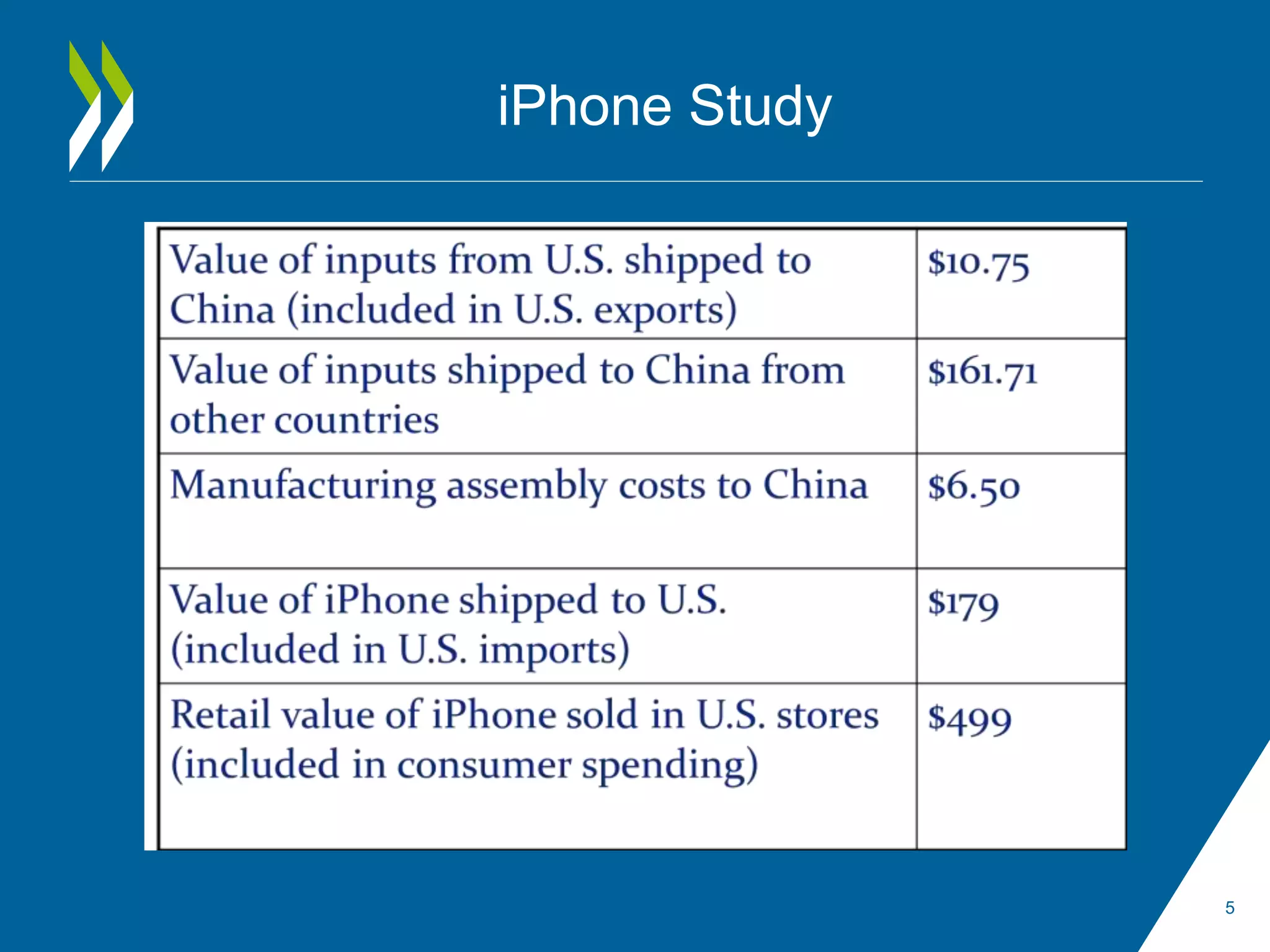

This document summarizes the findings of the UNECE Task Force on Global Production regarding the challenges of measuring global production in national accounts and balance of payments statistics. The Task Force developed a Guide to Measuring Global Production that provides a conceptual framework and typology for classifying different global production arrangements. It also provides guidance on practical issues like overcoming data gaps and accounting for large, complex multinational enterprises. The fragmentation of value chains across borders is increasingly challenging for statisticians, and global production will continue to require significant resources to adequately measure.

![Session 7 b commentson daneilkerpaperonukr&d servicelives2014iariw[1]](https://cdn.slidesharecdn.com/ss_thumbnails/pwfpecwntsmdld64j1xg-signature-6de5ee34a7e0a8be608105cfc95b1f55459403214875a488c94e063931d3b0c1-poli-140830080216-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)