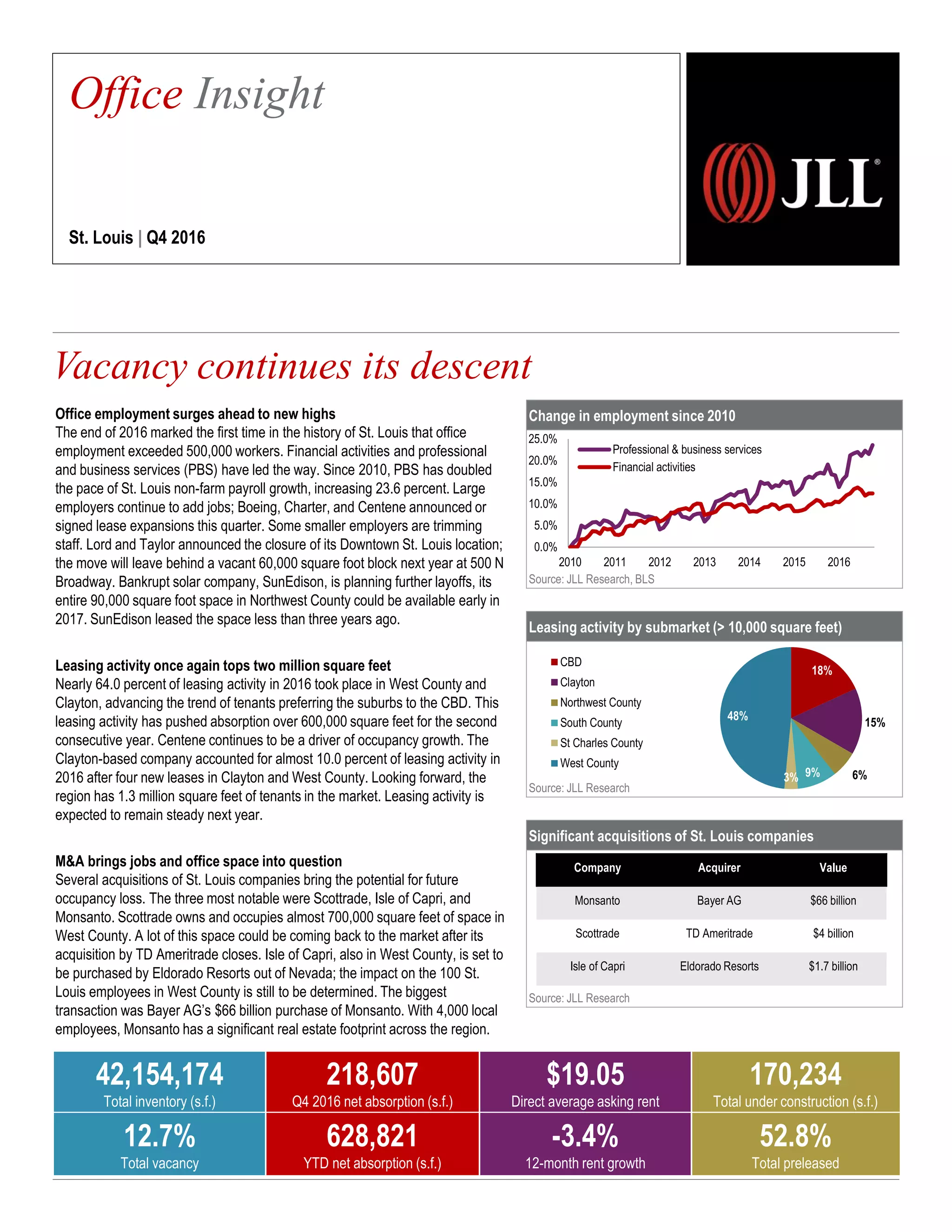

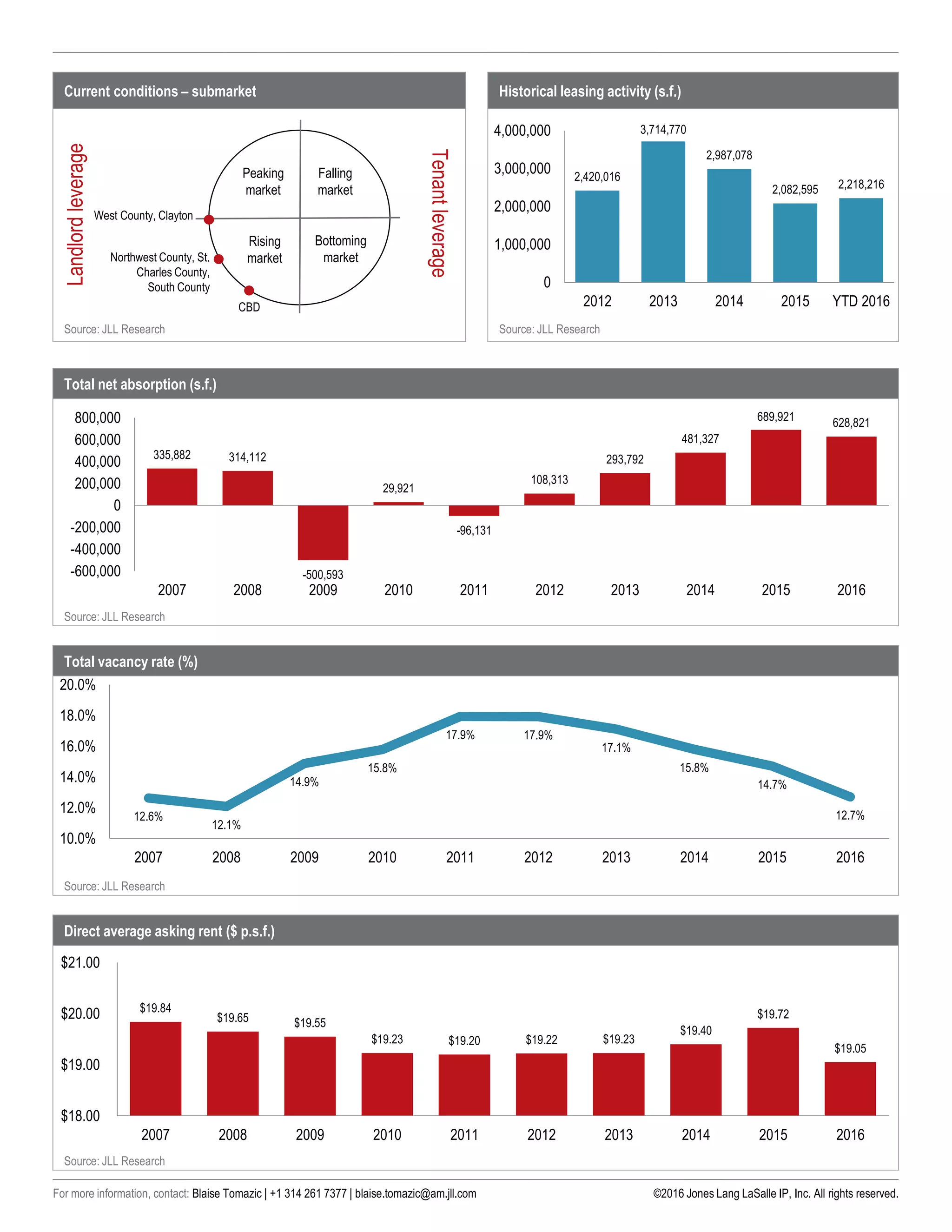

As of Q4 2016, St. Louis saw a surge in office employment, surpassing 500,000 workers for the first time, largely driven by financial activities and professional services. Despite a robust leasing activity of over two million square feet, acquisitions like Monsanto's by Bayer raise concerns about future vacancies. The overall market remains steady, with expectations for leasing activity to continue without significant fluctuations in 2017.