Quadrant 4 Systems Corporation (OTC: QFOR; Twitter: $QFOR) - Taglish Brothers Report

•

1 like•368 views

Quadrant 4 Systems Corporation (OTC: QFOR; Twitter: $QFOR) is the next generation entrepreneurial project of a team of accomplished IT industry veterans. The principals have built technology business enterprises from start up, grown organically and exited after creating shareholder value. The principals of Quadrant 4 cumulatively bring over 5 decades of entrepreneurial, technical and management expertise that are core to the success of building its next generation Information Technology (IT) services business.

Recommended

Recommended

More Related Content

What's hot

What's hot (19)

Viewers also liked

Viewers also liked (20)

Similar to Quadrant 4 Systems Corporation (OTC: QFOR; Twitter: $QFOR) - Taglish Brothers Report

Similar to Quadrant 4 Systems Corporation (OTC: QFOR; Twitter: $QFOR) - Taglish Brothers Report (20)

More from ProActive Capital Resources Group

More from ProActive Capital Resources Group (20)

Recently uploaded

Recently uploaded (7)

Quadrant 4 Systems Corporation (OTC: QFOR; Twitter: $QFOR) - Taglish Brothers Report

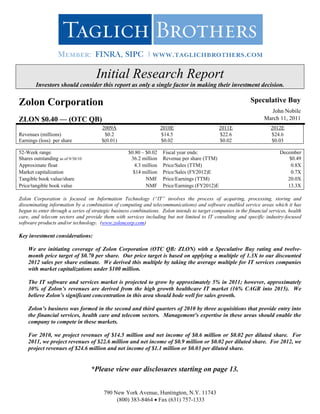

- 1. Initial Research Report Investors should consider this report as only a single factor in making their investment decision. Zolon Corporation Speculative Buy John Nobile ZLON $0.40 — (OTC QB) March 11, 2011 2009A 2010E 2011E 2012E Revenues (millions) $0.2 $14.5 $22.6 $24.6 Earnings (loss) per share $(0.01) $0.02 $0.02 $0.03 52-Week range $0.80 – $0.02 Fiscal year ends: December Shares outstanding as of 9/30/10 36.2 million Revenue per share (TTM) $0.49 Approximate float 4.3 million Price/Sales (TTM) 0.8X Market capitalization $14 million Price/Sales (FY2012)E 0.7X Tangible book value/share NMF Price/Earnings (TTM) 20.0X Price/tangible book value NMF Price/Earnings (FY2012)E 13.3X Zolon Corporation is focused on Information Technology (“IT” involves the process of acquiring, processing, storing and disseminating information by a combination of computing and telecommunications) and software enabled service areas which it has begun to enter through a series of strategic business combinations. Zolon intends to target companies in the financial services, health care, and telecom sectors and provide them with services including but not limited to IT consulting and specific industry-focused software products and/or technology. (www.zoloncorp.com) Key investment considerations: We are initiating coverage of Zolon Corporation (OTC QB: ZLON) with a Speculative Buy rating and twelve- month price target of $0.70 per share. Our price target is based on applying a multiple of 1.3X to our discounted 2012 sales per share estimate. We derived this multiple by taking the average multiple for IT services companies with market capitalizations under $100 million. The IT software and services market is projected to grow by approximately 5% in 2011; however, approximately 30% of Zolon’s revenues are derived from the high growth healthcare IT market (16% CAGR into 2015). We believe Zolon’s significant concentration in this area should bode well for sales growth. Zolon’s business was formed in the second and third quarters of 2010 by three acquisitions that provide entry into the financial services, health care and telecom sectors. Management’s expertise in these areas should enable the company to compete in these markets. For 2010, we project revenues of $14.5 million and net income of $0.6 million or $0.02 per diluted share. For 2011, we project revenues of $22.6 million and net income of $0.9 million or $0.02 per diluted share. For 2012, we project revenues of $24.6 million and net income of $1.1 million or $0.03 per diluted share. *Please view our disclosures starting on page 13. 790 New York Avenue, Huntington, N.Y. 11743 (800) 383-8464 Fax (631) 757-1333

- 2. Zolon Corporation Recommendation and Valuation We are initiating coverage of Zolon Corporation with a Speculative Buy rating. Recent acquisitions have positioned the company for growth in various IT services sectors including financial services, health care, and telecom. We are valuing shares of ZLON using a price/sales multiple on our 2012 sales estimate of $0.60 per share. The average multiple for IT services companies with market capitalizations under $100 million is 1.3X sales (excluding outliers). Applying a multiple of 1.3X to our 2012 sales value, we arrive at a price target of $0.78 per share. Discounting this value using a rate of 8% (derived by using the industry beta) gives us a twelve month price target of approximately $0.70 per share. History Headquartered in Rolling Meadows, Illinois, Zolon Corporation was incorporated in 1990 as Sun Express Group, Inc. for the purpose of obtaining air carrier certification. Several years later, the company decided to suspend its certification efforts and sell off its assets after which the company remained dormant until August, 2001, when it became involved in the motion picture industry. In June, 2005, current management completed a reverse acquisition with the company, changed its business focus to emerging technologies, (Voice over Internet Protocol “VoIP” and Closed Circuit Television “CCTV” security systems) replaced prior management and changed the company’s name to Aventura VoIP Networks, Inc. In December, 2009, the company changed its name to Zolon Corporation and in May 2010, the company changed its primary business model as described below. Business As a result of increasingly competitive markets in VOIP technology and CCTV, the company changed its business model to focus on Information Technology (IT) and software enabled service (combines proprietary software with service expertise) areas which it has begun to enter through a series of business combinations (as described below). Zolon intends to target companies in the financial services, health care, and telecom sectors and provide them with a services including but not limited to IT consulting (i.e. the upgrading of technology systems) and specific industry-focused software products and/or technology (i.e. the selling of software owned and created by Zolon). In the second and third quarters of 2010, Zolon acquired the following three companies from StoneGate Holdings: 1) VSG Acquisition Corp, 2) Resource Mine Acquisition Corp, and 3) Integrated Software Solutions, Inc. VSG Acquisition Corp is an IT consulting firm to multiple industries specializing in Java. Java is one of the most popular programming languages in use and is widely used from application software to web applications. VSG Acquisition Corp also is involved with .NET and Sharepoint technologies. .NET is a software framework intended to be used by most new applications created for the Windows platform. Sharepoint is a Web technology based server that can be used to build portals, coloration sites, and content management sites; it also includes a family of software products developed by Microsoft for collaboration, file sharing, and Web publishing. Resource Mine Acquisition Corp is a provider of architecture and development services for the financial services industry. Integrated Software Solutions, Inc. is a provider of custom software for global financial services providers, healthcare providers, and software and services companies. The three acquisitions provided over 150 clients to the company. In connection with the above acquisitions, Zolon issued 32.0 million shares of its common stock to StoneGate Holdings. Taglich Brothers, Inc. 2

- 3. Zolon Corporation Information Technology Overview The proliferation of smaller and less expensive personal computers and improvements in computing power in the early 1980s resulted in the sudden access and ability to share and store information for more and more workers. Connectivity between computers within companies led to the ability of workers at different levels to access greater amounts of information. In the 1990s, the spread of the Internet caused a sudden leap in access and ability to share information in businesses, at home and around the globe. Eventually, Information and Communication Technology—computers, computerized machinery, fiber optics, communication satellites, Internet, and other tools—became a significant part of the economy. Information Technology (IT) involves the process of acquiring, processing, storing and disseminating vocal, pictorial, textual and numerical information by a microelectronics-based combination of computing and telecommunications. IT is the area of managing technology and spans a wide variety of areas that include but are not limited to things such as processes, computer software, information systems, computer hardware, programming languages, and data constructs. In short, anything that renders data, information or perceived knowledge in any visual format whatsoever, via any multimedia distribution mechanism, is considered part of the domain space known as Information Technology. IT professionals perform a variety of functions that range from installing applications to designing complex computer networks and information databases. A few of the duties that IT professionals perform may include data management, networking, engineering computer hardware, database and software design, as well as management and administration of entire systems. Information technology is starting to spread farther than the conventional personal computer and network technology, and more into integrations of other technologies such as the use of cell phones, televisions, automobiles, and more, which is increasing the demand for such jobs. Market The following insights and forecasts relate specifically to the markets that Zolon operates in. Expectations are for the company to generate approximately 5% of total revenues from cloud computing projects, 30% from healthcare IT projects, and the remainder from the overall IT services and software market. IT spending in the United States has risen steadily over the past few decades as shown by the following chart. Although IT spending declined in 2009, new opportunities such as cloud computing suggest that the dip will be short lived. (Cloud computing is a style of computing in which services and storage are provided as a service to external customers using Internet technologies.) Taglich Brothers, Inc. 3

- 4. Zolon Corporation According to the market research firm International Data Corporation (IDC), global spending on information technology in 2010 surged to its fastest rate of growth since 2007, driven by pent-up demand for hardware upgrades and infrastructure investment after the financial crisis and global recession of 2009. IDC expects the pace of recovery to accelerate in 2011 with investments in new IT projects (including rapid adoption of cloud computing) driving that growth. IDC projects the overall IT market to grow by 7% in 2011 to $1.65 trillion with another year of double-digit growth for hardware spending (10%), while software and services markets will increase by 5% and 4% respectively. The top strategic technology for 2011 according to Gartner is in the area of cloud computing. Gartner defines a strategic technology as one with the potential for significant impact on the enterprise in the next three years. According to the global markets research firm MarketsandMarkets, the global cloud computing market is expected to grow from $37.8 billion in 2010 to $121.1 billion in 2015 for a compound annual growth rate of 26.2%. MarketsandMarkets said that cloud computing not only reduces costs, but also makes applications accessible from any location, and reacts swiftly to changes in business needs. IDC forecasts that from 2009 to 2014, U.S. public IT cloud services revenue will grow 21.6%, from $11.1 billion to $29.5 billion. The services and distribution sector – which includes vertical markets such as retail, wholesale, professional services, consumer and recreational services, and transportation – contributes the largest share of U.S. public IT cloud services revenue. Currently a $3 billion market, IDC estimates that it will more than double to $8.5 billion by 2014. Another area of high growth is expected to come from healthcare information technology spending. MarketsandMarkets estimates that global healthcare IT spending will exceed $25 billion by 2015 for a compound annual growth rate of more than 16% with electronic medical records (EMR) development driving this growth. Rising demand for healthcare cost containment and the need to improve the quality of healthcare service are driving the growth of the worldwide EMR market. MarketsandMarkets projects the global EMR market to grow from $4.355 billion in 2009 to $9.957 billion in 2015 for a compound annual growth rate of 14.9%. Competition and Strategy Zolon operates in industries which are highly competitive. The market includes a large number of well- capitalized competitors that have extensive experience, established distribution channels and facilities. The IT services market has a large number of participants and is segmented itself into several sectors, which include consulting, application software, and equipment companies to name just a few. Direct competitors include, among others, many tier 1 service providers such as Accenture (NYSE: ACN), IBM Global Services (NYSE: IBM), and Cap Gemini (OTC: CGEMY) at the global level and numerous small and boutique consulting shops at the local level. Key principal competitive factors affecting these market sectors are: size and strength of the balance sheet, credibility and performance, track record and reliability, quality of personnel, and competitive pricing. Based on their backgrounds, management’s expertise in the financial services, health care and telecom sectors should allow the company to effectively compete in these particular markets. Zolon’s growth strategy is to build the company through strategic acquisitions, to focus on organic growth through additional revenue from existing clients and adding new clients, and to grow into new markets such as infrastructure management, identity management, product engineering, business intelligence, internet security, enterprise mobility, and business and knowledge process outsourcing. Taglich Brothers, Inc. 4

- 5. Zolon Corporation Infrastructure management is the management of essential operation components, such as policies, processes, equipment, data, human resources, and external contacts, for overall effectiveness. Identity management deals with identifying individuals in a system (such as a network or organization) and controlling access to the resources in that system by placing restrictions on the established identities of the individuals). Business intelligence refers to computer-based techniques used in identifying and analyzing business data, such as sales revenue by products and/or departments, or by associated costs and incomes. Enterprise mobility involves the management of an increasing array of mobile devices, wireless networks, and related services. Business process outsourcing involves the contracting of the operations and responsibilities of specific business functions (or processes) to a third-party service provider. Financial Results Sales for the three months ended September 30, 2010 were $5.1 million compared to $32,000 in the comparable period in 2009. Net income was $180,000 or $0.00 per diluted share for the three months ended September 30, 2010 as compared to a net loss of $12,000 or $(0.00) per share . During 2010, the company acquired three business entities with established customers. The revenue generated for the third quarter of 2010 increased over the prior year due to the consulting income received from these newly acquired business entities. The $32,000 of income reported in the third quarter of 2009 is fee income. There was no fee income in the third quarter of 2010 due to the change in the company’s business model. Cost of revenue for the three months ended September 30, 2010 was $4.4 million compared to year earlier cost of revenue of zero. The increase in cost of revenue is due to the company’s acquisition of three business entities during 2010 which consists primarily of direct labor costs of employees providing consulting services. Selling, general & administrative (SG&A) expenses for the three months ended September 30, 2010 were $310,000 compared to $45,000 in the year earlier period. The increase was due to the company’s acquisition of three business entities during 2010. Interest expense was $314,000 for the three months ended September 30, 2010 compared to zero in the year earlier period. The increase was a result of interest expense incurred from borrowings against accounts receivables and short term debt financing. Sales for the nine months ended September 30, 2010 were $9.5 million compared to $144,000 in the comparable period in 2009. Net income was $422,000 or $0.01 per diluted share for the nine months ended September 30, 2010 as compared to a net loss of $13,000 or $(0.00) per share in the year earlier period. During 2010, the company acquired three business entities with established customers. The revenue generated for the nine months of 2010 increased over the prior year due to the consulting income received from these newly acquired business entities. Cost of revenue for the nine months ended September 30, 2010 was $8.0 million compared to $59,000 for the year earlier period. The increase in cost of revenue is due to the company’s acquisition of three business entities during 2010 which consists primarily of direct labor costs of employees providing consulting services. Selling, general & administrative (SG&A) expenses for the nine months ended September 30, 2010 were $0.5 million compared to $98,000 in the year earlier period. The increase was due to the company’s acquisition of three business entities during 2010. Interest expense was $0.5 million for the nine months ended September 30, 2010 compared to zero in the year earlier period. The increase was a result of interest expense incurred from borrowings against accounts receivables and short term debt financing. Taglich Brothers, Inc. 5

- 6. Zolon Corporation 9mos2009 9mos2010 Revenue 144 9,519 Cost of revenue 59 8,027 Gross profit 85 1,492 SG&A 98 529 Operating income (13) 963 Interest expense - 541 Net Income / (Loss) (13) 422 Basic EPS (0.00) 0.01 Diluted EPS (0.00) 0.01 Basic Shares Outstanding 3,150 35,400 Diluted Shares Outstanding 3,150 35,400 Margin Analysis Gross margin 59.0% 15.7% SG&A 68.1% 5.6% Operating margin -9.0% 10.1% Net margin -9.0% 4.4% Source: Company filings Liquidity As of September 30, 2010, the company exhibited liquidity issues as evidenced by current liabilities exceeding current assets by $2.9 million and an accumulated deficit of $0.7 million. The company had cash earnings of $430,000 for the nine months ended September 30, 2010. Notes payable and other current liabilities increased by $7.7 million which was offset in part by a $5.0 million increase in accounts receivable. Cash provided by operations for the nine months was $3.3 million. A $5.9 million increase in goodwill, $2.2 million proceeds from the issuance of stock and $0.5 million proceeds from the issuance of debt resulted in a net decrease in cash of $15,000 for a negative cash balance of $(14,000) at September 30, 2010. Subsequent to Q3/10, the company sold 5.1 million shares of its common stock at $0.30 per share and issued an equal amount of warrants for proceeds of $1.53 million. The warrants were priced at twice the price for the common stock. The company has no material commitments for capital expenditures and relies upon outside entities to finance its operations. Cloud-based Solution to Launch in Financial Services Market In March 2011, the company announced it acquired the rights to EXIS Consulting’s Genesis Capital Markets technology. Zolon intends to adapt the Genesis product to a Cloud-based service that will be marketed to financial institutions. Taglich Brothers, Inc. 6

- 7. Zolon Corporation Projections We project revenues over the next two years will grow at an annual rate of approximately 9% from the current annualized level ($20.7 million taking the latest quarter and annualizing it) barring any further acquisitions. We derived this rate by taking the weighted average of the estimated growth rates of the specific industries that the company operates in. Expectations are for the company to generate approximately 5% of total revenues from cloud computing projects, 30% from healthcare IT projects, and the remainder from the overall IT services and software market. We applied a 5% weight to the cloud computing growth rate of 24% (average growth rate projection from MarketsandMarkets and IDC), a 30% weight to the healthcare IT growth rate of 16% (growth rate projection from MarketsandMarkets), and a 65% weight to the overall software and services market growth rate of approximately 5% (growth rate projection from IDC). We project 2010 revenues of $14.5 million and net income of $0.6 million or $0.02 per diluted share. The company’s current gross margins of 15.5% should be sustainable. We project increased business will result in SG&A expenses of $0.8 million in 2010. Current interest expense should approximate $0.9 million in 2010. We project 2011 revenues of $22.6 million and net income of $0.9 million or $0.02 per diluted share. Gross margins are projected to remain at 15.5% while increased business should result in SG&A expenses of $1.4 million in 2011. With no further debt, interest expense should be $1.2 million in 2011. We project 2012 revenues of $24.6 million and net income of $1.1 million or $0.03 per diluted share. Gross margins are projected to remain at 15.5% while increased business should result in SG&A expenses of $1.5 million in 2012. Interest expense is projected to continue at $1.2 million in 2012. We project that the allowance for bad debt throughout our forecast horizon will increase in proportion to sales. Based on our projections, we believe the company will have sufficient cash flow to fund operations through 2012. For 2010, we project cash earnings of $0.6 million. A $1.9 million decrease in working capital, $6.0 million increase in goodwill, and $4.2 million proceeds from the issuance of securities should result in a $0.7 million net increase in cash to $0.7 million in 2010. For 2011, we project cash earnings of $0.9 million. A $2.8 million decrease in working capital and debt repayments of $3.6 million should result in a $0.1 million net increase in cash to $0.7 million in 2011. For 2012, we project cash earnings of $1.1 million. A $2.5 million decrease in working capital and debt repayments of $3.6 million should result in virtually no change to the net cash position for an ending balance of $0.7 million in 2012. Management Dhru Desai, Chairman of the Board and Chief Financial Officer - Built both private and public companies in the IT and telecommunications field over the past 25 years. Worked for AT&T Bell Labs and Teradyne. Founder and CEO of Cronus Technologies, Inc. where he built the industries’ first IP signaling gateway business and divested it to Cisco, FastCom and Advanced Fiber. In April 2005, served as chairman of the board of eNucleus Inc. and in several executive capacities until he resigned in July, 2006. Between July 2006 and June 2009, acted in the capacity of an advisor to a number of companies in the real estate and Information Technology sectors. M.S. in Computer Science from Illinois Institute of Technology. Taglich Brothers, Inc. 7

- 8. Zolon Corporation Nandu Thondavadi, Ph. D.; Chief Executive Officer - Founder of Global Technology Ventures, a consulting firm providing mergers and acquisition advisory services to companies in the information technology sector. Served in various roles from software development to heading a global IT firm with companies such as EDS, Square D, Coleman and others. Served as the Clinical Professor of Management at the Kellogg School of Management, Northwestern University, IL where he developed and taught graduate courses in Operations Management, Total Quality Management, Enterprise Resource Systems and also developed and taught executive programs in Strategic Cost Management and Business Process Reengineering. MBA from Northwestern University, Kellogg School of Management, IL; Ph.D. in Chemical Engineering; and M.S. in Industrial Engineering, both from the University of Cincinnati, OH, M.Sc. (Tech) and B.Sc. (Tech) both in Chemical Technology and both from the University of Bombay, Mumbai, India; B.Sc. in Chemistry and Physics from the University of Mysore, India. Bhushan Dandawate, Executive Vice President - Over 20 years, built, grown and managed companies in the IT, engineering services, telecom and other sectors. Created and built a new $150M division whose delivery capabilities span across the globe. As managing director of $35 Billion global conglomerate, led the group’s entry and successful endeavors into the US markets. Advanced degree in engineering as well as an MBA from University of Michigan’s Ross School of Business. Risks ZLON is suitable mainly for highly risk tolerant investors. In our view, careful consideration should be given to the following risk factors before deciding to make an investment in the company’s common stock. The markets in which Zolon operates are highly competitive. Some principal competitors may have significantly greater resources and larger customer bases than Zolon does. Price reductions by some of Zolon’s competitors are expected to continue putting pressure on gross margins. Unfavorable economic and market conditions and reduced IT spending may lead to decreased demand for the company’s services. The company may be experiencing collectibility issues as evidenced by the over $1 million allowance for bad debt (approximately 17% of accounts receivable) as of September 30, 2010. Zolon sells its services throughout the world and intends to penetrate international markets. Future results could be materially adversely affected by a variety of factors including changes in exchange rates, general economic conditions, regulatory requirements, tax structures or changes in tax laws, and longer payment cycles. Zolon has limited experience relating to the establishment of new business relationships including contracts with customers. Zolon has limited assets which may limit the company’s ability to take advantage of business relationships and opportunities. Zolon may have to issue securities, sometimes at prices substantially below market price, for acquisitions or for services or in order to pay off its debts. Such financing may depress the stock price and dilute the holdings of shareholders. Shares of ZLON have risks common to those of the microcap segment of the market. Often these risks cause microcap stocks to trade at discounts to their peers. The most common of these risks is liquidity risk, which is typically caused by small trading floats and very low trading volume and can lead to large spreads and high volatility in stock price. According to the company, there are 4.3 million shares in the float. Average daily volume is approximately 21,500 shares. The company's financial results and equity values are subject to other risks and uncertainties known and unknown, including but not limited to competition, operations, financial markets, regulatory risk, and/or other events. These risks may cause actual results to differ from expected results. Taglich Brothers, Inc. 8

- 9. Zolon Corporation Consolidated Balance Sheets (in thousands $) 2009A 9/10A 2010E 2011E 2012E Assets Current assets: Cash 1 (14) 660 747 718 Accounts receivable - 6,009 6,009 6,278 6,833 Allowance for bad debt - (1,015) (1,015) (1,100) (1,200) Other current assets - (4) (4) (4) (4) Total current assets 1 4,976 5,650 5,921 6,348 Fixed assets 26 - - - - Goodwill - 5,912 5,912 5,912 5,912 Other - 83 83 83 83 Total assets 27 10,971 11,645 11,916 12,343 Liabilities & stockholders' equity Current liabilities: Accounts payable - 222 222 265 289 Accrued compensation - 378 378 378 378 Payable to seller - 621 - - Other 10 313 313 313 313 Accrued interest - 27 27 27 27 Current portion of notes payable 22 3,418 3,618 3,600 3,600 Accounts receivable factoring - 2,899 2,250 1,700 1,100 Total current liabilities 32 7,878 6,808 6,283 5,707 Long-term liabilities - 500 500 500 500 Total liabilities 32 8,378 7,308 6,783 6,207 Total stockholders' equity (deficit) (5) 2,593 4,337 5,133 6,136 Total liabilities & stockholders' equity 27 10,971 11,645 11,916 12,343 Source: Company filings and Taglich Brothers' estimates Taglich Brothers, Inc. 9

- 10. Zolon Corporation Income Statements for the Fiscal Years Ended (in thousands $) 2008A 2009A 2010E 2011E 2012E Revenue 304 169 14,520 22,600 24,600 Cost of revenue 117 59 12,252 19,097 20,787 Gross profit 187 110 2,268 3,503 3,813 SG&A 126 140 829 1,350 1,470 Operating income 61 (30) 1,439 2,153 2,343 Interest expense - - 851 1,240 1,240 Net Income / (Loss) 61 (30) 588 913 1,103 EPS 0.02 (0.01) 0.02 0.02 0.03 Shares Outstanding 2,790 2,922 28,288 41,250 41,250 Margin Analysis Gross margin 61.5% 65.1% 15.6% 15.5% 15.5% SG&A 41.4% 82.8% 5.7% 6.0% 6.0% Operating margin 20.1% -17.8% 9.9% 9.5% 9.5% Net margin 20.1% -17.8% 4.0% 4.0% 4.5% Year / Year Growth Total Revenues -44.4% NMF 55.6% 8.8% Net Income -149.2% NMF 55.3% 20.8% EPS -147.0% NMF 6.5% 20.8% Source: Company filings and Taglich Brothers' estimates Taglich Brothers, Inc. 10

- 11. Zolon Corporation Taglich Brothers, Inc. 11

- 12. Zolon Corporation Statement of Cash Flows for the Periods Ended (in thousands $) 2009A 9mos2010A 2010E 2011E 2012E Cash Flows from Operating Activities Net income (loss) (31) 430 588 913 1,103 Depreciation 5 - - - - Changes in assets and liabilities Accounts receivable - (4,994) (6,009) (269) (556) Other current assets - 4 4 - - Prepaid expense - - - - - Security deposit 5 - - - - Accounts payable (17) 221 222 43 23 Accrued expenses (45) - - - - Notes payable and other - 7,656 7,656 3,000 3,000 Net Cash Provided by (Used in) Operations (83) 3,317 2,461 3,687 3,571 Cash Flows from Investing Activities Change in other assets (goodwill) - (5,995) (5,995) - - Disposition of fixed assets - (6) (6) - - Net Cash Provided by (Used in) Investing - (6,001) (6,001) - - Cash Flows from Financing Activities Proceeds from share issuance 80 2,169 3,700 - - Proceeds from debt issuance - 500 500 - - Payments of debt - - - (3,600) (3,600) Net Cash Provided by (Used in) Financing 80 2,669 4,200 (3,600) (3,600) Net Change in Cash (3) (15) 660 87 (29) Cash - Beginning of Period 3 1 - 660 747 Cash - End of Period - (14) 660 747 718 Source: Company filings and Taglich Brothers' estimates Taglich Brothers, Inc. 12

- 13. Zolon Corporation Price Chart Taglich Brothers’ Current Ratings Distribution Investment Banking Services for Companies Covered in the Past 12 Months Rating # % Buy Hold None Sell Not Rated Taglich Brothers, Inc. 13

- 14. Zolon Corporation Important Disclosures As of the date of this report, we, our affiliates, any officer, director or stockholder, or any member of their families do not have a position in the stock of the company mentioned in this report. Taglich Brothers, Inc. does not currently have an Investment Banking relationship with the company mentioned in this report and was not a manager or co-manager of any offering for the company within the last three years. All research issued by Taglich Brothers, Inc. is based on public information. The company paid a monetary fee of $5,250 (USD) in January 2011 for the creation and dissemination of research reports for the first three months. After the first three months of publication, the company will pay a monthly monetary fee of $1,750 (USD) for a minimum of twelve months to Taglich Brothers, Inc., for the creation and dissemination of research reports. General Disclosures The information and statistical data contained herein have been obtained from sources, which we believe to be reliable but in no way are warranted by us as to accuracy or completeness. We do not undertake to advise you as to changes in figures or our views. This is not a solicitation of any order to buy or sell. Taglich Brothers, Inc. is fully disclosed with its clearing firm, Pershing, LLC, is not a market maker and does not sell to or buy from customers on a principal basis. The above statement is the opinion of Taglich Brothers, Inc. and is not a guarantee that the target price for the stock will be met or that predicted business results for the company will occur. There may be instances when fundamental, technical and quantitative opinions contained in this report are not in concert. We, our affiliates, any officer, director or stockholder or any member of their families may from time to time purchase or sell any of the above-mentioned or related securities. Analysts and members of the Research Department are prohibited from buying or selling securities issued by the companies that Taglich Brothers, Inc. has a research relationship with, except if ownership of such securities was prior to the start of such relationship, then an Analyst or member of the Research Department may sell such securities after obtaining expressed written permission from Compliance. Analyst Certification I, John Nobile, the research analyst of this report, hereby certify that the views expressed in this report accurately reflect my personal views about the subject securities and issuers; and that no part of my compensation was, is, or will be, directly, or indirectly, related to the specific recommendations or views contained in this report. Public companies mentioned in this report: Accenture (NYSE: ACN) Cap Gemini (OTC: CGEMY) IBM Global Services (NYSE: IBM) Taglich Brothers, Inc. 14

- 15. Zolon Corporation Meaning of Ratings Buy We believe the company is undervalued relative to its market and peers. We believe its risk reward ratio strongly advocates purchase of the stock relative to other stocks in the marketplace. Remember, with all equities there is always downside risk. Speculative Buy We believe that the long run prospects of the company are positive. We believe its risk reward ratio advocates purchase of the stock. We feel the investment risk is higher than our typical “buy” recommendation. In the short run, the stock may be subject to high volatility and continue to trade at a discount to its market. Neutral We will remain neutral pending certain developments. Underperform We believe that the company may be fairly valued based on its current status. Upside potential is limited relative to investment risk. Sell We believe that the company is significantly overvalued based on its current status. The future of the company's operations may be questionable and there is an extreme level of investment risk relative to reward. Some notable Risks within the Microcap Market Stocks in the Microcap segment of the market have many risks that are not as prevalent in Large-cap, Blue Chips or even Small-cap stocks. Often it is these risks that cause Microcap stocks to trade at discounts to their peers. The most common of these risks is liquidity risk, which is typically caused by small trading floats and very low trading volume which can lead to large spreads and high volatility in stock price. In addition, Microcaps tend to have significant company specific risks that contribute to lower valuations. Investors need to be aware of the higher probability of financial default and higher degree of financial distress inherent in the microcap segment of the market. From time to time our analysts may choose to withhold or suspend a rating on a company. We continue to publish informational reports on such companies; however, they have no ratings or price targets. In general, we will not rate any company that has too much business or financial uncertainty for our analysts to form an investment conclusion, or that is currently in the process of being acquired. Taglich Brothers, Inc. 15