Download to read offline

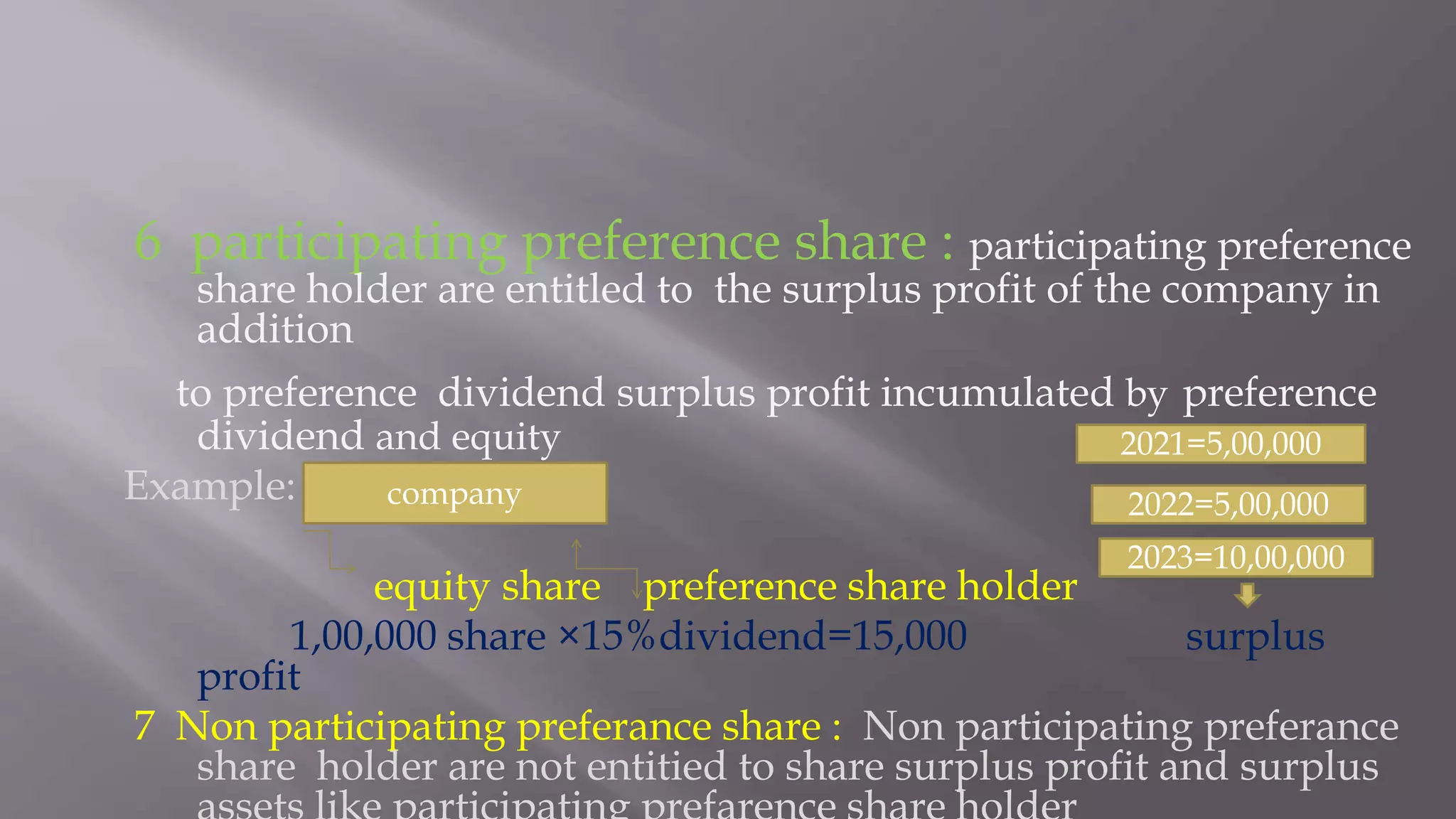

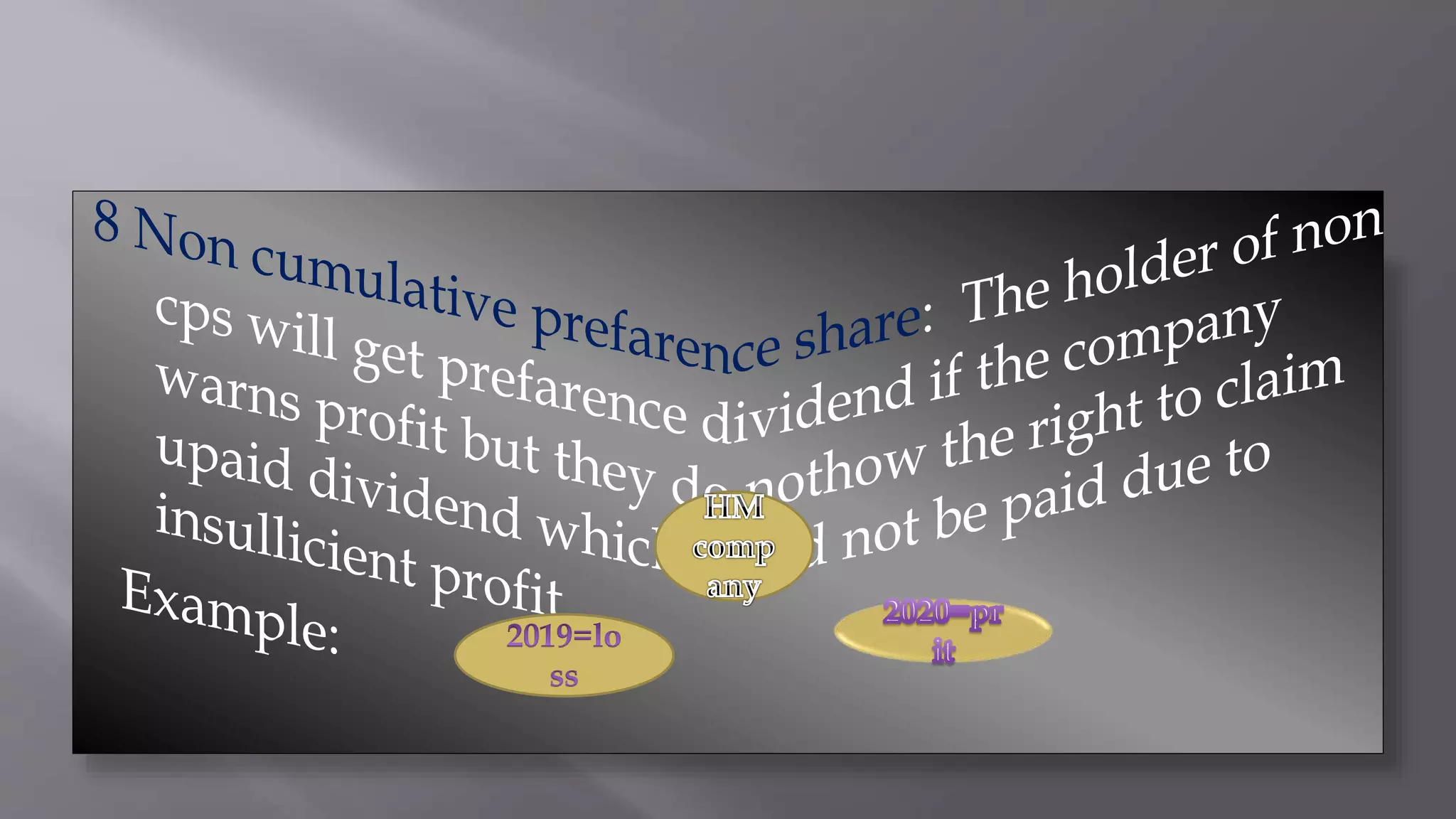

The document compares equity shares and preference shares, highlighting that equity shares do not have preferential rights while preference shares do, specifically concerning dividend payments and capital returns during winding up. It categorizes preference shares into types such as redeemable, irredeemable, convertible, non-convertible, participating, and non-participating, each with distinct characteristics. It provides an example of participating and non-participating preference shares regarding entitlement to surplus profits from the company.