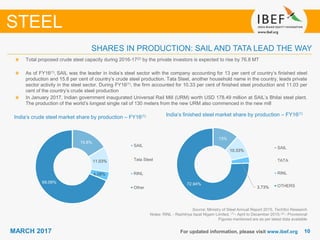

Downloaded 145 times

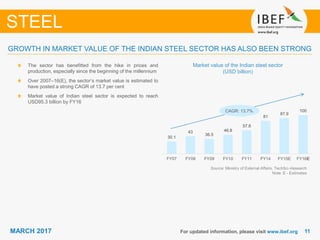

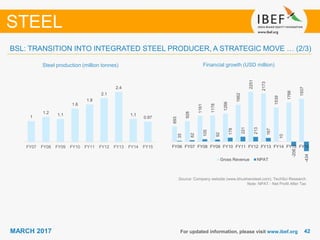

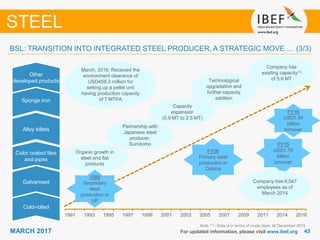

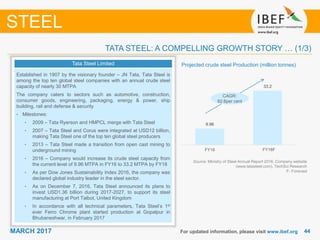

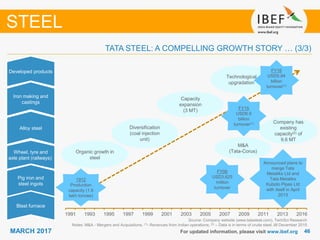

The document provides an overview of the Indian steel industry. It discusses key trends such as India becoming the third largest producer of crude steel in 2015. It also highlights growth opportunities in the industry given India's low per capita steel consumption and expected rise in demand from the infrastructure and automotive sectors. The document outlines factors like technological advancements, investments from domestic and international players, and the government's policy support as positives for the industry. It also examines aspects like leading companies, end use segments, production and consumption trends.