Under the new standard, Company A's gross margin percentage will decrease from 40% to 33% due to the impairment loss reducing net revenue rather than being reported below the line as bad debt expense.

Extreme Makeover -

RevenueRecognition

Joint Project of the

FASB and IASB

Revenue from contracts

with customers

2.

Learning Objectives

• Providehistory behind and current status of

the new revenue accounting rules

• Review the new five-step recognition model

• Illustrate key concepts through examples

• Impact considerations and next steps

3.

History – Whythe Shift to a New Framework?

Objectives of the FASB & IASB…

• One global standard for revenue accounting and

reporting

• Currently IFRS guidance is not extensive – users often

refer to US GAAP for specific guidance

• Currently US GAAP guidance is comprised of 1) over-

riding guidelines established by the SEC, and 2) industry

specific bright line rules

• Inconsistencies exist between industries

• New standard designed to promote consistency and

comparability across industries and capital markets

4.

Timeline & CurrentStatus

• Project began in 2006

• Initial Exposure Draft Issued 2010

• Revised Exposure Draft Issued November 14, 2011

• Final Standard Expected in early 2013

• Effective Date – fiscal years beginning on or after January

1, 2015

• Full Retrospective Application – therefore public

companies must start complying in 2013 to facilitate on

time adoption

5.

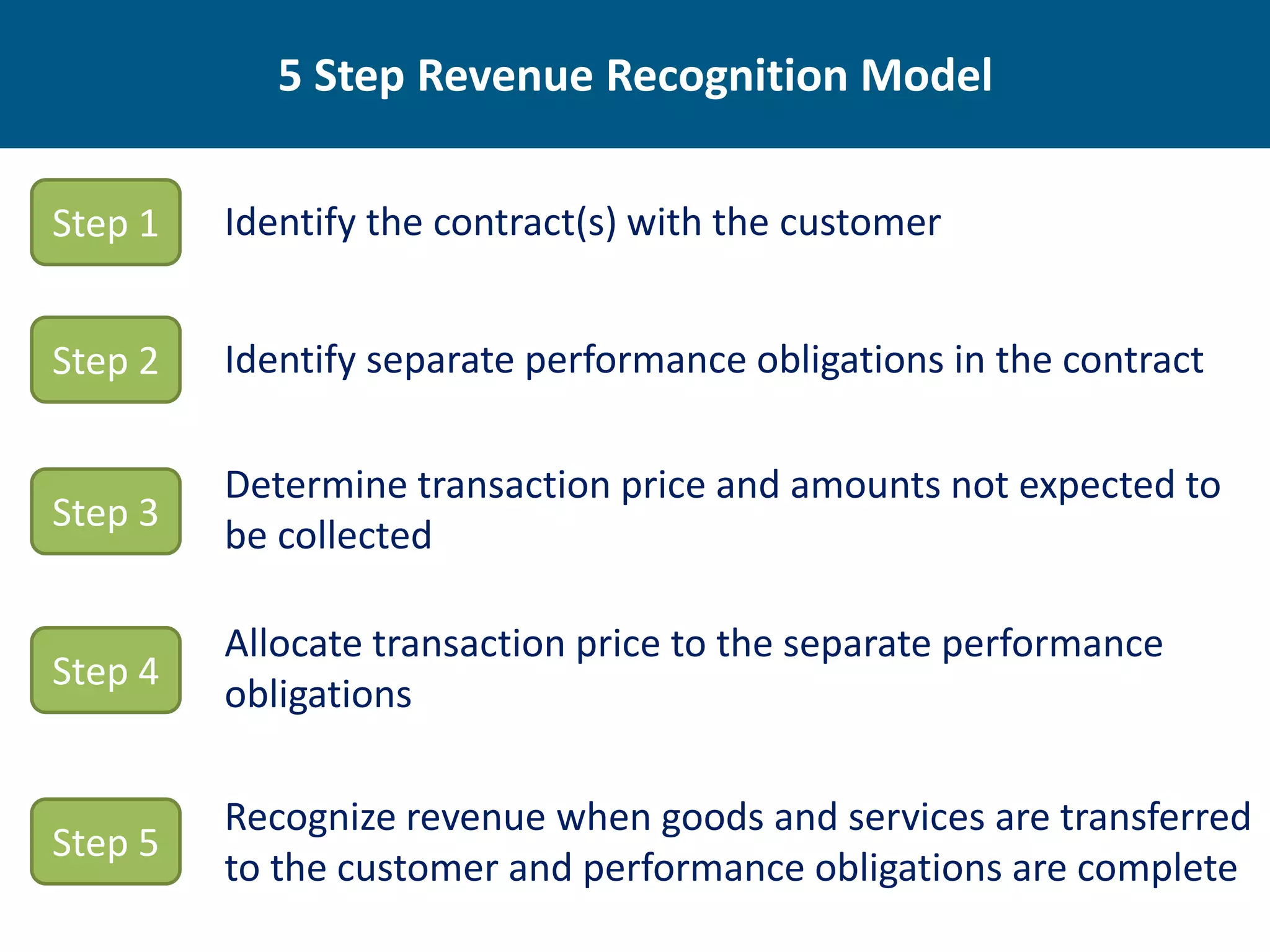

5 Step RevenueRecognition Model

Step 1 Identify the contract(s) with the customer

Step 2 Identify separate performance obligations in the contract

Determine transaction price and amounts not expected to

Step 3

be collected

Allocate transaction price to the separate performance

Step 4

obligations

Recognize revenue when goods and services are transferred

Step 5

to the customer and performance obligations are complete

6.

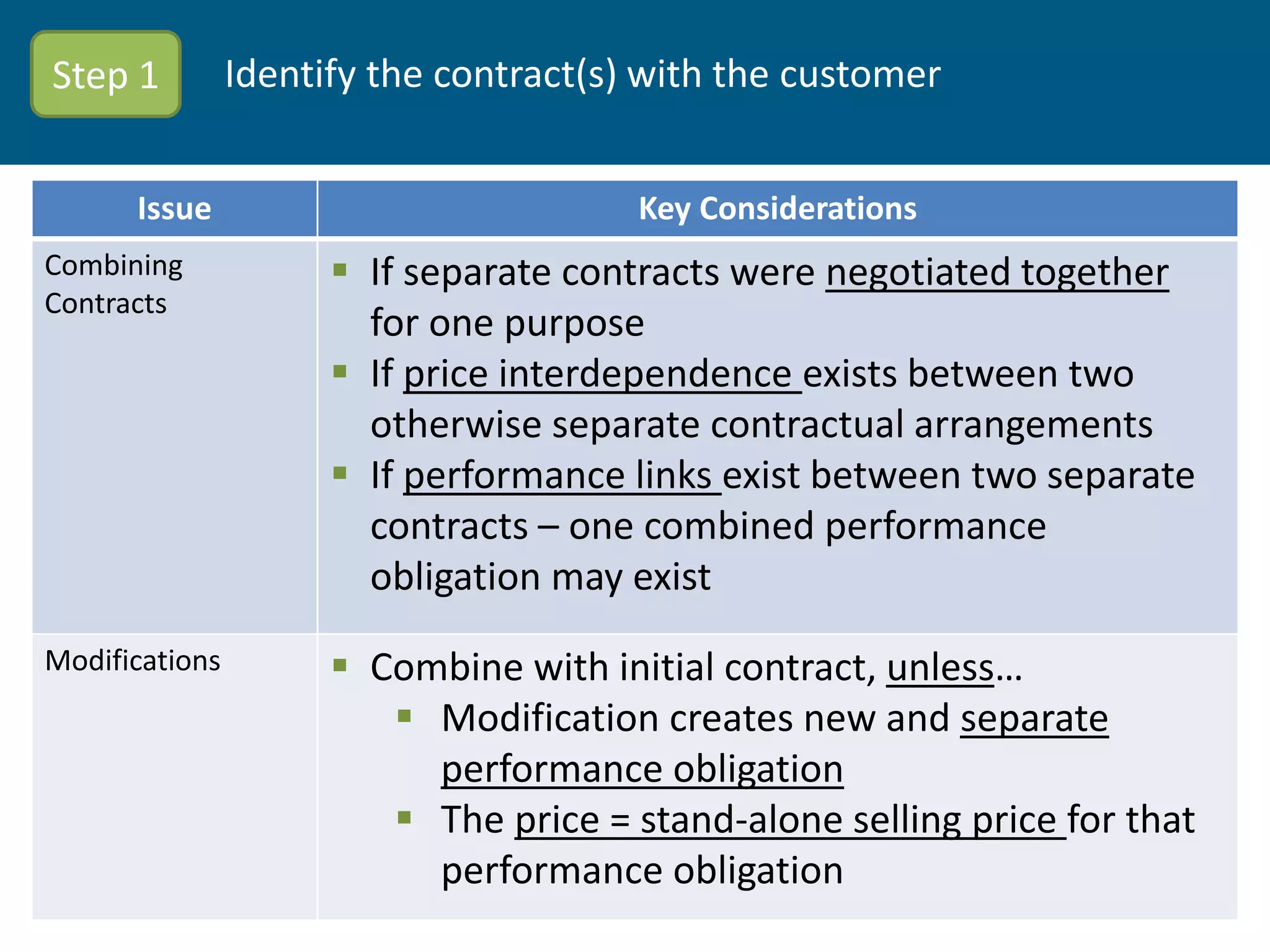

Step 1 Identify the contract(s) with the customer

Issue Key Considerations

Combining If separate contracts were negotiated together

Contracts

for one purpose

If price interdependence exists between two

otherwise separate contractual arrangements

If performance links exist between two separate

contracts – one combined performance

obligation may exist

Modifications Combine with initial contract, unless…

Modification creates new and separate

performance obligation

The price = stand-alone selling price for that

performance obligation

7.

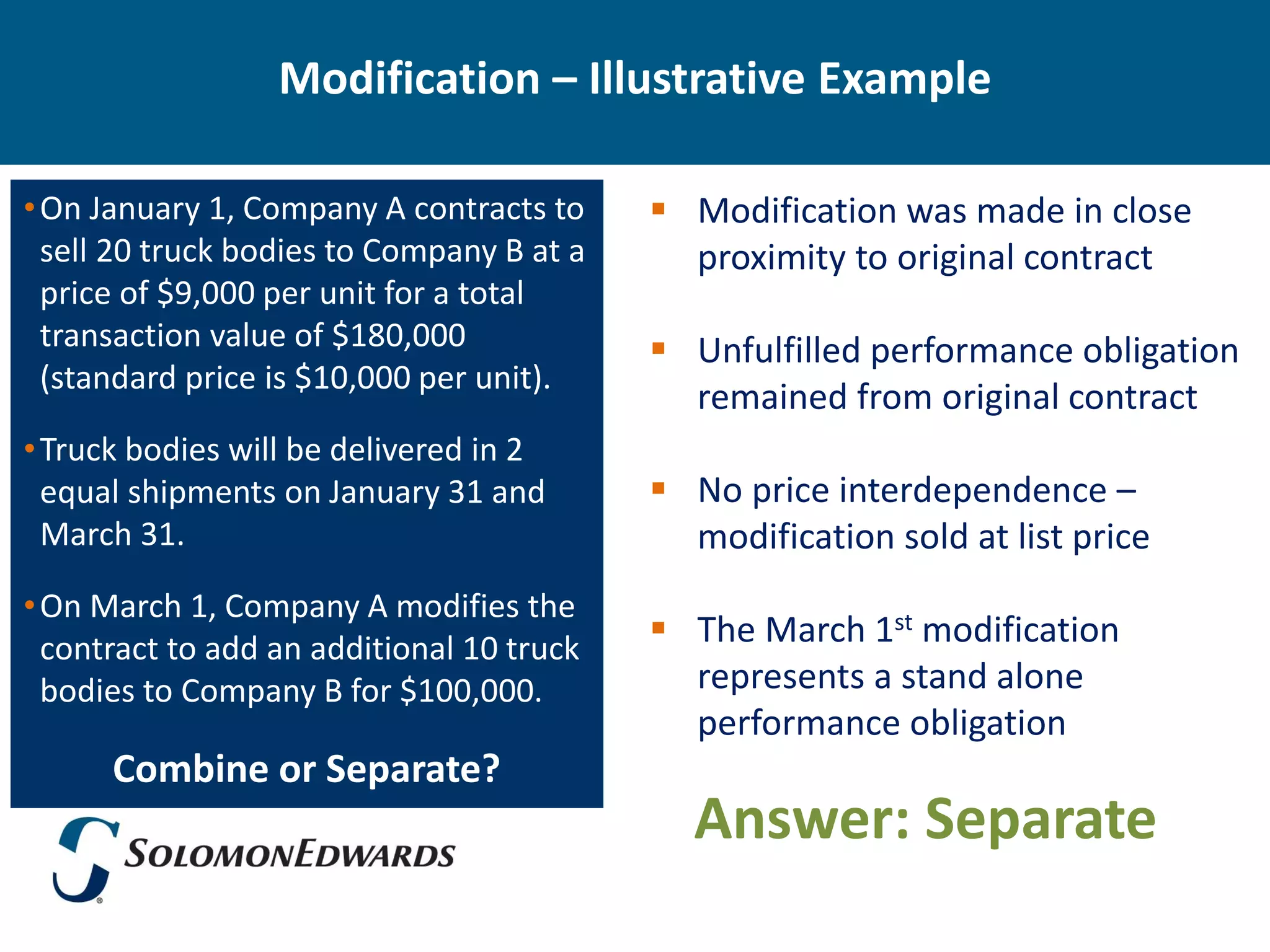

Modification – IllustrativeExample

• On January 1, Company A contracts to Modification was made in close

sell 20 truck bodies to Company B at a proximity to original contract

price of $9,000 per unit for a total

transaction value of $180,000 Unfulfilled performance obligation

(standard price is $10,000 per unit).

remained from original contract

• Truck bodies will be delivered in 2

equal shipments on January 31 and No price interdependence –

March 31. modification sold at list price

• On March 1, Company A modifies the

contract to add an additional 10 truck

The March 1st modification

bodies to Company B for $100,000. represents a stand alone

performance obligation

Combine or Separate?

Answer: Separate

8.

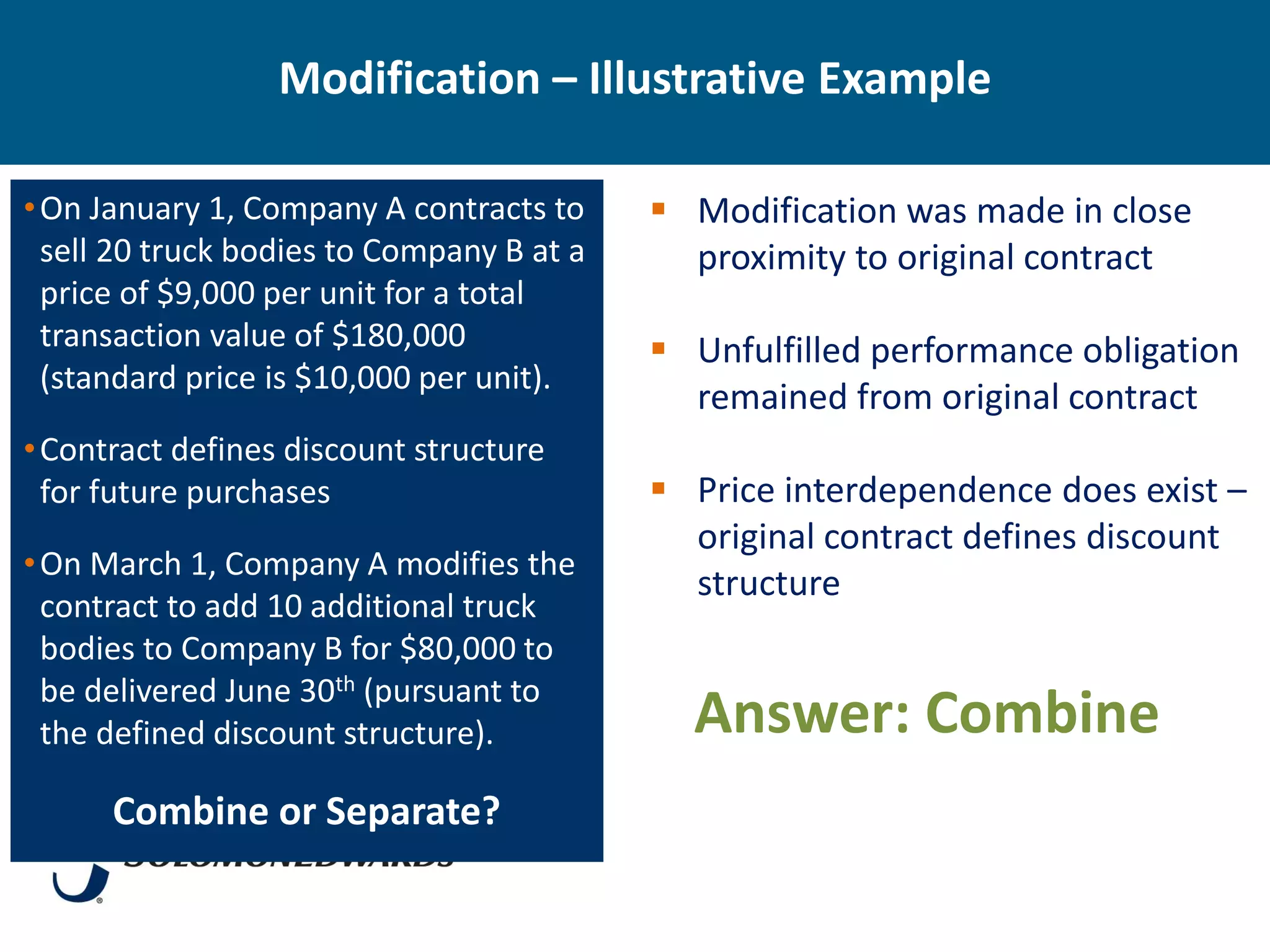

Modification – IllustrativeExample

• On January 1, Company A contracts to Modification was made in close

sell 20 truck bodies to Company B at a proximity to original contract

price of $9,000 per unit for a total

transaction value of $180,000 Unfulfilled performance obligation

(standard price is $10,000 per unit).

remained from original contract

• Contract defines discount structure

for future purchases Price interdependence does exist –

original contract defines discount

• On March 1, Company A modifies the

structure

contract to add 10 additional truck

bodies to Company B for $80,000 to

be delivered June 30th (pursuant to

the defined discount structure). Answer: Combine

Combine or Separate?

9.

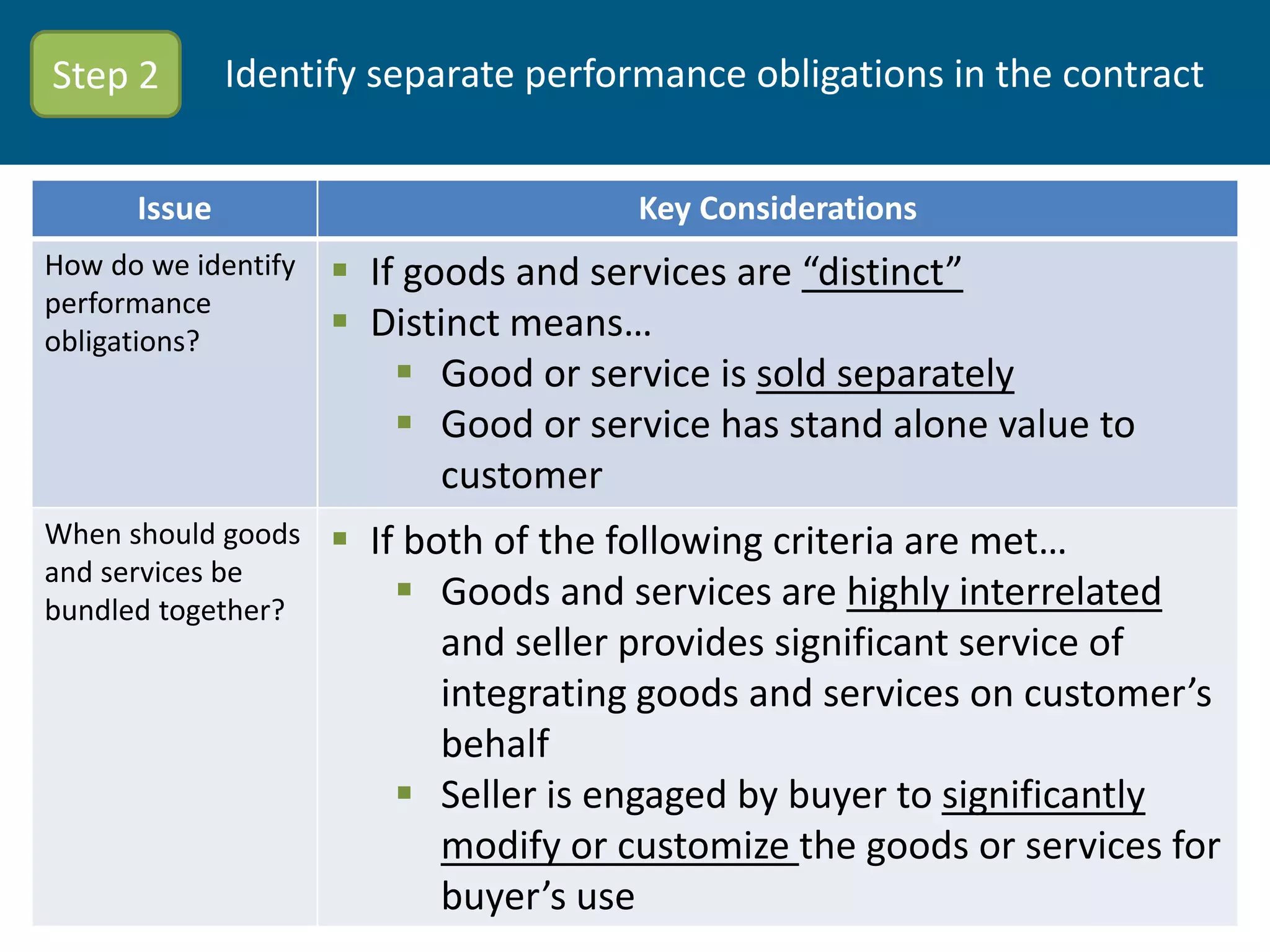

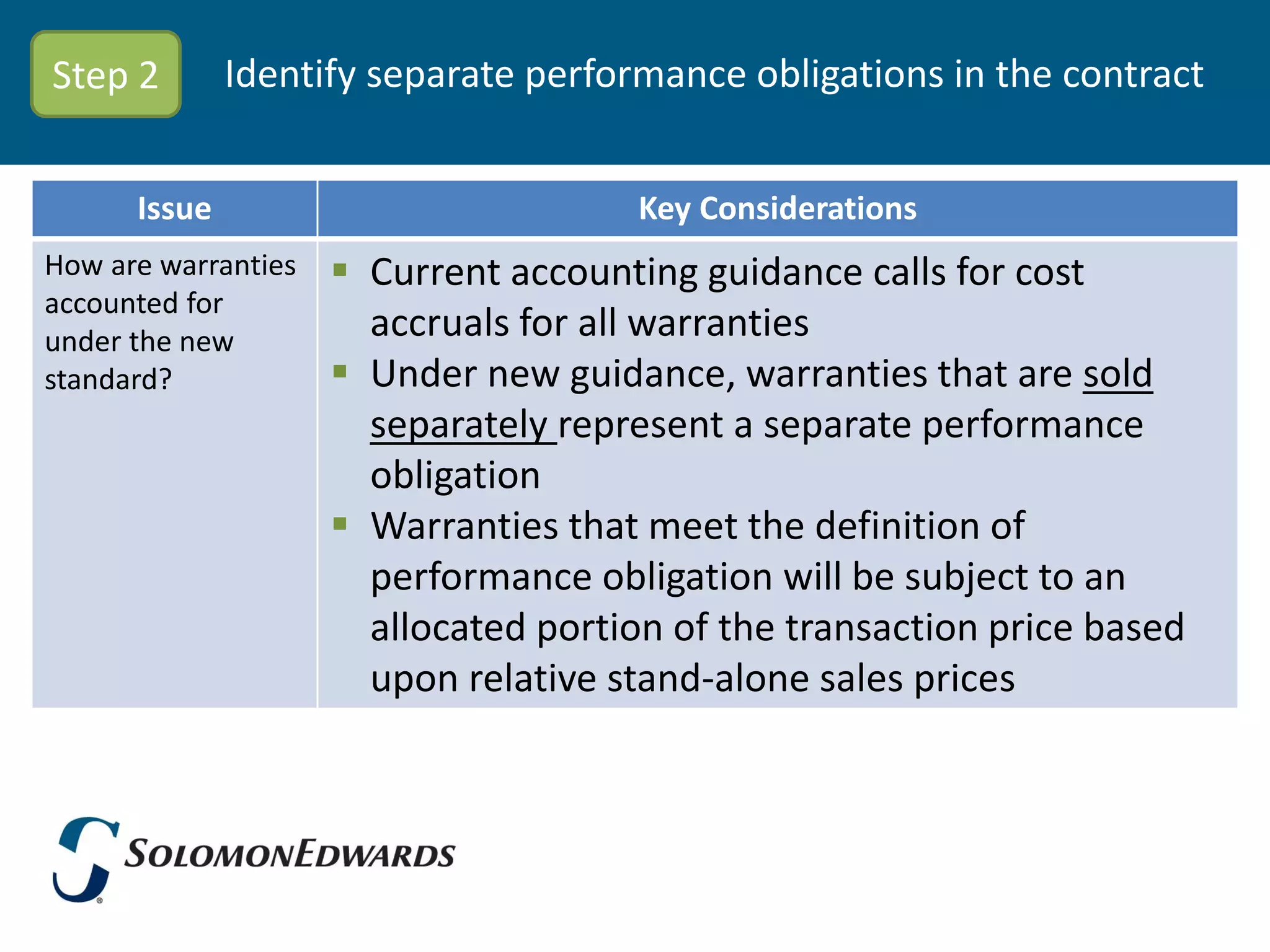

Step 2 Identify separate performance obligations in the contract

Issue Key Considerations

How do we identify If goods and services are “distinct”

performance

obligations? Distinct means…

Good or service is sold separately

Good or service has stand alone value to

customer

When should goods If both of the following criteria are met…

and services be

bundled together? Goods and services are highly interrelated

and seller provides significant service of

integrating goods and services on customer’s

behalf

Seller is engaged by buyer to significantly

modify or customize the goods or services for

buyer’s use

10.

Step 2 Identify separate performance obligations in the contract

Issue Key Considerations

How are warranties Current accounting guidance calls for cost

accounted for

under the new accruals for all warranties

standard? Under new guidance, warranties that are sold

separately represent a separate performance

obligation

Warranties that meet the definition of

performance obligation will be subject to an

allocated portion of the transaction price based

upon relative stand-alone sales prices

11.

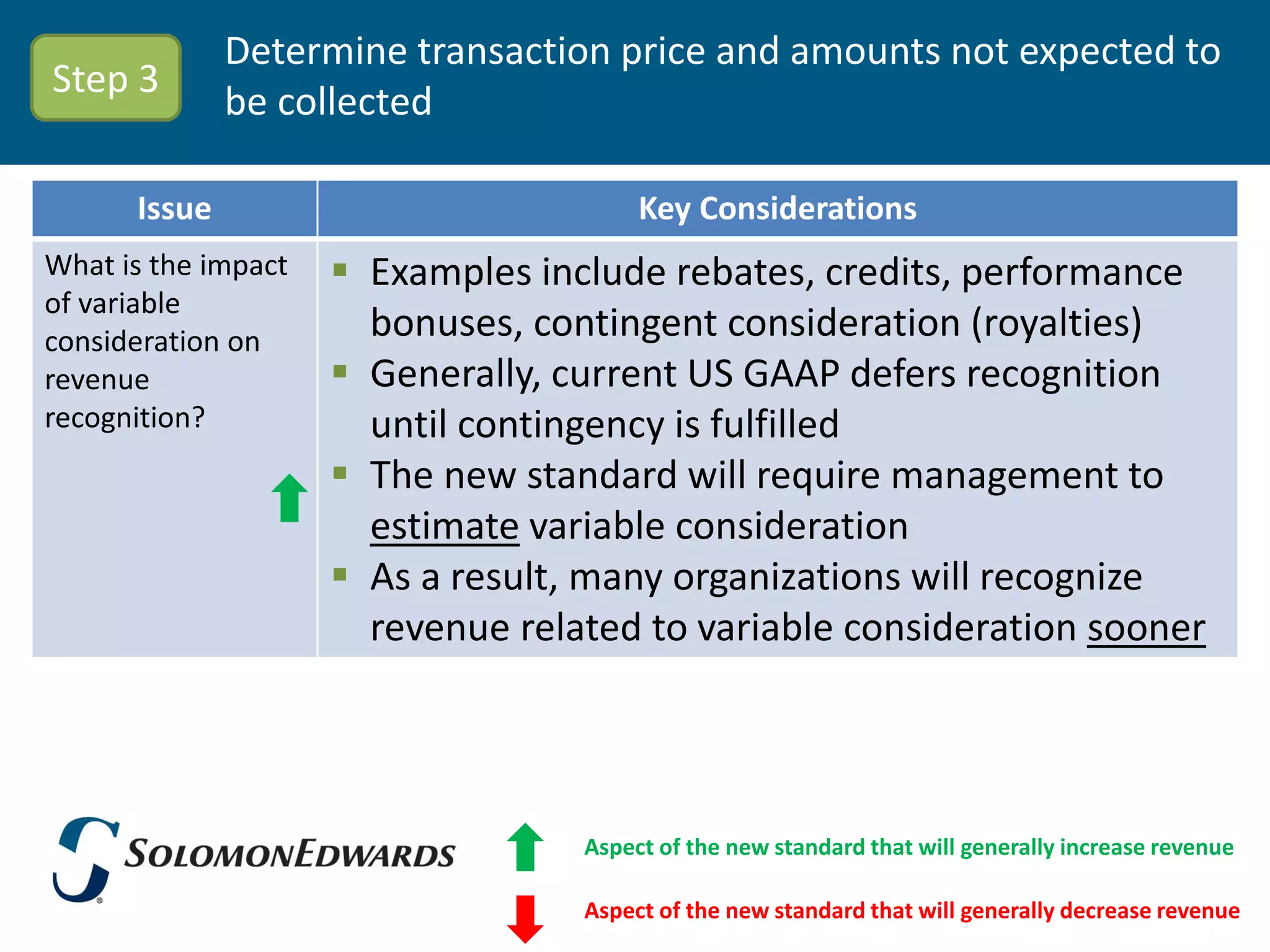

Determine transaction priceand amounts not expected to

Step 3

be collected

Issue Key Considerations

What is the impact Examples include rebates, credits, performance

of variable

consideration on bonuses, contingent consideration (royalties)

revenue Generally, current US GAAP defers recognition

recognition? until contingency is fulfilled

The new standard will require management to

estimate variable consideration

As a result, many organizations will recognize

revenue related to variable consideration sooner

Aspect of the new standard that will generally increase revenue

Aspect of the new standard that will generally decrease revenue

12.

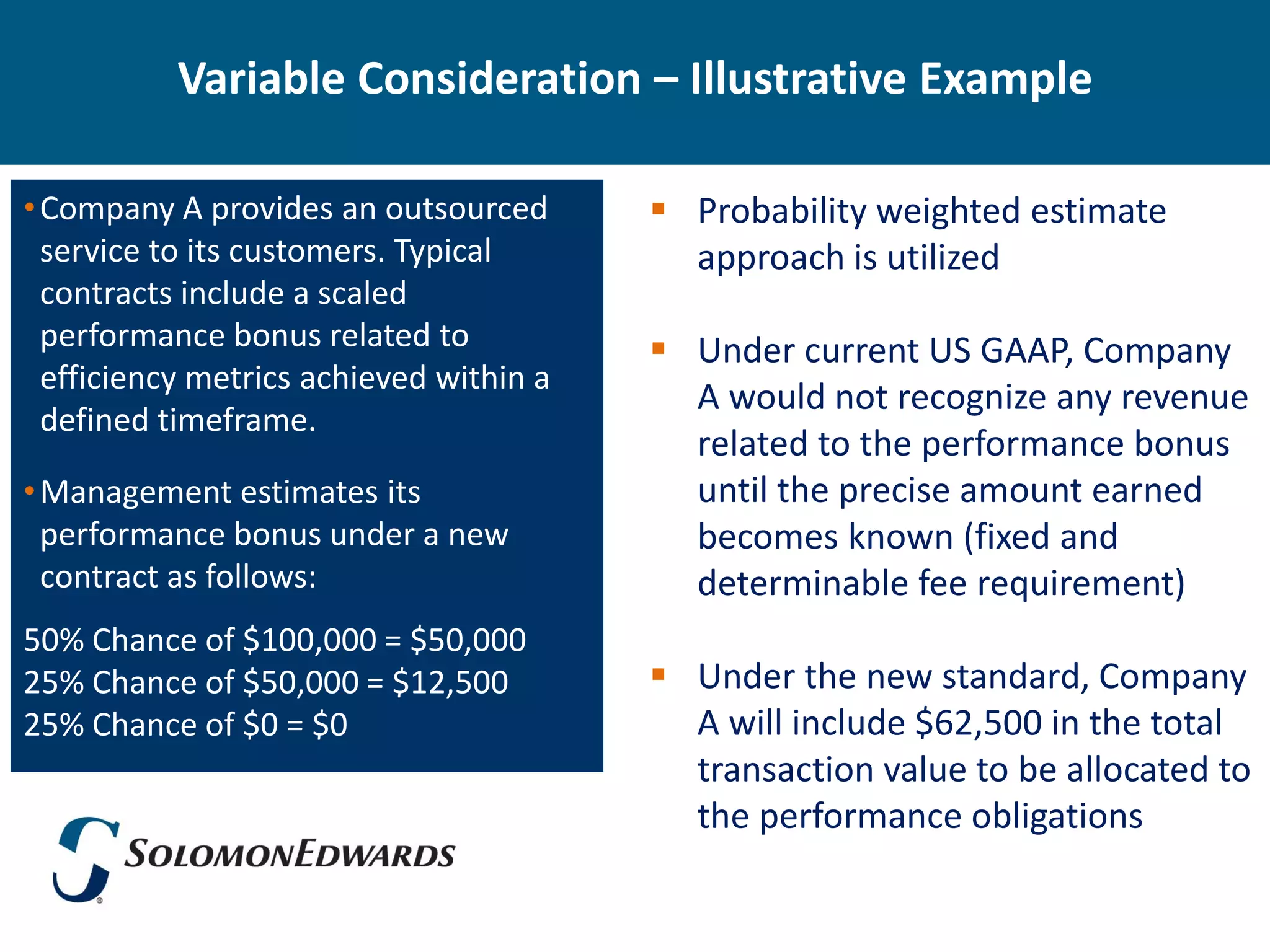

Variable Consideration –Illustrative Example

• Company A provides an outsourced Probability weighted estimate

service to its customers. Typical approach is utilized

contracts include a scaled

performance bonus related to Under current US GAAP, Company

efficiency metrics achieved within a

A would not recognize any revenue

defined timeframe.

related to the performance bonus

• Management estimates its until the precise amount earned

performance bonus under a new becomes known (fixed and

contract as follows: determinable fee requirement)

50% Chance of $100,000 = $50,000

25% Chance of $50,000 = $12,500 Under the new standard, Company

25% Chance of $0 = $0 A will include $62,500 in the total

transaction value to be allocated to

the performance obligations

13.

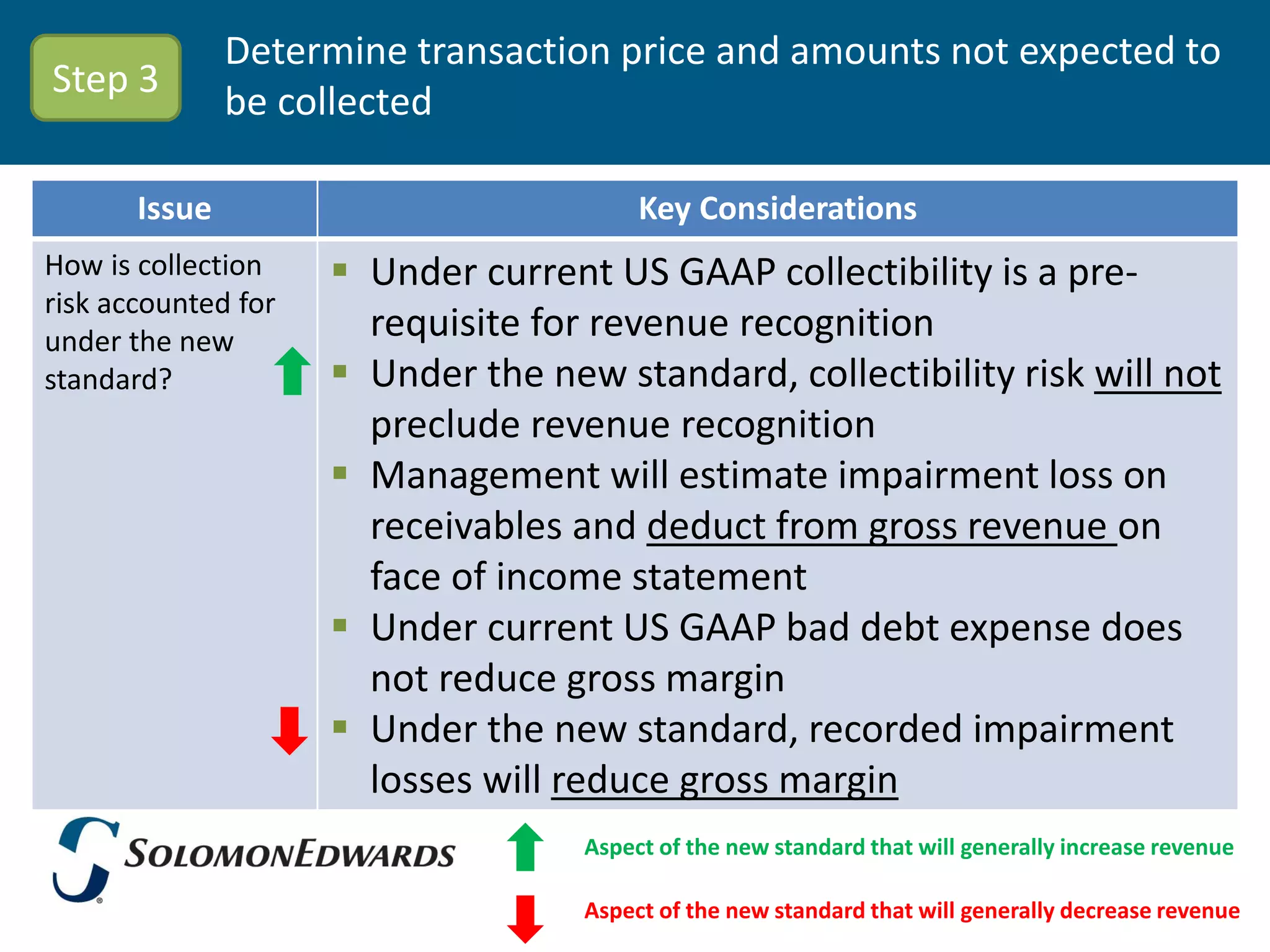

Determine transaction priceand amounts not expected to

Step 3

be collected

Issue Key Considerations

How is collection Under current US GAAP collectibility is a pre-

risk accounted for

under the new requisite for revenue recognition

standard? Under the new standard, collectibility risk will not

preclude revenue recognition

Management will estimate impairment loss on

receivables and deduct from gross revenue on

face of income statement

Under current US GAAP bad debt expense does

not reduce gross margin

Under the new standard, recorded impairment

losses will reduce gross margin

Aspect of the new standard that will generally increase revenue

Aspect of the new standard that will generally decrease revenue

14.

Collectibility– Illustrative Example

•Company A operates as a business to • Cost of sales per transaction is $3,000

consumer products seller.

• Historic bad debt write-offs at 10%

• Typical customer sales transactions

total $5,000

Current Accounting New Standard

Revenue $5,000 Revenue $5,000

Cost of Sales $3,000 Impairment Loss (500)

Gross Margin $2,000 Net Revenue $4,500

Gross Margin % 40% Cost of Sales $3,000

Bad Debt Expense $500 Gross Margin $1,500

Gross Margin % 30%

Bad Debt Expense $0

15.

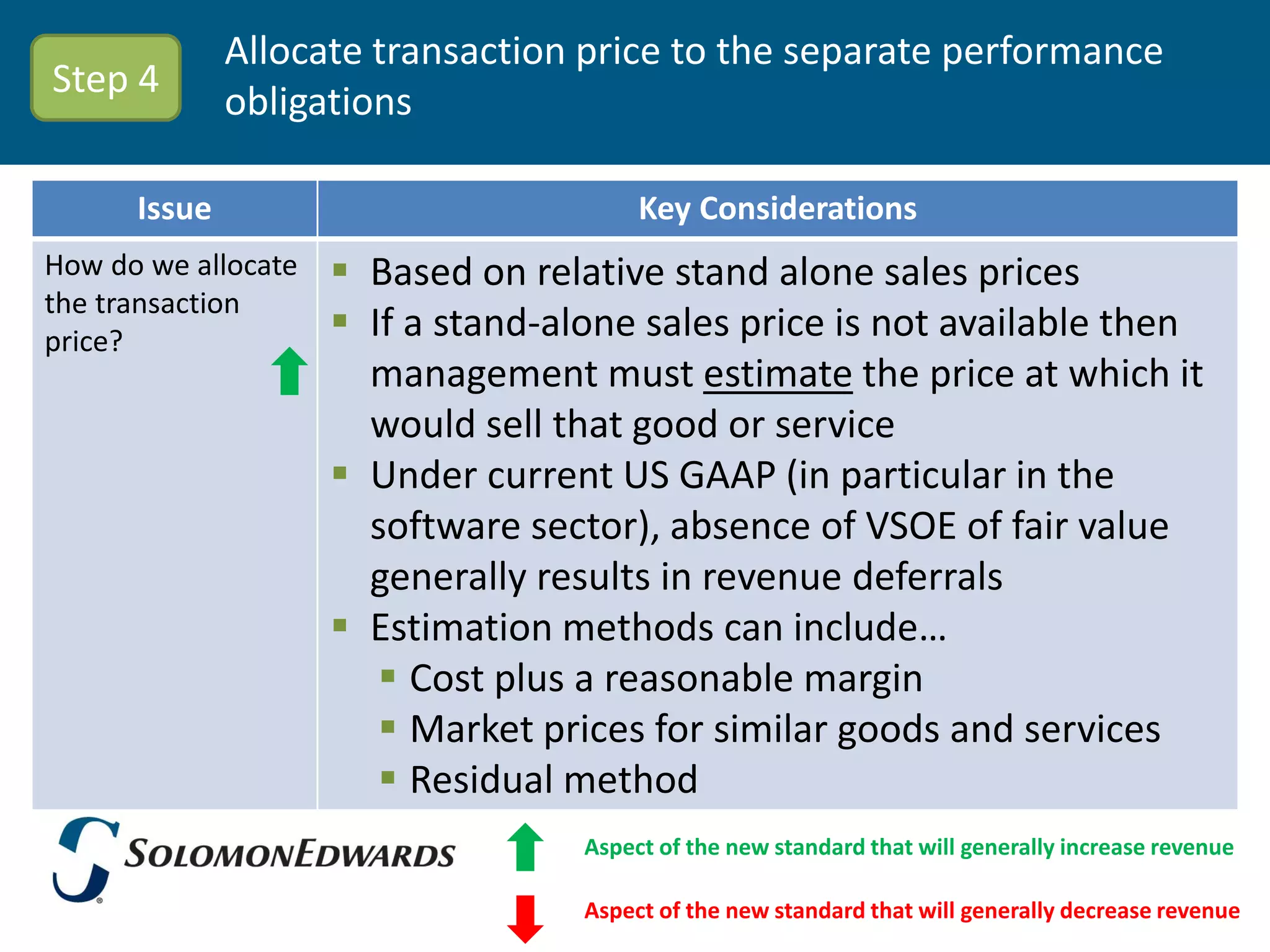

Allocate transaction priceto the separate performance

Step 4

obligations

Issue Key Considerations

How do we allocate Based on relative stand alone sales prices

the transaction

price? If a stand-alone sales price is not available then

management must estimate the price at which it

would sell that good or service

Under current US GAAP (in particular in the

software sector), absence of VSOE of fair value

generally results in revenue deferrals

Estimation methods can include…

Cost plus a reasonable margin

Market prices for similar goods and services

Residual method

Aspect of the new standard that will generally increase revenue

Aspect of the new standard that will generally decrease revenue

16.

Transaction Price Allocation– Illustrative Example

• Company A is a electronics products • 100 Hours of Design Service – Stand-

and services company. alone price is $500 per hour ($50,000)

• It has entered into a contract with a • Extended warranty – Stand-alone

customer that includes multiple price is $10,000

performance obligations including: • Contract value is $150,000

• Electronic component products –

Stand-alone price is $100,000

Performance Stand-alone Discount Factor Allocated

Obligation price ($150,000 / $160,000) Price

Electronic components $100,000 93.8% $93,750

Design services $50,000 93.8% $46,875

Extended warranty $10,000 93.8% $9,375

Totals $160,000 $150,000

17.

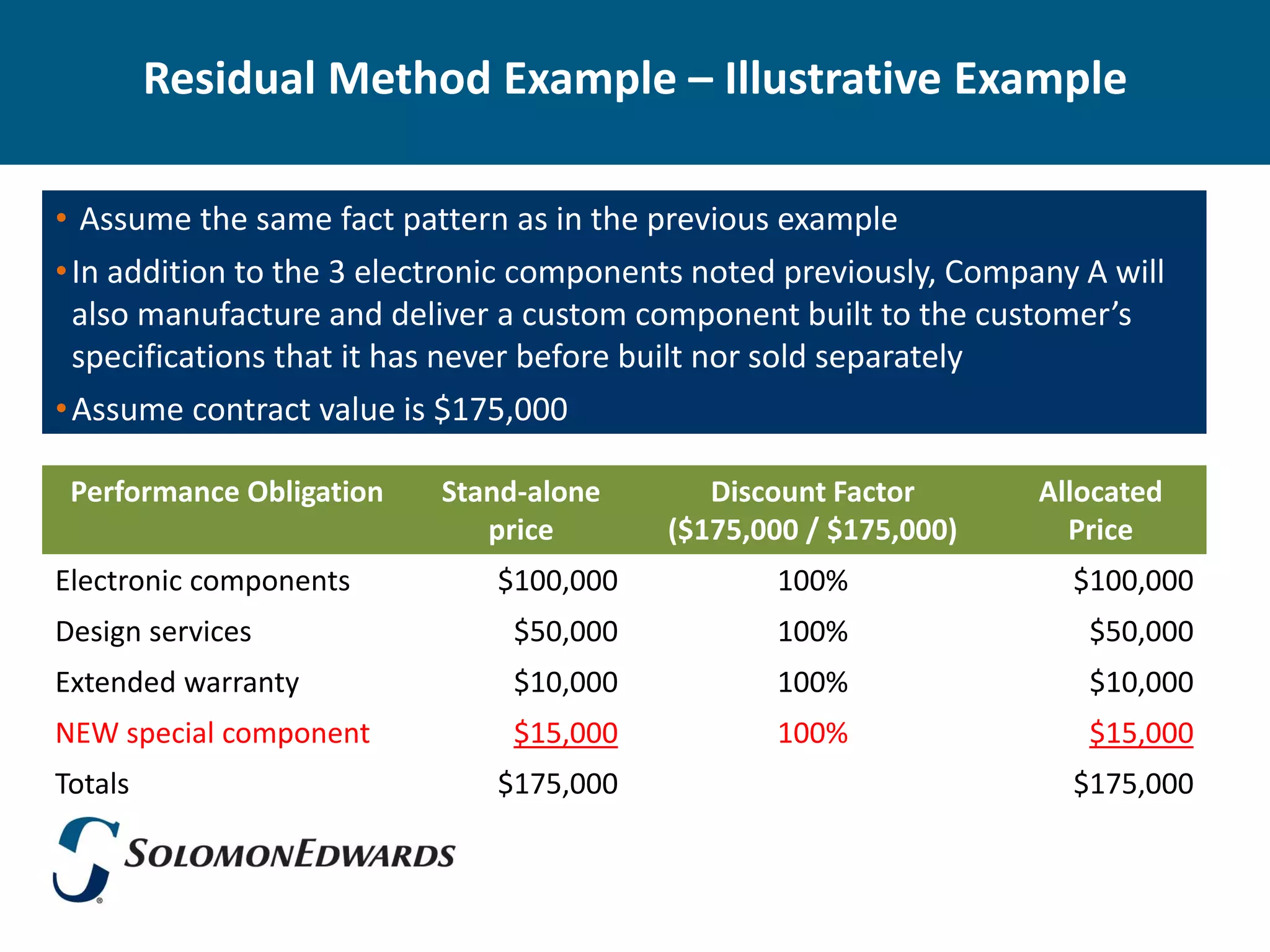

Residual Method Example– Illustrative Example

• Assume the same fact pattern as in the previous example

• In addition to the 3 electronic components noted previously, Company A will

also manufacture and deliver a custom component built to the customer’s

specifications that it has never before built nor sold separately

• Assume contract value is $175,000

Performance Obligation Stand-alone Discount Factor Allocated

price ($175,000 / $175,000) Price

Electronic components $100,000 100% $100,000

Design services $50,000 100% $50,000

Extended warranty $10,000 100% $10,000

NEW special component $15,000 100% $15,000

Totals $175,000 $175,000

18.

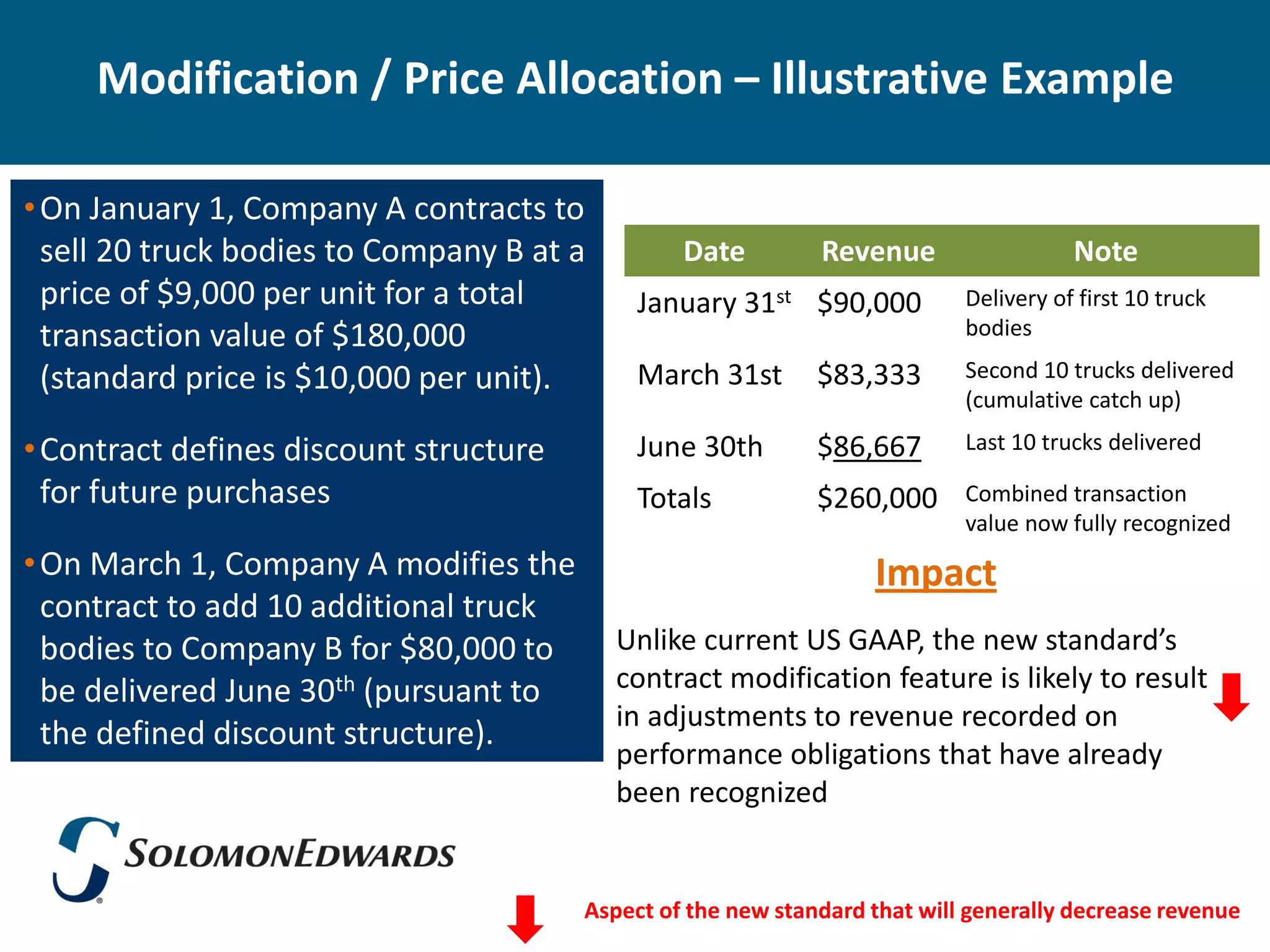

Modification / PriceAllocation – Illustrative Example

• On January 1, Company A contracts to

sell 20 truck bodies to Company B at a Date Revenue Note

price of $9,000 per unit for a total January 31st $90,000 Delivery of first 10 truck

transaction value of $180,000 bodies

(standard price is $10,000 per unit). March 31st $83,333 Second 10 trucks delivered

(cumulative catch up)

• Contract defines discount structure June 30th $86,667 Last 10 trucks delivered

for future purchases Totals $260,000 Combined transaction

value now fully recognized

• On March 1, Company A modifies the Impact

contract to add 10 additional truck

bodies to Company B for $80,000 to Unlike current US GAAP, the new standard’s

be delivered June 30th (pursuant to contract modification feature is likely to result

in adjustments to revenue recorded on

the defined discount structure).

performance obligations that have already

been recognized

Aspect of the new standard that will generally decrease revenue

19.

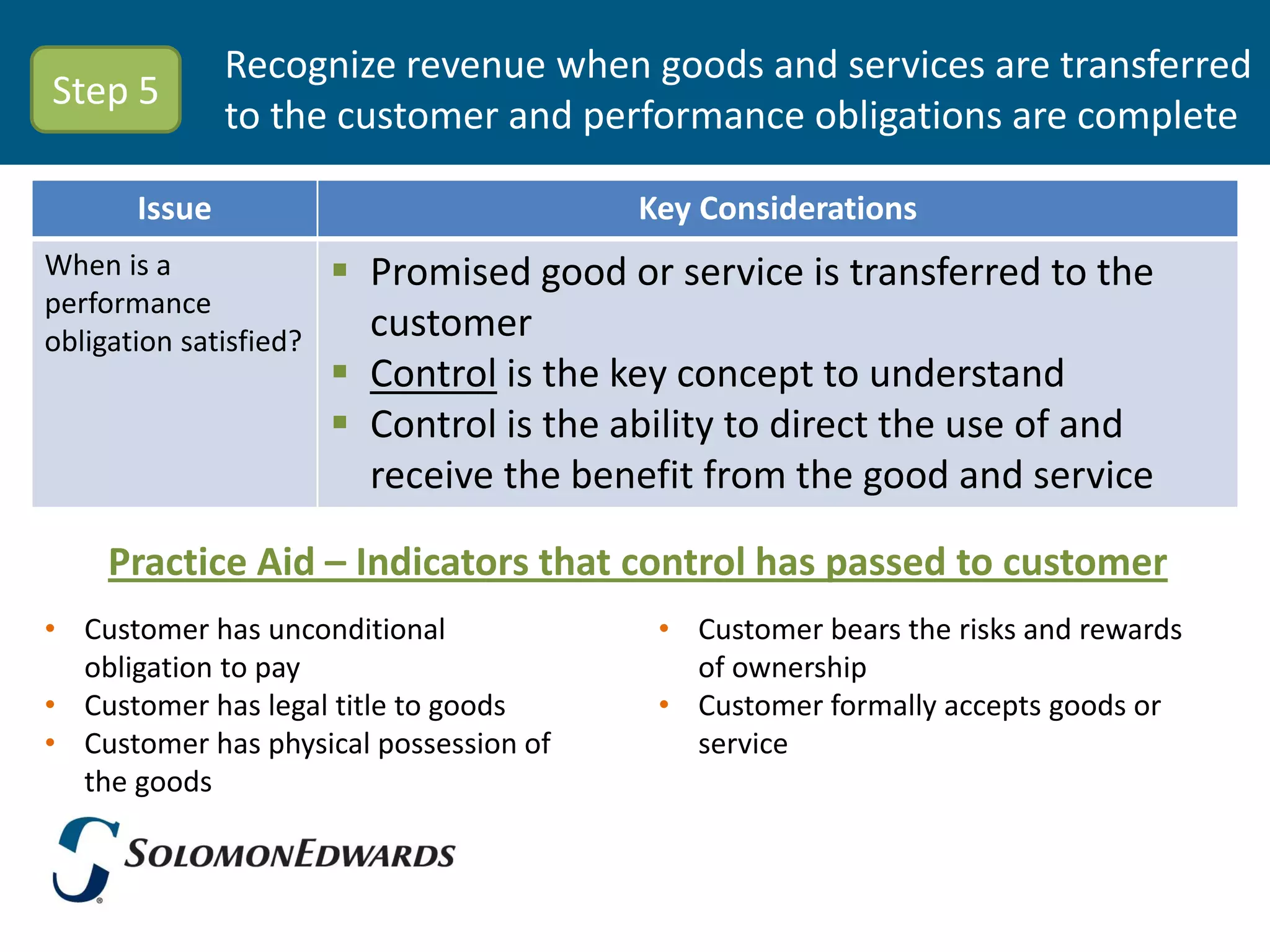

Recognize revenue whengoods and services are transferred

Step 5

to the customer and performance obligations are complete

Issue Key Considerations

When is a Promised good or service is transferred to the

performance

obligation satisfied? customer

Control is the key concept to understand

Control is the ability to direct the use of and

receive the benefit from the good and service

Practice Aid – Indicators that control has passed to customer

• Customer has unconditional • Customer bears the risks and rewards

obligation to pay of ownership

• Customer has legal title to goods • Customer formally accepts goods or

• Customer has physical possession of service

the goods

20.

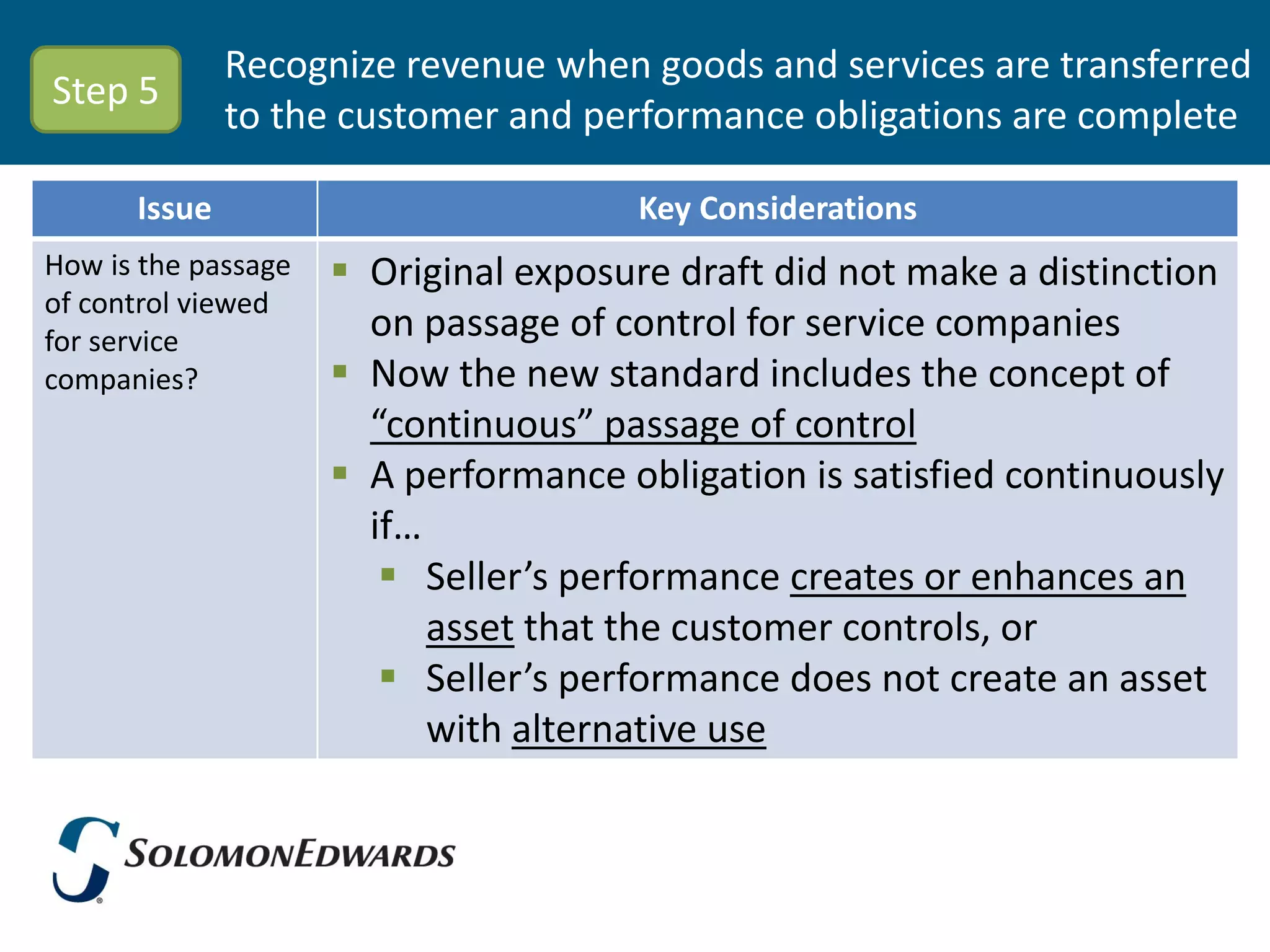

Recognize revenue whengoods and services are transferred

Step 5

to the customer and performance obligations are complete

Issue Key Considerations

How is the passage Original exposure draft did not make a distinction

of control viewed

for service on passage of control for service companies

companies? Now the new standard includes the concept of

“continuous” passage of control

A performance obligation is satisfied continuously

if…

Seller’s performance creates or enhances an

asset that the customer controls, or

Seller’s performance does not create an asset

with alternative use

21.

Other Important Highlightsof the New Standard

Unlike current US GAAP, the new standard

requires the capitalization of incremental

Contract Costs

costs incurred to obtain a contract if they are

expected to be recovered

• Applies to performance obligations

Onerous satisfied over 1 year or more

Performance • Assessed at performance obligation level

Obligations – not contract level

• Onerous = lowest cost of settling the

performance obligation exceeds the

amount of the transaction price allocated

22.

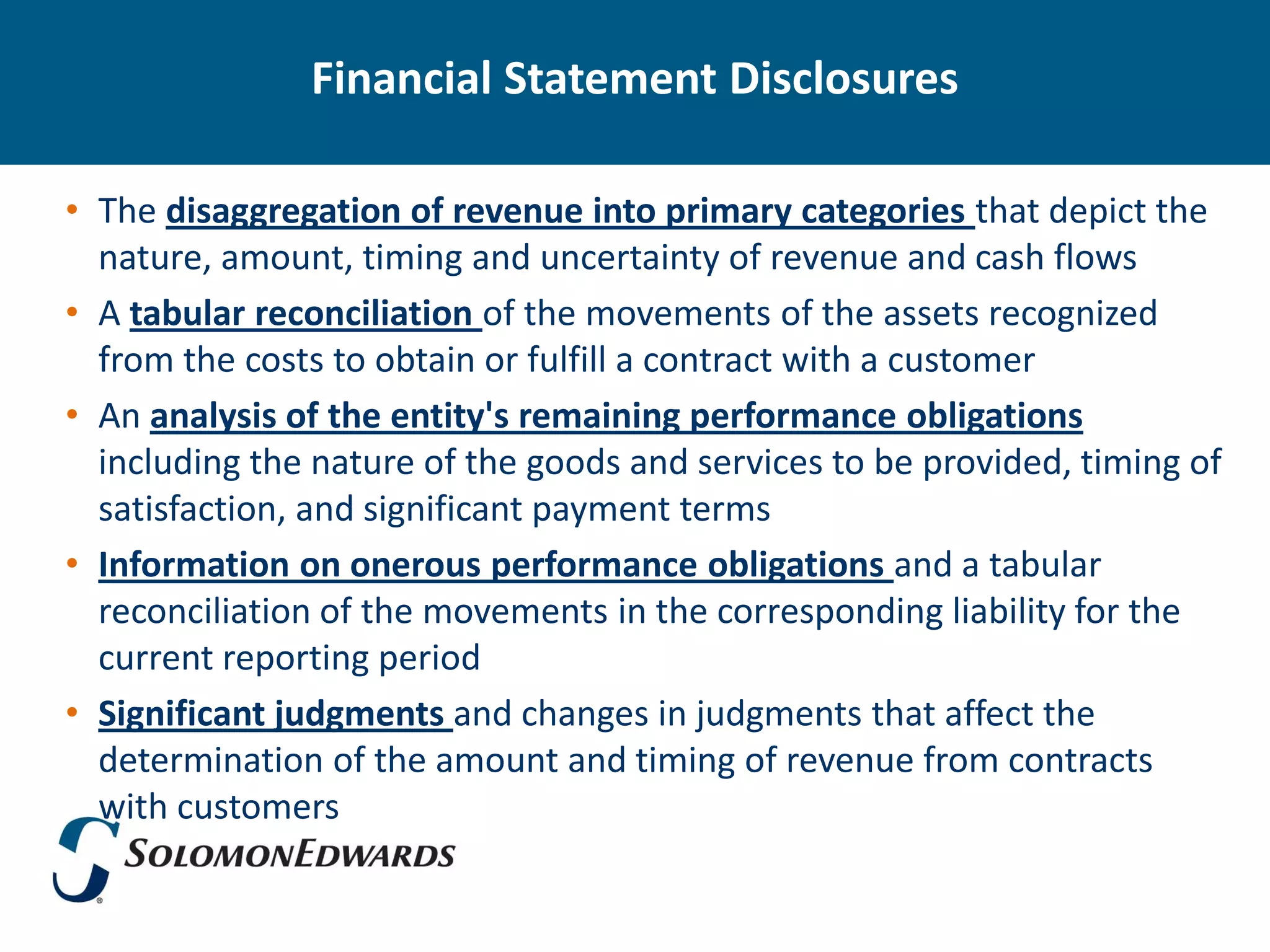

Financial Statement Disclosures

•The disaggregation of revenue into primary categories that depict the

nature, amount, timing and uncertainty of revenue and cash flows

• A tabular reconciliation of the movements of the assets recognized

from the costs to obtain or fulfill a contract with a customer

• An analysis of the entity's remaining performance obligations

including the nature of the goods and services to be provided, timing of

satisfaction, and significant payment terms

• Information on onerous performance obligations and a tabular

reconciliation of the movements in the corresponding liability for the

current reporting period

• Significant judgments and changes in judgments that affect the

determination of the amount and timing of revenue from contracts

with customers

23.

Comparison to StaffAccounting Bulletin Topic 13

(formerly SAB No. 104)

SAB Topic 13 Impact of IASB / FASB Exposure Draft

Contracts may be combined if highly interrelated or price

Persuasive interdependent

evidence of

arrangement Identify performance obligations for distinct goods or

services (distinct generally means “sold separately”)

Satisfaction of performance obligations triggers recognition

Customer must obtain control of the promised good or

Delivery has service

occurred or Distinction between goods and services now added in new

services have exposure draft – services subject to continuous control

been rendered passage guidance

Warranties (that can be purchased) are now treated as a

performance obligation not as a liability

24.

Comparison to StaffAccounting Bulletin Topic 13

(formerly SAB No. 104)

SAB Topic 13 Impact of IASB / FASB Exposure Draft

Transaction price is the amount of consideration expected to

be received from the customer

Allocate the transaction price to all distinct performance

The seller’s price obligations proportionally based on stand alone selling price

to the buyer is

fixed or Estimates of selling prices for distinct goods or services not

determinable sold separately will replace vendor specific objective

evidence criterion

Estimates will be incorporated when variable consideration

exists

Collection risk reflected as reduction of revenue rather than

Collectibility is bad debt – gross margins will be reduced

reasonably

assured Transactions falling short of SAB Topic 13 threshold may no

longer result in revenue deferrals

25.

Next Steps

• Theaccounting and disclosure requirements of the new revenue

standard are significant

• The impact will be greatest for companies with complex revenue

arrangements, bundled contracts and long term engagements

• Stay up to date on the evolving standard requirements and seek

out training opportunities

• Conduct an impact assessment in order to prepare for the

transition

• The retrospective transition provision means compliance may

need to start as soon as 2013

26.

SolomonEdwards At aGlance

SolomonEdwardsGroup, LLC (SolomonEdwards or SEG) is a national

business advisory and professional staffing firm. Our customized solutions

provide our clients with the right combination of talent and expertise to

achieve their business objectives.

With practices specialized in Accounting & Finance and Banking &

Financial Services, our strength lies in our ability to tactically assist clients

with special projects, transaction support & integration, business process

optimization initiatives, and regulatory compliance requirements.

Because we provide both business advisory and staffing services, SEG can

customize a solution for each client we serve. If you need an individual to

fill a role on an interim or permanent basis, a large team to execute a

project initiative, or expert consultation on a technical issue, we can help.

We operate from seven offices in major cities throughout the country and

maintain a global network of partners to serve multinational clients.

27.

Our Services &Solutions

Our core service capabilities encompass business advisory, project

management, interim staffing and professional search. We deliver our

services to our clients across a spectrum of functional and industry verticals

that enables us to provide the specific expertise and methodologies required

to deliver outstanding results.

28.

Our Services &Solutions

Interim CFO & Controller Business Process Improvement

General Ledger Accounting & Policy & Procedure Development

Reporting Business Intelligence Tools

Financial Modeling Financial Planning & Analysis

Financial System Assessment & Budgeting & Forecasting

Optimization Business

Accounting Shared Service Center Support

Process

& Finance

Optimization

Project Management Office Transaction Technical Accounting

Regulatory

Due Diligence Support & US GAAP & IFRS Advisory

Compliance

Merger Integration

Integration SEC Reporting & Compliance

Financial Carve-out Sarbanes-Oxley

IPO Readiness Internal Audit Services

Bankruptcy & Turnaround Technology Risk

29.

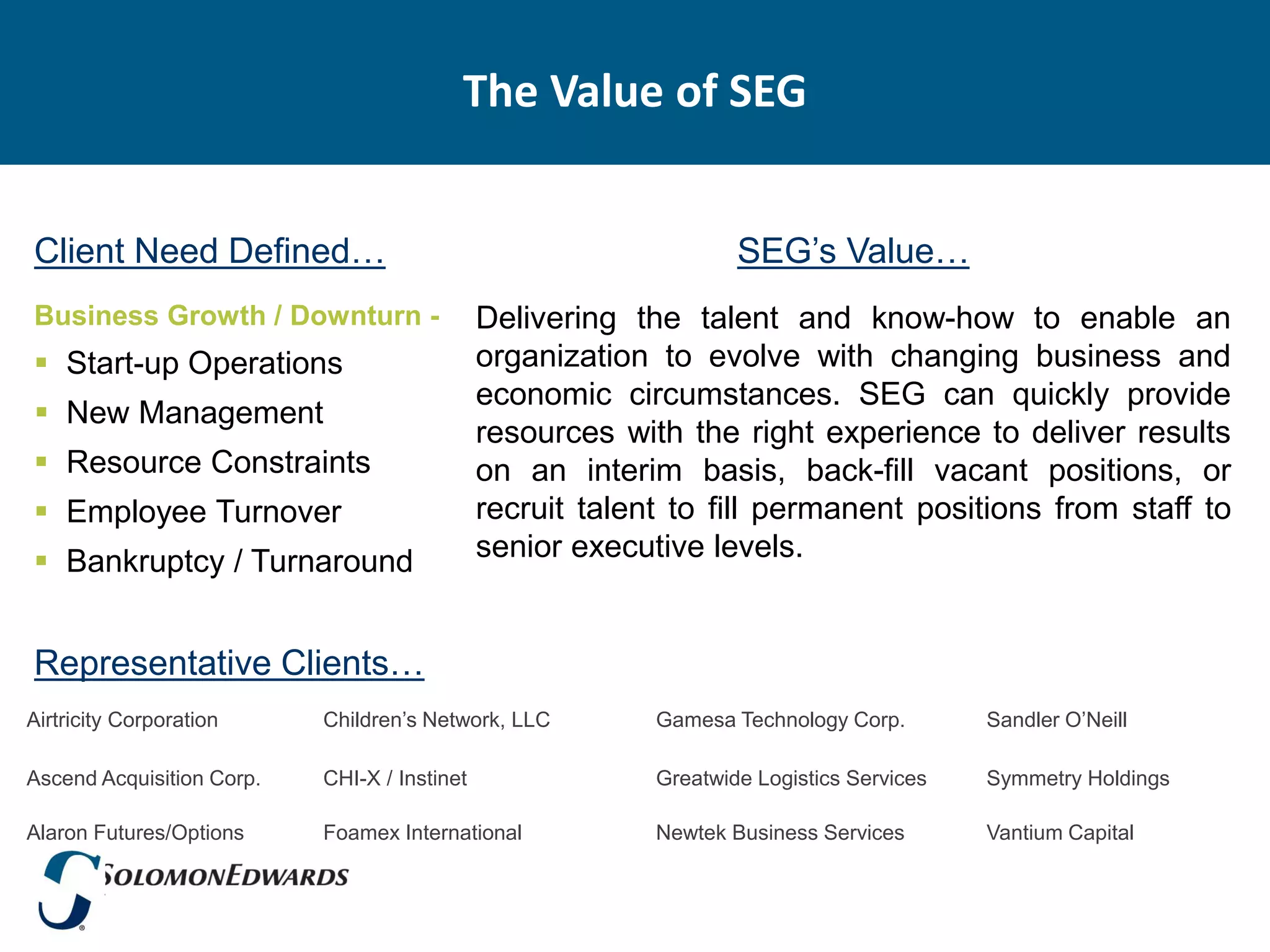

The Value ofSEG

Client Need Defined… SEG’s Value…

Ownership Change Delivering the talent and know-how to execute due

Mergers & Acquisitions diligence, merger integration, technical accounting,

SEC reporting, IPO readiness, SOX compliance and

IPO’s more. SEG can mobilize and manage resources for

Leveraged Buyout special projects, provide professionals to back-fill

positions during the change process or recruit talent

Private Equity investment to fill roles on a permanent basis.

Representative Clients…

Acqura Loan Services, Inc. Exelon Power Hexion Specialty Chemicals Talk America

Comcast Corporation Frontier Telecommunications PanAmSat Corporation Terra Nova Financial Group

Electro-Motive Diesel, Inc. Graftech, Inc. Olympus Power, LLC Verso Paper, Inc.

30.

The Value ofSEG

Client Need Defined… SEG’s Value…

Compliance Delivering the talent and know-how to enable our

SEC Reporting clients to comply with applicable regulations across of

broad spectrum of issues. SEG can serve as a

Financial Restatements technical advisor, mobilize and manage resources

US GAAP / IFRS for compliance initiatives, provide professionals to

Sarbanes - Oxley augment client teams during peak compliance

periods, or recruit talent to fill permanent roles.

Bank Compliance

Representative Clients…

ABN AMRO E.ON Climate & Renewables Franklin Bank Leo Burnett USA, Inc.

Amerisafe, Inc. FIMAT USA, Inc. GMH Communities Parsons Brinckerhoff

Cambridge Display Tech Foote, Cone & Belding Integra Life Sciences Whitney Bank

31.

The Value ofSEG

Client Need Defined… SEG’s Value…

Business Growth / Downturn - Delivering the talent and know-how to enable an

Start-up Operations organization to evolve with changing business and

economic circumstances. SEG can quickly provide

New Management

resources with the right experience to deliver results

Resource Constraints on an interim basis, back-fill vacant positions, or

Employee Turnover recruit talent to fill permanent positions from staff to

Bankruptcy / Turnaround senior executive levels.

Representative Clients…

Airtricity Corporation Children’s Network, LLC Gamesa Technology Corp. Sandler O’Neill

Ascend Acquisition Corp. CHI-X / Instinet Greatwide Logistics Services Symmetry Holdings

Alaron Futures/Options Foamex International Newtek Business Services Vantium Capital

32.

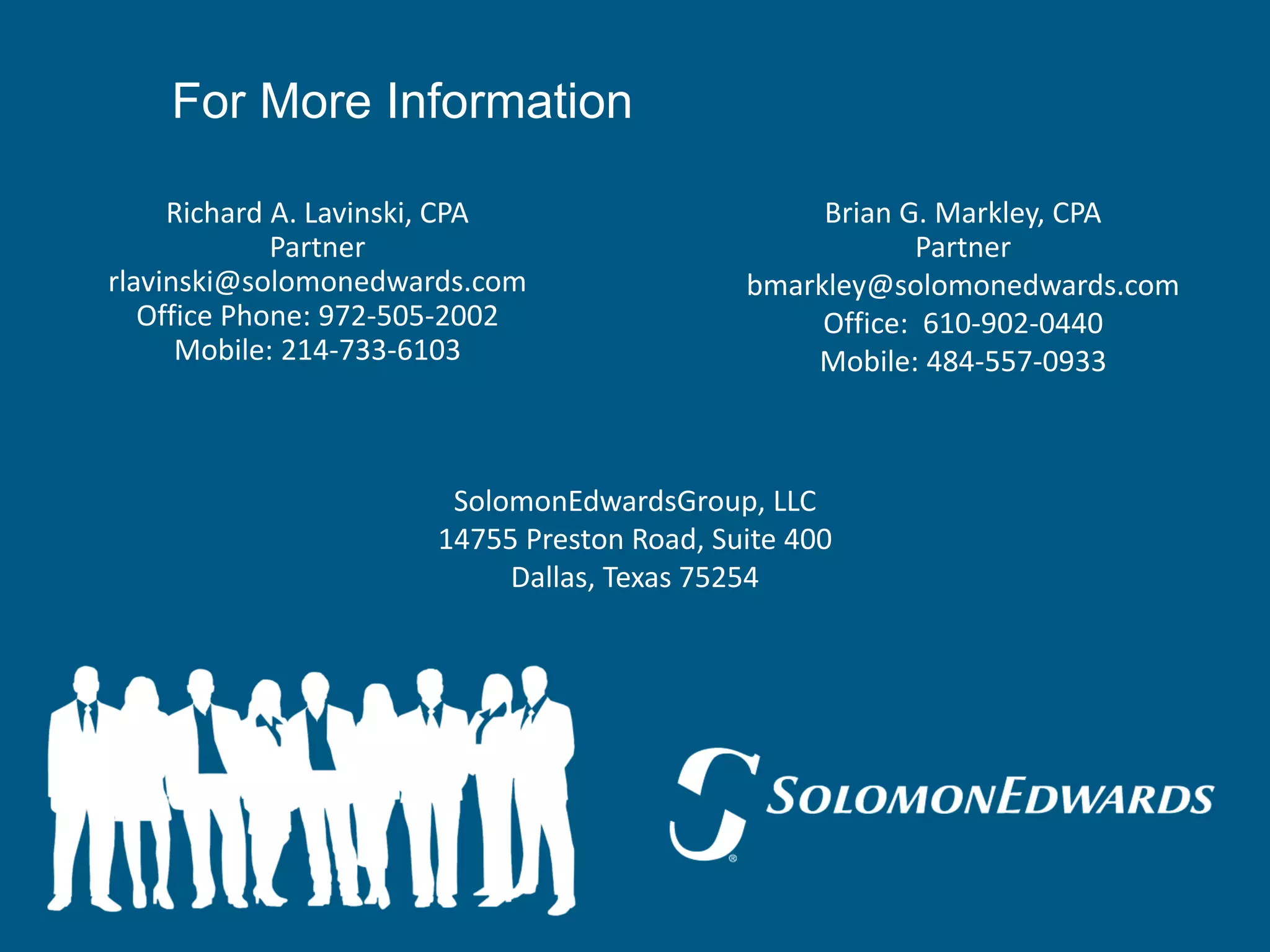

For More Information

Richard A. Lavinski, CPA Brian G. Markley, CPA

Partner Partner

rlavinski@solomonedwards.com bmarkley@solomonedwards.com

Office Phone: 972-505-2002 Office: 610-902-0440

Mobile: 214-733-6103 Mobile: 484-557-0933

SolomonEdwardsGroup, LLC

14755 Preston Road, Suite 400

Dallas, Texas 75254

![CleanMyMac X v5.2.8 Crack for MacOS Full Version [Latest] pptx](https://cdn.slidesharecdn.com/ss_thumbnails/softwareoverview-251207194121-a81f0142-thumbnail.jpg?width=640&height=640&fit=bounds)

![Wondershare Filmora 15.0.11 Crack for Mac Key Full Download [Latest] pptx](https://cdn.slidesharecdn.com/ss_thumbnails/software-251207184836-1d16ba16-thumbnail.jpg?width=640&height=640&fit=bounds)

![Chapter4_Initiation_of_Sediment_Motion_v2[1].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/chapter4initiationofsedimentmotionv21-251208223747-f94ef163-thumbnail.jpg?width=640&height=640&fit=bounds)

![Moho Pro 14.4 Crack for MacOS Works Until 2050 [Latest] pptx](https://cdn.slidesharecdn.com/ss_thumbnails/softwareoverview-251207192639-797289c4-thumbnail.jpg?width=640&height=640&fit=bounds)

![Soundtoys Mac v5.5.5.0 Crack for MacOS Full Version [Latest] pptx](https://cdn.slidesharecdn.com/ss_thumbnails/softwareoverview-251207193711-91d8ae6b-thumbnail.jpg?width=640&height=640&fit=bounds)

![iStat Menus 7.20 Crack for MacOS 2026 Full Version [Latest] pptx](https://cdn.slidesharecdn.com/ss_thumbnails/softwareoverview-251207191544-22b737dc-thumbnail.jpg?width=640&height=640&fit=bounds)