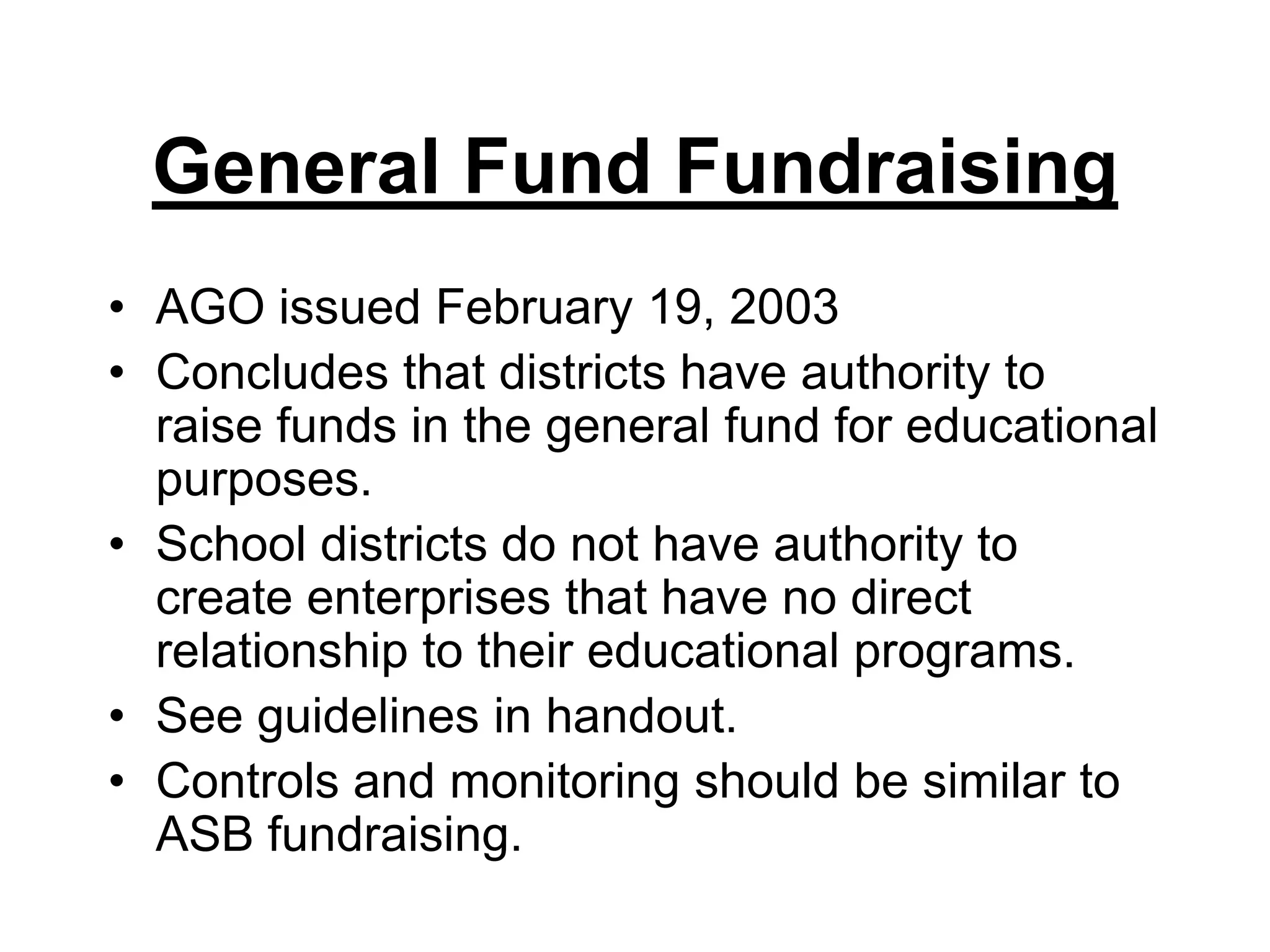

The document provides an overview of the 2003 Schools Workshop and guidance for auditing schools for the 2002-2003 fiscal year. Key points included changes to financial reporting requirements to comply with GASB 34, evaluating fundraising activities and the use of restricted funds, ensuring proper treatment of I-728 moneys, and current hot topics like the authority of districts to conduct general fund fundraising and the applicability of competitive bidding requirements. Auditors were instructed to focus on areas like enrollment trends, financial condition indicators, and the proper categorization of fund balance reserves and designations.