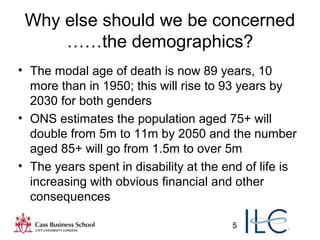

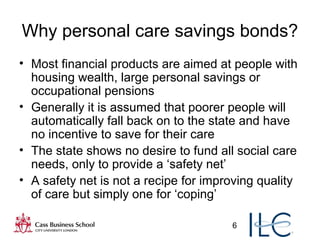

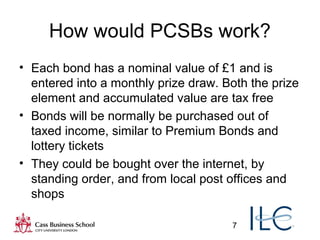

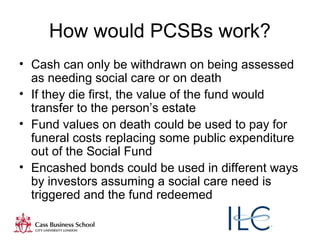

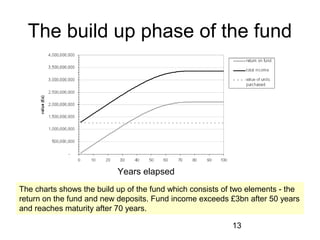

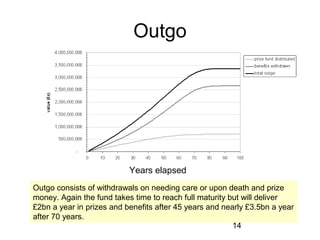

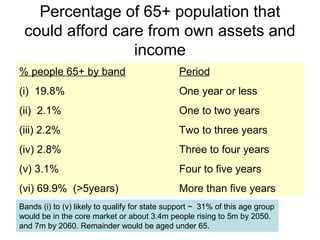

The document discusses the concept of Personal Care Savings Bonds (PCSBs) as a means to finance social care for the ageing population in the UK. It highlights the demographic challenges, the need for individual savings rather than reliance on the state, and the operational mechanics of PCSBs, including tax benefits and liquidity upon triggering care needs. The proposed system aims to encourage saving while providing a safety net for social care, with potentially significant financial impacts by 2050.

![Ad presentation to lga summit 13th july[1]](https://cdn.slidesharecdn.com/ss_thumbnails/adpresentationtolgasummit13thjuly1-110720113424-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)