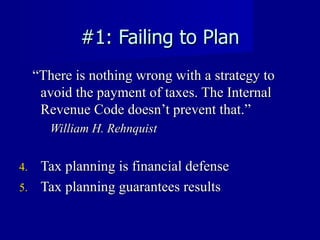

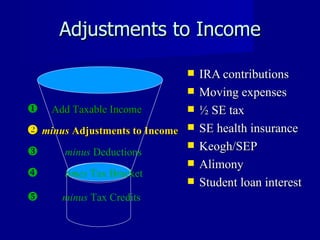

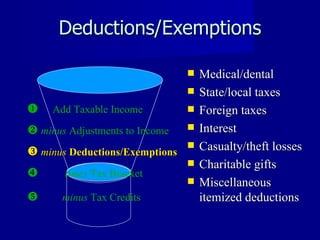

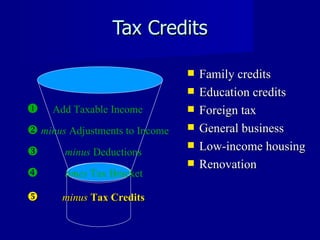

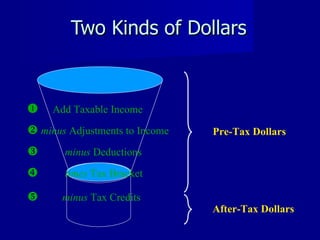

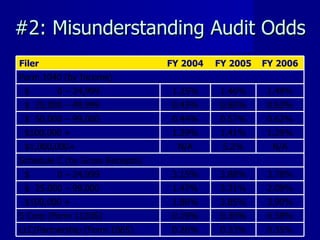

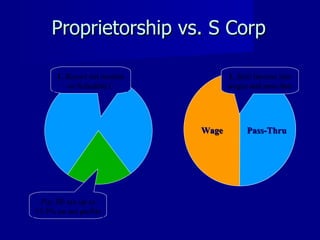

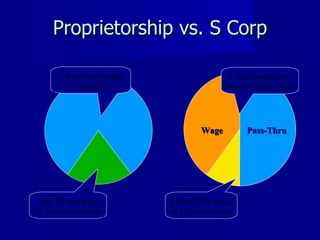

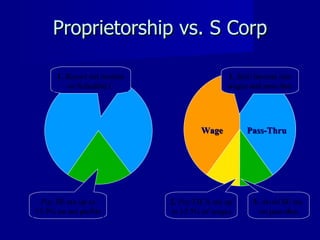

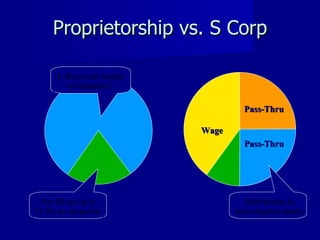

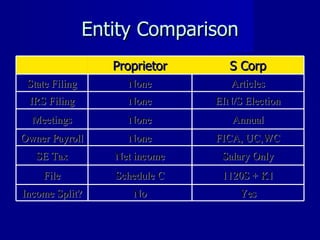

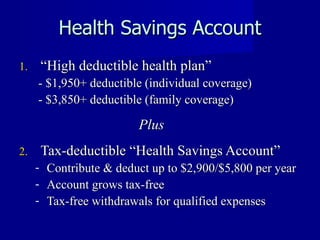

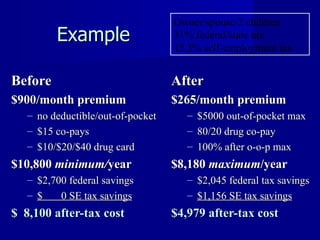

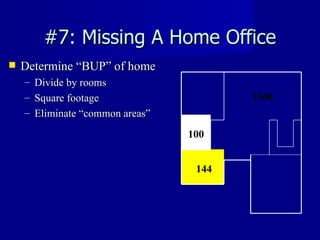

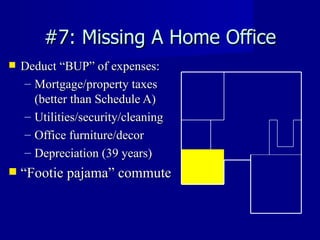

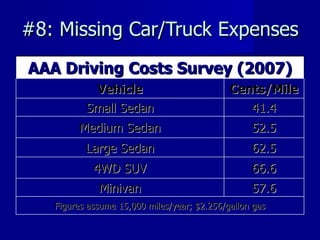

The document discusses the top 10 most expensive tax mistakes that business owners can make, including failing to do tax planning, misunderstanding audit odds, paying too much self-employment tax, choosing the wrong retirement plan, missing opportunities for family employment and medical benefits, not claiming a home office deduction, missing car and truck expense deductions, not deducting meals and entertainment expenses, and not using tax coaching services. It provides details on how to avoid these costly mistakes.