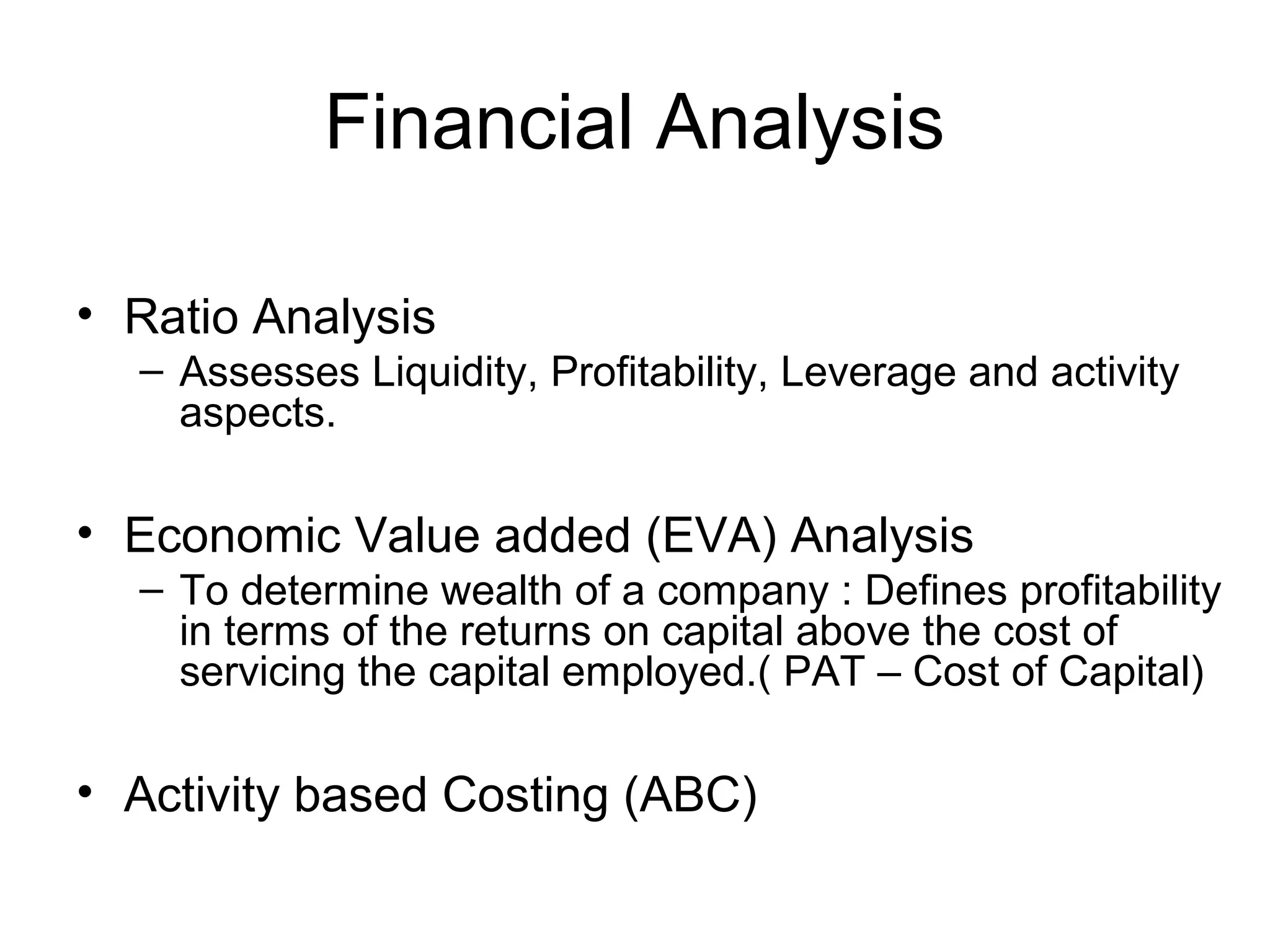

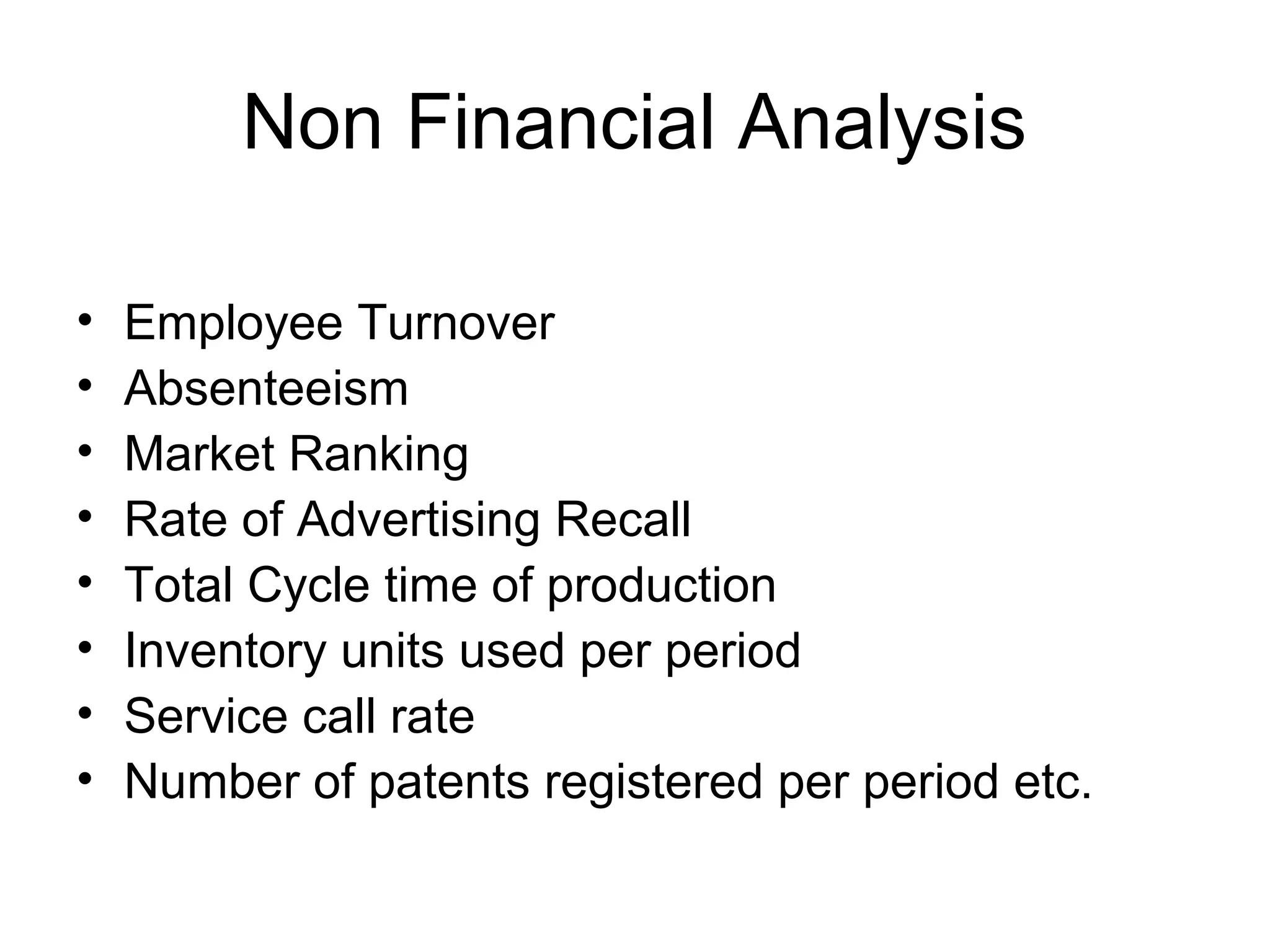

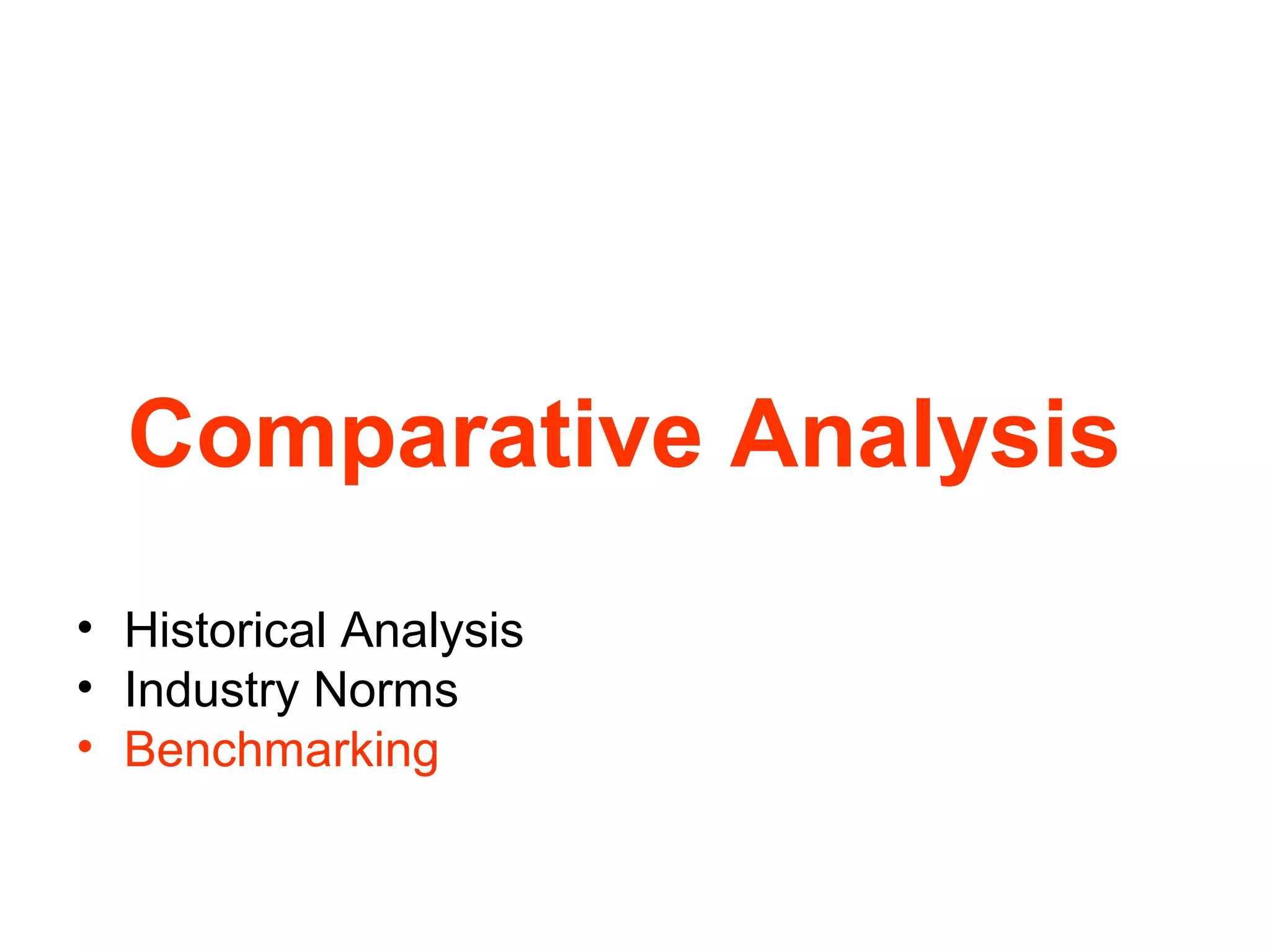

Highlights quantitative analysis methods including financial and non-financial measures as well as comparative analysis techniques.

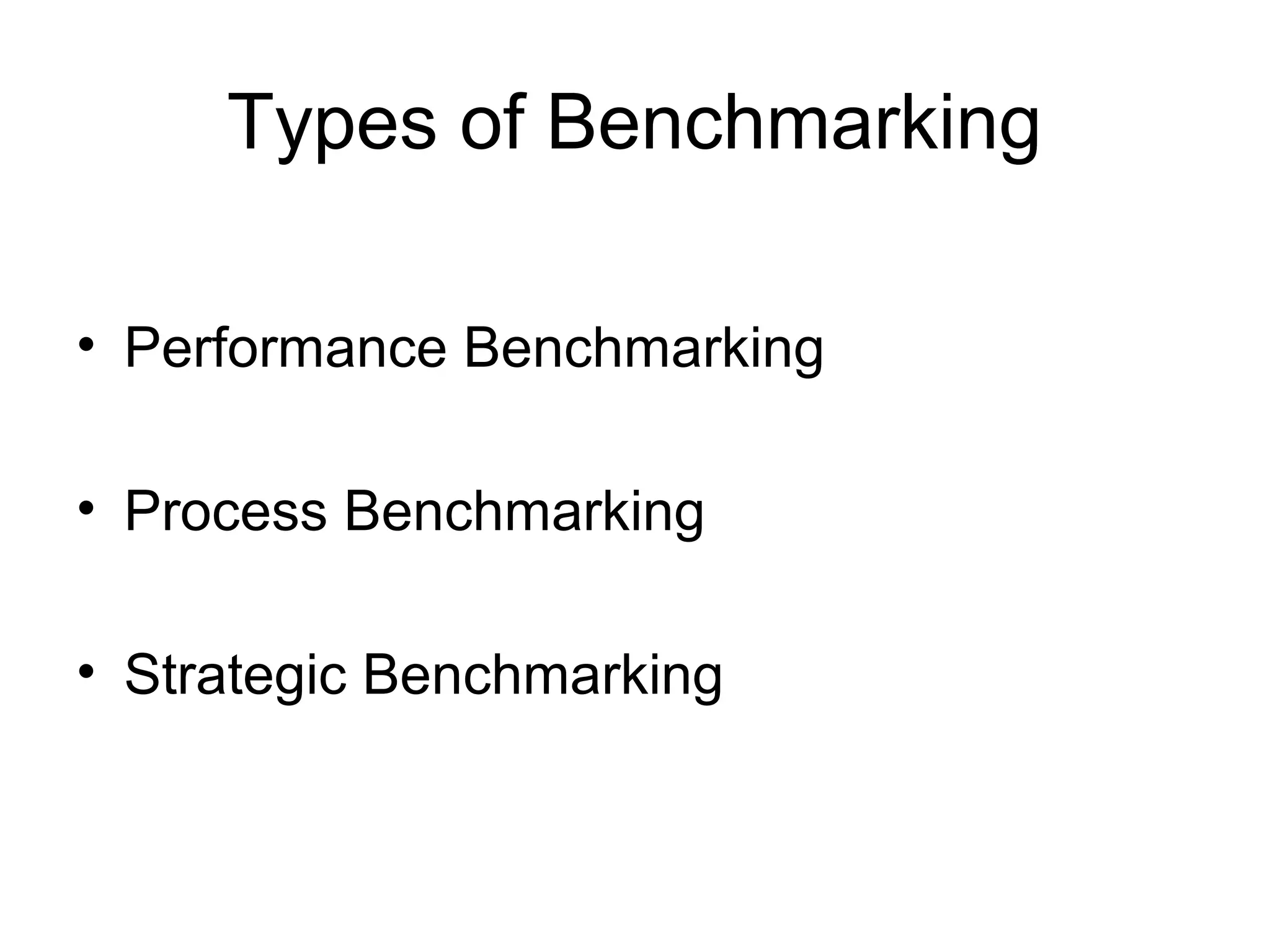

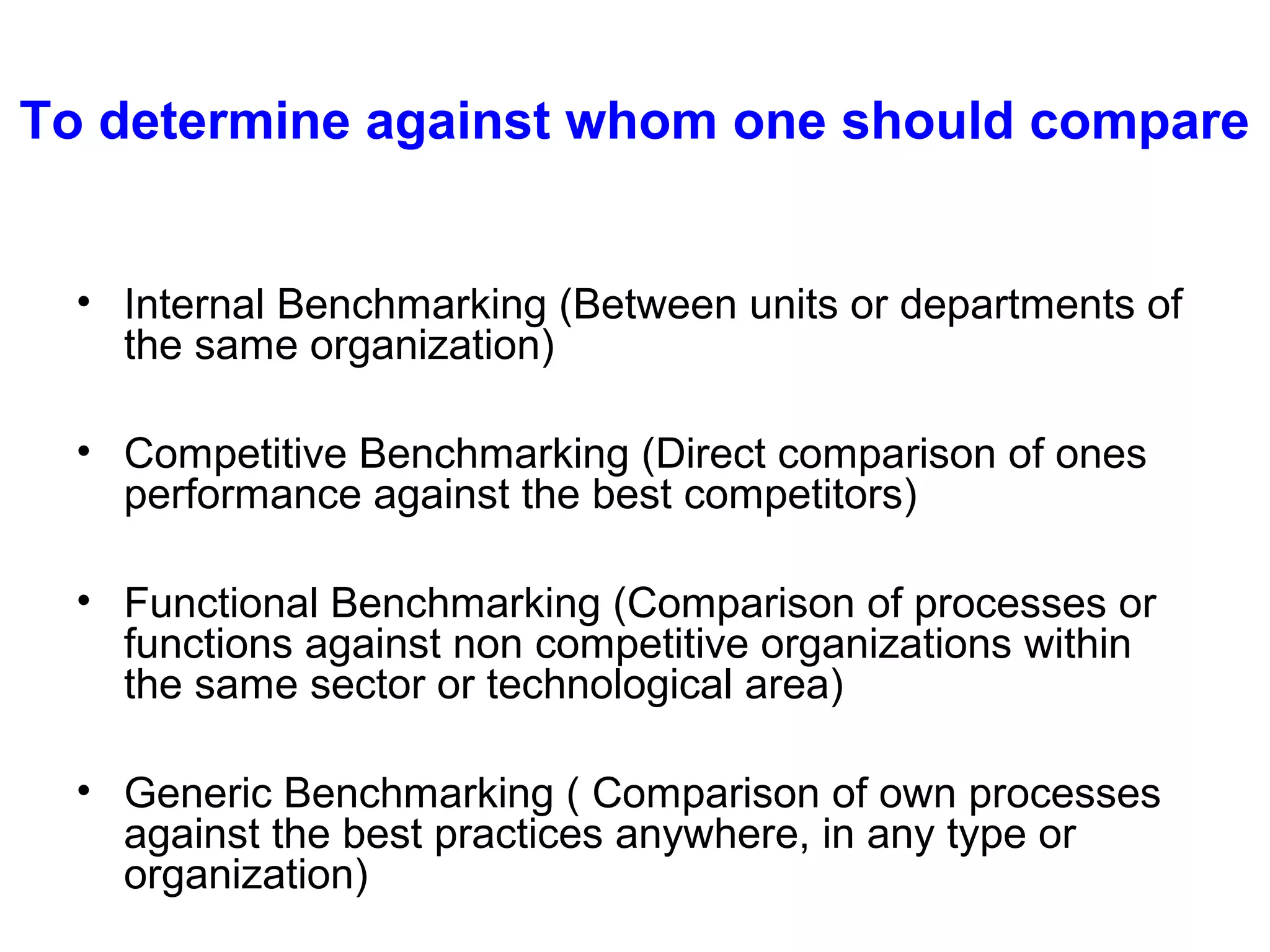

Discusses types of benchmarking, key factor rating, business intelligence, and the use of balance scorecard for a comprehensive analysis.