Download to read offline

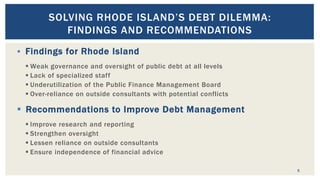

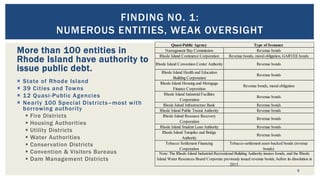

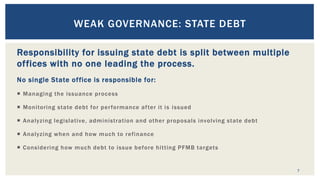

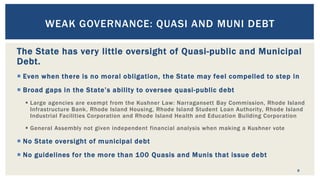

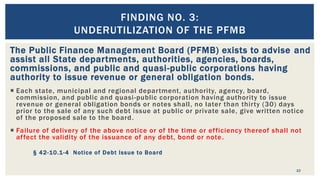

This document summarizes the findings of research into Rhode Island's public debt management practices. It identifies four main findings: 1) numerous entities issue debt with weak oversight; 2) a lack of professional debt management staff; 3) underutilization of the Public Finance Management Board; and 4) over-reliance on external consultants. It then provides recommendations to address these findings, including establishing an Office of Debt Management, strengthening PFMB oversight of quasi-public debt, ensuring independence of financial advice, and improving research and reporting. The document concludes systemic reform is needed to solve Rhode Island's debt management challenges.