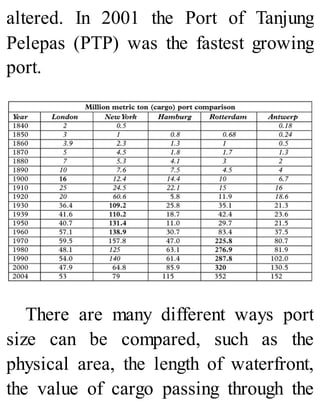

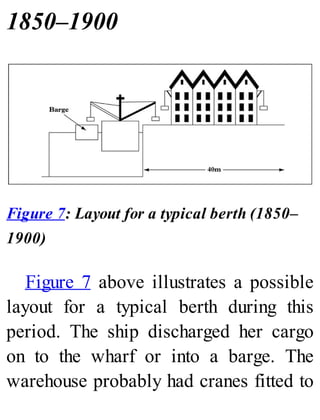

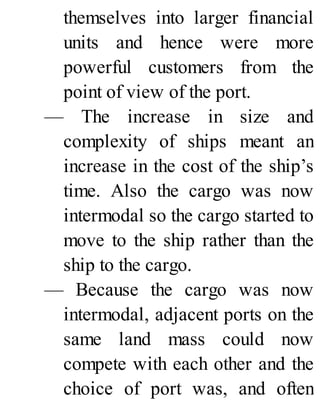

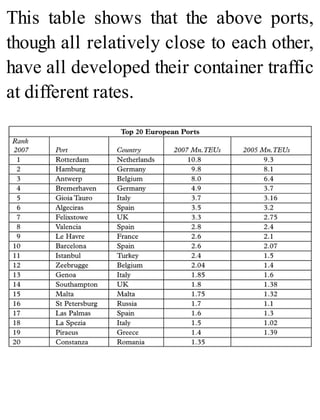

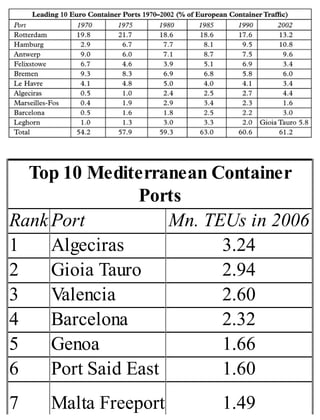

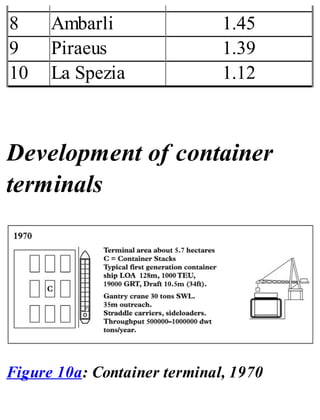

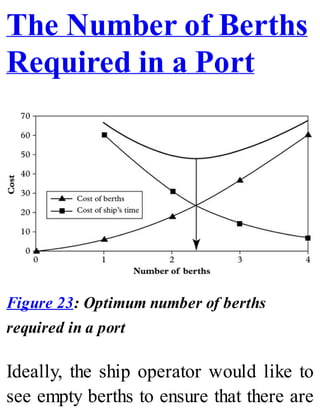

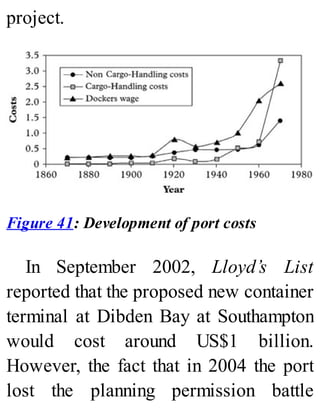

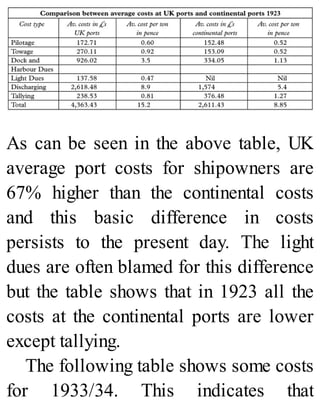

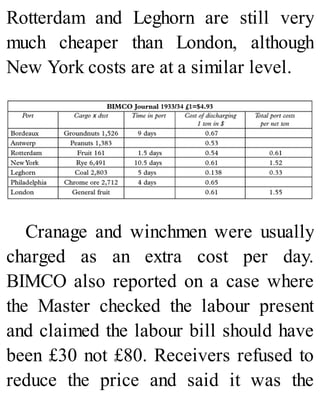

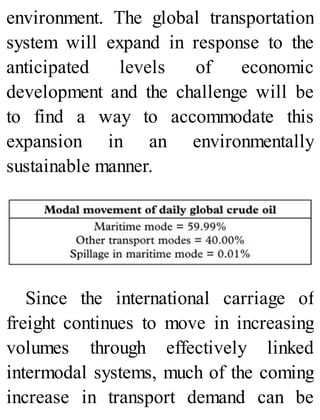

Downloaded 361 times

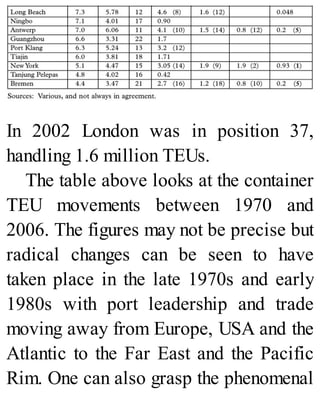

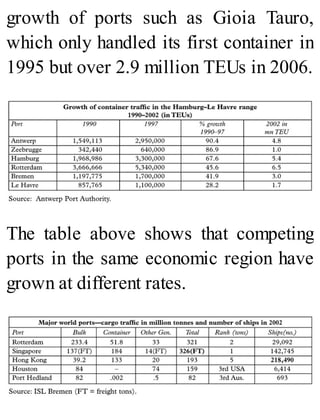

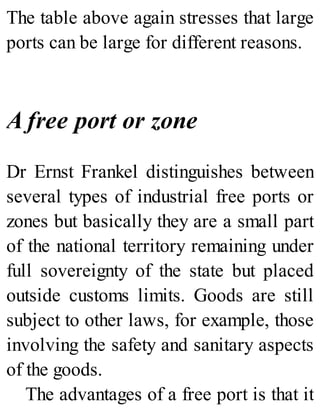

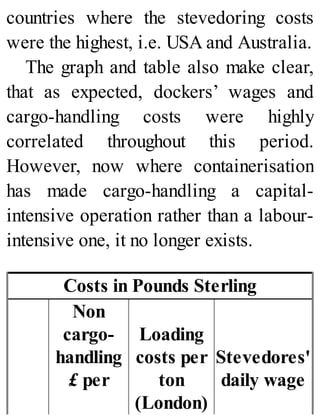

This document provides a summary of the contents of the book "Port Management and Operations" by Professor Patrick M. Alderton. It discusses 12 chapters that will cover topics related to port development, changing ship technology, port approaches, administration, policy, berths, cargo handling, labor, time in port, costs, and environmental matters. It includes a preface by the author providing background on the book and its third edition. It also lists several other titles in the Lloyd's Practical Shipping Guides series.