Download as PDF, PPTX

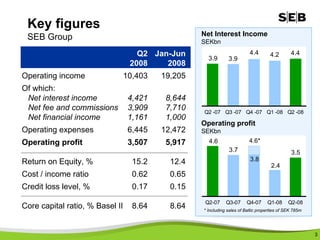

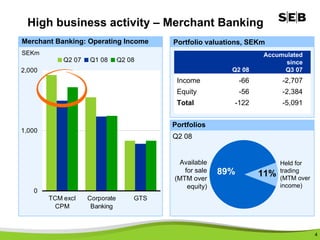

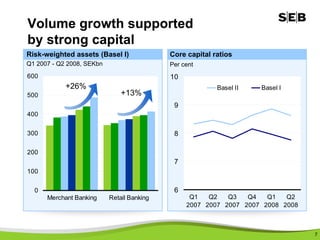

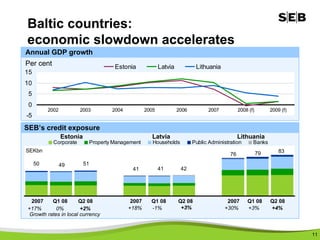

1) SEB reported strong second quarter results with income regaining strength and operating profit reaching its second highest level ever, though costs were higher due to continued investments and business activity was impacted by losses in the Baltic region. 2) Business activity was generally strong across most areas including merchant banking, asset management, and retail banking in Sweden, though the Baltic countries saw economic slowdowns and increased credit losses in Estonia. 3) SEB remains well capitalized and has sufficient liquidity, but expects costs to continue growing around 4% in 2008 due to ongoing investments while maintaining a cost savings program targeting 1.5-2 billion kronor by 2009.