Download to read offline

![Introduction and summary

4

Michael-Paul James

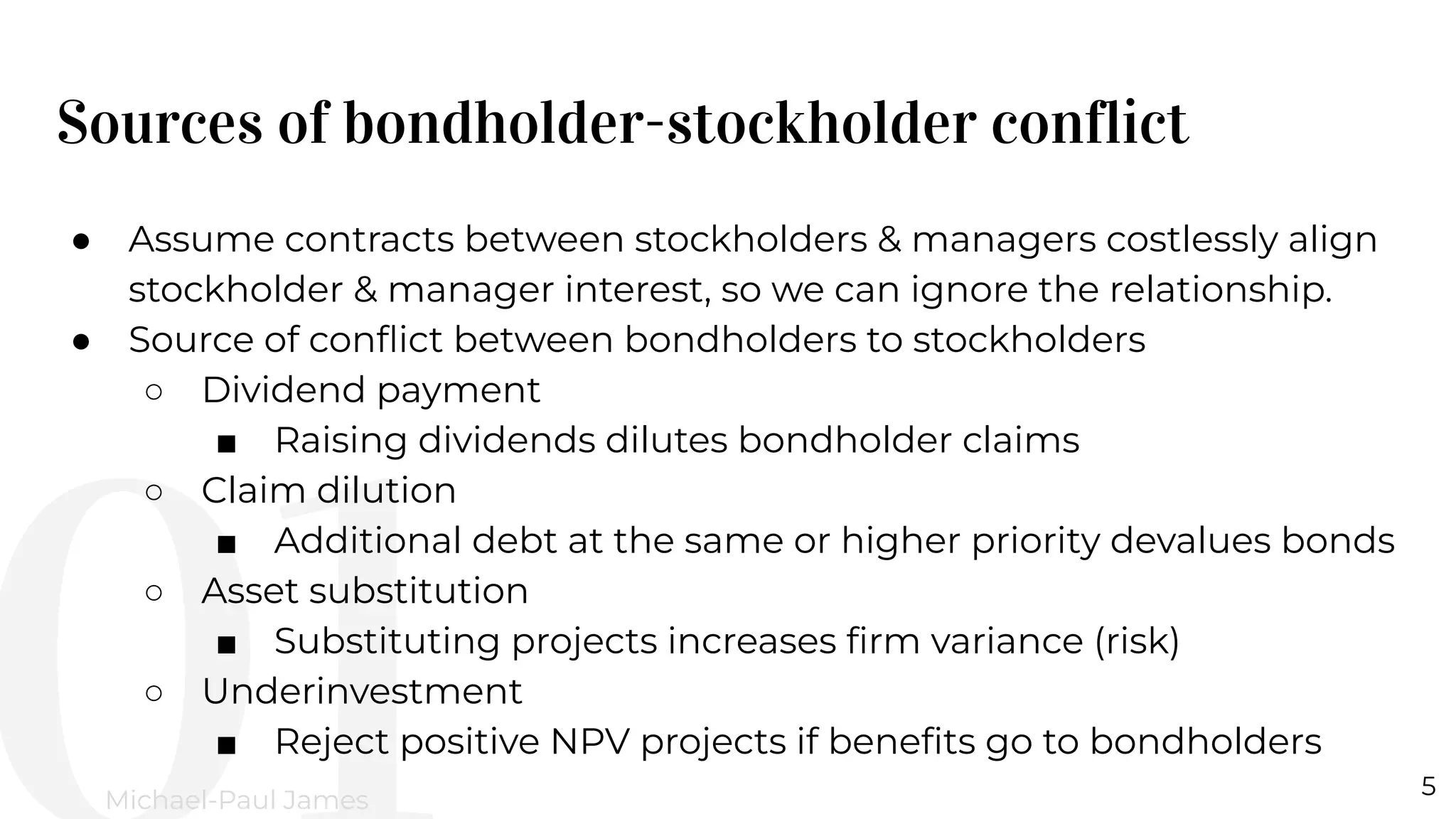

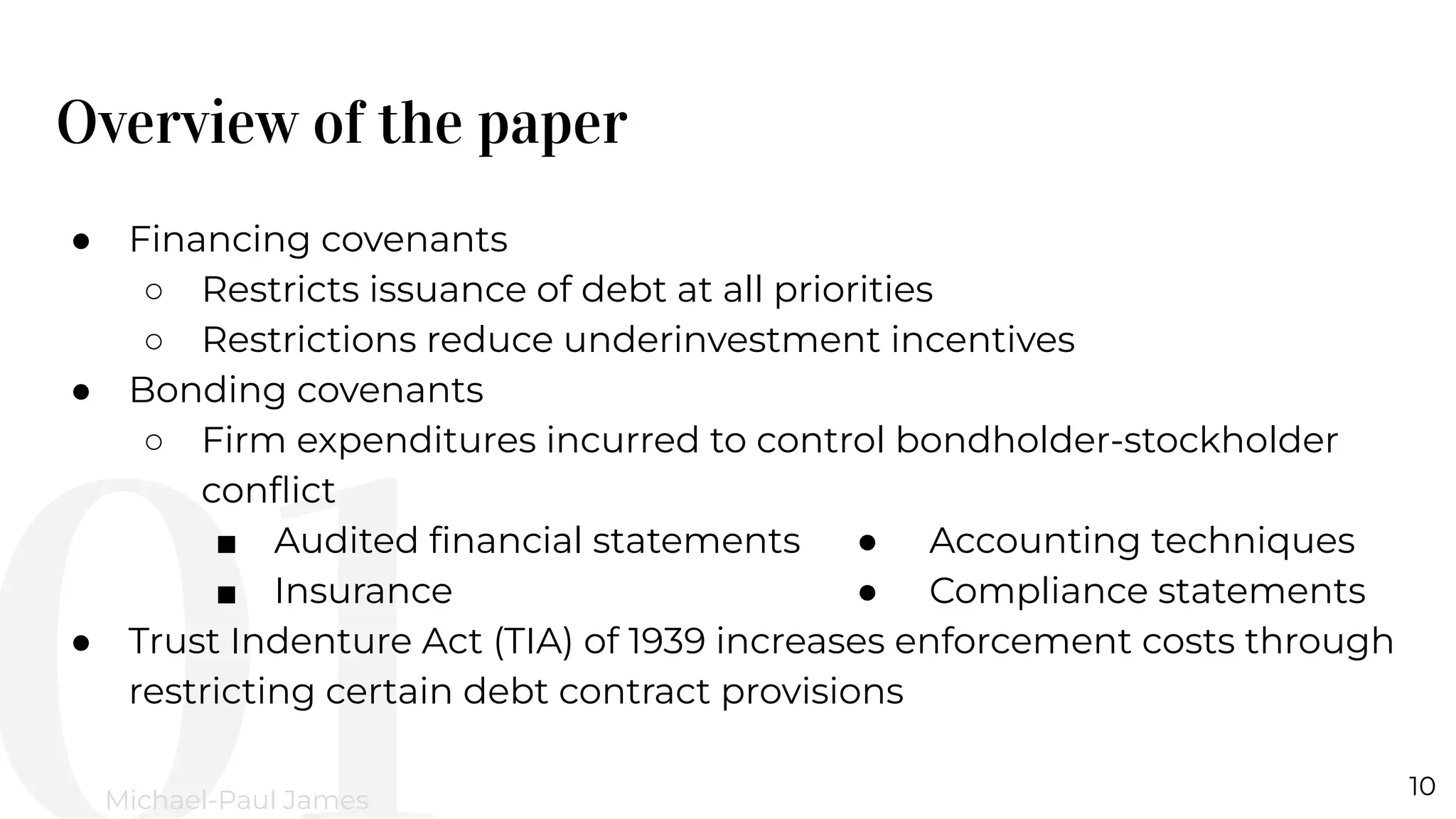

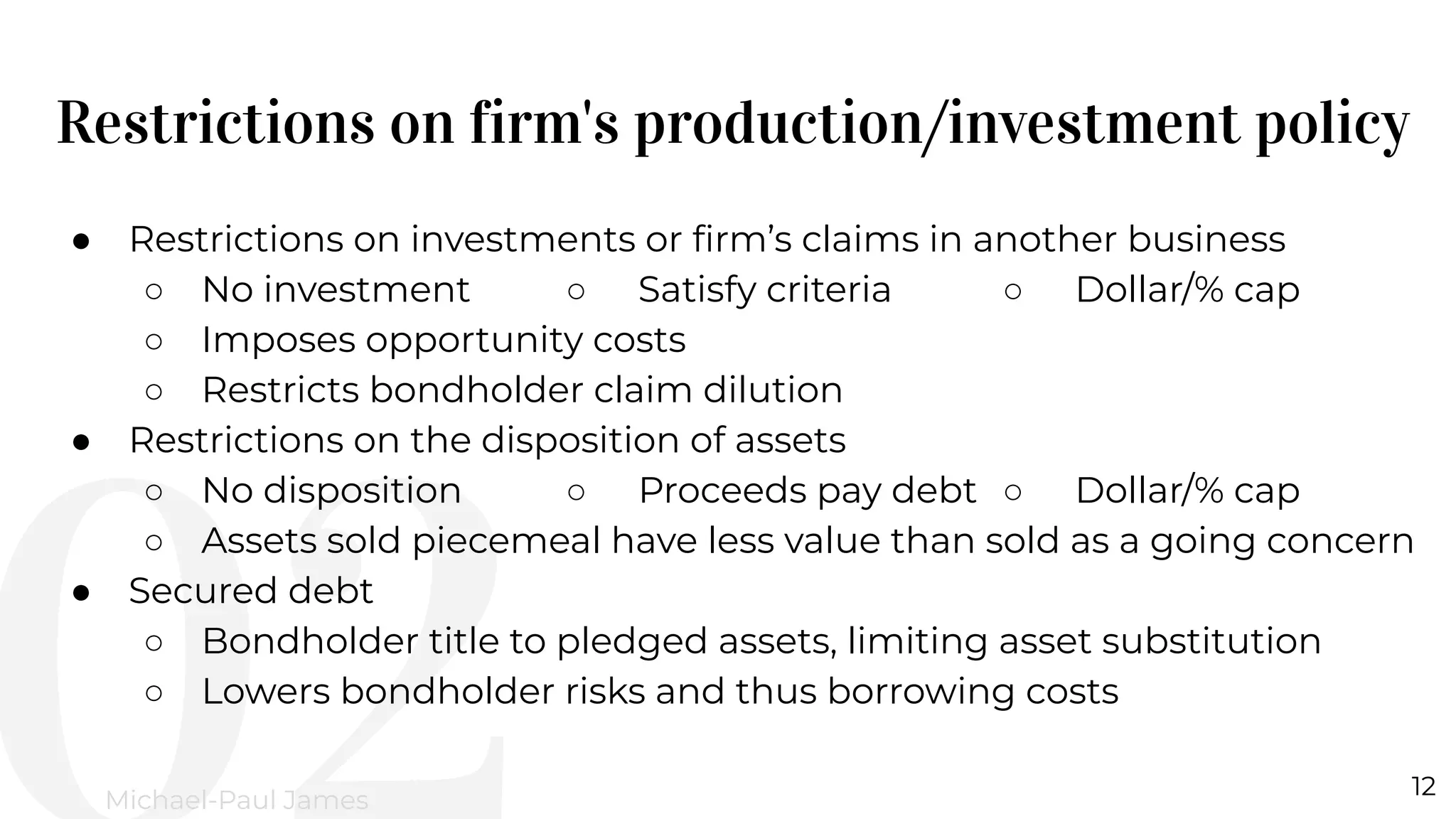

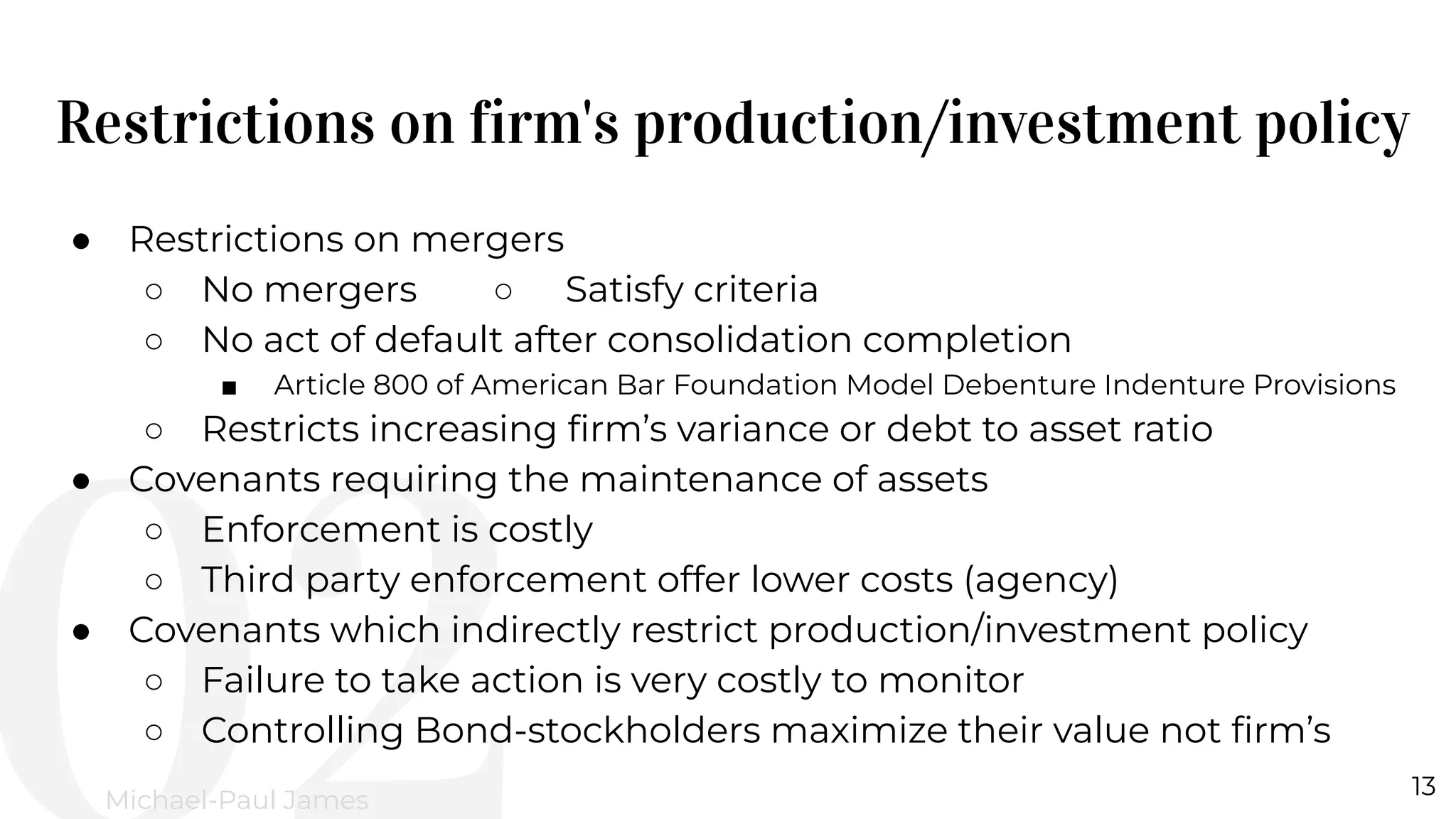

● Conflict of interest between bondholders and stockholders

○ Production plans can be constructed to maximize the wealth of

the bondholders or the stockholders

■ Equity call option [max(S(T)-Debt,0)]: Biases equity risk preference

○ Ideally, production plans should maximize firm value

● Bond covenant used to mitigate bondholder-stockholder conflict

○ Restricts the firm from engaging in specified actions after the

bonds are sold

● Provisions from the American Bar Foundation compendium

○ Commentaries on Indentures](https://image.slidesharecdn.com/04jamessmithwarner1979-220317205028/75/Presentation-on-On-Financial-Contracting-An-Analysis-of-Covenants-4-2048.jpg)

The document analyzes the conflict between bondholders and stockholders in financial contracting, emphasizing how bond covenants can mitigate these conflicts by imposing restrictions on corporate actions. It reviews evidence from a sample of bond covenants and discusses various enforcement mechanisms, including legal liabilities and the role of trustees. The conclusions highlight the implications of bond covenants on capital structure and suggest avenues for further research on contractual provisions and conflict management.