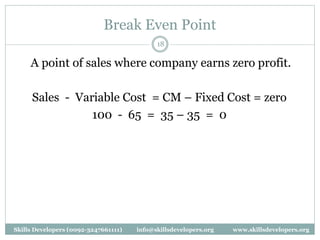

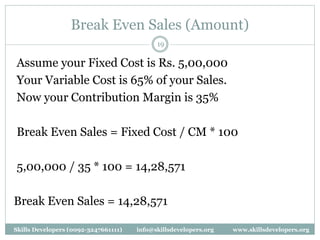

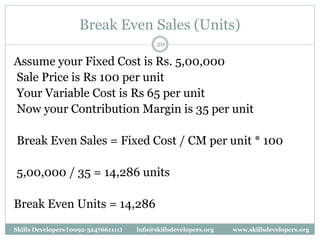

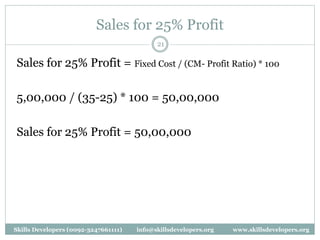

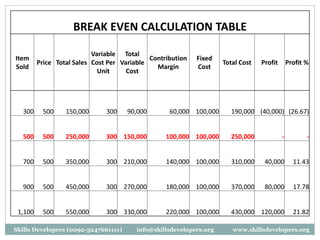

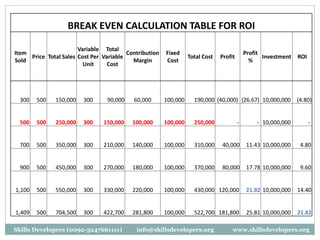

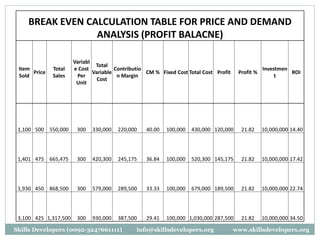

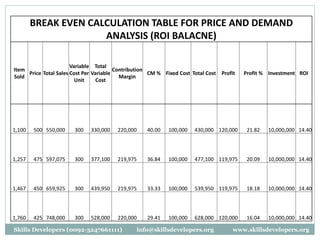

The document discusses various pricing techniques used by companies to maximize profits. It describes different cost-based pricing methods like cost-plus pricing, full cost pricing, and marginal cost pricing. Other pricing strategies covered include demand-based pricing techniques like skimming pricing and penetration pricing. The document also discusses break-even analysis and how to determine pricing based on competition in the market. A variety of factors are highlighted that companies should consider when determining prices.