Download as PDF, PPTX

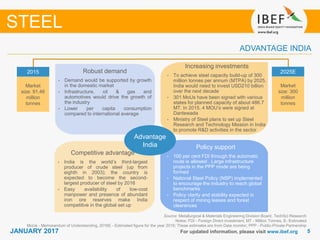

- India is the third largest producer of crude steel in the world and is expected to become the second largest producer by 2016. Total finished steel production in India reached 92.16 million tonnes in FY15. - Demand for steel is expected to grow significantly due to India's low per capita steel consumption and increased infrastructure development. Consumption is projected to reach 104 million tonnes by 2017. - However, domestic production has not been able to keep up with rising demand, leading to increased steel imports. The government has imposed measures like minimum import prices to boost domestic production and reduce imports.