Download to read offline

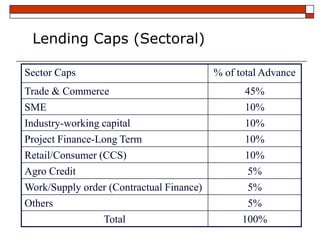

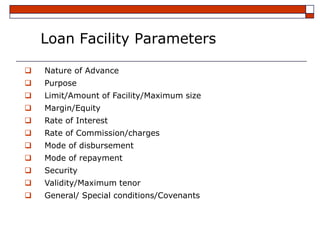

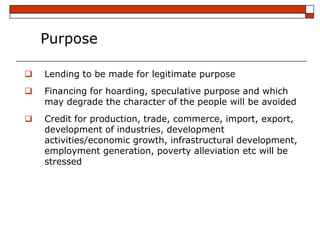

This document outlines the credit risk management guidelines of an organization. It discusses the industries and business segments the organization focuses on, encourages or maintains lending to. It also lists the types of loan facilities offered and sets lending limits for single borrowers/groups and sectors. The document provides guidelines on loan parameters such as purpose, security requirements, interest rates and repayment terms. It identifies business types that are discouraged and outlines processes for legal documentation and insurance of loans.