Download as PDF, PPTX

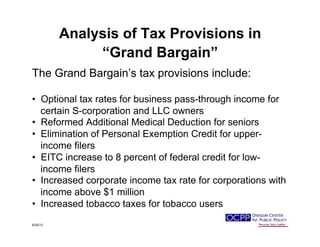

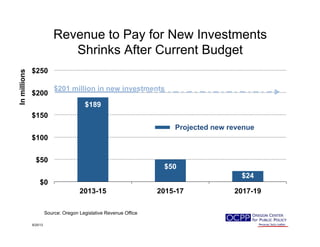

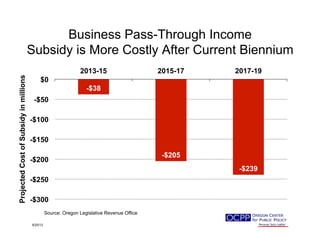

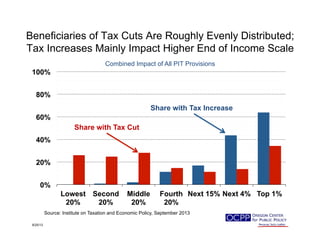

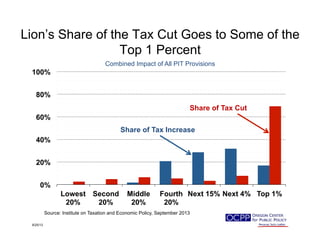

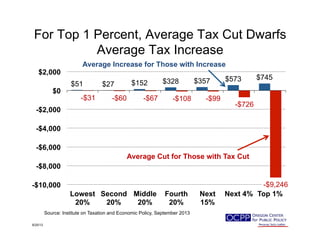

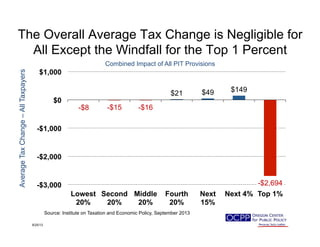

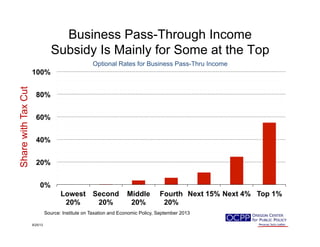

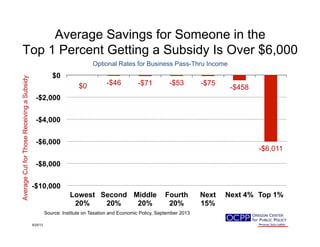

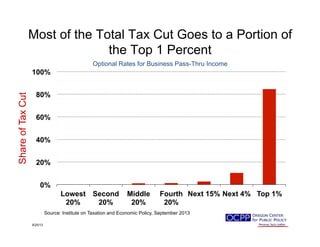

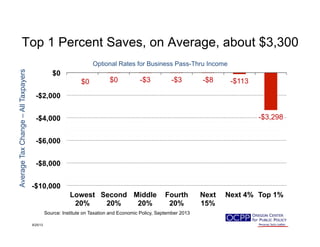

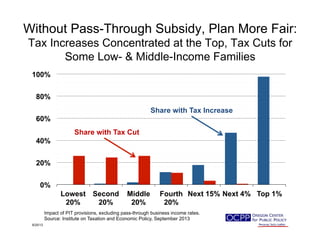

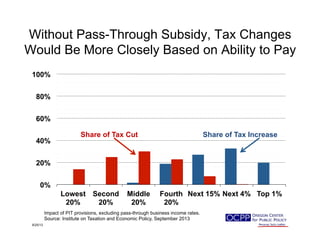

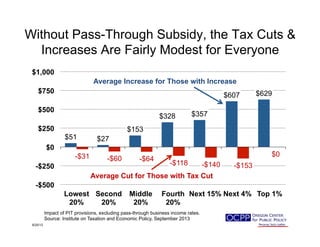

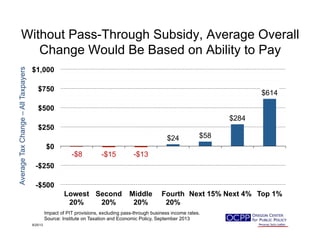

The document evaluates the tax provisions of the 'grand bargain' in Oregon, which includes various changes primarily benefiting upper-income individuals, particularly through a business pass-through income tax subsidy. It concludes that the current tax package will be insufficient to finance proposed investments in education and health services, particularly due to increasing costs associated with the subsidy. Eliminating the subsidy would enable more equitable tax changes and retain necessary revenue for public services.