The St. Louis office market summary document reports:

1) Job growth in St. Louis has accelerated and is now on par with national growth rates, with financial activities and professional services posting annual gains.

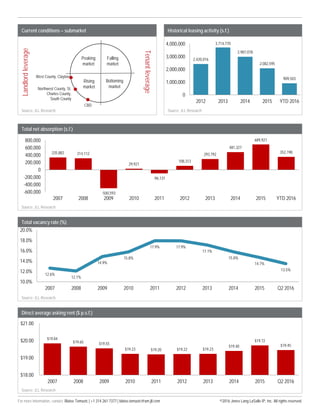

2) Vacancy rates have fallen below 14% for the first time since 2008 due to several large lease expansions. Class A suburban vacancy has hit single digits.

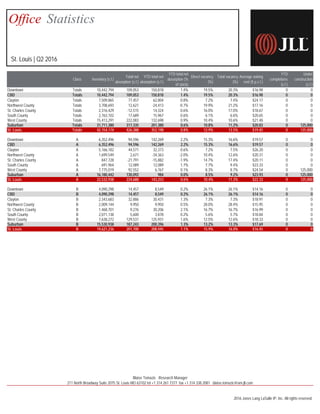

3) Large blocks of Class A office space remain scarce due to limited new construction supply, restricting options for tenants seeking over 50,000 square feet.