Recommended

More Related Content

What's hot

What's hot (19)

Viewers also liked

Viewers also liked (14)

Similar to Physician Long Term Disability Flyer

Similar to Physician Long Term Disability Flyer (20)

Physician Long Term Disability Flyer

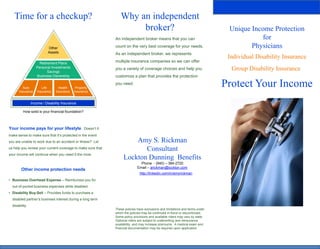

- 1. Time for a checkup? Why an independent broker? Unique Income Protection An independent broker means that you can for Other count on the very best coverage for your needs. Physicians Assets As an independent broker, we represents Individual Disability Insurance Retirement Plans multiple insurance companies so we can offer Personal Investments Savings you a variety of coverage choices and help you Group Disability Insurance Business Ownership customize a plan that provides the protection Auto Life Health Property you need. Protect Your Income Insurance Insurance Insurance Insurance Income / Disability Insurance How solid is your financial foundation? Your income pays for your lifestyle. Doesn’t it make sense to make sure that it’s protected in the event you are unable to work due to an accident or illness? Let Amy S. Rickman us help you review your current coverage to make sure that Consultant your income will continue when you need it the most. Lockton Dunning Benefits Phone - (940) – 384-2720 Email – arickman@lockton.com Other income protection needs http://linkedin.com/in/amyrickman • Business Overhead Expense – Reimburses you for out-of-pocket business expenses while disabled. • Disability Buy-Sell – Provides funds to purchase a disabled partner’s business interest during a long term disability. These policies have exclusions and limitations and terms under which the policies may be continued in-force or discontinued. Some policy provisions and available riders may vary by state. Optional riders are subject to underwriting and reinsurance availability, and may increase premiums. A medical exam and financial documentation may be required upon application.

- 2. Does your policy have these important features? • Own Occupation Definition of Disability – Allows you to receive up to 100% of your benefit if you cannot perform the duties of your own occupation, even if What’s your earning potential? Life is full of risks A disability could prevent you from earning an income. working in another occupation. • Cost of Living Adjustment – During a disability, you As a physician, you’ve seen firsthand how often disabilities Could you afford your lifestyle without it? The charts below receive cost of living adjustments to your monthly benefit occur. Almost three in 10 of today’s 20 year olds will show what your potential earnings to age 67 could be (with to help keep up with inflation. become disabled before reaching age 671. You take care no annual salary increases): • Future Increase Option – These may be available of others – but who will take care of you if a disability automatically to help keep your policy up-to-date without strikes and you are unable to generate an income to meet requiring additional medical underwriting. ANNUAL INCOME your financial needs? • Catastrophic Benefits – Provides a monthly benefit in Age $150,000 $350,000 $500,000 addition to the base benefit during a catastrophic 30 $5,550,000 $12,950,000 $18,500,000 disability. You might be surprised to learn that: 35 $4,800,000 $11,200,000 $16,000,000 • Unlimited Mental and Nervous Coverage– Mental and nervous conditions covered as any other disability. • The average long-term disability absence lasts 2 ½ 40 $4,050,000 $9,450,000 $13,500,000 • Retirement Protection – Additional monthly benefits years.2 45 $3,300,000 $7,700,000 $11,000,000 designed to protect retirement plan contributions. • In June of 2010, there were nearly 2.5 million disabled workers in their 20s, 30s, and 40s receiving SSDI Help protect your most valuable asset – your ability to work Are you taking advantage of discounts that may benefits.3 and earn an income – with a personal disability income be available? • More than one in five workers will be disabled for 5 years policy. Individual DI insurance can be a “lifesaver” when • State and local associations or more during their working careers.4 you need it most. • Hospital affiliation • Multilife discounts Age Male Female Discounted 30 $270.08 $424.89 $231.50 35 $310.96 $463.86 $263.52 1SocialSecurity Administration, Fact Sheet 2009 2Commissioner’s Disability Insurance Tables A and C, assuming 40 $415.42 $577.13 $347.09 equal weights by gender and occupation class 45 $519.71 $678.68 $429.09 3U.S. Census Bureau, 2007 American Community Survey 4Commissioner's Disability Insurance Tables A and C, assuming Rates based on a $10,000 monthly benefit, 5A-M occ equal weights by gender and occupation class class, 90 day elimination period, Age 67 benefit period.