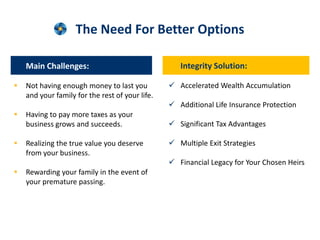

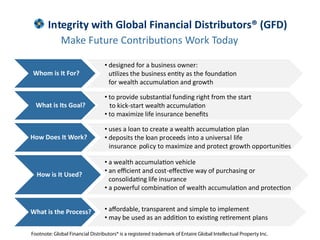

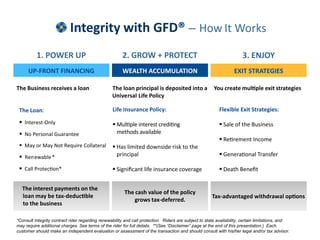

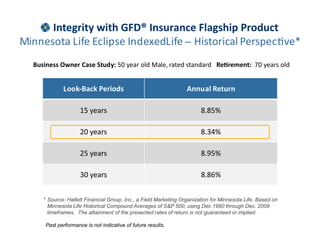

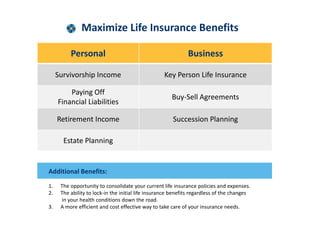

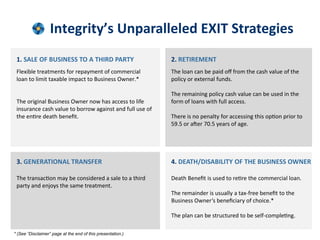

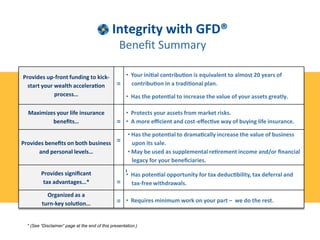

The document provides an overview of the Integrity with GFD solution, a new wealth accumulation and protection solution for business owners. It addresses main challenges business owners face like not having enough money for retirement or rewarding family. The Integrity solution offers accelerated wealth accumulation, additional life insurance protection, and significant tax advantages. It works by providing an upfront loan that is deposited into a universal life insurance policy to grow tax-deferred. Business owners can then enjoy multiple exit strategies like selling the business, using it for retirement income, or leaving a financial legacy.

![Client Presentation[1] Entaire](https://cdn.slidesharecdn.com/ss_thumbnails/clientpresentation1entaire-124467293854-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)