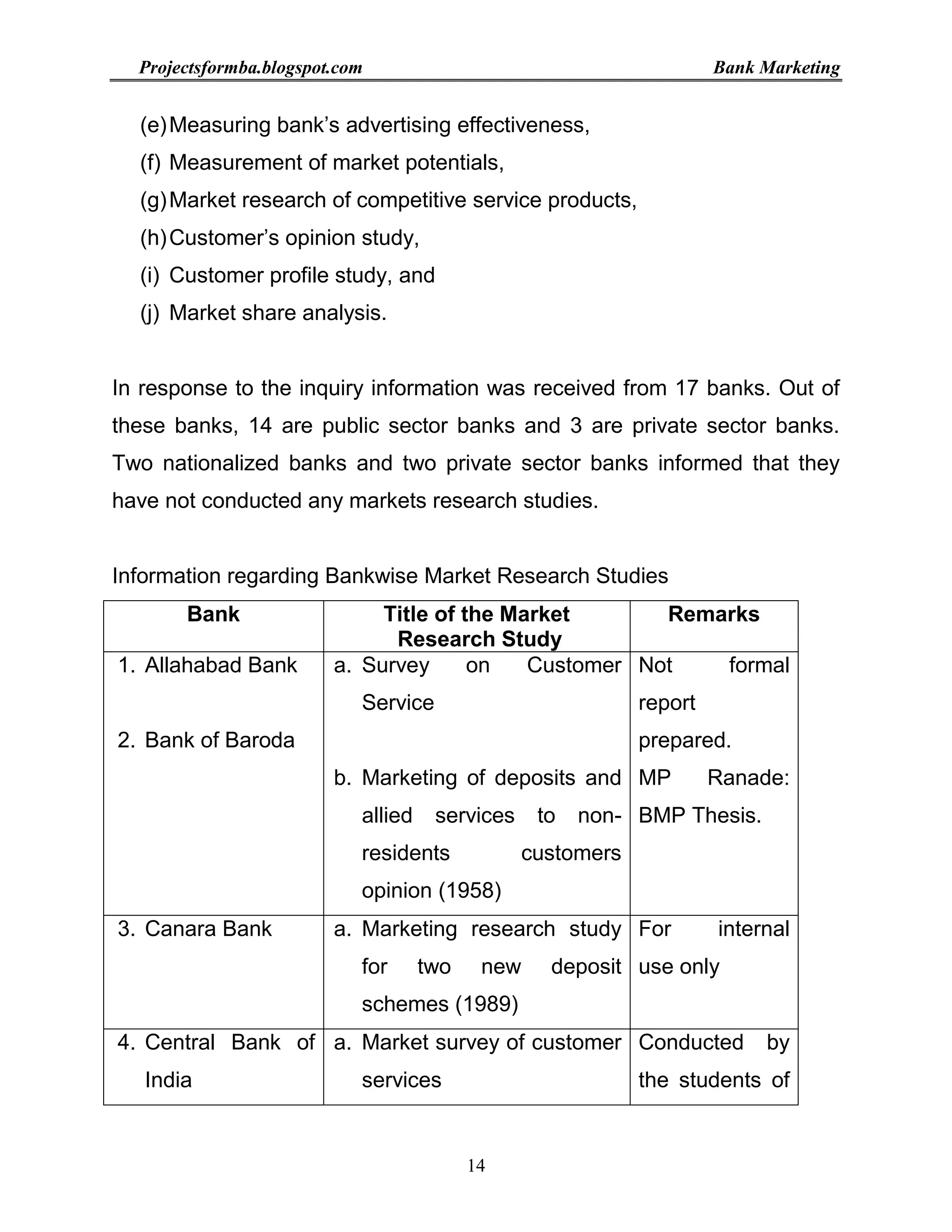

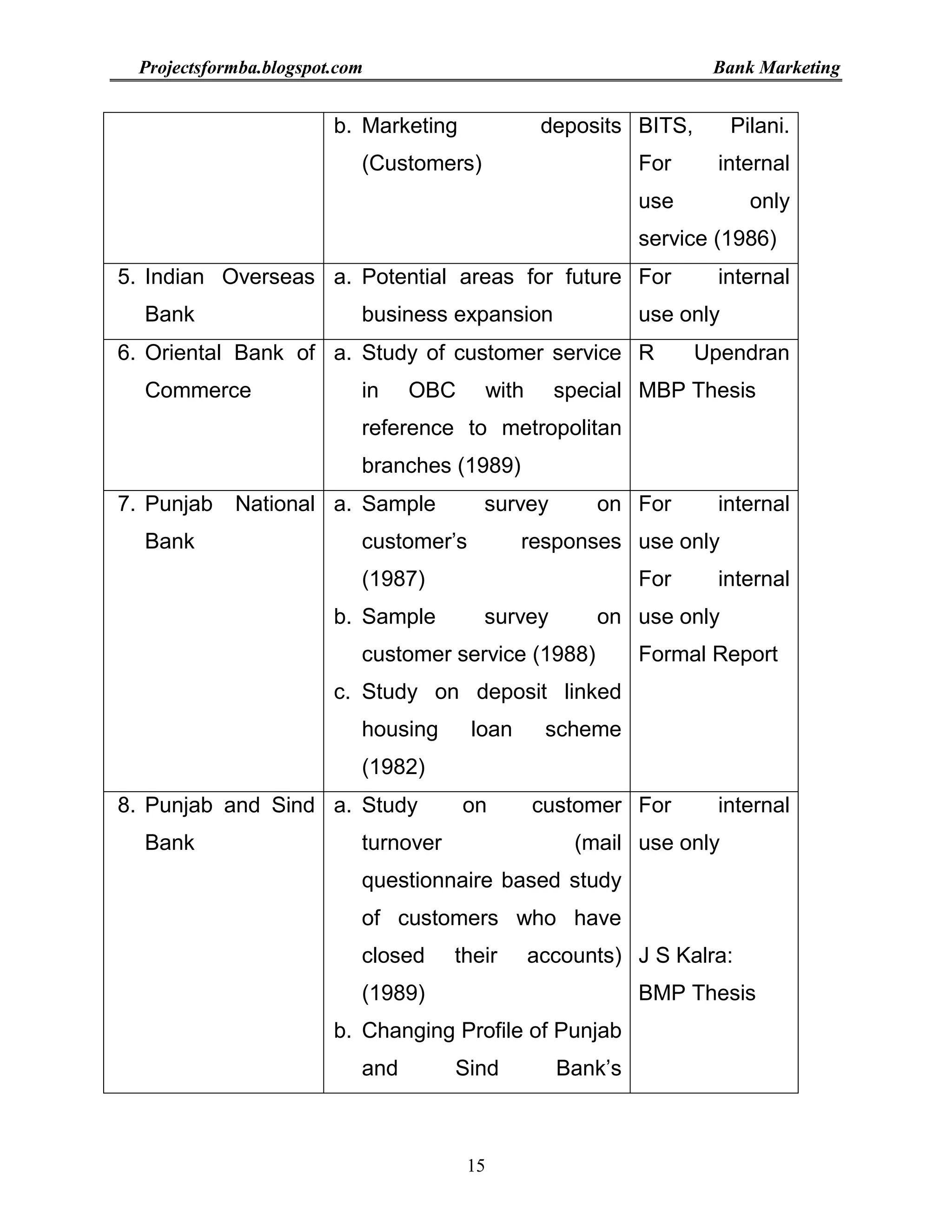

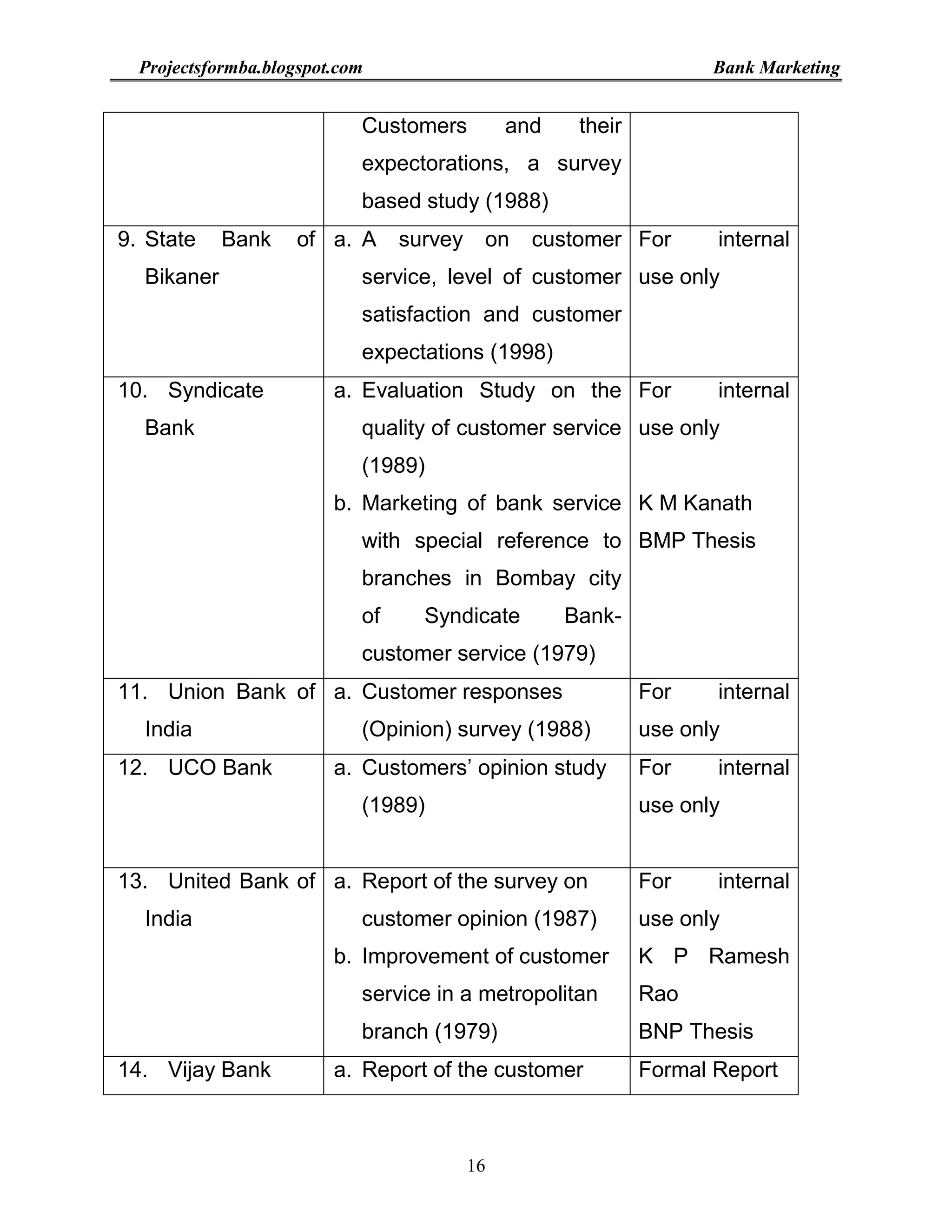

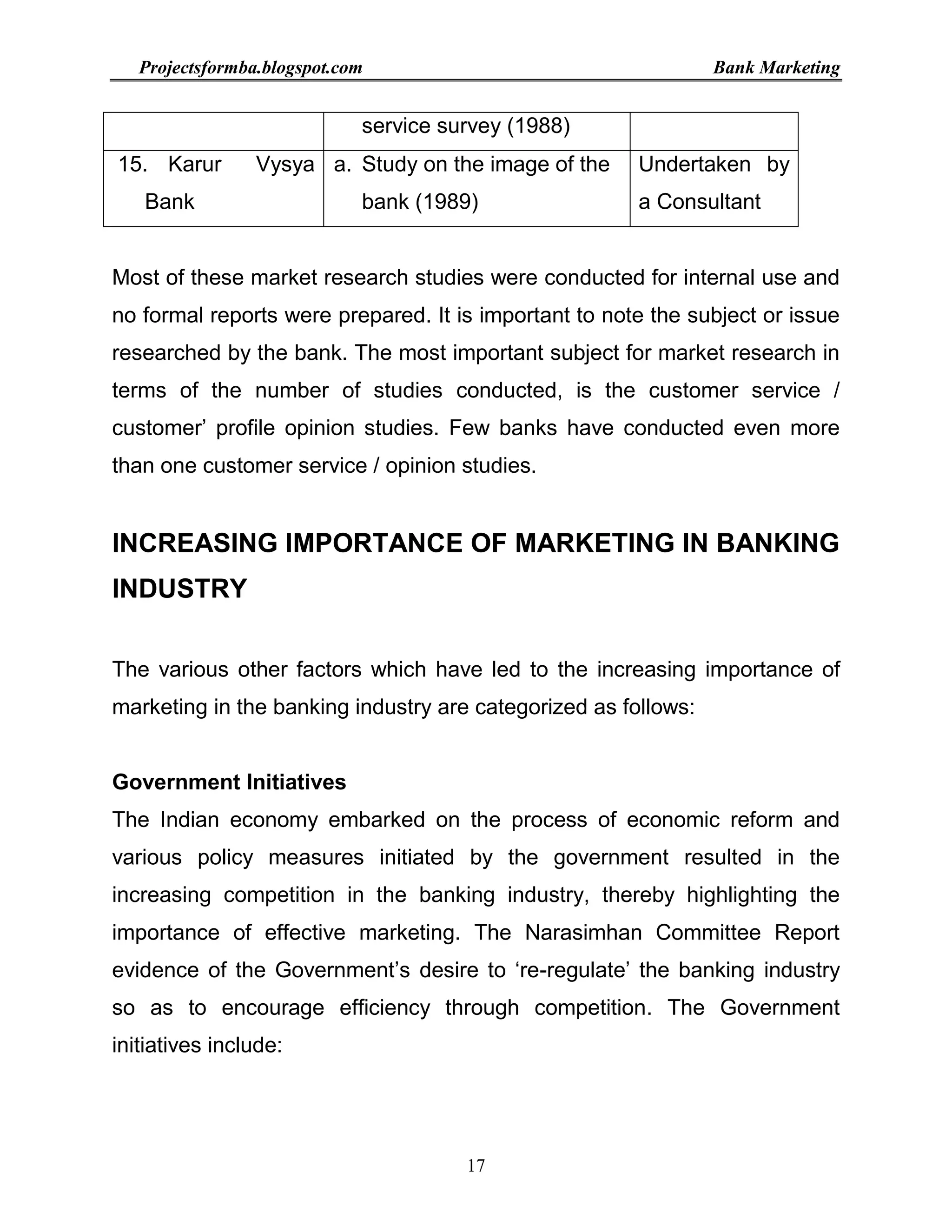

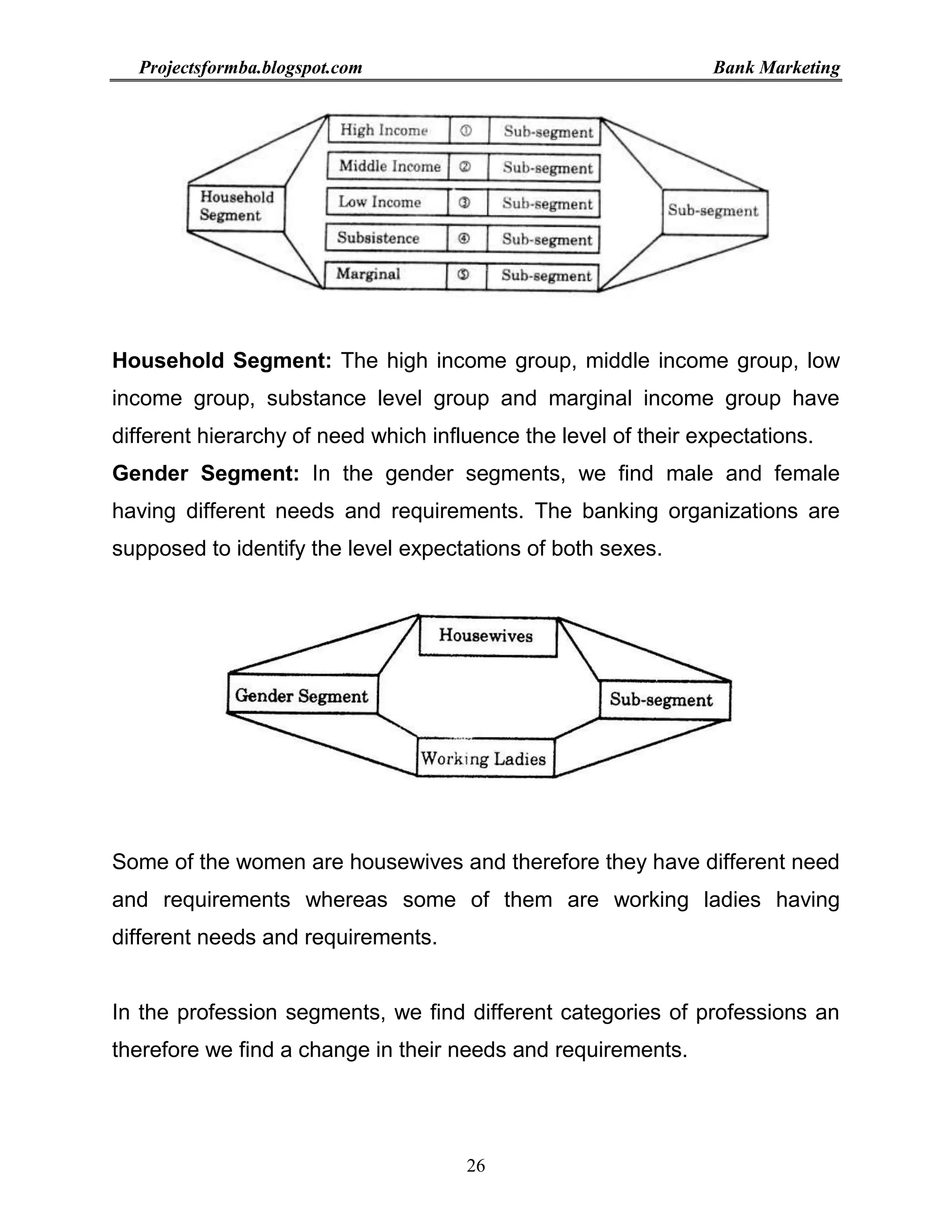

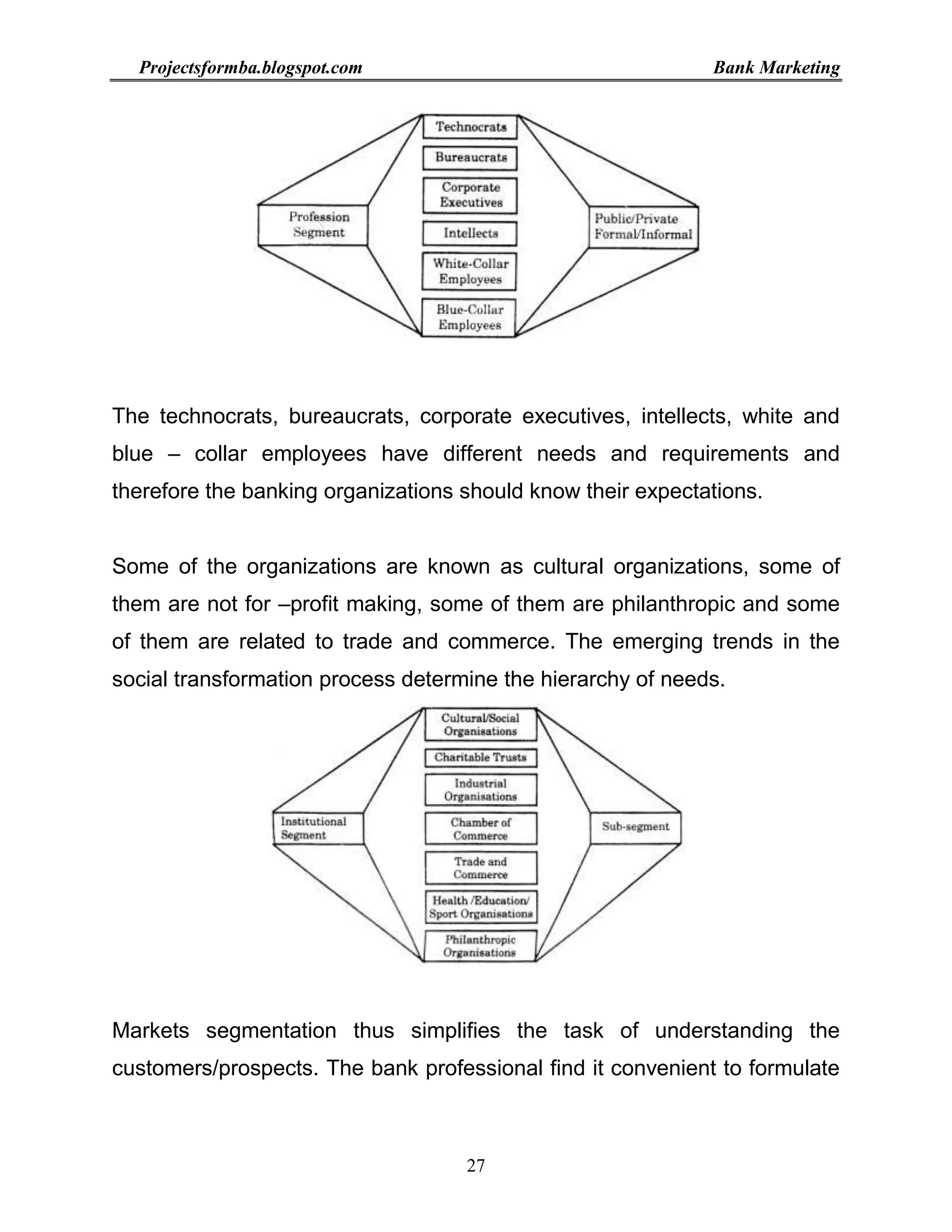

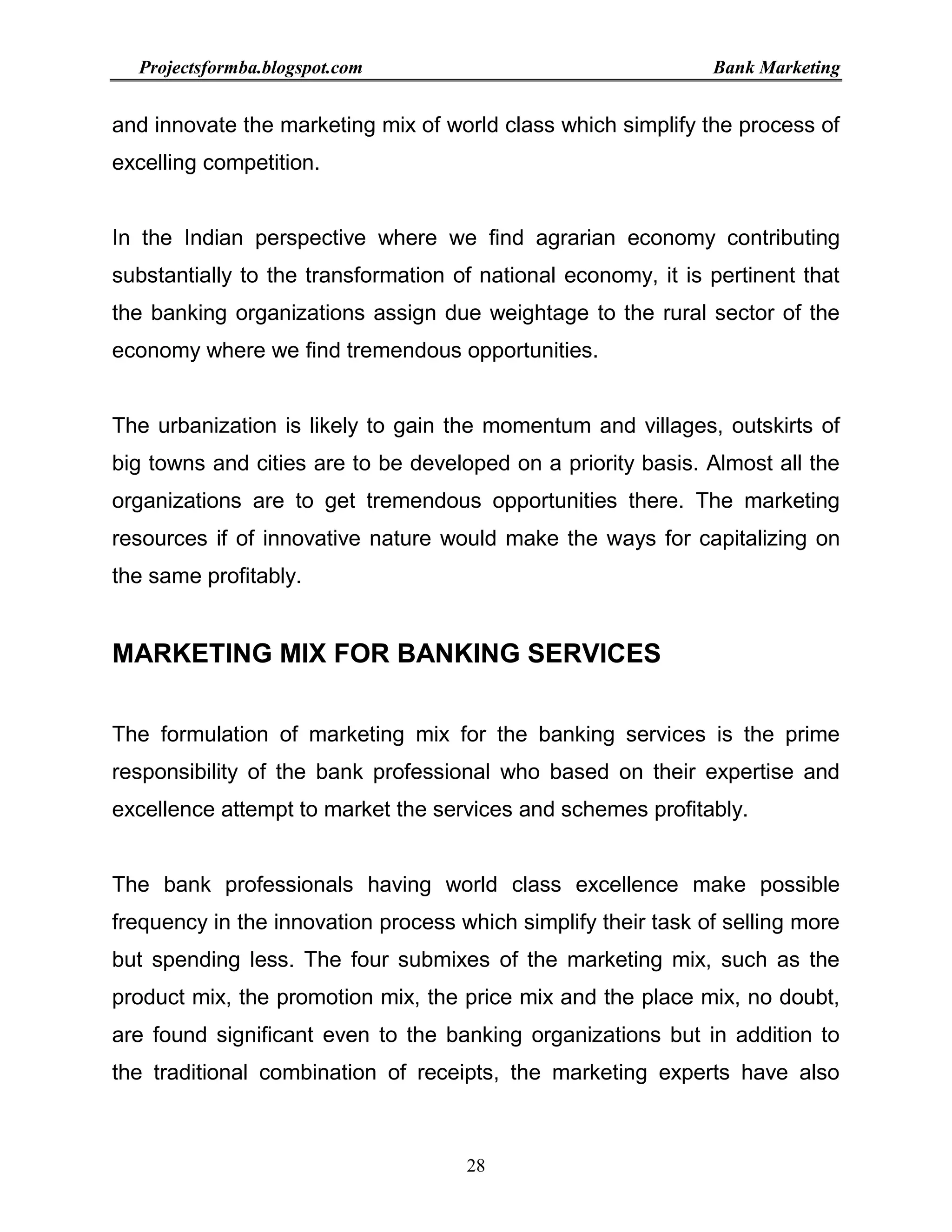

The document provides an overview of banking and finance in India. It discusses the origin of the word "bank" and defines what a bank is. It also covers the evolution of marketing concepts and their application to banking. Marketing and competition in the banking industry are increasing in importance as banks need to effectively target and segment customers to stay profitable in the face of new competitors. New technologies like electronic banking, phone banking, and online banking are changing how banks interact with and serve customers.