POSITIVE DAN NORMATIVE THEORIES ACCOUNTING

•Download as DOCX, PDF•

0 likes•487 views

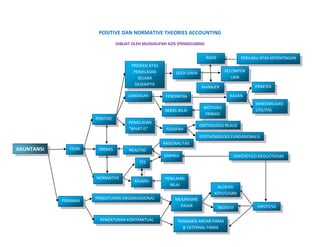

The document discusses positive and normative theories of accounting. Positive theories aim to objectively explain and predict phenomena, relying on empirical observations and rational foundations. Normative theories make value judgments and establish standards or ideals for practice, focusing on mechanisms for decision making and resource allocation. The document contrasts the descriptive, empirical nature of positive theories with the prescriptive, value-based approach of normative theories in accounting.

Recommended

More Related Content

More from Universitas Mulawarman Samarinda

More from Universitas Mulawarman Samarinda (20)

Recently uploaded

Recently uploaded (20)

POSITIVE DAN NORMATIVE THEORIES ACCOUNTING

- 1. POSITIVE DAN NORMATIVE THEORIES ACCOUNTING DIBUAT OLEH MUSDALIFAH AZIS (P0500310004) AGEN PERILAKU ATAS KEPENTINGAN PREDIKSI ATAS PENJELASAN OLEH SIAPA KELOMPOK SECARA LAIN DESKRIPTIF PRAKTEK MANAJER LANDASAN FENOMENA KAJIAN MAKSIMILISASI MOTIVASI BEBAS NILAI UTILITAS PRIBADI POSITIVE PENJELASAN ONTHOLOGIS REALIS “WHAT IS” FILSAFAH EPISTHEMOLOGI FUNDASIONALIS RASIONALITAS AKUNTANSI TEORI PREMIS REALITAS EMPIRIS HYPOTETICO-DEDUCTIVISM TES NORMATIVE PENILAIAN ASUMSI NILAI ALOKASI KEPUTUSAN PENGATURAN ORGANISASIONAL MEKANISME PERANAN PASAR INSENTIF HIPOTESIS PENGATURAN KONTRAKTUAL TRANSAKSI ANTAR FIRMA & EXTERNAL FIRMA