JLL Louisville Office Insight & Statistics - Q3 2016

•

1 like•73 views

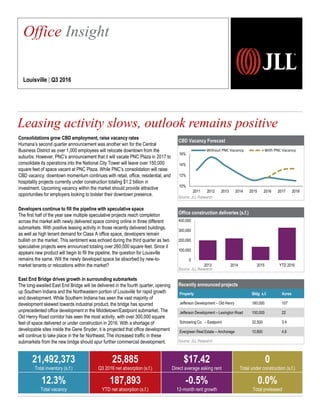

Year-to-date leasing activity surpassed the 2015 total in the third quarter, a positive sign for market. As the long-awaited East End Bridge nears completion, developers are looking to acquire land along the newly-opened access points as activity shifts to the northeast. In addition, four projects were announced in the third quarter total over 300,000 square feet of proposed speculative space as developers remain bullish on the market.

Recommended

Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Similar to JLL Louisville Office Insight & Statistics - Q3 2016

Similar to JLL Louisville Office Insight & Statistics - Q3 2016 (20)

More from Ross Bratcher

Recently uploaded

Recently uploaded (20)

JLL Louisville Office Insight & Statistics - Q3 2016

- 1. CBD Vacancy Forecast Source: JLL Research Office construction deliveries (s.f.) Source: JLL Research Recently announced projects Source: JLL Research Property Bldg s.f. Acres Jefferson Development – Old Henry 160,000 107 Jefferson Development – Lexington Road 100,000 22 Schroering Co. – Eastpoint 32,500 3.4 Evergreen Real Estate – Anchorage 10,800 4.6 Consolidations grow CBD employment, raise vacancy rates Humana’s second quarter announcement was another win for the Central Business District as over 1,000 employees will relocate downtown from the suburbs. However, PNC’s announcement that it will vacate PNC Plaza in 2017 to consolidate its operations into the National City Tower will leave over 150,000 square feet of space vacant at PNC Plaza. While PNC’s consolidation will raise CBD vacancy, downtown momentum continues with retail, office, residential, and hospitality projects currently under construction totaling $1.2 billion in investment. Upcoming vacancy within the market should provide attractive opportunities for employers looking to bolster their downtown presence. Developers continue to fill the pipeline with speculative space The first half of the year saw multiple speculative projects reach completion across the market with newly delivered space coming online in three different submarkets. With positive leasing activity in those recently delivered buildings, as well as high tenant demand for Class A office space, developers remain bullish on the market. This sentiment was echoed during the third quarter as two speculative projects were announced totaling over 260,000 square feet. Since it appears new product will begin to fill the pipeline, the question for Louisville remains the same. Will the newly developed space be absorbed by new-to- market tenants or relocations within the market? East End Bridge drives growth in surrounding submarkets The long-awaited East End Bridge will be delivered in the fourth quarter, opening up Southern Indiana and the Northeastern portion of Louisville for rapid growth and development. While Southern Indiana has seen the vast majority of development skewed towards industrial product, the bridge has spurred unprecedented office development in the Middletown/Eastpoint submarket. The Old Henry Road corridor has seen the most activity, with over 300,000 square feet of space delivered or under construction in 2016. With a shortage of developable sites inside the Gene Snyder, it is projected that office development will continue to take place in the far Northeast. The increased traffic in these submarkets from the new bridge should spur further commercial development. Leasing activity slows, outlook remains positive 2,257 Office Insight Louisville | Q3 2016 21,492,373 Total inventory (s.f.) 25,885 Q3 2016 net absorption (s.f.) $17.42 Direct average asking rent 0 Total under construction (s.f.) 12.3% Total vacancy 187,893 YTD net absorption (s.f.) -0.5% 12-month rent growth 0.0% Total preleased 0 100,000 200,000 300,000 400,000 2013 2014 2015 YTD 2016 10% 12% 14% 16% 2011 2012 2013 2014 2015 2016 2017 2018 Without PNC Vacancy With PNC Vacancy

- 2. Current conditions – submarket Historical leasing activity (s.f.) Source: JLL Research Source: JLL Research Total net absorption (s.f.) Source: JLL Research Total vacancy rate (%) Source: JLL Research Direct average asking rent ($ p.s.f.) Source: JLL Research 517,690 -148,020 -77,885 86,194 462,281 313,754 426,281 204,612 304,088 187,893 -200,000 0 200,000 400,000 600,000 2007 2008 2009 2010 2011 2012 2013 2014 2015 YTD 2016 $16.59 $16.60 $16.93 $17.24 $16.97 $16.31 $17.11 $17.23 $17.50 $17.42 $15.50 $16.00 $16.50 $17.00 $17.50 $18.00 2007 2008 2009 2010 2011 2012 2013 2014 2015 YTD 2016 11.0% 12.5% 14.2% 15.9% 15.3% 14.8% 13.6% 13.1% 12.8% 12.3% 5.0% 7.0% 9.0% 11.0% 13.0% 15.0% 17.0% 2007 2008 2009 2010 2011 2012 2013 2014 2015 YTD 2016 959,766 1,067,415 938,552 738,564 850,124 0 200,000 400,000 600,000 800,000 1,000,000 1,200,000 2012 2013 2014 2015 YTD 2016 ©2016 Jones Lang LaSalle IP, Inc. All rights reserved.For more information, contact: Ross Bratcher | ross.bratcher@am.jll.com Landlordleverage Tenantleverage Peaking market Falling market Bottoming market Rising market Plainview/Middletown CBD South Central Hurstbourne/Lyndon St. Matthews Westport Road/Brownsboro Rd

- 3. 2,257 Office Statistics Louisville | Q3 2016 Class Inventory (s.f.) Total net absorption (s.f.) YTD total net absorption (s.f.) YTD total net absorption (% ofstock) Directvacancy (%) Total vacancy (%) Average direct asking rent($ p.s.f.) YTD completions (s.f.) Under construction (s.f.) CBD Totals 10,293,175 67,357 -1,090 0.0% 11.3% 11.6% $16.46 0 0 Urban Totals 10,293,175 67,357 -1,090 0.0% 11.3% 11.6% $16.46 0 0 Hurstbourne/Lyndon Totals 4,808,195 -13,471 55,875 1.2% 13.1% 13.3% $21.69 245,000 0 Plainview/Middletown Totals 2,888,204 -3,945 77,715 2.7% 13.4% 13.4% $15.74 38,400 0 South Central Totals 1,493,851 -56,357 -26,864 -1.8% 12.5% 16.7% $13.24 0 0 St. Matthews Totals 1,079,692 5,021 33,897 3.1% 8.7% 8.7% $17.61 45,000 0 WestportRoad/Brownsboro Rd Totals 929,256 27,280 48,360 5.2% 8.8% 9.1% $21.62 0 0 Suburbs Totals 11,199,198 -41,472 188,983 1.7% 12.3% 13.0% $18.19 328,400 0 Louisville Totals 21,492,373 25,885 187,893 0.9% 11.8% 12.3% $17.42 328,400 0 CBD A 4,295,069 13,858 13,233 0.3% 11.2% 11.8% $19.34 0 0 Urban A 4,295,069 13,858 13,233 0.3% 11.2% 11.8% $19.34 0 0 Hurstbourne/Lyndon A 3,835,708 -11,432 61,420 1.6% 13.6% 13.8% $22.48 245,000 0 Plainview/Middletown A 1,027,506 0 54,763 5.3% 6.2% 6.2% $18.47 38,400 0 St. Matthews A 459,453 -4,601 33,723 7.3% 7.8% 7.8% $21.25 45,000 0 WestportRoad/Brownsboro Rd A 783,477 27,280 52,571 6.7% 9.2% 9.6% $22.40 0 0 Suburbs A 6,106,144 11,247 202,477 3.3% 11.3% 11.5% $22.04 328,400 0 Louisville A 10,401,213 25,105 215,710 2.1% 11.3% 11.6% $20.93 328,400 0 CBD B 5,998,106 53,499 -14,323 -0.2% 11.3% 11.4% $14.50 0 0 Urban B 5,998,106 53,499 -14,323 -0.2% 11.3% 11.4% $14.50 0 0 Hurstbourne/Lyndon B 972,487 -2,039 -5,545 -0.6% 11.4% 11.4% $16.68 0 0 Plainview/Middletown B 1,860,698 -3,945 22,952 1.2% 17.4% 17.4% $15.35 0 0 South Central B 1,493,851 -56,357 -26,864 -1.8% 12.5% 16.7% $13.24 0 0 St. Matthews B 620,239 9,622 174 0.0% 9.3% 9.3% $15.36 0 0 WestportRoad/Brownsboro Rd B 145,779 0 -4,211 -2.9% 6.8% 6.8% $16.00 0 0 Suburbs B 5,093,054 -52,719 -13,494 -0.3% 13.5% 14.7% $14.93 0 0 Louisville B 11,091,160 780 -27,817 -0.3% 12.3% 12.9% $14.73 0 0 ©2016 Jones Lang LaSalle IP, Inc. All rights reserved.For more information, contact: Ross Bratcher | ross.bratcher@am.jll.com