Status of the Microfluidics Industry 2019 report by Yole Développement

•

5 likes•2,494 views

Diversification of microfluidic technologies has led to burgeoning new applications and market growth, driving players’ interest and M&A. More information on https://www.i-micronews.com/products/status-of-the-microfluidics-industry-2019/

Recommended

Recommended

More Related Content

What's hot

What's hot (20)

Similar to Status of the Microfluidics Industry 2019 report by Yole Développement

Similar to Status of the Microfluidics Industry 2019 report by Yole Développement (20)

More from Yole Developpement

More from Yole Developpement (20)

Recently uploaded

Recently uploaded (20)

Status of the Microfluidics Industry 2019 report by Yole Développement

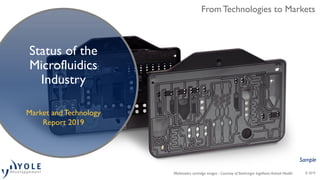

- 1. © 2019 From Technologies to Markets Status of the Microfluidics Industry Mobinostics cartridge images - Courtesy of Boehringer Ingelheim Animal Health Market and Technology Report 2019 Sample

- 2. 2 Sébastien CLERC Sébastien Clerc works as a Technology & Market Analyst, Microfluidics & Medical Technologies at Yole Développement (Yole). As part of the Life Sciences & Healthcare division, Sébastien has authored a collection of market and technology reports dedicated to topics such as microfluidics, point- of-care, MEMS for healthcare applications and connected medical devices. In parallel, he is daily involved in custom projects such as strategic marketing, technology scouting and technology evaluation to help academic and industrial players in their innovation processes. Thanks to his technology & market expertise, Sébastien has spoken in more than 10 industry conferences worldwide over the last 2 years. Sébastien Clerc graduated from Grenoble Institute of Technology (Grenoble INP - Grenoble, France) with a Master’s degree in Biomedical Technologies. He then completed his cursus with a Master’s degree in Innovation and Technology Management in the same institute. Contact: clerc@yole.fr Asma SIARI As a Technology & Market Analyst, Biotechnologies & Molecular Innovations, Medical Technologies in the Life Sciences & Healthcare division at Yole Développement (Yole), Asma Siari is involved in the development of technology & market reports as well as the production of custom consulting projects. After a Master’s degree in Biotechnologies, Diagnostic Therapeutics & Management, Asma served as Research Assistant at the Moores Cancer Center (San Diego, CA). She is a coauthor in three scientific publications published in the Molecular Cancer Research Journal. Asma Siari graduated with an Advanced Master’s degree in International Strategy & Marketing BtoB from EM Lyon Business School (France). Contact: siari@yole.fr Status of the Microfluidics Industry 2019 | Sample | www.yole.fr | ©2019 ABOUT THE AUTHORS Biographies & contacts

- 3. 3 3M, 10X Genomics,Abaxis (Zoetis), Abbott, Alere (Abbott), Achira Labs, Affymetrix (Thermo Fisher Scientific), AGC, Agilent Technologies,Akatsuki Tech, Akonni Biosystems, Allevi, ALine, Alveo Technologies, Angle plc, Applied Microarrays, Araymond Life, Arrayit, Arrayjet, Ativa Medical, Atlas Genetics (binx health), AutoGenomics (Prescient Medicine), AxoSim, Axxicon, Axxin, Balda AG (Stevanato Group), Base4 Innovation, BD, BGI, binx health, Biocartis, Biocept, BioFire Diagnostics (bioMérieux), BioFluidica, Biolidics, Bionano Genomics, Bio-Rad, BioSensia (Kypha), Biosurfit, BOE, Boehringer Ingelheim, Boehringer Ingelheim microParts, Bosch Vivalytic (Bosch Healthcare), Bronkhorst, Caliper Life Sciences (PerkinElmer), Cambridge Consultants, CapitalBio Corporation, Capsum, Carville, CBio, CDA, Cellenion (Scienion), Celsee Diagnostics, Centrillion Technologies, Cepheid (Danaher), CG.TEC Injection, Chemtrix, CiDRA Precision Services (IDEX), CombiMatrix (Invitae), Corium, Corning, CorSolutions, Curetis, Cygnus Biosciences, Cytena, Cytosurge, Daktari Diagnostics, DARPA, Debiotech, Denz Bio-Medical, Dianax, DiaSorin Molecular, DNAe, Dolomite (Syrris), Eksigent, Elveflow (Elvesys), Emulate, Enplas, Epigem, Epicore Biosystems, ExcitePCR, Fast Radius, FlexoSense, FlowJem, Fluidic Analytics, Fluidigm, Fluigent, Fluxion Biosciences, Focus Diagnostics (DiaSorin Molcular), Formulatrix (Qiagen), GenapSys, GenePOC (Meridian Biosciences), GeneSystems (Pall), GenMark Diagnostics, Gradientech, Great Basin Scientific (Vela Diagnostics), Gyros Protein Technologies, Helvoet, Hemocue (Radiometer, Danaher), Hesperos, HifiBio, IDEX Health & Science, Illumina, imec, IMTAG (Heidenhain), IMT MEMS, Inanovate, Instant Labs (Luminultra), Instrumentation Laboratory (Werfen), Intabio, IntegenX (Thermo Fisher Scientific), Invenios (Corning), Invetech, InziGn, Ion Torrent (Thermo Fisher Scientific), IQuum (Roche), Klearia, Kloé, KURZ, LabCyte (Beckman Coulter), LexaGene, LioniX International (Magic Micro), Little Things Factory, (Plan Optik), L’Oréal, Luminex Corporation, MakeFluidics, MBio, MedSpray, MeMed, Menarini Silicon Biosystems, Mesa Biotech, MGI (BGI), Micralyne, MicroDrop Technologies, Microfluidic ChipShop, MicroLiquid, Micronit, Microsaic Systems, MilliDrop, Mimetas, Minicare, MiniFAB (Schott), Mission Bio, Mobidiag, Mobinostics (Boehringer Ingelheim), Nabsys, Namocell, NanoCellect Biomedical, NanoEntek, Nanomix, Nanopass, Nanoscribe, NanoString Technologies, NASA, Natech Plastics, NeuMoDx (Qiagen), Nokia, Nypro (Jabil), Omniome, Ontera, OPKO Diagnostics, Oxford Nanopore Technologies, Pacific Biosciences, Parallex Bioassays, PathogenDx, PharmaFluidics, Phase Three Product Development, Philips Innovation Services, POC Medical Systems, Precision Nanosystems, Qiagen, Qorvo, Qorvo Biotechnologies, Quantapore, Quanterix, Quantum Biosystems, QuantuMDx, Quidel, Qvella Corporation, RAB-Microfluidics, RainDance Technologies (Bio-Rad), RedBud Labs, Redshift Bioanalytics, Rheonix, Roche Diagnostics, Rogue Valley Microdevices, Roswell Biotechnologies, rqmicro, Samplix, Samsung, Sandstone Diagnostics, Sanwa Biotech, SawDx, Schlumberger, Schott, Schott Nexterion, Scienion, Sciex, Sensera, Shimadzu, Siemens, Sight Diagnostics, Silex Microsystems, SMB (Zoetis), Sophion Bioscience, Sphere Fluidics, Spinchip Diagnostics, SpinDiag, Stat-Dx (Qiagen), Stilla Technologies, STMicroelectronics, Stratec, Surfix (LioniX), Symbient Product Development,T2 Biosystems, Talis Biomedical, TearLab, Tecan, Technicolor, Technicolor Precision BioDevices, Tecnisco, Teledyne Dalsa, thinXXS (IDEX), Toolbox Medical Innovations, Translume, Trilobite, Trinean (Unchained Labs), Tronics Microsystems, TSMC, TTP Group, Two Pore Guys (Ontera), uFluidix, Universal Sequencing Technology, Varioptic (Invenios, Corning), Vaxxas, Velabs, Veredus Laboratories, Vortex Biosciences, WaferGen Biosystems (Takara Bio), Waters, Weidmann Plastics, Wi, Zimmer & Peacock, z- microsystems, Zoetis, Zomedica Pharmaceuticals, and more. Status of the Microfluidics Industry | Report | www.yole.fr | ©2019 COMPANIES CITED IN THIS REPORT 380+ slides of market and technology analysis Information gathered through direct discussions with players all along the supply chain

- 4. 4 Glossary and definitions p.2 Table of contents p.3 Report objectives p.5 Report scope p.6 Report methodology p.7 About the authors p.8 Companies cited in this report p.9 What we got right, What we got wrong p.10 Who should be interested by this report p.11 Yole Group related reports p.12 Executive Summary p.15 Context p.52 o Definition – our vision of microfluidics o Microfluidics – advantages and drawbacks o Our vision of the microfluidics market o Examples of applications that use microfluidic products o Why are microfluidic solutions used? o Microfluidic applications – definitions Market forecasts p.62 o Market segmentation o Market forecasts for microfluidic products and devices (units and value) o Segment dynamics (CAGR vs. Segment size) o How the value is spread across the supply chain o What we got right/wrong and why o Material mix analysis o Conclusion TABLE OF CONTENTS Part 1/2 Market trends p.87 o An increasing on-chip complexity for ever more integration and automation o Razor and razor-blade business model o A myriad of microfluidic players o In-house vs. Outsourced production o The lure of high-volume microfluidic device production o Reaching commercial success is not an easy path o Addressing other markets before human diagnostics, a wrong good idea? o Road to market: comparison of applications o Distribution networks are key for success o Examples of distribution agreements o A limited market for the fabs o Is the key to success out of point-of-care? o The market growth paradox! o Reasons why companies choose to internalize production o The barriers of in-house production o Why don’t large companies work (much) with the fabs? o A fight to acquire value o Significant new entrants o Towards standardized cartridge footprints? o Having a fixed design and a secured supply chain is mandatory o Combining the development of instrument and consumable o Importance of multiplexing and wide assay menu o The development of « open platform » business models o Standardization of microfluidic devices: setting-up an ISO norm o Success of Microfluidic technologies - Dream or reality? o Financial analysis of publicly listed companies

- 5. 5 TABLE OF CONTENTS Part 2/2 Microfluidic segments description p.139 o Clinical and veterinary testing o Point-of-care testing o Industrial, environmental, and agro-food testing o Pharmaceutical and life science research o Micro-reaction and flow chemistry o Analytical devices o Drug delivery o Accurate dispensing o Flow control components and modules o Emerging applications Focus: Microfluidic technologies for biotech applications p.203 o Overview o Single-cell isolation and analysis o Cell line development o Gene editing and therapeutics o Supply chain and business models Market shares & supply chain p.266 o Different models for different volumes o Microfluidic integrators, per material o Microfluidic integrators: 2018 market share o Main mergers and acquisitions since 2017 + analysis o Fundraising since 2017 + analysis o Microfluidic fabs: overview, geographical location, materials, ranking o Other levels of the supply chain (design houses, prototyping houses, materials providers, etc.) o Analysis of recent acquisitions of microfluidic fabs o Who’s working with who? Technology trends p.341 o Materials & hybrid integration o Manufacturing processes comparison o Reshaping processes o Subtractive processes o 3D printing o Combination of manufacturing expertise o Cost analysis: cost of goods, yield, split across the manufacturing process, contribution of the device in the final product selling price, gross margin analysis o Detection methods + focus on acoustic detection methods o Integration of complex sample prep steps o Multiplexing: high-plex vs. low-plex o Smartphone-based diagnostic products o Mixing technologies Outlooks p.374 o Conclusions Yole Corporate Presentation p.380

- 6. 6 This new Yole Développement report provides a complete analysis of microfluidic device/product applications, markets, and technologies: o New major trends and evolutions in the microfluidics industry markets and business models o Analysis of strategic moves since 2017: mergers and acquisitions, fundraising, etc. o New microfluidic players/foundries - 2018 rankings o Updated market data and forecast up to 2024, in value and units for microfluidic devices and products o Supply chain description and analysis In order to better understand how value is distributed across the supply chain, this report covers both the microfluidic device and microfluidic-based product markets Market trends and main players are presented for each product category via an exclusive market segmentation An exhaustive analysis is supplied covering the materials and manufacturing processes in various microfluidic segments Also furnished is a presentation of new, promising applications for microfluidic technologies REPORT OBJECTIVES

- 7. 7 REPORT SCOPE Yours needs are out of the report’ scope? Contact us for a custom: Other methods controlling very small fluid volumes Microfluidics is the science and technology that deals with the manipulation of fluids, usually in the range of microliters (10-6) to picoliters (10-12) and/or in networks of micrometer-size channels Our definition of microfluidics encompasses: Micro-fabricated devices with channels below ~500µm in size and/or

- 8. 8 METHODOLOGIES & DEFINITIONS Market Volume (in Munits) ASP (in $) Revenue (in $M) Yole’s market forecast model is based on the matching of several sources: Information Aggregation Preexisting information

- 9. 9 WHO SHOULD BE INTERESTED IN THIS REPORT? Financial & strategic investors: o Realize microfluidic technologies’ potential o See the latest moves within the industry o Learn the sweet spots and growing applications, and understand end-users’ objectives R&D players: o Understand new challenges linked to microfluidic technologies o Address the right market with the right technology Healthcare & governmental organizations: o Evaluate microfluidic technologies’ benefits o Identify relevant companies Diagnostics, pharmaceutical, biotechnology, industrial, and other companies: o Understand what is “state of the art” in microfluidic technologies, and which solutions could bring operational benefits o Identify the different players across the supply chain o Comprehend behavior evolution o Highlight competitors and targets for collaborations or M&A Microfluidic foundries and device makers: o Grasp technical requirements o Recognize business opportunities and prospects o Understand the evolution of the supply chain MEMS, electronics, and optics players: o Perceive the microfluidics market and technologies o Interpret the requirements for market entry

- 10. Report sample

- 11. 11 Microfluidic Applications MICROFLUIDIC APPLICATIONS - DEFINITION Microfluidic technology is used everywhere Clinical & Veterinary Diagnostics Point-of- Care Diagnostics Pharma & Life Science Research Analytical Devices Industrial, Environmental & Agro-Food Drug Delivery Micro Reaction - Flow Chemistry • Clinical and Veterinary Diagnostics Laboratory equipment for clinical and veterinary diagnostics • Point-of-Care Diagnostics Diagnostic equipment for out-of-reference laboratory, near- patient testing (intensive care, doctor’s offices, home testing, etc.) • Pharmaceutical and Life Science Research Microfluidic devices for drug discovery and screening, genomics, proteomics, cell analysis • Analytical Devices Microfluidic chips and columns for mass spectrometry, chromatography, and HPLC sample preparation • Industrial, Environmental, and Agro-FoodTesting Microfluidic-based tests for quality/process control and food/water testing (pesticides, bacteria, etc.). Includes military, security, and forensics applications. • Drug delivery Microfluidic devices for drug delivery, such as inhalers, microneedles, and implantable micropumps • Micro Reaction - Flow Chemistry Microfluidic devices for micro reaction involved in research or in pilot-production units

- 12. 12 INTRODUCTION Microfluidics - advantages and drawbacks Reduced sample and reagent volumes Shorter times for liquid displacement, thermal transfers, and analysis Automation and integration of complex operations Precise liquid control Diffusion-based mixing (due to highly-viscous forces) takes time Actuation is required for improving mixing steps Better control of chemical reactions Improved safety for chemical reactions

- 13. 13 INTRODUCTION Our vision of the microfluidics market (1/3) Example: Binx Health analyzer Microfluidic device: chip (raw hardware) Microfluidic product: cartridge with reagents and packaging Example: Binx Health cartridge Microfluidic analyzer

- 14. 14 We divided microfluidic technologies into two types of components in order to better explain the microfluidics market: o Microfluidic device: • A microfluidic device is defined as a micro-structured component in which a fluid will flow when it will be used. This can be a chip, a dispensing tool, a flow control component, or other microfluidic component types. It a the first-level packaged component. • Microfluidic chips represent 85% (in value) of the microfluidic device market. o Microfluidic product: • A microfluidic product is defined as the microfluidic device packaged for sale to the end-user • When needed, reagents and biological content are added to the device to create the product. It can be surface functionalization with antibodies or nucleic acid probes, liquid buffers in blisters, deposition of dry reagents, etc. • For example, in point-of-care applications, the microfluidic product is a microfluidic device to which reagents are added. The functionalized chip is packaged into a cartridge (often in plastic) with all the other required elements. • Complex cartridges can sometimes integrate tens or even hundreds of elements! We also consider microfluidic instruments for detection (diagnostics: chip readers), for droplet generation, for flow/pressure control, for dispensing, etc. However, these instruments are not quantified (either in volume nor in value) in this report. INTRODUCTION Our vision of the microfluidics market (2/3)

- 15. 15 INTRODUCTION Our vision of the microfluidics market (3/3) Most microfluidic devices are chips. When combined with biological content and packaged into cartridges, these chips become products. Chips Other Devices Microfluidic product breakdown for chips and other devices in 2018, in $B Chips $2.6B Other $0.4B Devices $3.0B Products $8.8B

- 16. 16 MARKET DATA AND FORECASTS

- 20. 20 FOCUS: MICROFLUIDIC TECHNOLOGIES FOR BIOTECH APPLICATIONS

- 21. 21 MARKET SHARES AND SUPPLY CHAIN (1/2)

- 22. 22 MARKET SHARES AND SUPPLY CHAIN (2/2)

- 24. 24 Contact our SalesTeam for more information Chinese Microfluidics Industry 2018 Point-of-Need Testing: Application of Microfluidic Technologies Next-Generation Sequencing & DNA Synthesis 2019 Liquid Biopsy: From Isolation to Downstream Applications 2018 YOLE GROUP RELATED REPORTS Yole Développement

- 25. 25 Contact our SalesTeam for more information Thermo Fisher Ion 520 DNA Sequencing Chip Status of the Microfluidics Industry | Report | www.yole.fr | ©2019 YOLE GROUP RELATED REPORTS System Plus Consulting

- 26. 26 Contact our SalesTeam for more information Nanopore Sequencing Patent Landscape Analysis 2019 Status of the Microfluidics Industry | Report | www.yole.fr | ©2019 YOLE GROUP RELATED REPORTS Knowmade

- 27. The first commercially-available lab-on-a- chip devices are now more than 20 years old. Microfluidic device complexity has increased ever since, leading to extremely sophisticated cartridges performing automated, complex sample preparation steps. Microfluidics is now a mature technology, and today the identified number of companies developing microfluidic- based solutions worldwide far surpasses a thousand (including myriad opportunistic start- ups), and the applications are end-less. As a consequence, Yole Développement’s (Yole) analysts estimate that the microfluidic products market reached $8.7B in 2018, and will grow at a CAGR2019-2024 of 11.7%, reaching $17.4B. The two principal applications are still point-of-care (PoC) testing and pharmaceutical/ life science research (including sequencing, genomics, and proteomics). However, the dynamics per application are evolving. While PoC devices are increasing in complexity and integrating more and more hybrid materials (i.e. glass + polymer, or silicon + polymer in order to offer additional functions), we also see high-end applications increasingly using polymer when possible, in order to decrease costs. Glass and silicon have a large share in these applications, especially in sequencing, but these semiconductor materials are increasingly integrated at the heart of complex plastic cartridges. This is also the case in drug delivery – even though most devices are made of glass and silicon today, we may soon observe the entry of polymer devices. Overall, thanks to increased commercial adoption, all three materials are growing nicely. In this report, Yole’s analysts present 2017 – 2024 market data and forecasts per application, with a detailed material mix analysis. STATUS OF THE MICROFLUIDICS INDUSTRY 2019 Market & Technology Report - August 2019 MICROFLUIDICS APPLICATIONS ARE GREATLY DIVERSIFYING, CREATING NEW OPPORTUNITIES Diversification of microfluidic technologies has led to burgeoning new applications and market growth, driving players’ interest and M&A. Global microfluidic devices and products market: 2019-2024 forecast WHAT’S NEW • Updated 2017 - 2024 market data and forecasts (in $US and units) for microfluidic devices and products, along with material mix analysis • Evolution and estimated 2018 microfluidic players’ market share at fab level and end-product level • Breakdown of the latest industry moves (M&A, fundraising), market and technology trends and evolutions, and potential acquisition targets • Updated information, by microfluidic market segment • Review of new, promising applications for microfluidic technologies (including a focus on biotechnology applications) • Comprehensive supply chain analysis KEY FEATURES • Provide a global view of the future for microfluidic devices and products • Establish an understanding of every microfluidics application, with an overview of the main players per application • Analyze microfluidic players’ dynamics and ranking, and understand the latest industry trends, strategic moves, and business models’ evolutions • Furnish 2017 and 2018 market data for microfluidic products and devices, along with 2019 – 2024 forecasts in units and $US • Explore technology, materials, and manufacturing trends • Explain how the supply chain is organized and how value is distributed across it THE ACQUISITION WAVE CONTINUES, LEADING TO AN IMPRESSIVELY RAPID STRUCTURATION For the last decade, PoC has been considered microfluidics’ greatest promise, with the potential for rapid-testing cartridges to reach millions of units per year.Nonetheless,the mass production of such devices is still far from being widespread, and companies now realize that the barriers are high on the road to success.Just having a good technology is not enough: financial strength, supply chain security, regulatory, and market access are also mandatory. In particular, numerous companies struggle to reach the next step because of a weak commercial network. Thus, acquisition by a larger company is often a good way to gain access to an established distributionnetworkandimprovedlogisticssupport. BioFire (bioMérieux), IQuum (Roche), and Cepheid (Danaher) are good examples of technologies that have literally taken off after acquisition, and we will see in the coming years whether recently- acquired companies like GenePOC (Meridian Biosciences) and Abaxis (Zoetis) mimic these successes. Overall, large diagnostic companies have acquired numerous promising or successful microfluidic technologies through the purchase of small and medium-size companies, to the extent that a group of around 15 players now represents more than 75% of the market.This is an impressive concentration, especially given the variety of applications. Contrarily, hundreds of start-ups with low revenue struggle to reach commercial success for the reasons mentioned above. In-between, we find around 50 players with $10M – 100M in microfluidics revenue, mostly start-ups that have accessed the next steps and are now likely acquisition targets. (Yole Développement,August 2019)

- 28. STATUS OF THE MICROFLUIDICS INDUSTRY 2019 At another supply chain level, we observe an impressive structuration. Indeed, the microfluidic device manufacturers (“fabs”) have experienced a strong wave of acquisitions by larger players since 2015 – the latest being MiniFAB in June 2019. Such larger players thus acquire their own production facilities and aim to produce for larger customers from the diagnostics and life sciences fields, which fabs today struggle to address. Overall, after the recent acquisitions, the only remaining established microfluidic fabs above $10M in revenue and still independent are Micronit and Microfluidic ChipShop. Last but not least, over the past two years several large companies (leaders in other technology fields) have decided to enter or strengthen their position in the microfluidics market: this is the case for Technicolor, Qorvo Biotechnologies, and Schott. Such decisions exemplify the attractiveness of this dynamic field, which presents a viable opportunity for these companies to find new growth areas. They will soon be followed by others – in fact, we are aware of several players that are preparing to enter the microfluidics field, at diverse levels of the supply chain! MICROFLUIDIC TECHNOLOGIES ARE PENETRATING VARIOUS FLOURISHING APPLICATIONS, WHERE THE CHALLENGES ARE BIG BUT THE POTENTIAL IS SIGNIFICANT Emerging applications, in particular within the biotechnology field, can benefit from the improvement of microfluidic technologies which represent valuable tools for complex operations. Today, academics and researchers are the main users of such technologies in biotech, but we have begun seeing an increased adoption from pharmaceutical companies, Contract Research Organizations (CRO), and industrial biotech companies: for example, cell line development, single-cell isolation/analysis, as well as cell-gene therapies and gene editing, are all applications where microfluidics have a role to play. In particular, microfluidics is receiving enthusiastic response from single-cell isolation, where there are already several successful commercialized technologies. The other applications mentioned above are steadily emerging, and it is time for innovative microfluidic companies to take the opportunity to solve the issues linked to integration, automation, throughput increase, etc. Indeed, most solutions used today are expensive and low-throughput, and thus prone to human error due to manual operations. In this report, Yole’s analysts describe the challenges these fields face and how microfluidic technologies, for example droplet microfluidics, can address the bottlenecks and forge new possibilities. *Non-exhaustive list of companies Single-cell isolation Cell line development Gene editing and therapeutics Non droplet microfluidics technologies Microfluidic technologies droplets Not yet in commercial production Still at very early stage of R&D Not yet in commercial production Still at very early stage of R&D Not yet in commercial production Established application Emerging application (Yole Développement,August 2019) Microfluidic players* landscape per revenue (Yole Développement,August 2019) Players* involvement in microfluidic technologies for biotechnology applications matrix *Non-exhaustive list of companies *Non-exhaustive list of companies

- 29. AUTHORS Sébastien Clerc works as a Technology & Market Analyst, Microfluidics & Medical Technologies at Yole Développement (Yole). As part of the Life Sciences & Healthcare division, Sébastien has authored a collection of market and technology reports dedicated to topics such as microfluidics, point-of- care, MEMS for healthcare applications and connected medical devices. In parallel, he is daily involved in custom projects such as strategic marketing, technology scouting and technology evaluation to help academic and industrial players in their innovation processes. Thanks to his technology & market expertise, Sébastien has spoken in more than 10 industry conferences worldwide over the last 2 years. Sébastien Clerc graduated from Grenoble Institute of Technology (Grenoble INP - Grenoble, France) with a Master’s degree in Biomedical Technologies. He then completed his cursus with a Master’s degree in Innovation and Technology Management in the same institute. COMPANIES CITED IN THE REPORT (non exhaustive list) 3M, 10X Genomics, Abaxis (Zoetis), Abbott, Alere (Abbott), Achira Labs, Affymetrix (Thermo Fisher Scientific), AGC, Agilent Technologies, Akatsuki Tech, Akonni Biosystems, Allevi, ALine, Alveo Technologies, Angle plc, Applied Microarrays, Araymond Life, Arrayit, Arrayjet, Ativa Medical, Atlas Genetics (binx health), AutoGenomics (Prescient Medicine), AxoSim, Axxicon, Axxin, Balda AG (Stevanato Group), Base4 Innovation, BD, BGI, binx health, Biocartis, Biocept, BioFire Diagnostics (bioMérieux), BioFluidica, Biolidics, Bionano Genomics, Bio-Rad, BioSensia (Kypha), Biosurfit, BOE, Boehringer Ingelheim, Boehringer Ingelheim microParts, Bosch Vivalytic (Bosch Healthcare), Bronkhorst, Caliper Life Sciences (PerkinElmer), Cambridge Consultants, CapitalBio Corporation, Capsum, Carville, CBio, CDA, Cellenion (Scienion), Celsee Diagnostics, Centrillion Technologies, Cepheid (Danaher), CG.TEC Injection, Chemtrix, CiDRA Precision Services (IDEX), CombiMatrix (Invitae), Corium Corning, CorSolutions, Curetis, Cygnus Biosciences, Cytena, Cytosurge, Daktari Diagnostics, DARPA, Debiotech, Denz Bio-Medical, Dianax, DiaSorin Molecular, DNAe and more. As a Technology & Market Analyst, Biotechnologies & Molecular Innovations, Medical Technologies in the Life Sciences & Healthcare division at Yole Développement (Yole), Asma Siari is involved in the development of technology & market reports as well as the production of custom consulting projects. After a Master’s degree in Biotechnologies, Diagnostic Therapeutics & Management, Asma served as Research Assistant at the Moores Cancer Center (San Diego, CA). She is a coauthor in three scientific publications published in the Molecular Cancer Research Journal. Asma Siari graduated with an Advanced Master’s degree in International Strategy & Marketing BtoB from EM Lyon Business School (France). Executive summary 15 Context 52 Definition – our vision of microfluidics Microfluidics – advantages and drawbacks Applications that use microfluidic products Market forecasts 62 Market segmentation Market forecasts for microfluidic products and devices (units and value) and segment dynamics How value is spread across the supply chain What we got right/wrong, and why Material mix analysis Market trends 87 An increasing on-chip complexity Razor and razor-blade business model In-house vs. outsourced production The lure of high-volume microfluidic device production Attaining commercial success is not easy Road to market: applications comparison Reasons why companies choose to internalize production The barriers of in-house production A fight to acquire value Significant new entrants The development of « open platform » business models Success of microfluidic technologies – dream or reality? Financial analysis of publicly-listed companies Microfluidic segments description 139 Clinical and veterinary testing Point-of-care testing Industrial, environmental, and agro-food testing Pharmaceutical and life science research Micro-reaction and flow chemistry Analytical devices Drug delivery Accurate dispensing Flow control components and modules Emerging applications Focus : Microfluidic technologies for biotech applications 203 Single-cell isolation and analysis Cell line development Gene editing and therapeutics Supply chain and business models Market shares and supply chain 266 Different models for different volumes Microfluidic integrators, per material Microfluidic integrators – 2018 market share Main MAs and fundraising since 2017 Microfluidic fabs: overview, geographical location, materials, ranking Other levels of the supply chain (design houses, prototyping houses, materials providers, etc.) Analysis of recent microfluidic fabs’ acquisitions Who’s working with who? Technology trends 341 Materials and hybrid integration Manufacturing processes description and comparison Cost analysis: cost of goods, yield, split across the manufacturing process, contribution of the device in the final product selling price, gross margin analysis Detection methods Conclusions 374 TABLE OF CONTENTS (complete content on i-Micronews.com) • Chinese Microfluidics Industry 2018 • Point-of-Need Testing: Application of Microfluidic Technologies • Liquid Biopsy: From Isolation to Downstream Applications 2018 • Nanopore Sequencing 2019 – Patent Landscape Analysis – by KnowMade Find all our reports on www.i-micronews.com RELATED REPORTS Benefit from our Bundle Annual Subscription offers and access our analyses at the best available price and with great advantages MARKET TECHNOLOGY REPORT

- 30. ORDER FORM Status of the Microfluidics Industry 2019 SHIPPING CONTACT First Name: Email: Last Name: Phone: PAYMENT BY CREDIT CARD Visa Mastercard Amex Name of the Card Holder: Credit Card Number: Card Verification Value (3 digits except AMEX: 4 digits): Expiration date: BY BANK TRANSFER BANK INFO: HSBC, 1 place de la Bourse, F-69002 Lyon, France, Bank code: 30056, Branch code: 00170 Account No: 0170 200 1565 87, SWIFT or BIC code: CCFRFRPP, IBAN: FR76 3005 6001 7001 7020 0156 587 RETURN ORDER BY • MAIL: YOLE DÉVELOPPEMENT, Le Quartz, 75 Cours Emile Zola, 69100 Villeurbanne/Lyon - France SALES CONTACTS • Western US Canada - Steve Laferriere: + 1 310 600-8267 – laferriere@yole.fr • Eastern US Canada - Chris Youman: +1 919 607 9839 – chris.youman@yole.fr • Europe RoW - Lizzie Levenez: + 49 15 123 544 182 – levenez@yole.fr • Japan Rest of Asia - Takashi Onozawa: +81-80-4371-4887 – onozawa@yole.fr • Greater China - Mavis Wang: +886 979 336 809 – wang@yole.fr • Korea - Peter OK: +82 10 4089 0233 – peter.ok@yole.fr • Specific inquiries: +33 472 830 180 – info@yole.fr (1) Our Terms and Conditions of Sale are available at www.yole.fr/Terms_and_Conditions_of_Sale.aspx The present document is valid 24 months after its publishing date: August 22, 2019 / ABOUT YOLE DEVELOPPEMENT BILL TO Name (Mr/Ms/Dr/Pr): Job Title: Company: Address: City: State: Postcode/Zip: Country*: *VAT ID Number for EU members: Tel: Email: Date: PRODUCT ORDER - Ref YD19037 Please enter my order for above named report: One user license*: Euro 5,990 Multi user license: Euro 6,490 - The report will be ready for delivery from September 9, 2019 - For price in dollars, please use the day’s exchange rate. All reports are delivered electronically at payment reception. For French customers, add 20% for VAT I hereby accept Yole Développement’s Terms and Conditions of Sale(1) Signature: *One user license means only one person at the company can use the report. Founded in 1998, Yole Développement (Yole) has grown to become a group of companies providing marketing, technology and strategy consulting, media and corporate finance services, reverse engineering and reverse costing services and well as IP and patent analysis. With a strong focus on emerging applications using silicon and/or micro manufacturing, the Yole group of companies has expanded to include more than 120 collaborators worldwide covering MEMS and image sensors, Compound semiconductors, RF Electronics, Solid-state lighting, Displays, Software, Optoelectronics, Microfluidics Medical, Advanced Packaging, Manufacturing, Power Electronics, Batteries Energy Management and Memory. The “More than Moore” market research, technology and strategy consulting company Yole Développement, along with its partners System Plus Consulting, PISEO, KnowMade and Blumorpho, supports industrial companies, investors and RD organizations worldwide to help them understand markets and follow technology trends to grow their business. CONSULTING AND ANALYSIS • Market data research, marketing analysis • Technology analysis • Strategy consulting • Reverse engineering costing • Patent analysis • Design and characterization of innovative optical systems • Financial services (due diligence, MA with our partner) More information on www.yole.fr MEDIA EVENTS • i-Micronews.com website, application related e-newsletter • Communication webcast services • Events: TechDays, forums… More information on www.i-Micronews.com REPORTS • Market technology reports • Patent investigation and patent infringement risk analysis • Structure, process and cost analysis and teardowns • Cost simulation tool More information on www.i-micronews.com/reports CONTACTS For more information about : • Consulting Financial Services: Jean-Christophe Eloy (eloy@yole.fr) • Reports Monitors: David Jourdan (jourdan@yole.fr) Fayçal Khamassi (khamassi@yole.fr) • Marketing Communication: Camille Veyrier (veyrier@yole.fr) • Public Relations: Sandrine Leroy (leroy@yole.fr)

- 31. © 2019 Yole Développement From Technologies to Market Source: Wikimedia Commons

- 32. 28©2019 | www.yole.fr | About Yole Développement YOLE DEVELOPPEMENT – FIELDS OF EXPERTISE Life Sciences Healthcare o Microfluidics o BioMEMS Medical Microsystems o Inkjet and accurate dispensing o Solid-State Medical Imaging BioPhotonics o BioTechnologies Power Wireless o RF Devices Technologies o Compound Semiconductors Emerging Materials o Power Electronics o Batteries Energy Management Semiconductor Software o Package,Assembly Substrates o Semiconductor Manufacturing o Memory o Software Computing Photonics, Sensing Display o Solid-State Lighting o Display o MEMS, Sensors Actuators o Imaging o Photonics Optoelectronics Semiconductor Software Power Wireless Photonics, Sensing Display Life Sciences Healthcare About Yole Développement | www.yole.fr | ©2019

- 33. 29©2019 | www.yole.fr | About Yole Développement 4 BUSINESS MODELS o Consulting and Analysis • Market data research, marketing analysis • Technology analysis • Strategy consulting • Reverse engineering costing • Patent analysis • Design and characterization of innovative optical systems • Financial services (due diligence, MA with our partner) www.yole.fr o Syndicated reports • Market technology reports • Patent investigation and patent infringement risk analysis • Teardowns reverse costing analysis • Cost simulation tool www.i-Micronews.com/reports o Media • i-Micronews.com website and application • i-Micronews e-newsletter • Communication webcast services • Events:TechDays, forums,… www.i-Micronews.com o Monitors • Monthly and quarterly update • Excel database covering supply, demand, and technology • Price, market, demand and production forecasts • Supplier market shares www.i-Micronews.com/reports About Yole Développement | www.yole.fr | ©2019

- 34. 30©2019 | www.yole.fr | About Yole Développement 6 COMPANIES TO SERVEYOUR BUSINESS Due diligence www.yole.fr Manufacturing costs analysis Teardown and reverse engineering Cost simulation tools www.systemplus.fr Market, technology and strategy consulting www.yole.fr IP analysis Patent assessment www.knowmade.fr Innovation and business maker www.bmorpho.com Design and characterization of innovative optical systems www.piseo.fr Yole Group of Companies About Yole Développement | www.yole.fr | ©2019

- 35. 31 OUR GLOBAL ACTIVITY 30%of our business 40%of our business 30%of our business Greater China office Yole Japan HQ in Lyon Nantes Paris Nice Vénissieux Yole Deutschland Frankfurt Hsinchu Tokyo Yole Korea Seoul Palo Alto Yole Inc. Cornelius About Yole Développement | www.yole.fr | ©2019

- 36. 32©2019 | www.yole.fr | About Yole Développement ANALYSIS SERVICES - CONTENT COMPARISON High Technology and Market Report Leadership Meeting QA Service Depth of the analysis Breadthoftheanalysis Meet the Analyst Custom Analysis High Low About Yole Développement | www.yole.fr | ©2019

- 37. 33©2019 | www.yole.fr | About Yole Développement SERVING THE ENTIRE SUPPLY CHAIN Our analysts provide market analysis, technology evaluation, and business plans along the entire supply chain Integrators, end- users and software developers Device manufacturers Suppliers: material, equipment, OSAT, foundries… Financial investors, RD centers About Yole Développement | www.yole.fr | ©2019

- 38. 34©2019 | www.yole.fr | About Yole Développement SERVING MULTIPLE INDUSTRIAL FIELDS We work across multiples industries to understand the impact of More-than- Moore technologies from device to system From A to Z… Transportation makers Mobile phone and consumer electronics Automotive Medical systems Industrial and defense Energy management About Yole Développement | www.yole.fr | ©2019

- 39. 35 o Over the course of more than 20 years, Yole Développement has grown to become a group of companies. Together with System Plus Consulting and KnowMade, we now provide marketing, technology and strategy consulting, media and corporate finance services, reverse costing, structure, process and cost analysis services and well as intellectual property (IP) and patent analysis. Together, our group of companies is collaborating ever closer and therefore will offer, in 2019, a collection of over 125 reports, 10 new monitors and 120 teardowns. Combining respective expertise and methodologies from the three companies, they cover: o If you are looking for: • An analysis of your product market and technology • A review of how your competitors are evolving • An understanding of your manufacturing and production costs • An understanding of your industry’s technology roadmap and related IPs • A clear view supply chain evolution Our reports and monitors are for you! o Our team of over 70 analysts, including PhD and MBA qualified industry veterans from Yole Développement, System Plus Consulting and KnowMade, collect information, identify trends, challenges, emerging markets, and competitive environments. They turn that information into results and give you a complete picture of your industry’s landscape. In the past 20 years, we have worked on more than 2,000 projects, interacting with technology professionals and high-level opinion makers from the main players of their industries and realized more than 5,000 interviews per year. WHAT TO EXPECT IN 2019? In 2019 we will extend our offering with a new ‘monitor’ product which provides more updates on your industry during the year. The Yole Group of Companies is also building on and expanding its investigations of the memory industry. Moreover, in parallel, the Yole Group reaffirms its commitment to a new collection of reports mixing software and hardware and is increasing its involvement in displays, radio-frequency (RF) technology, advanced substrates, batteries and compound semiconductors. Last but not least, System Plus Consulting is developing its teardowns service providing 120+ offers related to phones, smart home, wearables and connected devices. Discover our 2019 program right now, and ensure you get a true vision of the industry. Stay tuned! REPORTS COLLECTION www.i-Micronews.com • MEMS Sensors • RF devices technologies • Medical technologies • Semiconductor Manufacturing • Advanced packaging • Memory • Batteries and energy management • Power electronics • Compound semiconductors • Solid state lighting • Displays • Software • Imaging • Photonics About Yole Développement | www.yole.fr | ©2019

- 40. 36 OUR 2019 REPORTS COLLECTION (1/4) 18 fields of excellence combined with six markets to provide a complete picture of your industry landscape Market –Technology – Strategy – byYole Développement Yole Développement (Yole) offers market reports including quantitative market forecasts, technology trends, company strategy evaluation and indepth application analyses. Yole will publish more than 55 reports in 2019, with our partner PISEO contributing to some of the lighting reports. Reverse Costing® – Structure, Process and Cost Analysis – by System Plus Consulting The Reverse Costing® report developed by System Plus Consulting provides full teardowns, including detailed photos, precise measurements, material analyses, manufacturing process flows, supply chain evaluations, manufacturing cost analyses and selling price estimations. The reports listed below are comparisons of several analyzed components from System Plus Consulting. More reports are however available, and over 60 reports will be released in 2019.The complete list is available at www.systemplus.fr. Patent Reports – by KnowMade More than describing the status of the IP situation, these analyses provide a missing link between patented technologies and market, technological and business trends. They offer an understanding of the competitive landscape and technology developments from a patent perspective. They include key insights into key IP players, key patents and future technology trends. For 2019 KnowMade will release over 15 reports. The markets targeted are : • Mobile Consumer • Automotive Transportation • Medical • Industrial • Telecom Infrastructure • Defense Aerospace • Linked reports are dealing with the same topic to provide • a more detailed analysis. About Yole Développement | www.yole.fr | ©2019

- 41. 37 OUR 2019 REPORTS COLLECTION (1/5) 18 fields of excellence combined with six markets to provide a complete picture of your industry landscape MEMS SENSORS o MARKET ANDTECHNOLOGY REPORT • Status of the MEMS Industry 2019 - Update • Status of the Audio Industry 2019 - New • Uncooled Infrared Imagers and Detectors 2019 – Update • Consumer Biometrics:Technologies and MarketTrends 2018 • MEMS Pressure Sensor Market and Technologies 2018 • Gas Particle Sensors 2018 o STRUCTURE, PROCESS COST REPORT • MEMS Sensors Comparison 2019 • MEMS Pressure Sensor Comparison 2018 • Particle Sensors Comparison 2019 • Miniaturized Gas Sensors Comparison 2018 o PATENT REPORT • MEMS Foundry Business Portfolio 2019 - New • Miniaturized Gas Sensors 2019 - New PHOTONIC AND OPTOELECTRONICS o MARKET ANDTECHNOLOGY REPORT • Silicon Photonics and Photonic Integrated Circuits 2019 • LiDARs for Automotive and Industrial Applications 2019 - Update o PATENT REPORT • Silicon Photonics for Data Centers: Optical Transceiver 2019 - New • LiDAR for Automotive 2018 RF DEVICES ANDTECHNOLOGIES o MARKET ANDTECHNOLOGY REPORT • RF GaN Market:Applications, Players,Technology, and Substrates 2019 - Update • 5G’s Impact on RF Front-End Module and Connectivity for Cell Phones 2019 – Update • 5G Impact on Telecom Infrastructure 2019 - New • Radar and Wireless for Automotive: Market and Technology Trends 2019 - Update • Passive Active Antenna Systems for Telecom Infrastructure 2019 - New • RF Standards and Technologies for Connected Objects 2018 o STRUCTURE, PROCESS COST REPORT • RF Front-End Module Comparison 2019 - Update • Automotive Radar RF Chipset Comparison 2018 o PATENT REPORT • Antenna for 5G Wireless Communications 2019 - New • RF Front End Modules for Cellphones 2018 • RF Filter for 5G Wireless Communications: Materials and Technologies 2019 • RF GaN 2019 – Patent Landscape Analysis Update : 2018 version still available About Yole Développement | www.yole.fr | ©2019

- 42. 38 OUR 2019 REPORTS COLLECTION (2/5) 18 fields of excellence combined with six markets to provide a complete picture of your industry landscape IMAGING o MARKET ANDTECHNOLOGY REPORT • Status of the CIS Industry 2019:Technology and Foundry Business - Update • Imaging for Automotive 2019 - Update • NeuromorphicTechnologies for Sensing 2019 - Update • Status of the CCM and WLO Industry 2019 – Update • 3D Imaging Sensing 2018 • MachineVision for Industry and Automation 2018 • Sensors for RoboticVehicles 2018 o STRUCTURE, PROCESS COST REPORT • Compact Camera Modules Comparison 2019 • CMOS Image Sensors Comparison 2019 o PATENT REPORT • Facial Gesture Recognition Technlogies in Mobile Devices 2019 - New • Apple iPhone X Proximity Sensor Flood Illuminator 2018 MEDICAL IMAGING AND BIOPHOTONICS o MARKET ANDTECHNOLOGY REPORT • X-Ray Detectors for Medical, Industrial and Security Applications 2019- New • Microscopy Life Science Cameras: Market and Technology Analysis 2019 • Ultrasound technologies for Medical, Industrial and Consumer Applications 2018 o PATENT REPORT • Optical Coherence Tomography Medical Imaging 2018 MICROFLUIDICS o MARKET ANDTECHNOLOGY REPORT • Status of the Microfluidics Industry 2019 - Update • Next Generation Sequencing DNA Synthesis - Technology, Consumables Manufacturing and MarketTrends 2019 - New • Organ-on-a-Chip Market Technology Landscape 2019 - Update • Point-of-Need Testing Application of MicrofluidicTechnologies 2018 • Liquid Biopsy: from Isolation to Downstream Applications 2018 • Chinese Microfluidics Industry 2018 o PATENT REPORT • Microfluidic ManufacturingTechnologies 2019 – New • Nanopore Sequencing 2019 - New INKJET AND ACCURATE DISPENSING o MARKET ANDTECHNOLOGY REPORT • Inkjet Printheads - Dispensing Technologies Market Landscape 2019 - Update • Emerging Printing Technologies for Microsystem Manufacturing 2019 - New • Piezoelectric Devices from Bulk to Thin Film 2019 - New • Inkjet Functional and Additive Manufacturing for Electronics 2018 o STRUCTURE, PROCESS COST REPORT • Piezoelectric Materials from Bulk to Thin Film Comparison 2019 Update : 2018 version still available About Yole Développement | www.yole.fr | ©2019

- 43. 39 OUR 2019 REPORTS COLLECTION (3/5) 18 fields of excellence combined with six markets to provide a complete picture of your industry landscape BIOMEMS MEDICAL MICROSYSTEMS o MARKET ANDTECHNOLOGY REPORT • Medical Wearables: Market Technology Analysis 2019 - New • Neurotechnologies and Brain Computer Interface 2018 • BioMEMS Non-Invasive Sensors: Microsystems for Life Sciences Healthcare 2018 o PATENT REPORT • 3D Cell Printing 2019 - New • CirculatingTumor Cells Isolation 2019 - New SOFTWARE AND COMPUTING o MARKET ANDTECHNOLOGY REPORT • Artificial Intelligence Computing For Automotive 2019 - New • Hardware and Software for Artificial Intelligence (AI) in Consumer Applications 2019 - Update • Image Signal Processor andVision Processor Market and Technology Trends 2019 • xPU (Processing Units) for Cryptocurrency, Blockchain, HPC and Gaming 2019 – New • Artificial Intelligence for Medical Imaging 2019 - New o PATENT REPORT • Artificial Intelligence for Medical Diagnostics - New MEMORY o MARKET ANDTECHNOLOGY REPORT • Status of the Memory Industry 2019 - New • MRAM Technology and Business 2019 - New • Emerging NonVolatile Memory 2018 o STRUCTURE, PROCESS COST REPORT • Memory Comparison 2019 o PATENT REPORT • Magnetoresistive Random-Access Memory (MRAM) 2019 - New • 3D Non-Volatile Memory 2018 ADVANCED PACKAGING o MARKET ANDTECHNOLOGY REPORT • Fan Out PackagingTechnologies and MarketTrends 2019 - Update • 3D TSV Integration and Monolithic Business Update 2019 - Update • Advanced RF SiP for Cellphones 2019 - Update • Status of the Advanced Packaging Industry 2019 - Update • Status of the Advanced Substrates 2019 - Update • Panel Level PackagingTrends 2019 - Update • Automotive Packaging Market Technology Trends 2019 - New • Trends in Automotive Packaging 2018 • Thin-Film Integrated Passive Devices 2018 o STRUCTURE, PROCESS COST REPORT • Advanced RF SiP for Cellphones Comparison 2019 Update : 2018 version still available About Yole Développement | www.yole.fr | ©2019

- 44. 40 OUR 2019 REPORTS COLLECTION (4/5) 18 fields of excellence combined with six markets to provide a complete picture of your industry landscape SEMICONDUCTOR MANUFACTURING o MARKET ANDTECHNOLOGY REPORT • Nano-Imprint Technology Trends for Semiconductor Applications 2019 - New • Equipment and Materials for Fan Out Packaging 2019 - Update • Equipment for More than Moore:Thin Film Deposition Etching 2019 - New • Wafer Starts for More Than Moore Applications 2018 • Polymeric Materials atWafer-Level for Advanced Packaging 2018 • Bonding and Lithography Equipment Market for More than Moore Devices 2018 o STRUCTURE, PROCESS COST REPORT • Wafer Bonding Comparison 2018 o PATENT REPORT • Hybrid Bonding for 3D Stack 2019 – New BIOTECHNOLOGIES o MARKET ANDTECHNOLOGY REPORT • CRISPR-Cas9 Technology: From Lab to Industries 2018 o PATENT REPORT • Personalized Medicine 2019 – New SOLID STATE LIGHTING o MARKET ANDTECHNOLOGY REPORT • Status of the Solid State Light Source Industry 2019 - New • Edge Emitting Lasers (EELS) 2019 - New • Light Shaping Technologies 2019 - New • Automotive Advanced Front Lighting Systems 2019 - New • VCSELs – Market and Technology Trends 2019 - Update • IR LEDs and Laser Diodes – Technology,Applications, and Industry Trends 2018 • Automotive Lighting 2018:Technology, Industry and MarketTrends • UV LEDs - Technology, Manufacturing and ApplicationTrends 2018 • LiFi:Technology, Industry and MarketTrends 2018 o STRUCTURE, PROCESS COST REPORT • VCSEL Comparison 2019 o PATENT REPORT • VCSELs 2018 DISPLAY o MARKET ANDTECHNOLOGY REPORT • Next Generation 3D Displays 2019 - New • Next Generation Human Machine Interaction (HMI)in Displays 2019 - New • Micro-and Mini-LED Displays 2019 - Update • Next Generation TV Panels: New Technologies, Features and Market Impact 2019 • Displays OpticalVision Systems forVR,AR MR 2018 o PATENT REPORT • MicroLED Displays : Intellectual Property Landscape 2018 Update : 2018 version still available About Yole Développement | www.yole.fr | ©2019

- 45. 41 OUR 2019 REPORTS COLLECTION (5/5) 18 fields of excellence combined with six markets to provide a complete picture of your industry landscape POWER ELECTRONICS o MARKET ANDTECHNOLOGY REPORT • Power SiC: Materials, Devices and Applications 2019 - Update • Power Electronics for EV/HEV and e-mobility: Market, Innovations and Trends 2019 - Update • Status of the Power Electronics Industry 2019 - Update • Discrete Power Packaging : Material Market and Technology Trends 2019 - New • Status of the Power ICs Industry 2019 - Update • Status of the Passive Components for the Power Electronics Industry 2019 - Update • Status of the Inverter Industry 2019 - Update • Status of the Power Module Packaging Industry 2019 - Update • Wireless Charging Market Expectations and Technology Trends 2018 • Power GaN 2018: Epitaxy, Devices,Applications and Technology Trends o STRUCTURE, PROCESS COST REPORT • Automotive Power Module Packaging Comparison 2018 • GaN-on-Silicon Transistor Comparison 2019 • SiC Transistor Comparison 2019 o PATENT REPORT • Power SiC : Materials, Devices and Modules 2019 - New • Power GaN : Materials, Devices and Modules 2019 – Update BATTERY ENERGY MANAGEMENT o MARKET ANDTECHNOLOGY REPORT • Status of the Rechargeable Li-ion Battery Industry 2019 - New • Li-ion Battery Packs for Automotive and Stationary Storage Applications 2019 - Update o PATENT REPORT • Battery Energy Density Increase: Materials and EmergingTechnologies 2019 - New • Solid-State Batteries 2019 - New • Status of the Battery Patents 2018 COMPOUND SEMI. o MARKET ANDTECHNOLOGY REPORT • Emerging Semiconductor Substrates: Market Technology Trends 2019- New • Status of the Compound Semiconductor Industry 2019 - New • InP Materials, Devices and Applications 2019 - New • GaAsWafer and Epiwafer Market: RF, Photonics, LED and PV Applications 2018 o PATENT REPORT • GaN-on-Silicon Substrate: Materials, Devices and Applications 2019 - Update Update : 2018 version still available About Yole Développement | www.yole.fr | ©2019

- 46. 42 OUR 2019 MONITORS COLLECTION (1/2) Get the most updated overview of your market to monitor your strategy Yole Développement, System Plus Consulting and KnowMade, all part of the Yole Group of Companies, are launching a collection of 10 monitors in 2019. The monitors aim to provide updated market, technology and patent data as well dedicated quarterly analyses of the evolution in your industry over the previous 12 months. Furthermore, you can benefit from direct access to the analyst for an on-demand QA and discussion session regarding trend analyses, forecasts and breaking news. Topics covered will be compact camera modules (CCMs), advanced packaging, compound semiconductors, microfluidics, batteries, RF and memory. MARKET MONITOR byYole Développement A FULL PACKAGE: The monitors will provide the evolution of the market in units, wafer area and revenues. They will also offer insights into what is driving the business and a close look at what is happening will also be covered in it. The following deliverables will be included in the monitors: • An Excel database with all historical and forecast data • A PDF slide deck with graphs and comments/analyses covering the expected evolutions o ADVANCED PACKAGING – NEW This monitor will provide the evolution of the advanced packaging platforms. It will cover Fan-Out Wafer Level Packaging (WLP), Fan-Out Panel Level Packaging (PLP), Wafer-Level Chip Scale Packaging (WLCSP), Flip Chip packaging platforms, and 2.5D and 3D Through Silicon Via (TSV) integration. Frequency: Quarterly, starting from Q3 2019 o COMPOUND SEMI. – NEW This monitor will describe how the compound semiconductor industry is evolving. It will offer a close look at GaAs, InP, SiC, GaN and other compounds of interest providing wafer volumes, revenues, application breakdowns and momentum. Frequency: Quarterly, starting from Q3 2019 o CAMERA MODULE – NEW This monitor will provide the evolution of the imaging industry, with a close look at image sensor, camera module, lens and VCM. Volumes, revenues and momentum of companies like Sony, Samsung, Omnivision and OnSemi will thus be analysed. Frequency: Quarterly, starting from Q3 2019 o MEMORY – UPDATE For the memory industry you can have access to a quaterly monitor, as well as an additional service, a monthly pricing. Both services can be bought seprately: • DRAM Service: Including a quarterly monitor and monthly pricing. • NAND Service: Including a quarterly monitor and monthly pricing. REVERSETECHNOLOGY MONITOR by System Plus Consulting o SMARTPHONES – NEW To stay updated on the latest components, packaging and silicon chip choices of the smartphone makers, System Plus Consulting has created its first Smartphone Reverse Technology monitor. This year, get access to the packaging and silicon content database of at least 20 different flagship smartphones – more than five per quarter. Starting at the beginning of 2019, the monitor will include an Excel database report for each phone and a quarterly comparison. About Yole Développement | www.yole.fr | ©2019

- 47. 43 OUR 2019 MONITORS COLLECTION (2/2) Get the most updated overview of your market to monitor your strategy PATENT MONITOR by KnowMade A FULL PACKAGE: Starting at the beginning of the year, the KnowMade monitors include the following deliverables: • An Excel file including the monthly IP database of: • New patent applications • Newly granted patents • Expired or abandoned patents • Transfer of IP rights through re-assignment and licensing • Patent litigation and opposition • Quarterly report including a PDF slide deck with the key facts figures of the quarter: IP trends over the three last months, with a close look to key IP players and key patented technologies. o GaN for Power RF Electronics Wafers and epiwafers, GaN-on-SiC, silicon, sapphire or diamond, semiconductor devices such as transistors, and diodes, devices and applications including converters, rectifiers, switches, amplifiers, filters, and Monolothic Microwave Integrated Circuits (MMICs), packaging, modules and systems. o GaN for Optoelectronics Photonics Wafers and epiwafers, GaN-on-sapphire, SiC or silicon; semiconductor devices such as LEDs and lasers; and applications including lighting, display, visible communication, photonics, packaging, modules and systems. o Li-ion Batteries Anodes made of lithium metal, silicon, and lithium titanate (LTO); cathodes made of Lithium Iron Phosphate (LFP), Nickel-Manganese-Cobalt (NMC), Lithium Nickel Cobalt Aluminium Oxide (NCA), Lithium Nickel Metal Dioxide (LiNiMO2), Lithium Metal Phosphate (LiMPO4), and Lithium Metal Tetroxide (LiMO4); electrolytes including liquid, polymer/gel, and solid inorganics; ceramic and other separators; battery cells including thin film/microbattery, flexible, cylindrical and prismatic; and battery packs and systems. o Post Li-ion Batteries Battery technologies including redox-flow batteries, sodium-ion, lithiumsulfur, lithium- air, and magnesium-ion, and their supply chains, including electrodes, electrolytes, battery cells and battery packs/systems. o Solid-State Batteries Supply chain including electrodes, battery cells, battery packs/systems and electrolytes, including polymer, inorganic and inorganic/polymer, inorganic materials, including argyrodites, LIthium Super Ionic CONductor, (LISICONs), Thio-LISICONs, sulfide glasses, oxide glasses, perovskites, anti-perovskites and garnets. o RF Acoustic Wave Filters Including Surface Acoustic Wave (SAW), Temperature Compensated (TC)- SAW, Bulk Acoustic Wave- Free-standing Bulk Acoustic Resonator (BAWFBAR), BAW-Solidly- Mounted Resonator (BAW-SMR), and Packaging. o RF Power Amplifiers Including Low Noise Amplifiers, Doherty Amplifiers, Packaging, and Millimeter-Wave technology. o RF Front-End Modules o Microfluidics From components to chips and systems, including all applications. About Yole Développement | www.yole.fr | ©2019

- 48. 44 I-MICRONEWS MEDIA To meet the growing demand for market, technological and business information, i-Micronews Media integrates several tools able to reach each individual contact within its network. We will ensure your company benefits from this ONLINE ONSITE INPERSON i-Micronews e-newsletter i-Micronews.com FreeFullPDF.com Events Webcasts Unique, cost-effective ways to reach global audiences. Online display advertising campaigns are great strategies for improving your product/brand visibility.They are also an efficient way to adapt with the demands of the times and to evolve an effective marketing plan and strategy. Brand visibility, networking opportunities Today's technology makes it easy for us to communicate regularly, quickly, and inexpensively – but when understanding each other is critical, there is no substitute for meeting in-person. Events are the best way to exchange ideas with your customers, partners, prospects while increasing your brand/product visibility. Targeted audience involvement equals clear, concise perception of your company’s message. Webcasts are a smart, innovative way of communicating to a wider targeted audience.Webcasts create very useful, dynamic reference material for attendees and also for absentees, thanks to the recording technology. #15,800+ monthly unique visitors on i-Micronews.com #10,900+ weekly readers of i-Micronews e-newsletter #110 attendees on average #7+ key events planned for 2019 on different topics #380 registrants per webcast on average to gain new leads for your business Contact: CamilleVeyrier (veyrier@yole.fr), Marketing Communication Director About Yole Développement | www.yole.fr | ©2019

- 49. 45 CONTACT INFORMATION o CONSULTING AND SPECIFICANALYSIS, REPORT BUSINESS • North America: • Steve LaFerriere, Senior Sales Director forWestern US Canada Email: laferriere@yole.fr – + 1 310 600-8267 • ChrisYouman, Senior Sales Director for Eastern US Canada Email: chris.youman@yole.fr – +1 919 607 9839 • Japan Rest of Asia: • Takashi Onozawa, General Manager,Asia Business Development (India ROA) Email: onozawa@yole.fr - +81 34405-9204 • Miho Ohtake, Account Manager (Japan) Email: ohtake@yole.fr - +81 3 4405 9204 • Itsuyo Oshiba, Account Manager (Japan Singapore) Email: oshiba@yole.fr - +81-80-3577-3042 • Korea: Peter Ok, Business Development Director Email: peter.ok@yole.fr - +82 10 4089 0233 • Greater China: Mavis Wang, Director of Greater China Business Development Email: wang@yole.fr - +886 979 336 809 • Europe: Lizzie Levenez, EMEA Business Development Manager Email: levenez@yole.fr - +49 15 123 544 182 • RoW: Jean-Christophe Eloy, CEO President,Yole Développement Email eloy@yole.fr - +33 4 72 83 01 80 o FINANCIAL SERVICES (in partnership withWoodside Capital Partners) • Jean-Christophe Eloy, CEO President Email: eloy@yole.fr - +33 4 72 83 01 80 • Ivan Donaldson,VP of Financial Market Development Email: ivan.donaldson@yole.fr - +1 208 850 3914 o CUSTOM PROJECT SERVICES • Jérome Azémar,Technical Project Development Director Email: azemar@yole.fr - +33 6 27 68 69 33 o GENERAL • CamilleVeyrier, Director, Marketing Communication Email: veyrier@yole.fr - +33 472 83 01 01 • Sandrine Leroy, Director, Public Relations Email: leroy@yole.fr - +33 4 72 83 01 89 / +33 6 33 11 61 55 • Email: info@yole.fr - +33 4 72 83 01 80 Follow us on