Simple Average Method- Problem.pptx

•Download as PPTX, PDF•

0 likes•89 views

Simple Average Method - Goodwill Calculation

Recommended

More Related Content

Similar to Simple Average Method- Problem.pptx

Similar to Simple Average Method- Problem.pptx (15)

More from Kumarasamy Dr.PK

More from Kumarasamy Dr.PK (20)

Recently uploaded

Recently uploaded (20)

Simple Average Method- Problem.pptx

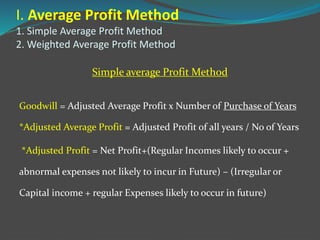

- 1. I. Average Profit Method 1. Simple Average Profit Method 2. Weighted Average Profit Method Simple average Profit Method Goodwill = Adjusted Average Profit x Number of Purchase of Years *Adjusted Average Profit = Adjusted Profit of all years / No of Years *Adjusted Profit = Net Profit+(Regular Incomes likely to occur + abnormal expenses not likely to incur in Future) – (Irregular or Capital income + regular Expenses likely to occur in future)

- 2. Profit Given xxxxxxx Add : Expenses and Losses not likely to occur in future xxxxxxx (Abnormal or irregular, loss, salary Capital exp etc) Add : All profit likely to come in future xxxxxxx ---------- xxxxxxxx Less : All Expenses and losses Expected to occur in future (salary, insurance, Depreciation, Cost to Management etc) xxxxxxx Less: Profit not likely to recur in future xxxxxxx -------------------- Adjusted profit of the year xxxxxxx Finding of Adjusted Profit

- 3. Problem No 1: G & Co. decided to purchase a business. Its profits for the last 4 years were Year 1998 – Rs.40,000, Year 1999- Rs.50,000, Year 2000 – Rs.48,000, Year 2001 – Rs.46,000 The business was looked after by the management. Remuneration from alternative employment if not engaged in the business comes to Rs.6,000p.a. Find out the amount of goodwill, if it is valued on the basis of 3 years purchase at the average net profit for the last 4 years. Avg Profit : Rs.40,000, Goodwill. Rs 1,20,000)

- 4. Step 1 : Calculation of Adjusted Profit Particulars 1998 1999 2001 2001 Profit of the year 40,000 50,000 48,000 46,000 Less : Remuneration to Management 6,000 6,000 6,000 6,000 ------------------------------------------------ Adjusted Profits 34,000 44,000 42,000 40,000 ------------------------------------------------- Step 2 : Adjusted Average Profit = Total Profits of all years / No of years = (34,000+44,000+42,000+40,000) / 4 years = 1,60,000 / 4 = 40,000 Step 3 : Calculation of Goodwill =Adjusted Average Profit x No of years of purchase = 40,000 x 3 years = 1,20,000

- 5. Problem No: 1. Mr. Amar has been doing business, intends to sell his business on 1-12-2006. From the following particulars ascertain the amount of goodwill based on 3 years purchase of average profits of last 4 years. The profits during 4 years were as follows: a) 2003-Rs.2,00,000 ; b) 2004—Rs. 1,40,000 ; c) 2005- Rs.3,00,000 d) 2006- Rs.3,60,000 Additional Information 1.At the time of acquisition of business, the buyer was employed as a manager of business on a salary of Rs.6,000 per month. 2.The profits of 2006 include income from investment of Rs.20,000. 3.The profits of 2003 were reduced by Rs.60,000 being loss on speculation. 4.Similarly, in 2005 profits were reduced by Rs.1,00,000 due to loss from betting. Ans: Adj. Avg. Profit : Rs. 2,38,000 (188000+168000+328000+268000/4) , Goodwill : Rs 7,14,000

- 6. Step 1 : Calculation of Adjusted Profit Step 2 : Calculation of Adjusted Average Profit = (1,88,000 + 1,68,000 + 3,28,000 + 2,68,000) / 4 years = 9,52,000 / 4 = 2,38,000 Step 3 : Calculation of Goodwill = Average Profit x No of years of Purchase = 2,38,000 x 3 = 7,14,000 Particulars 2003 2004 2005 2006 Profit (given) 2,00,000 2,40,000 3,00,000 3,60,000 Add: Speculation Loss 60,000 - - - Add: Loss from Betting - - 1,00,000 - Total 2,60,000 2,40,000 4,00,000 3,60,000 Less: Managerial Salary 72,000 72,000 72,000 72,000 Less : Income on Investment - - - 20,000 Adjusted Profit 1,88,000 1,68,000 3,28,000 2,68,000

- 7. Problem 5- (Weighted Average Profit Method) Particulars 2001 2002 2003 2004 Profit Given 40,500 47,500 60,000 75,000 Expenses will not inccur in future (Furniture – capital exp) - - 10,000 - Less : Expenses occur in future -Depreciation - - 500 950 Administration Expenses 5000 5000 5000 5000 Less: over valuation opening Stock - 2500 Add: Over Valuation of Closing Stock - 2500 35500 45000 62000 69050

- 8. Step 2 - Calculation of Weighted Profit 35,500 X 1 35,500 45,000 x X 2.5 11,250 62,000 x X 3.8 2,35,600 69,050 x X 4.2 2,90,010 -------------- Total Weighted Profit 6,73,110 -------------- Step 3 - Weighted Average Profit Total Profit of All Year / Total Weightage = 6,73,110 / 11.5 =58,531 Step 4 – Calculation of Goodwill Goodwill = Weighted Average Profit x No. of Years of Purchase = 58,531 X 3 Years = 1,75,593

- 9. Note ; 1. Cost of Furniture is Incurred for business. But it is not revenue expenditure in nature. So Deducted one should be added again. 2. Depreciation – it should be calculated to the year concerned and next year that immediately following. Period of the furniture usage : From July to December=6 months ; = 10,000 x 10/100 x 6/12 = 500 3. In the following year (2004) = 9500 x 10/100 = 950 4. Adjustment of Stock (Material Consumed) = ( opening St + Purchase - Cl.Stock ) Take Reverse Action