Download free for 30 days

Sign in

Upload

Language (EN)

Support

Business

Mobile

Social Media

Marketing

Technology

Art & Photos

Career

Design

Education

Presentations & Public Speaking

Government & Nonprofit

Healthcare

Internet

Law

Leadership & Management

Automotive

Engineering

Software

Recruiting & HR

Retail

Sales

Services

Science

Small Business & Entrepreneurship

Food

Environment

Economy & Finance

Data & Analytics

Investor Relations

Sports

Spiritual

News & Politics

Travel

Self Improvement

Real Estate

Entertainment & Humor

Health & Medicine

Devices & Hardware

Lifestyle

Change Language

Language

English

Español

Português

Français

Deutsche

Cancel

Save

Submit search

EN

TT

Uploaded by

taxman taxman

171 views

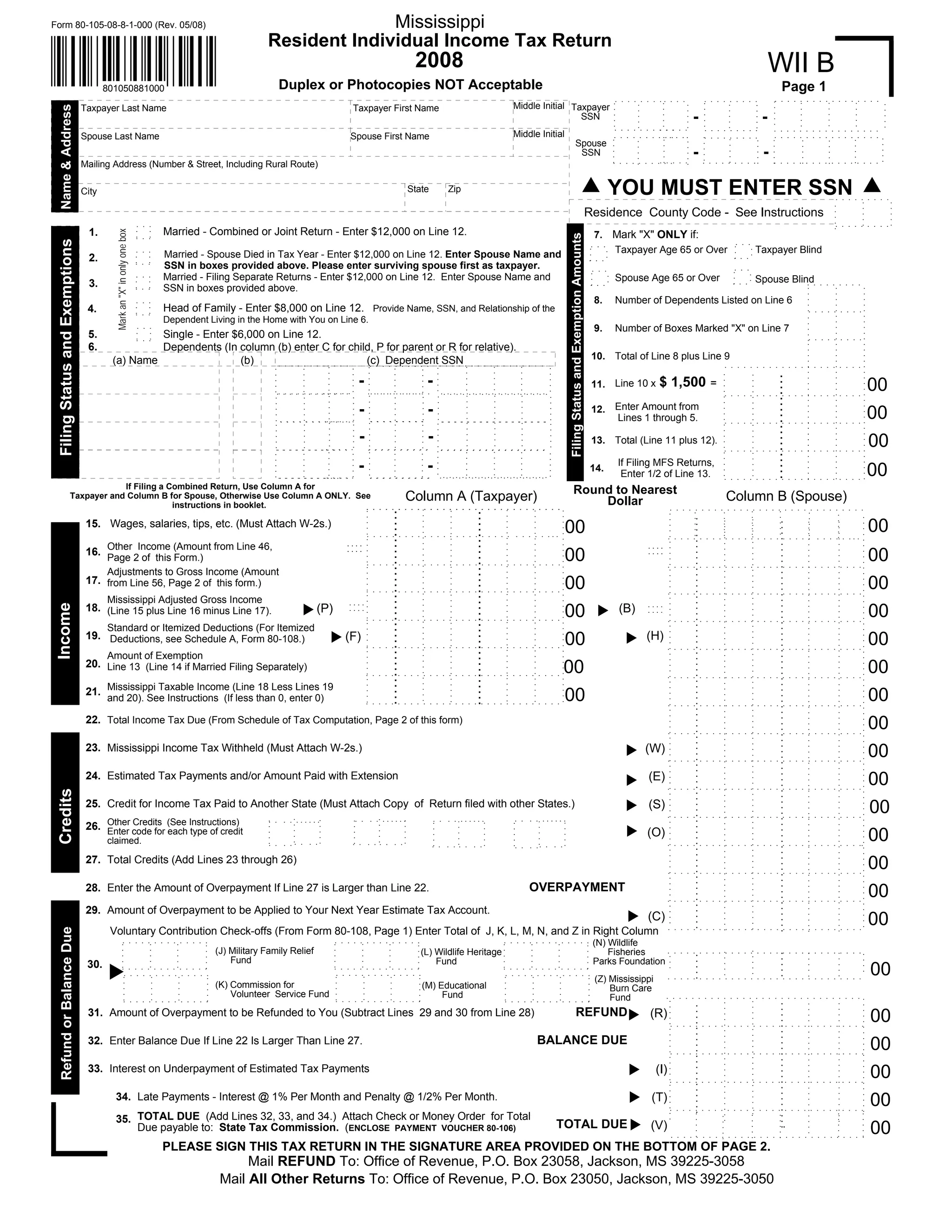

Resident Individual Income Tax Return

Business

◦

Technology

◦

Read more

1

Save

Share

Embed

Embed presentation

Download

Download to read offline

1

/ 2

2

/ 2

More Related Content

PDF

Employee's Claim for Credit for Excess WD/HC and Disability Contributions for...

by

taxman taxman

PPTX

evaluation 7

by

Luca Riccio

ODP

Media evaluation 2

by

siobhanwren24

DOC

Tax Relief for Tornado Victims

by

taxman taxman

PDF

118

by

Siounincid1982825

PDF

Logo for Asianet

by

thang.bdq

PDF

Nonresident Seller's Tax Declaration

by

taxman taxman

PDF

Request for Computer Data

by

taxman taxman

Employee's Claim for Credit for Excess WD/HC and Disability Contributions for...

by

taxman taxman

evaluation 7

by

Luca Riccio

Media evaluation 2

by

siobhanwren24

Tax Relief for Tornado Victims

by

taxman taxman

118

by

Siounincid1982825

Logo for Asianet

by

thang.bdq

Nonresident Seller's Tax Declaration

by

taxman taxman

Request for Computer Data

by

taxman taxman

Viewers also liked

PPTX

A2 media questionnaire analysis

by

07knappchr

PDF

Consumer Use Tax Form

by

taxman taxman

PDF

Small Business Guarantee Fee Credit

by

taxman taxman

PDF

LDR Affidavit of Fraudulent Refund Deposit for Married Filing Jointly Filing...

by

taxman taxman

PDF

Cleanweb Intro for Clean Tuesday Meet-up in Hong Kong

by

JackTownsend

PDF

Bbb

by

guest6117b631

PDF

No phone on the road

by

Boonlert Aroonpiboon

PDF

Rigo It En

by

ParadisoDellaCasa

PDF

NYC-E911 SURCHARGE Return of E-911 Surcharge by Telecommunication Providers

by

taxman taxman

PDF

L Panel 1

by

guest35ce498

A2 media questionnaire analysis

by

07knappchr

Consumer Use Tax Form

by

taxman taxman

Small Business Guarantee Fee Credit

by

taxman taxman

LDR Affidavit of Fraudulent Refund Deposit for Married Filing Jointly Filing...

by

taxman taxman

Cleanweb Intro for Clean Tuesday Meet-up in Hong Kong

by

JackTownsend

Bbb

by

guest6117b631

No phone on the road

by

Boonlert Aroonpiboon

Rigo It En

by

ParadisoDellaCasa

NYC-E911 SURCHARGE Return of E-911 Surcharge by Telecommunication Providers

by

taxman taxman

L Panel 1

by

guest35ce498

More from taxman taxman

PDF

ftb.ca.gov forms 09_3528a

by

taxman taxman

PDF

ftb.ca.gov forms 09_593bk

by

taxman taxman

PDF

ftb.ca.gov forms 09_593v

by

taxman taxman

PDF

ftb.ca.gov forms 09_593i

by

taxman taxman

PDF

ftb.ca.gov forms 09_593c

by

taxman taxman

PDF

ftb.ca.gov forms 09_593

by

taxman taxman

PDF

ftb.ca.gov forms 09_592v

by

taxman taxman

PDF

ftb.ca.gov forms 09_592b

by

taxman taxman

PDF

ftb.ca.gov forms 09_592a

by

taxman taxman

PDF

ftb.ca.gov forms 09_592

by

taxman taxman

PDF

ftb.ca.gov forms 09_590p

by

taxman taxman

PDF

ftb.ca.gov forms 09_590

by

taxman taxman

PDF

ftb.ca.gov forms 09_588

by

taxman taxman

PDF

ftb.ca.gov forms 09_587

by

taxman taxman

PDF

ftb.ca.gov forms 09_570

by

taxman taxman

PDF

ftb.ca.gov forms 09_541es

by

taxman taxman

PDF

ftb.ca.gov forms 09_540esins

by

taxman taxman

PDF

ftb.ca.gov forms 09_540es

by

taxman taxman

PDF

ftb.ca.gov forms 1240

by

taxman taxman

PDF

ftb.ca.gov forms 1015B

by

taxman taxman

ftb.ca.gov forms 09_3528a

by

taxman taxman

ftb.ca.gov forms 09_593bk

by

taxman taxman

ftb.ca.gov forms 09_593v

by

taxman taxman

ftb.ca.gov forms 09_593i

by

taxman taxman

ftb.ca.gov forms 09_593c

by

taxman taxman

ftb.ca.gov forms 09_593

by

taxman taxman

ftb.ca.gov forms 09_592v

by

taxman taxman

ftb.ca.gov forms 09_592b

by

taxman taxman

ftb.ca.gov forms 09_592a

by

taxman taxman

ftb.ca.gov forms 09_592

by

taxman taxman

ftb.ca.gov forms 09_590p

by

taxman taxman

ftb.ca.gov forms 09_590

by

taxman taxman

ftb.ca.gov forms 09_588

by

taxman taxman

ftb.ca.gov forms 09_587

by

taxman taxman

ftb.ca.gov forms 09_570

by

taxman taxman

ftb.ca.gov forms 09_541es

by

taxman taxman

ftb.ca.gov forms 09_540esins

by

taxman taxman

ftb.ca.gov forms 09_540es

by

taxman taxman

ftb.ca.gov forms 1240

by

taxman taxman

ftb.ca.gov forms 1015B

by

taxman taxman

Download