Downloaded 14 times

![ReferencesReferences

Business and it audit [Web Graphic]. Retrieved from

http://www.boundlessllc.com/images/Audit_27.jpg

Compliance [Web Graphic]. Retrieved from

https://www.atcoresystems.com/sugarcrm-

images/compliance_sugarcrm_atcore_systems.jpg

Corporate governance [Web Graphic]. Retrieved from

http://www.insecticidesindia.com/images/corporate-

governance.jpg

Goldberg, M. IT Security Auditing [PowerPoint slides]. Retrieved

from https://www.google.com/url?

sa=t&rct=j&q=&esrc=s&source=web&cd=11&cad=rja&uact=8&ve

d=0CKQBEBYwCg&url=https%3A%2F%2Fisis.poly.edu

%2Fcourses%2Fcs996-management-s2005%2FLectures

%2Fsecurity

%2520audit.ppt&ei=LIyTU9_qJNTNsQT_n4CQCg&usg=AFQjCNEw

Yf2W68P7jNw9J6DzJxNirMhLDw&sig2=2JrsyrbmWZ_4s1xhQeOVz

A&bvm=bv.68445247,d.cWc](https://image.slidesharecdn.com/8171dc4b-ad83-480d-9cc9-25d8a6ab29db-151118043835-lva1-app6892/75/Project_Paper_Presentation_ISSC471_Intindolo-13-2048.jpg)

![References Cont’d.References Cont’d.

Jackson, R. (2013). Internal audit in 2020. Retrieved from

http://www.theiia.org/intAuditor/feature-

articles/2013/december/internal-audit-in-2020/

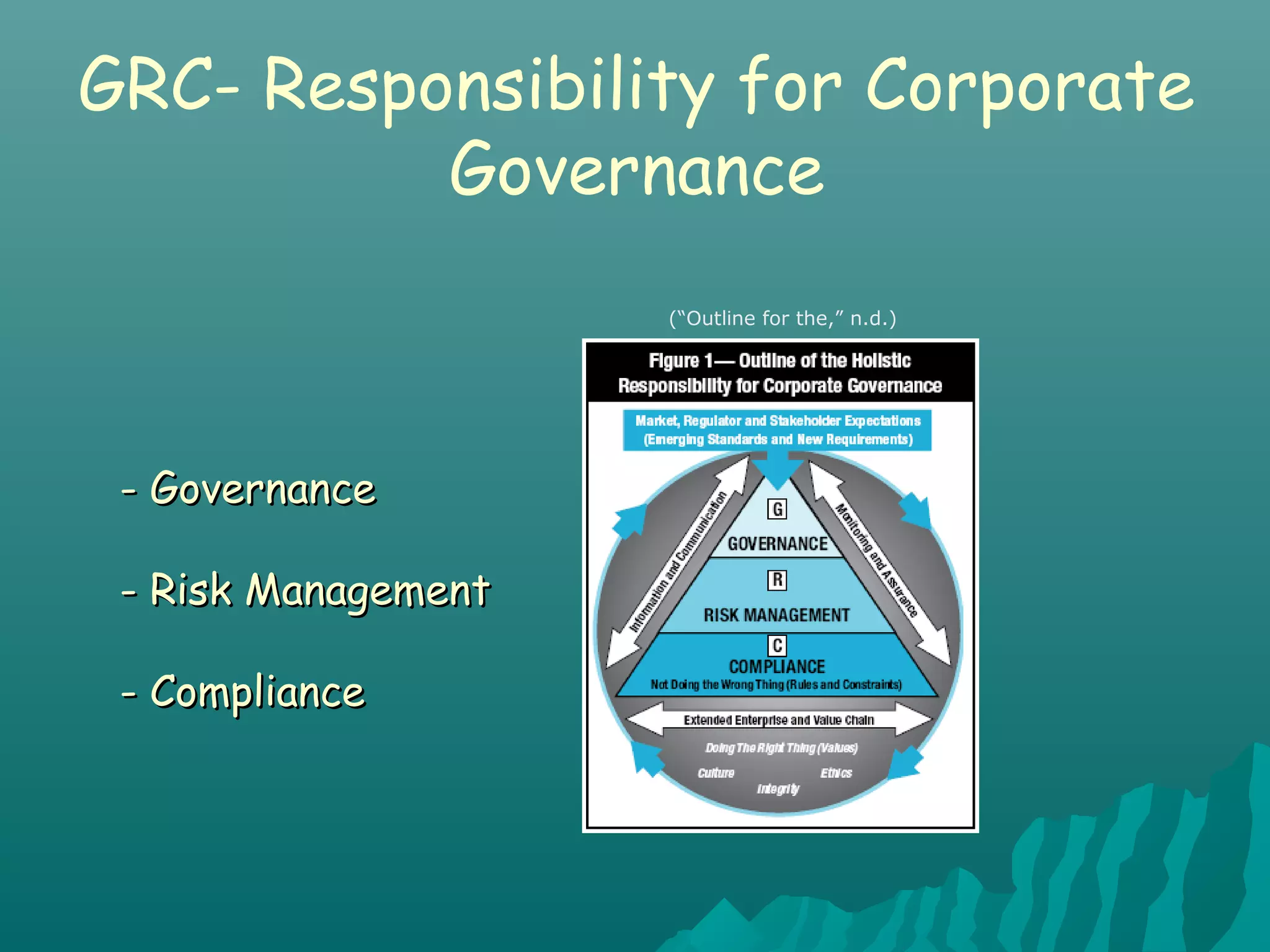

Outline of the holistic responsibility for corporate governance

[Web Graphic]. Retrieved from

http://www.isaca.org/Images/journal/j0905-complinace-mgt1.gif

Quiet please compliance person at work [Web Graphic]. Retrieved

from

http://hipaanews.net/files/2010/10/quiet_please_compliance_per

son_at_work_tshirt-p2359222439750942623gdm_400-

300x300.jpg

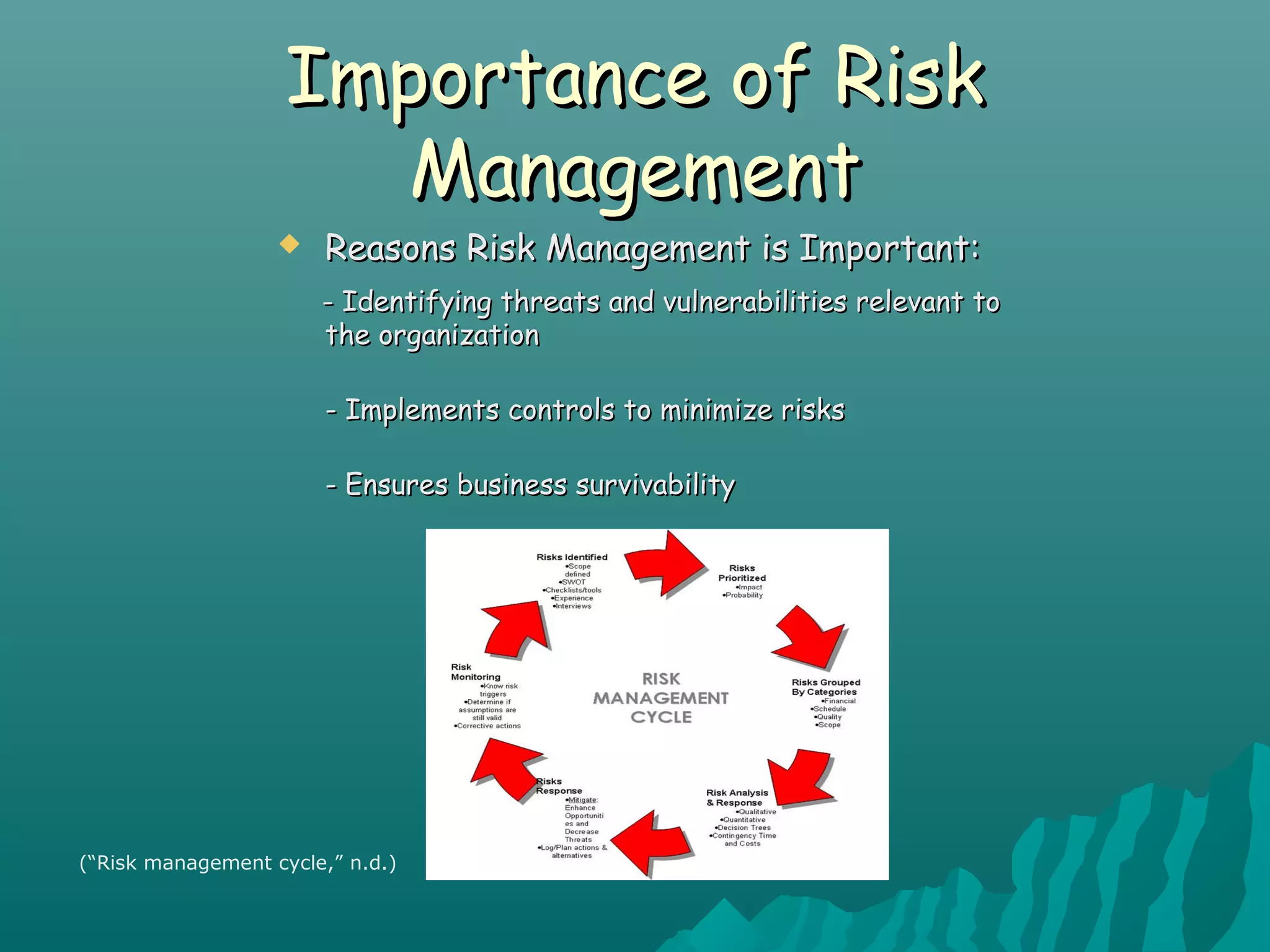

Risk management cycle [Web Graphic]. Retrieved from

http://www.pharmadirections.com/images/Headers and

Graphics/riskmanagement.jpg

Sun, L. (n.d.). Why is corporate governance important. Retrieved

from http://www.businessdictionary.com/article/618/why-is-

corporate-governance-important/](https://image.slidesharecdn.com/8171dc4b-ad83-480d-9cc9-25d8a6ab29db-151118043835-lva1-app6892/75/Project_Paper_Presentation_ISSC471_Intindolo-14-2048.jpg)

An IT security audit is an independent analysis of a company's IT system controls, policies, and procedures to evaluate their adequacy and ensure compliance. The document discusses the importance of governance, risk management, and compliance for IT security audits. It also outlines the audit process, future trends including a focus on risk and analytics, and regulatory issues concerning frameworks, cybersecurity, and auditing standards.