Download to read offline

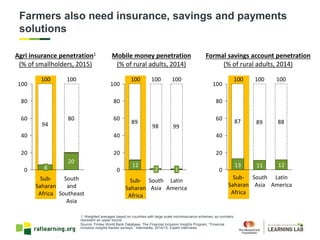

The document discusses partnerships between last mile firms (value chain actors and ag-focused technology companies) and financial institutions to increase access to finance for smallholder farmers. It provides examples of three partnerships: 1) Biopartenaire partners with Advans bank to provide savings products to cocoa farmers and outsource lending to reduce costs and risks. 2) Kifiya partners with multiple financial institutions and insurance companies to leverage its digital financial services platform and increase transaction volumes. 3) Prep-eez offers farmer data to multiple financial institutions to develop new products delivered through its platform, in order to increase farmer purchasing power.

![Presentation1[1].pptx JHAKShsHHHHHHHHHHHHHHHHHHH](https://cdn.slidesharecdn.com/ss_thumbnails/presentation11-240616122800-7ad0e6ef-thumbnail.jpg?width=640&height=640&fit=bounds)