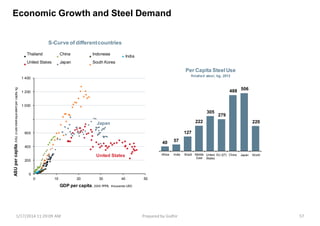

The document discusses challenges facing the Indian steel industry and its future outlook. It notes that while Indian steel companies have achieved higher profit margins than global peers, the industry now faces issues like volatile domestic iron ore supply, potential overcapacity, and changing customer demands. The industry must improve resource management, project execution, customer focus, supply chain management, and human capital management to better position itself for future growth opportunities in India.