Slides

Prepared

by:

Dr.

Mahtab

Alam

UNIT

-II

Unit Sub Unit

UnitII

Sales

Planning and

Budgeting

Sales Planning and Budgeting: Sales Planning

Process, Developing Sales Forecast, Types of

Sales Forecasts. Sales Forecasting Methods,

Sales Budget, Purpose of Sales Budget,

Methods used for Deciding Sales Expenditure

Budget, Sales Budgeting Process.

Slides

Prepared

by:

Dr.

Mahtab

Alam Sales Planning-Definition

PhilipKotler: "Sales planning is the structured

development of sales strategies and operational

plans that align with the company's marketing

objectives, ensuring effective customer targeting and

resource utilization.”

William J. Stanton: "Sales planning involves

analyzing the market, setting achievable sales targets,

and preparing the necessary steps to direct and

control the sales efforts of an organization."

5.

Slides

Prepared

by:

Dr.

Mahtab

Alam

Goal-Oriented Process.

Customer Centric Approach.

Aligned withVision, Mission, Goals & Objectives.

Alignment with Marketing Goals

Required Market Analysis

Used for Sales Forecasting

Used for Resource Allocation

Sales Strategies decision

Sales Budgeting decision

Sales Territories decision

Sales Target Allocation

Sales Performance monitoring & controlling

Features of Sales Planning

6.

Slides

Prepared

by:

Dr.

Mahtab

Alam

Set ClearSales Targets

Align with Organizational Goals

Optimize Resource Allocation

Improve Sales Forecasting

Enhance Market Understanding

Increase Revenue and Profitability

Strengthen Customer Relationships

Facilitate Coordination

Adapt to Market Changes

Track and Monitor Performance

Objectives of Sales Planning

7.

Slides

Prepared

by:

Dr.

Mahtab

Alam

Advantages

ReducesUncertainty

Focus on Objectives/Goals

Economical Operation

Facilitates Control

Encourages Innovation and Creativity

Improves Motivation

Avoids Random Activity

Improves Competitive Strength

Focuses attention on objectives and

results

Establishes a basis for teamwork

Helps anticipate problems and cope with

change

Better coordination

Advantages & Disadvantages of Sales Planning

Disadvantages

Lack of Reliable Data

Rigidity

Time Consuming Process

Costly Process

Rapid Change

Resistance to Change

Slides

Prepared

by:

Dr.

Mahtab

Alam Sales ForecastingMeaning

Sales forecasting is the process of predicting future sales based

on historical data, market trends, and other influencing factors.

A sales forecast is an estimation of sales volume that a company can

expect to attain within the specified future period.

Businesses use sales forecasts to make informed decisions about

production, inventory management, budgeting, and resource

allocation etc.

12.

Slides

Prepared

by:

Dr.

Mahtab

Alam

•Philip Kotler –"Sales forecasting is the art of anticipating what buyers

are likely to do under a given set of conditions.“

•William J. Stanton – "Sales forecasting is an estimate of sales, in

monetary or physical units, for a specified future period under a proposed

marketing plan or program and under an assumed set of economic and

other forces outside the unit for which the forecast is made.“

•Cundiff and Still – "Sales forecast is an estimate of sales during a

specified future period which is based on one or more specified

assumptions.“

•American Marketing Association (AMA) – "Sales forecasting is the

process of estimating future sales. Accurate sales forecasts enable

companies to make informed business decisions and predict short-term

and long-term performance."

Sales Forecasting-Definition

Slides

Prepared

by:

Dr.

Mahtab

Alam

3. Based onApproach

Top Down Sales Forecast

The forecast starts with the overall

company goal or industry growth

rate and then breaks it down into smaller

segments (regions, products, or

departments).

Example: A tech company predicts

global sales growth and then allocates

targets to various departments (like

product development and marketing).

Bottom Up Sales Forecast

The forecast begins with the individual

sales teams or departments, where each

part predicts its own sales and the total is

then aggregated.

Example: A chain of restaurants gets

input from individual locations, each

predicting its monthly sales, and the totals

are then added up to forecast the overall

sales.

3. Based on Purpose

Demand Forecast

To estimate future demand for products

or services, and help in planning

production, inventory, staffing, and marketing

efforts.

Example: A clothing brand forecasts its

sales for the next quarter by analyzing

past sales trends, current season, and

consumer demand.

Budget Forecast

A Budget Forecast is an estimate of

future income and expenses over a

specific period. It helps businesses plan their

financial resources and allocate budgets

across departments, projects, or activities.

Example: A tech company forecasts its

budget for the year by estimating income

from product sales and then calculating

anticipated expenses like R&D, marketing,

and staffing costs

Slides

Prepared

by:

Dr.

Mahtab

Alam

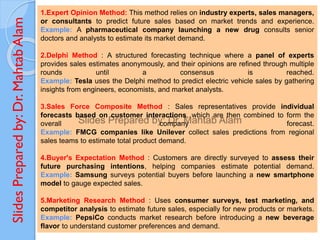

1.Expert Opinion Method:This method relies on industry experts, sales managers,

or consultants to predict future sales based on market trends and experience.

Example: A pharmaceutical company launching a new drug consults senior

doctors and analysts to estimate its market demand.

2.Delphi Method : A structured forecasting technique where a panel of experts

provides sales estimates anonymously, and their opinions are refined through multiple

rounds until a consensus is reached.

Example: Tesla uses the Delphi method to predict electric vehicle sales by gathering

insights from engineers, economists, and market analysts.

3.Sales Force Composite Method : Sales representatives provide individual

forecasts based on customer interactions, which are then combined to form the

overall company forecast.

Example: FMCG companies like Unilever collect sales predictions from regional

sales teams to estimate total product demand.

4.Buyer's Expectation Method : Customers are directly surveyed to assess their

future purchasing intentions, helping companies estimate potential demand.

Example: Samsung surveys potential buyers before launching a new smartphone

model to gauge expected sales.

5.Marketing Research Method : Uses consumer surveys, test marketing, and

competitor analysis to estimate future sales, especially for new products or markets.

Example: PepsiCo conducts market research before introducing a new beverage

flavor to understand customer preferences and demand.

22.

Slides

Prepared

by:

Dr.

Mahtab

Alam Quantitative Methodsof Sales Forecasting

1. Moving Average Method: This method predicts future sales by

calculating the average of past sales over a specific period, helping to

smooth out short-term fluctuations.

Example: Maruti Suzuki uses the moving average method to forecast

monthly car demand by averaging sales data from the last six months.

23.

Slides

Prepared

by:

Dr.

Mahtab

Alam

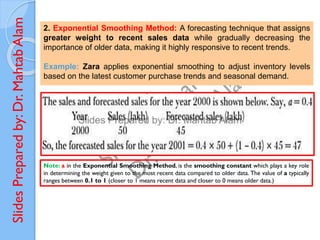

2. Exponential SmoothingMethod: A forecasting technique that assigns

greater weight to recent sales data while gradually decreasing the

importance of older data, making it highly responsive to recent trends.

Example: Zara applies exponential smoothing to adjust inventory levels

based on the latest customer purchase trends and seasonal demand.

Note: a in the Exponential Smoothing Method, is the smoothing constant which plays a key role

in determining the weight given to the most recent data compared to older data. The value of a typically

ranges between 0.1 to 1 (closer to 1 means recent data and closer to 0 means older data.)

24.

Slides

Prepared

by:

Dr.

Mahtab

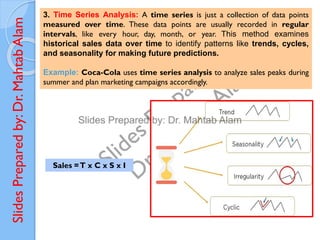

Alam 3. TimeSeries Analysis: A time series is just a collection of data points

measured over time. These data points are usually recorded in regular

intervals, like every hour, day, month, or year. This method examines

historical sales data over time to identify patterns like trends, cycles,

and seasonality for making future predictions.

Example: Coca-Cola uses time series analysis to analyze sales peaks during

summer and plan marketing campaigns accordingly.

Sales =T x C x S x I

25.

Slides

Prepared

by:

Dr.

Mahtab

Alam

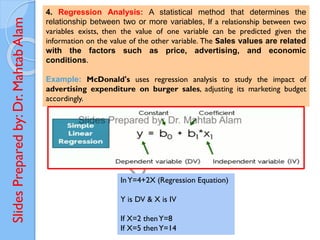

4. Regression Analysis:A statistical method that determines the

relationship between two or more variables, If a relationship between two

variables exists, then the value of one variable can be predicted given the

information on the value of the other variable. The Sales values are related

with the factors such as price, advertising, and economic

conditions.

Example: McDonald's uses regression analysis to study the impact of

advertising expenditure on burger sales, adjusting its marketing budget

accordingly.

InY=4+2X (Regression Equation)

Y is DV & X is IV

If X=2 thenY=8

If X=5 thenY=14

26.

Slides

Prepared

by:

Dr.

Mahtab

Alam

5. Econometric Analysis:A complex statistical method that considers

multiple economic variables (like GDP, inflation, consumer income) to

forecast sales based on broader economic trends.

Example: Airbus uses econometric analysis to predict future aircraft

demand based on GDP growth, fuel prices, and airline profitability trends.

Y=a+b1X1+b2X2+...+bnXn

where:

•Y = Sales Forecasting

•X1,X2,...,XnX_1, X_2, ..., X_nX1,X2,...,Xn = Economic factors (e.g., GDP,

inflation, employment)

•b1,b2,...,bnb_1, b_2, ..., b_nb1,b2,...,bn = Coefficients measuring impact

27.

Slides

Prepared

by:

Dr.

Mahtab

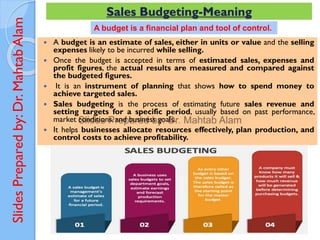

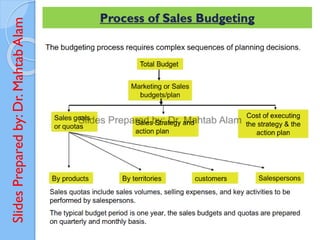

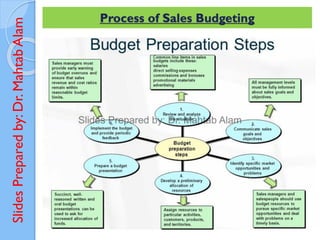

Alam Sales Budgeting-Meaning

A budget is an estimate of sales, either in units or value and the selling

expenses likely to be incurred while selling.

Once the budget is accepted in terms of estimated sales, expenses and

profit figures, the actual results are measured and compared against

the budgeted figures.

It is an instrument of planning that shows how to spend money to

achieve targeted sales.

Sales budgeting is the process of estimating future sales revenue and

setting targets for a specific period, usually based on past performance,

market conditions, and business goals.

It helps businesses allocate resources effectively, plan production, and

control costs to achieve profitability.

A budget is a financial plan and tool of control.

28.

Slides

Prepared

by:

Dr.

Mahtab

Alam Sales Budgeting-Definition

•Cundiffand Still: "A sales budget is a forecast of expected sales during

a future period, expressed in monetary or quantitative terms.“

•Ronald Hilton: "A sales budget is a detailed schedule showing the

expected sales for the budget period, typically expressed in both units

and dollars.“

•Wheldon: "A sales budget is an estimate of expected total sales

revenue and selling expenses of the firm for a future period.“

•Terry Lucey: "Sales budgeting is the process of predicting and

controlling sales revenue, considering external factors like market

demand and internal capabilities."

29.

Slides

Prepared

by:

Dr.

Mahtab

Alam Sales Budgeting-Features

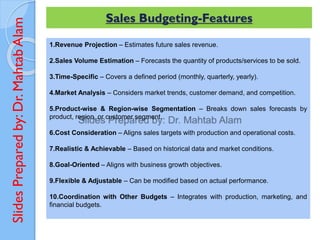

1.RevenueProjection – Estimates future sales revenue.

2.Sales Volume Estimation – Forecasts the quantity of products/services to be sold.

3.Time-Specific – Covers a defined period (monthly, quarterly, yearly).

4.Market Analysis – Considers market trends, customer demand, and competition.

5.Product-wise & Region-wise Segmentation – Breaks down sales forecasts by

product, region, or customer segment.

6.Cost Consideration – Aligns sales targets with production and operational costs.

7.Realistic & Achievable – Based on historical data and market conditions.

8.Goal-Oriented – Aligns with business growth objectives.

9.Flexible & Adjustable – Can be modified based on actual performance.

10.Coordination with Other Budgets – Integrates with production, marketing, and

financial budgets.

Slides

Prepared

by:

Dr.

Mahtab

Alam Purpose ofSales Budgeting

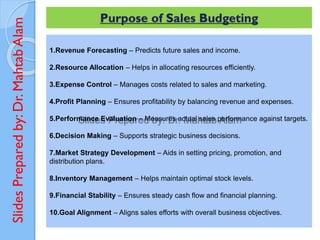

1.Revenue Forecasting – Predicts future sales and income.

2.Resource Allocation – Helps in allocating resources efficiently.

3.Expense Control – Manages costs related to sales and marketing.

4.Profit Planning – Ensures profitability by balancing revenue and expenses.

5.Performance Evaluation – Measures actual sales performance against targets.

6.Decision Making – Supports strategic business decisions.

7.Market Strategy Development – Aids in setting pricing, promotion, and

distribution plans.

8.Inventory Management – Helps maintain optimal stock levels.

9.Financial Stability – Ensures steady cash flow and financial planning.

10.Goal Alignment – Aligns sales efforts with overall business objectives.

32.

Slides

Prepared

by:

Dr.

Mahtab

Alam Challenges ofSales Budgeting

1. Uncertain Market Conditions: Economic downturns, inflation, or political instability

,Changing customer preferences and demand fluctuations can impact sales projections.

2. Inaccurate Sales Forecasting: Overestimating sales can lead to excess inventory and

increased costs. Underestimating sales may cause stock shortages and lost revenue.

3. Lack of Reliable Data: Incomplete or outdated historical sales data can lead to incorrect

estimates. Poor data collection and analysis reduce the accuracy of projections.

4. Competition and Market Dynamics: Competitor actions, such as pricing changes or

product launches, can impact sales. New entrants or disruptive technologies can reduce

market share.

5. Internal Operational Constraints: Limited production capacity can restrict sales

growth. Inadequate distribution channels or workforce shortages can hinder targets.

6. Pricing and Discount Challenges: Unstable pricing strategies due to fluctuating raw

material costs affect sales forecasts. High discounting or promotional offers can create

unrealistic revenue expectations.

7. Seasonality and Demand Variability: Some industries experience high sales in specific

seasons and slowdowns in others. Failure to account for seasonal trends can lead to misleading

budgets.

8. Coordination Between Departments: Sales, finance, and operations teams may have

conflicting priorities. Poor communication leads to misalignment in budgeting and goal setting.

9. Regulatory andTaxation Changes: Sudden changes in government policies, taxation, or

import/export laws can impact sales. Compliance with new regulations may increase costs and

affect profitability.

10. External Economic Factors: Exchange rate fluctuations can affect international sales.

Interest rate changes can impact consumer spending and business investments.

Slides

Prepared

by:

Dr.

Mahtab

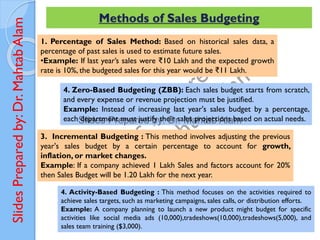

Alam Methods ofSales Budgeting

1. Percentage of Sales Method: Based on historical sales data, a

percentage of past sales is used to estimate future sales.

•Example: If last year’s sales were ₹10 Lakh and the expected growth

rate is 10%, the budgeted sales for this year would be ₹11 Lakh.

3. Incremental Budgeting : This method involves adjusting the previous

year's sales budget by a certain percentage to account for growth,

inflation, or market changes.

Example: If a company achieved 1 Lakh Sales and factors account for 20%

then Sales Budget will be 1.20 Lakh for the next year.

4. Zero-Based Budgeting (ZBB): Each sales budget starts from scratch,

and every expense or revenue projection must be justified.

Example: Instead of increasing last year's sales budget by a percentage,

each department must justify their sales projections based on actual needs.

4. Activity-Based Budgeting : This method focuses on the activities required to

achieve sales targets, such as marketing campaigns, sales calls, or distribution efforts.

Example: A company planning to launch a new product might budget for specific

activities like social media ads (10,000),tradeshows(10,000),tradeshows(5,000), and

sales team training ($3,000).

36.

Slides

Prepared

by:

Dr.

Mahtab

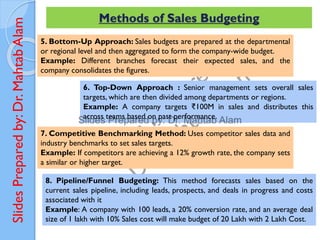

Alam Methods ofSales Budgeting

5. Bottom-Up Approach: Sales budgets are prepared at the departmental

or regional level and then aggregated to form the company-wide budget.

Example: Different branches forecast their expected sales, and the

company consolidates the figures.

6. Top-Down Approach : Senior management sets overall sales

targets, which are then divided among departments or regions.

Example: A company targets ₹100M in sales and distributes this

across teams based on past performance.

7. Competitive Benchmarking Method: Uses competitor sales data and

industry benchmarks to set sales targets.

Example: If competitors are achieving a 12% growth rate, the company sets

a similar or higher target.

8. Pipeline/Funnel Budgeting: This method forecasts sales based on the

current sales pipeline, including leads, prospects, and deals in progress and costs

associated with it

Example: A company with 100 leads, a 20% conversion rate, and an average deal

size of 1 lakh with 10% Sales cost will make budget of 20 Lakh with 2 Lakh Cost.

37.

Slides

Prepared

by:

Dr.

Mahtab

Alam Methods ofSales Budgeting

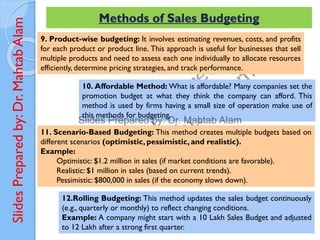

9. Product-wise budgeting: It involves estimating revenues, costs, and profits

for each product or product line. This approach is useful for businesses that sell

multiple products and need to assess each one individually to allocate resources

efficiently, determine pricing strategies, and track performance.

10. Affordable Method: What is affordable? Many companies set the

promotion budget at what they think the company can afford. This

method is used by firms having a small size of operation make use of

this methods for budgeting.

11. Scenario-Based Budgeting: This method creates multiple budgets based on

different scenarios (optimistic, pessimistic, and realistic).

Example:

Optimistic: $1.2 million in sales (if market conditions are favorable).

Realistic: $1 million in sales (based on current trends).

Pessimistic: $800,000 in sales (if the economy slows down).

12.Rolling Budgeting: This method updates the sales budget continuously

(e.g., quarterly or monthly) to reflect changing conditions.

Example: A company might start with a 10 Lakh Sales Budget and adjusted

to 12 Lakh after a strong first quarter.

38.

Slides

Prepared

by:

Dr.

Mahtab

Alam Sample ofSales Budget

Green Tech Solutions Sales Budget Plan for 2025

Product

Line

Q1 Sales

(Units)

Q2

Sales

(Units)

Q3

Sales

(Units)

Q4

Sales

(Units)

Average

Price per

Unit

Total

Revenue

Solar-

Powered

Lights

5,000 6,000 7,000 8,000 $50 $1,300,000

Energy-

Efficient

Fans

3,000 4,000 5,000 6,000 $80 $1,440,000

Smart

Thermostats

2,000 2,500 3,000 3,500 $120 $1,320,000

$4,060,000

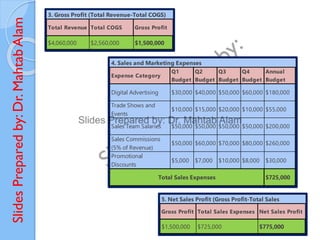

1. Revenue Projections

Total Revenue

Product

Line

Units

Sold

(Annual)

COGS per

Unit

Total

COGS

Solar-

Powered

Lights

26,000 $30 $780,000

Energy-

Efficient

Fans

18,000 $50 $900,000

Smart

Thermostats

11,000 $80 $880,000

$2,560,000

2. Cost of Goods Sold (COGS)

Total COGS

39.

Slides

Prepared

by:

Dr.

Mahtab

Alam

Expense Category

Q1

Budget

Q2

Budget

Q3

Budget

Q4

Budget

Annual

Budget

Digital Advertising$30,000 $40,000 $50,000 $60,000 $180,000

Trade Shows and

Events

$10,000 $15,000 $20,000 $10,000 $55,000

Sales Team Salaries $50,000 $50,000 $50,000 $50,000 $200,000

Sales Commissions

(5% of Revenue)

$50,000 $60,000 $70,000 $80,000 $260,000

Promotional

Discounts

$5,000 $7,000 $10,000 $8,000 $30,000

$725,000

4. Sales and Marketing Expenses

Total Sales Expenses

Gross Profit Total Sales Expenses Net Sales Profit

$1,500,000 $725,000 $775,000

5. Net Sales Profit (Gross Profit-Total Sales

Total Revenue Total COGS Gross Profit

$4,060,000 $2,560,000 $1,500,000

3. Gross Profit (Total Revenue-Total COGS)