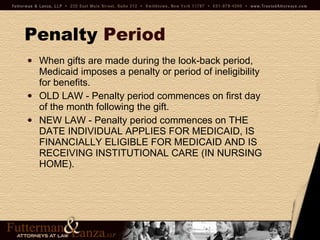

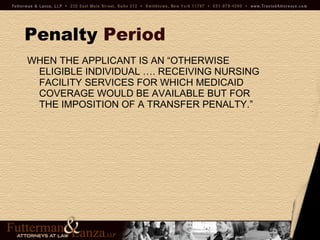

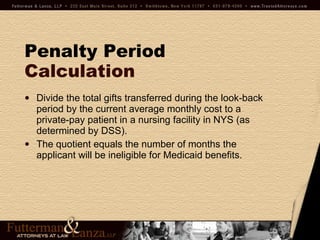

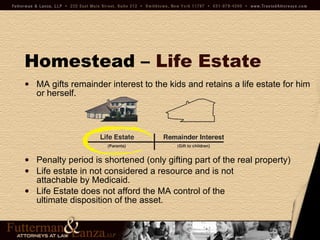

This document discusses Medicaid eligibility rules and planning for long-term care costs. It notes that long-term care can be expensive, with nursing home care costing $9,000-$17,000 per month on Long Island. Medicaid is a means-tested program that can help cover long-term care costs. The document outlines Medicaid eligibility requirements around income, resources, transfers of assets, and penalty periods for gifts made during the 60-month lookback period. Protecting the homestead through sale, transfer, life estate, or trust is also discussed.