Penalty for non maintaing statutory records & registers

•

1 like•9,852 views

Penalties under Companies Act, 2013. Penalty for non maintaining statutory records & Registers. A small compilation on penalties under New Companies Act, 2013 for non maintaining Minutes of Board Meetings, General Meetings and Statutory Register.

Report

Share

Report

Share

Download to read offline

Recommended

A Brief About Forensic Accounting

Forensic Accounting is the use of accounting skills to investigate fraud and analyze the financial information that can be useful in legal proceedings. Areas of forensic involvement fall into two categories namely litigation support and investigative accounting. Go through the slides to have a brief idea about Forensic Accounting and the common accounting fraud areas. Also know what exactly forensic accountants do.

Credit monitoring

Credit monitoring is the ongoing supervision of a loan account to ensure the borrower continues to meet the terms of the loan sanction. It helps maintain asset quality and prevent slippage into NPA status. There are four stages of monitoring - pre-sanction, post-sanction pre-disbursement, during disbursement, and post-disbursement. Regular inspections, financial statement reviews, and verifying end-use of funds are some key monitoring activities. Early warning signs like delays in submission of documents or frequent requests for extensions should trigger corrective actions like discussions with the borrower to resolve issues impacting the business.

PENALTIES FOR ILLEGAL STRIKES AND LOCKOUTS

The document discusses penalties for illegal strikes and lockouts under the Industrial Dispute Act of 1947. It outlines that workers participating in an illegal strike can face up to one month imprisonment or a 50 rupee fine, or both. Employers conducting an illegal lockout can face up to one month imprisonment or a 1,000 rupee fine, or both. Anyone instigating or supporting an illegal strike or lockout can be imprisoned for up to six months or fined 1,000 rupees, or both. Providing financial support for an illegal strike or lockout is also punishable with up to six months imprisonment, a 1,000 rupee fine, or both.

CAIIB Super Notes: Corporate Banking: Module A: Corporate Banking and Finance...

CAIIB Super Notes: If you are preparing for CAIIB- these are a must-have. Visit http://sirfbusiness.blogspot.com for more info.

80g

This document provides information about donations to charitable organizations under Section 80G of the Indian Income Tax Act. It outlines the benefits of Section 80G deductions for donors and NGOs, eligibility requirements, the application process for 12A and 80G certifications, validity periods of registrations, factors to consider for 80G approval, organizations that offer 100% deductions without limits, and the different deduction amounts and limits under Section 80G.

Credit rating

This document discusses credit ratings. It begins by defining credit ratings as assessments of creditworthiness based on borrowing history and financial information. It then outlines the different types of ratings and the rating process. The rating process involves analyzing factors like the economy, business, management, and finances. It also lists the major credit rating agencies in India - CRISIL, ICRA, CARE, ONICRA - and provides details on each one. Finally, it discusses who uses credit ratings like investors, regulators, and issuers, and notes some disadvantages of credit ratings.

Disorders of perception, AMU Aligarh

This document discusses disorders of perception, including the differences between sensation and perception. Sensation involves detection of stimuli by sensory receptors, while perception involves higher-level processing and interpretation of sensory information in the brain. Abnormal perceptions can include sensory distortions like changes in intensity, quality, spatial form, or the experience of time. They can also involve splitting of perceptions or sensory deceptions like illusions and hallucinations. Specific perceptual disorders discussed include micropsia, macropsia, metamorphopsia, akinetopsia, and Todd's syndrome. Causes can include organic brain conditions, migraines, psychoactive drug use, or psychotic disorders like schizophrenia.

Assessment of huf

Meaning, Schools of Hindu Law, Treatment of fee or salary earned by coparcener as director or partner, Remuneration paid by HUF to a member for conducting its business, Incomes not treated as HUF incomes, Partition of HUF, Deductions under section 80C to 80U applicable to HUF, Computation of Total income of HUF and Tax Liability.

Recommended

A Brief About Forensic Accounting

Forensic Accounting is the use of accounting skills to investigate fraud and analyze the financial information that can be useful in legal proceedings. Areas of forensic involvement fall into two categories namely litigation support and investigative accounting. Go through the slides to have a brief idea about Forensic Accounting and the common accounting fraud areas. Also know what exactly forensic accountants do.

Credit monitoring

Credit monitoring is the ongoing supervision of a loan account to ensure the borrower continues to meet the terms of the loan sanction. It helps maintain asset quality and prevent slippage into NPA status. There are four stages of monitoring - pre-sanction, post-sanction pre-disbursement, during disbursement, and post-disbursement. Regular inspections, financial statement reviews, and verifying end-use of funds are some key monitoring activities. Early warning signs like delays in submission of documents or frequent requests for extensions should trigger corrective actions like discussions with the borrower to resolve issues impacting the business.

PENALTIES FOR ILLEGAL STRIKES AND LOCKOUTS

The document discusses penalties for illegal strikes and lockouts under the Industrial Dispute Act of 1947. It outlines that workers participating in an illegal strike can face up to one month imprisonment or a 50 rupee fine, or both. Employers conducting an illegal lockout can face up to one month imprisonment or a 1,000 rupee fine, or both. Anyone instigating or supporting an illegal strike or lockout can be imprisoned for up to six months or fined 1,000 rupees, or both. Providing financial support for an illegal strike or lockout is also punishable with up to six months imprisonment, a 1,000 rupee fine, or both.

CAIIB Super Notes: Corporate Banking: Module A: Corporate Banking and Finance...

CAIIB Super Notes: If you are preparing for CAIIB- these are a must-have. Visit http://sirfbusiness.blogspot.com for more info.

80g

This document provides information about donations to charitable organizations under Section 80G of the Indian Income Tax Act. It outlines the benefits of Section 80G deductions for donors and NGOs, eligibility requirements, the application process for 12A and 80G certifications, validity periods of registrations, factors to consider for 80G approval, organizations that offer 100% deductions without limits, and the different deduction amounts and limits under Section 80G.

Credit rating

This document discusses credit ratings. It begins by defining credit ratings as assessments of creditworthiness based on borrowing history and financial information. It then outlines the different types of ratings and the rating process. The rating process involves analyzing factors like the economy, business, management, and finances. It also lists the major credit rating agencies in India - CRISIL, ICRA, CARE, ONICRA - and provides details on each one. Finally, it discusses who uses credit ratings like investors, regulators, and issuers, and notes some disadvantages of credit ratings.

Disorders of perception, AMU Aligarh

This document discusses disorders of perception, including the differences between sensation and perception. Sensation involves detection of stimuli by sensory receptors, while perception involves higher-level processing and interpretation of sensory information in the brain. Abnormal perceptions can include sensory distortions like changes in intensity, quality, spatial form, or the experience of time. They can also involve splitting of perceptions or sensory deceptions like illusions and hallucinations. Specific perceptual disorders discussed include micropsia, macropsia, metamorphopsia, akinetopsia, and Todd's syndrome. Causes can include organic brain conditions, migraines, psychoactive drug use, or psychotic disorders like schizophrenia.

Assessment of huf

Meaning, Schools of Hindu Law, Treatment of fee or salary earned by coparcener as director or partner, Remuneration paid by HUF to a member for conducting its business, Incomes not treated as HUF incomes, Partition of HUF, Deductions under section 80C to 80U applicable to HUF, Computation of Total income of HUF and Tax Liability.

PRIORITY SECTOR LENDING (PSL).pptx

The document discusses India's Priority Sector Lending (PSL) guidelines. It defines PSL as lending by banks to sectors like agriculture, micro, small and medium enterprises, housing, education etc. that are considered economically important. Banks must lend at least 40% of their adjusted net bank credit or credit equivalent amount of off-balance sheet exposure to these priority sectors. Specific lending targets are set for sectors like agriculture (18%), micro enterprises (7.5%), and weaker sections (10%). Eligible activities under priority sectors and their loan limits are also defined.

Export credit refinance

This document discusses export credit refinance facilities provided by the Reserve Bank of India (RBI) to banks. It defines key terms and outlines two main facilities - the rupee refinance facility and a special dollar refinance facility introduced to support pre-shipment export credit in foreign currency. Under the rupee facility, banks can access refinancing of up to 50% of their outstanding rupee export credit at the RBI's repo rate. The special dollar facility allows banks to swap rupees for dollars from RBI at market rates, using the dollars to provide export financing while paying the rupee refinance rate. Documentation, interest rates, and other terms are also outlined.

non banking financial companies

Non-banking financial companies (NBFCs) are financial institutions that provide banking services like loans and credit facilities but do not hold a banking license. NBFCs are registered under the Companies Act and regulated by the Reserve Bank of India. They provide services such as private education funding, retirement planning, money market trading, stock underwriting and portfolio management. Some major NBFCs in India include HDFC, Power Finance Corporation, Reliance Capital, and Infrastructure Development Finance Company. NBFCs play an important role in the Indian financial system by providing quick financing alternatives to businesses without complex banking procedures.

Banking and legal framework

This document discusses banking and legal frameworks in India. It outlines key acts like the Banking Regulation Act of 1949 and Reserve Bank of India Act of 1934 that established regulations for banks. It also summarizes Basel accords I, II, and III which establish international capital standards and risk management. The document defines risks faced by banks and capital adequacy ratios which represent minimum capital requirements as a percentage of risk-weighted assets.

Borderline Personality Disorder presented by MANASA GS, MSC APPLIED PSYCHOLOG...

Borderline Personality Disorder (BPD) is characterized by unstable moods, behavior, and relationships. It was first included in the DSM-III in 1980. BPD involves a pervasive pattern of instability in interpersonal relationships, self-image, and emotions that begins in early adulthood. Dialectical Behavior Therapy (DBT) is the gold standard treatment for BPD and focuses on mindfulness, distress tolerance, emotion regulation, and interpersonal effectiveness skills. DBT aims to reduce self-harming behaviors and improve relationships through individual therapy and skills training groups over several treatment stages with the goal of maintaining treatment gains.

Lesson 06

The document discusses the history of clinical psychology and its involvement in treatment and prevention. It describes how during the 19th century, the focus shifted from classifying psychoses to investigating treatments for neurotic patients using suggestion and hypnosis. It then outlines key figures like Jean Charcot, Josef Breuer, and Sigmund Freud and their contributions to developing psychoanalysis. World War II renewed the need for psychological assessment and led to clinical psychologists emerging as providers of treatment for psychopathology like shell shock, now known as PTSD.

7 idx monthly statistics juli 2019

This document is the Indonesia Stock Exchange's monthly statistics report for July 2019. It provides various data and statistics related to stock trading on the Indonesia Stock Exchange in July, including stock indices performance, trading volumes and values, most active stocks, new and delisted listings, and financial data and ratios for listed companies. The report aims to inform readers about the performance and activities on the Indonesia Stock Exchange in July 2019.

Antiepileptic Drugs

- Lessons from Psychiatry

In this lecture:

1. AED’s: Looking Beyond Epilepsy- Their Relevance & Utility in Neuropsychiatry

2. Parodoxical relationships: seizures, behavior and AEDs

3. What relevance do these findings hold for epilepsy

Optitax's presentation on implication of gst on related party 10.06.2018

In this presentation we have tried to highlight the implication of GST on related party transactions. Everyone should be aware that under GST if there is any transaction with related party then valuation aspect to be kept in mind.

Crr and slr management

cash reserve ratio, statutory liquidity ratio, borrowing and lending behaviour of financial institutions

Chapter 1 the nature of fraud

The document defines fraud and discusses its different types. It describes fraud as theft by deception or trickery to obtain an unjust advantage. The main types are occupational fraud committed by employees against an organization, and fraud committed for an organization like financial statement fraud. Employee embezzlement, vendor fraud, and customer fraud are provided as examples of fraud against an organization. Management fraud committed through misleading financial statements can harm shareholders and investors. Criminal prosecution through law and civil lawsuits aim to punish fraudsters and compensate victims.

NBFCs - A quick guide by Niddhi Parmar

This document provides a summary of Non-Banking Financial Companies (NBFCs) in India. It defines what an NBFC is, outlines the key types of NBFCs such as asset finance companies, loan companies, investment companies, and microfinance institutions. It also describes important NBFC concepts like capital adequacy requirements, classification of assets, and the regulations applicable to different categories of NBFCs. The document is intended to serve as a quick guide to NBFCs in India.

Auditing

This document provides an overview of auditing. It defines auditing as an unbiased examination and evaluation of a company's financial statements, internally or externally. It distinguishes auditing from bookkeeping and accounting by noting that auditing examines the accuracy and fairness of financial records, while bookkeeping records transactions and accounting analyzes results. The document also describes common types of errors like omissions and commissions that may occur, and how they differ from intentional frauds. Finally, it gives examples of specific frauds like misappropriation of cash, goods, assets, and manipulation of accounts.

Know your customer(kyc) Norms

The document discusses Know Your Customer (KYC) norms and their importance. It begins by stating the session objectives of explaining the significance of KYC norms and why banks need to comply with them. It then provides examples of identity theft, credit card fraud, and money laundering to illustrate the risks banks face and why KYC procedures are necessary to prevent illicit transactions, money laundering, and terrorist financing. The document emphasizes that KYC norms issued by the Reserve Bank of India are aimed at arresting these criminal activities. It also notes exceptions for "no frills" accounts that have stricter limits on balances and credit amounts.

Bill of exchange

The document defines a bill of exchange as a written instrument containing an unconditional order from a creditor (drawer) to a debtor (drawee) to pay a specified amount of money to a person (payee). There are three parties to a bill of exchange: the drawer, drawee, and payee. The drawer makes the order, the drawee is directed to pay, and the payee receives the money. A bill of exchange must be in writing, contain an express order to pay, specify three definite parties, state a certain amount of money payable in legal tender, and comply with formalities like date and stamp.

mental status examination

A mental status examination (MSE) is used to evaluate a patient's psychological well-being and state of mind. It includes objective observations by the clinician and subjective reports from the patient. The MSE assesses several domains including appearance, motor skills, speech, mood, affect, thought processes, thought content, perception, and cognitive functioning. However, an MSE is not an intelligence test and cannot provide a fully precise evaluation. It is a standard clinical technique used to evaluate symptoms of conditions like depression, mania, schizophrenia, and others.

residential status and its effect on tax incidence

The document discusses the determination of residential status in India for income tax purposes. It defines the different types of residential statuses as ordinary resident, resident but not ordinarily resident, and non-resident. It outlines the basic conditions and additional conditions to determine if an individual, HUF, firm, company, etc. qualifies as a ordinary resident or resident but not ordinarily resident. The control and management of affairs is used to determine residential status for HUF, firm, association of persons, and companies. Income from different sources is taxable in India based on the residential status of the assessee.

Role of RBI in financial inclusion

Starting of Financial Inclusion in India

Banking and financial services at an affordable cost to the vast sections of disadvantaged and low income groups.

Important step towards inclusive growth

SPECIAL KINDS OF HALLUCINATIONS oroginal.pptx

functional ,reflex ,autoscopy ,extracampine ,pseudohallucinations ,induced hallucinations ,phantom limb pain as described in fish psychopathology and SIMS(symptoms of mind) for m.phil clinical psychology

Entrepreneurship development - Institutional Assistance

Financial Assistance through SFCs,

SIDBI, Commercial bank, KSIDC,

KSSIC, IFCI; Non – financial

assistance from DIC, SISI, EDI, SIDO,

AWAKE, TCO, TECKSOK, KVIC;

Financial Incentives for SSI and Tax

Concessions’ Industrial Estates – its

roles and types.

Penalties under indian companies act

This document outlines penalties under the Indian Companies Act for various offenses. It provides a table with 34 sections listing the nature of the offense, applicable penalty, and persons held responsible. Penalties include fines from Rs. 500 to Rs. 50,000 per day and imprisonment up to 5 years for offenses such as failing to hold annual general meetings, not filing annual accounts, improper financial reporting, accepting deposits over limits, and prospectus violations. The document emphasizes that knowledge of company law and potential penalties is essential for company directors and officers to avoid legal issues arising from non-compliance.

Maintenance of records, electronically.

Companies Act 2013 requires listed companies and companies with over 1000 shareholders to maintain all statutory records electronically. Other companies can choose physical or electronic records but must follow guidelines if choosing electronic. Records include registers, minutes, agreements and other documents. Electronic records must be readable, retrievable, reproducible, capable of being dated and digitally signed. Managing directors are responsible for ensuring security, accuracy, accessibility and backup of electronic records. Records must be available for inspection electronically on payment. Companies must follow additional requirements for maintaining books electronically like ensuring accessibility in India and regular backups.

More Related Content

What's hot

PRIORITY SECTOR LENDING (PSL).pptx

The document discusses India's Priority Sector Lending (PSL) guidelines. It defines PSL as lending by banks to sectors like agriculture, micro, small and medium enterprises, housing, education etc. that are considered economically important. Banks must lend at least 40% of their adjusted net bank credit or credit equivalent amount of off-balance sheet exposure to these priority sectors. Specific lending targets are set for sectors like agriculture (18%), micro enterprises (7.5%), and weaker sections (10%). Eligible activities under priority sectors and their loan limits are also defined.

Export credit refinance

This document discusses export credit refinance facilities provided by the Reserve Bank of India (RBI) to banks. It defines key terms and outlines two main facilities - the rupee refinance facility and a special dollar refinance facility introduced to support pre-shipment export credit in foreign currency. Under the rupee facility, banks can access refinancing of up to 50% of their outstanding rupee export credit at the RBI's repo rate. The special dollar facility allows banks to swap rupees for dollars from RBI at market rates, using the dollars to provide export financing while paying the rupee refinance rate. Documentation, interest rates, and other terms are also outlined.

non banking financial companies

Non-banking financial companies (NBFCs) are financial institutions that provide banking services like loans and credit facilities but do not hold a banking license. NBFCs are registered under the Companies Act and regulated by the Reserve Bank of India. They provide services such as private education funding, retirement planning, money market trading, stock underwriting and portfolio management. Some major NBFCs in India include HDFC, Power Finance Corporation, Reliance Capital, and Infrastructure Development Finance Company. NBFCs play an important role in the Indian financial system by providing quick financing alternatives to businesses without complex banking procedures.

Banking and legal framework

This document discusses banking and legal frameworks in India. It outlines key acts like the Banking Regulation Act of 1949 and Reserve Bank of India Act of 1934 that established regulations for banks. It also summarizes Basel accords I, II, and III which establish international capital standards and risk management. The document defines risks faced by banks and capital adequacy ratios which represent minimum capital requirements as a percentage of risk-weighted assets.

Borderline Personality Disorder presented by MANASA GS, MSC APPLIED PSYCHOLOG...

Borderline Personality Disorder (BPD) is characterized by unstable moods, behavior, and relationships. It was first included in the DSM-III in 1980. BPD involves a pervasive pattern of instability in interpersonal relationships, self-image, and emotions that begins in early adulthood. Dialectical Behavior Therapy (DBT) is the gold standard treatment for BPD and focuses on mindfulness, distress tolerance, emotion regulation, and interpersonal effectiveness skills. DBT aims to reduce self-harming behaviors and improve relationships through individual therapy and skills training groups over several treatment stages with the goal of maintaining treatment gains.

Lesson 06

The document discusses the history of clinical psychology and its involvement in treatment and prevention. It describes how during the 19th century, the focus shifted from classifying psychoses to investigating treatments for neurotic patients using suggestion and hypnosis. It then outlines key figures like Jean Charcot, Josef Breuer, and Sigmund Freud and their contributions to developing psychoanalysis. World War II renewed the need for psychological assessment and led to clinical psychologists emerging as providers of treatment for psychopathology like shell shock, now known as PTSD.

7 idx monthly statistics juli 2019

This document is the Indonesia Stock Exchange's monthly statistics report for July 2019. It provides various data and statistics related to stock trading on the Indonesia Stock Exchange in July, including stock indices performance, trading volumes and values, most active stocks, new and delisted listings, and financial data and ratios for listed companies. The report aims to inform readers about the performance and activities on the Indonesia Stock Exchange in July 2019.

Antiepileptic Drugs

- Lessons from Psychiatry

In this lecture:

1. AED’s: Looking Beyond Epilepsy- Their Relevance & Utility in Neuropsychiatry

2. Parodoxical relationships: seizures, behavior and AEDs

3. What relevance do these findings hold for epilepsy

Optitax's presentation on implication of gst on related party 10.06.2018

In this presentation we have tried to highlight the implication of GST on related party transactions. Everyone should be aware that under GST if there is any transaction with related party then valuation aspect to be kept in mind.

Crr and slr management

cash reserve ratio, statutory liquidity ratio, borrowing and lending behaviour of financial institutions

Chapter 1 the nature of fraud

The document defines fraud and discusses its different types. It describes fraud as theft by deception or trickery to obtain an unjust advantage. The main types are occupational fraud committed by employees against an organization, and fraud committed for an organization like financial statement fraud. Employee embezzlement, vendor fraud, and customer fraud are provided as examples of fraud against an organization. Management fraud committed through misleading financial statements can harm shareholders and investors. Criminal prosecution through law and civil lawsuits aim to punish fraudsters and compensate victims.

NBFCs - A quick guide by Niddhi Parmar

This document provides a summary of Non-Banking Financial Companies (NBFCs) in India. It defines what an NBFC is, outlines the key types of NBFCs such as asset finance companies, loan companies, investment companies, and microfinance institutions. It also describes important NBFC concepts like capital adequacy requirements, classification of assets, and the regulations applicable to different categories of NBFCs. The document is intended to serve as a quick guide to NBFCs in India.

Auditing

This document provides an overview of auditing. It defines auditing as an unbiased examination and evaluation of a company's financial statements, internally or externally. It distinguishes auditing from bookkeeping and accounting by noting that auditing examines the accuracy and fairness of financial records, while bookkeeping records transactions and accounting analyzes results. The document also describes common types of errors like omissions and commissions that may occur, and how they differ from intentional frauds. Finally, it gives examples of specific frauds like misappropriation of cash, goods, assets, and manipulation of accounts.

Know your customer(kyc) Norms

The document discusses Know Your Customer (KYC) norms and their importance. It begins by stating the session objectives of explaining the significance of KYC norms and why banks need to comply with them. It then provides examples of identity theft, credit card fraud, and money laundering to illustrate the risks banks face and why KYC procedures are necessary to prevent illicit transactions, money laundering, and terrorist financing. The document emphasizes that KYC norms issued by the Reserve Bank of India are aimed at arresting these criminal activities. It also notes exceptions for "no frills" accounts that have stricter limits on balances and credit amounts.

Bill of exchange

The document defines a bill of exchange as a written instrument containing an unconditional order from a creditor (drawer) to a debtor (drawee) to pay a specified amount of money to a person (payee). There are three parties to a bill of exchange: the drawer, drawee, and payee. The drawer makes the order, the drawee is directed to pay, and the payee receives the money. A bill of exchange must be in writing, contain an express order to pay, specify three definite parties, state a certain amount of money payable in legal tender, and comply with formalities like date and stamp.

mental status examination

A mental status examination (MSE) is used to evaluate a patient's psychological well-being and state of mind. It includes objective observations by the clinician and subjective reports from the patient. The MSE assesses several domains including appearance, motor skills, speech, mood, affect, thought processes, thought content, perception, and cognitive functioning. However, an MSE is not an intelligence test and cannot provide a fully precise evaluation. It is a standard clinical technique used to evaluate symptoms of conditions like depression, mania, schizophrenia, and others.

residential status and its effect on tax incidence

The document discusses the determination of residential status in India for income tax purposes. It defines the different types of residential statuses as ordinary resident, resident but not ordinarily resident, and non-resident. It outlines the basic conditions and additional conditions to determine if an individual, HUF, firm, company, etc. qualifies as a ordinary resident or resident but not ordinarily resident. The control and management of affairs is used to determine residential status for HUF, firm, association of persons, and companies. Income from different sources is taxable in India based on the residential status of the assessee.

Role of RBI in financial inclusion

Starting of Financial Inclusion in India

Banking and financial services at an affordable cost to the vast sections of disadvantaged and low income groups.

Important step towards inclusive growth

SPECIAL KINDS OF HALLUCINATIONS oroginal.pptx

functional ,reflex ,autoscopy ,extracampine ,pseudohallucinations ,induced hallucinations ,phantom limb pain as described in fish psychopathology and SIMS(symptoms of mind) for m.phil clinical psychology

Entrepreneurship development - Institutional Assistance

Financial Assistance through SFCs,

SIDBI, Commercial bank, KSIDC,

KSSIC, IFCI; Non – financial

assistance from DIC, SISI, EDI, SIDO,

AWAKE, TCO, TECKSOK, KVIC;

Financial Incentives for SSI and Tax

Concessions’ Industrial Estates – its

roles and types.

What's hot (20)

Borderline Personality Disorder presented by MANASA GS, MSC APPLIED PSYCHOLOG...

Borderline Personality Disorder presented by MANASA GS, MSC APPLIED PSYCHOLOG...

Optitax's presentation on implication of gst on related party 10.06.2018

Optitax's presentation on implication of gst on related party 10.06.2018

residential status and its effect on tax incidence

residential status and its effect on tax incidence

Entrepreneurship development - Institutional Assistance

Entrepreneurship development - Institutional Assistance

Viewers also liked

Penalties under indian companies act

This document outlines penalties under the Indian Companies Act for various offenses. It provides a table with 34 sections listing the nature of the offense, applicable penalty, and persons held responsible. Penalties include fines from Rs. 500 to Rs. 50,000 per day and imprisonment up to 5 years for offenses such as failing to hold annual general meetings, not filing annual accounts, improper financial reporting, accepting deposits over limits, and prospectus violations. The document emphasizes that knowledge of company law and potential penalties is essential for company directors and officers to avoid legal issues arising from non-compliance.

Maintenance of records, electronically.

Companies Act 2013 requires listed companies and companies with over 1000 shareholders to maintain all statutory records electronically. Other companies can choose physical or electronic records but must follow guidelines if choosing electronic. Records include registers, minutes, agreements and other documents. Electronic records must be readable, retrievable, reproducible, capable of being dated and digitally signed. Managing directors are responsible for ensuring security, accuracy, accessibility and backup of electronic records. Records must be available for inspection electronically on payment. Companies must follow additional requirements for maintaining books electronically like ensuring accessibility in India and regular backups.

List of Statutory Registers under Companies Act 2013

The document outlines 12 statutory registers that companies are required to maintain under the Companies Act, 2013 and related rules. For each register, it provides the name, applicable section/rule, companies required to maintain, timeline for entries/preservation, and authentication requirements. The registers include the register of charges, loans/guarantees provided by the company, investments not held in company's name, contracts with related parties, members, debenture/security holders, renewed/duplicate share certificates, sweat equity shares, employee stock options, shares bought back, deposits accepted, and directors/KMP and their shareholdings. Most registers must be authenticated by a director/company secretary and preserved permanently at the registered office.

Checklist COMPLIANCE'S OF LISTED COMPANIES AS PER NEW COMPANIES ACT, 2013

1. This document provides a checklist of compliance requirements for listed companies on a quarterly basis, including deadlines for submitting various reports to the stock exchange, ROC, and SEBI.

2. It outlines numerous reporting deadlines, such as submitting quarterly financial results within 30 days of the quarter end, publishing results within 48 hours of the board meeting, and filing annual reports within 30 days of the AGM.

3. The checklist covers compliance requirements for four quarters as well as annual and general requirements, with deadlines specified for each item. It aims to help listed companies adhere to all necessary regulatory filings on time.

iPro - Software for Company Statutory e-forms & Registers.

iPro is software designed for statutory forms and registers required of companies according to government guidelines. It allows users to maintain annual returns, combined registers, minutes, forms, notices, certificates and more as required by ROC. The software features automatic population of company data, import of financial data, management of shares and shareholder data, fixed assets, meetings and charges. It supports all major e-forms and provides reports like shareholder lists, director details, single transaction reports, uploaded forms and more. The software aims to automate back office processes for companies to reduce manual work.

Format Of All Statutory Registers Under Companies Act

The document outlines the various statutory registers that must be maintained by companies under the Companies Act, 1956. It lists 20 different types of registers including registers for members, charges, investments, deposits, allotments, directors' interests and minutes of meetings. For each register, it provides details on the relevant section of the Companies Act that mandates the register, its name and whether it is maintained in physical or soft copy format and whether it is updated. Standard formats for maintaining the information in many of the registers are also presented.

Statutory meeting of company

The document discusses the statutory meeting requirements for companies limited by shares or guarantee under section 157 of the Companies Law. It states that every such company must hold a statutory meeting within 3-6 months of being entitled to commence business. At least 21 days prior, directors must provide members with a statutory report certified by at least 3 directors including the CEO. The report must provide details of share allotments, cash receipts, financial statements, directors and advisers, contracts, and commissions paid. The meeting allows members to discuss the formation and affairs of the company. Non-compliance can result in fines or winding up proceedings.

All about Permanent Account Number (PAN)

The document provides information about Permanent Account Numbers (PAN) in India. It discusses that PAN is a 10-digit alphanumeric number issued by the Income Tax department to identify taxpayers. The fourth character of the PAN denotes the taxpayer type such as individual, company, HUF, etc. and the fifth character denotes the first letter of the name. Instructions are provided on how to apply for a PAN, required documents, fees, and tracking application status.

Forms & deadline under companies act, 2013

This document outlines various compliance requirements and deadlines for filing forms under the Companies Act, 2013. It lists 23 different forms that must be filed for events like changes to a company's registered office, allotment of securities, annual returns, financial statements, appointment of directors, and more. The deadlines for filing these forms range from 15 days to 60 days after the relevant event occurs. Failure to meet these deadlines to file the required forms can result in penalties for the company.

Viewers also liked (9)

List of Statutory Registers under Companies Act 2013

List of Statutory Registers under Companies Act 2013

Checklist COMPLIANCE'S OF LISTED COMPANIES AS PER NEW COMPANIES ACT, 2013

Checklist COMPLIANCE'S OF LISTED COMPANIES AS PER NEW COMPANIES ACT, 2013

iPro - Software for Company Statutory e-forms & Registers.

iPro - Software for Company Statutory e-forms & Registers.

Format Of All Statutory Registers Under Companies Act

Format Of All Statutory Registers Under Companies Act

Similar to Penalty for non maintaing statutory records & registers

ROC Compliance Calendar: Key Dates and Deadlines You Should Know About

ROC Compliance Calendar: Key Dates and Deadlines You Should Know AboutManish Anil Gupta & Co. - A CA firm in Delhi, India

This article briefly describes the ROC Compliance Calendar 2022-23, & Documents required for the ROC Compliance for Private Limited CompanyDecriminalisation of offences under LLP Act, 2008

Key Takeaways:

- In house adjudication mechanism

- Introduction of Small LLP

- Issuance of NCDs by LLPs

- Concomitant & consequential amendments

Board of directors meetings of companies

The document discusses various aspects related to appointment of directors in a public company.

It outlines the process for appointing new directors other than retiring directors which includes the person expressing their intention to be appointed as director by giving a 14 day notice along with depositing Rs. 100,000. The company must then inform all members about the candidature at least 7 days before the meeting. If the person is elected, the deposit is refunded, otherwise it is forfeited.

The document also discusses rules regarding minimum and maximum number of directors, types of directors like additional, alternate, independent, rotational directors. It provides details on disqualifications, duties and liabilities of directors. Meeting procedures for board and general meetings

Secretarial Standard 1 - Mehta & Mehta

The document summarizes the key aspects of Secretarial Standard 1 regarding meetings of the board of directors. It outlines requirements for convening board meetings such as minimum notice period, quorum, and frequency of meetings. It also discusses procedures that must be followed including maintenance of attendance registers, drafting and circulation of minutes, and other governance matters related to board meetings. The standard aims to integrate and standardize diverse secretarial practices across companies.

The secrets to avoiding penalties and fines - Perspectives of HR & Finance

This is the presentation of 2nd Mini Conference as a part of Relativity's Knowledge Series program at Coimbatore & Bangalore. We introduced "Learning Via Gamification" via this program and was a great success. Participants learn real & live scenarios & nuances of compliance.

Summary of comparison of provisions of Companies (Amendment) Act, 2017 with C...

Summary of comparison of provisions of Companies (Amendment) Act, 2017 with Companies (Amendment) Ordinance Act, 2018.

Rbi guidelines for appointment of statutory central auditors

Reserve Bank of India on April 27, 2021 has issued Guidelines for appointment of Statutory Central Auditors/ Statutory Auditors of Commercial Banks (Excluding RRBs), UCBs, NBFCs (Including HFCs).

For easy understanding of above guidelines, I have prepared small presentation for the readers

Secretarial Standards- 1&2

The document summarizes standards for meetings of boards of directors and general meetings of companies in India. Some key points:

- Board meetings must be held at least once per quarter, with a maximum gap of 120 days between meetings. A quorum of at least 1/3 of directors or 2 directors, whichever is higher, is required.

- General meetings include annual general meetings that must be held annually within time limits prescribed by law, and extraordinary general meetings. Notice must be given to members at least 21 days in advance.

- Proxies allow members to appoint a representative to vote on their behalf. A member can appoint only one proxy, holding no more than 10% of shares, except members holding over

CSC: Loafing, habitual absenteeism, tardiness

The document is a memorandum from the Civil Service Commission (CSC) reminding government workers about policies regarding work hours and offenses like absenteeism, tardiness, and loafing. It warns that these behaviors are detrimental to public service. It reiterates that workers must work 8 hours per day, Monday through Friday. It states the penalties for loafing, which is suspension for 6 months to 1 year for the first offense and dismissal for the second offense. It directs agency heads to ensure workers observe proper hours and implement measures to deter unauthorized absences and tardiness.

Incorp, issue & transfer of shares final

The document provides information on various types of companies under the Companies Act 2013 such as one person company, small company, dormant company, and their key characteristics. It also summarizes the roles of an associate, registered valuer, financial year, corporate social responsibility, secretarial audit, and the National Financial Reporting Authority. Some of the key points covered include that a one person company can be owned by one individual, small companies have certain relaxations, dormant companies are inactive companies registered for future projects, associates have significant influence through shareholding or agreements, and registered valuers are required for certain valuation work.

fine and penalties as per Value Added Tax, 2052 Nepal.pdf

The document outlines various penalties under the tax act, including penalties of Rs. 20,000 for not registering within 30 days, Rs. 1,000 for not displaying registration documents, and Rs. 2,000 for not displaying a tax plate. It also lists penalties for other offenses such as not providing changes to business details within 15 days, not issuing or obtaining tax invoices, maintaining improper records, evading taxes, and various other non-compliance issues. Penalties range from Rs. 1,000 to 100% of taxes owed and include potential jail time.

Payroll & Compliance workshop for SME's

This is the presentation of 2nd Mini Conference as a part of Relativity's Knowledge Series program at Chennai. It was a great success. Participants learn real & live scenarios & nuances of compliance

Company management

Company management involves directors who collectively make up the board of directors. Directors control and manage the company's affairs as the company itself cannot act. Every company must have at least two directors for a private company and three for a public company. Directors are appointed by the articles of association, shareholders, other directors, or government in some cases. They have fiduciary duties to the company and duties of care, attendance, non-delegation, and conflict disclosure. Directors can be removed by shareholders or government in certain circumstances.

New concepts companies act 2013

The document summarizes several new concepts introduced in the Companies Act 2013, including associate companies, one person companies, independent directors, women directors, class action suits, corporate social responsibility, secretarial audits, registered valuers, and private placements. Key points include: associate companies will be considered related parties and details must be provided in annual returns; one person companies allow sole proprietorships to be formed as private companies; requirements for independent directors include a minimum number for listed companies and declarations of independence; women directors are required for certain large companies; and private placements can now be conducted by public companies through offer letters to select investors.

Companies (Amendment) Act, 2020

The document summarizes key amendments made to the Companies Act, 2013 by the Companies (Amendment) Act, 2020 relating to removal of imprisonment and changing fines to penalties for certain offences. It provides tables listing sections of the earlier Act, the previous provisions including fines and imprisonment, and the amended provisions focusing on penalties without imprisonment. The amendments aim to decriminalize certain offenses and reduce compliance burden for companies.

Private limited ppt

A private limited company is formed to expand a sole trader or partnership business through raising capital from investors while limiting liability. It must have at least 2 directors, 2 shareholders, and limits the number of members to 200. It must hold annual board meetings and an annual general meeting each year. Financial statements must be audited and filed with the Registrar of Companies along with other annual compliance filings. Record keeping includes statutory registers and compliance with income tax requirements.

manegireal remuneration

This document outlines the procedures for appointing and setting remuneration for managerial personnel under the Companies Act 2013. Key points include: managerial positions are limited to 5-year terms; qualifications like age and criminal history disqualify candidates; board approval and shareholder ratification are required for appointments; and maximum remuneration is capped at 11% of net profits, with exceptions to pay more subject to approvals. Public companies must also disclose managerial pay ratios and increases in their board reports.

Secretarial Standard on Board meetings

This standard issued by the Institute of Company Secretaries of India outlines key requirements for company board and committee meetings under SS-1, effective July 1, 2015. It allows directors to participate electronically except for restricted items, and requires notice and agenda to be circulated at least 7 days in advance. It also details requirements for independent director meetings, handling of unpublished price sensitive information, additional agenda items, interested director recusal, quorum, attendance records, resolution passing, and minutes documentation.

Company Act

The document discusses various requirements and formalities related to the appointment of directors and managing directors in companies under the Companies Act. It provides information on obtaining details from directors, differences between private and public companies, restrictions on loans and remuneration to directors, and requirements regarding appointment of managing directors and other managerial personnel.

Company Act

The document discusses various requirements and formalities related to the appointment of directors and managing directors in companies under the Companies Act. It provides information on obtaining details from directors, differences between private and public companies, restrictions on loans and remuneration to directors, and requirements regarding appointment of managing directors and other managerial personnel.

Similar to Penalty for non maintaing statutory records & registers (20)

ROC Compliance Calendar: Key Dates and Deadlines You Should Know About

ROC Compliance Calendar: Key Dates and Deadlines You Should Know About

The secrets to avoiding penalties and fines - Perspectives of HR & Finance

The secrets to avoiding penalties and fines - Perspectives of HR & Finance

Summary of comparison of provisions of Companies (Amendment) Act, 2017 with C...

Summary of comparison of provisions of Companies (Amendment) Act, 2017 with C...

Rbi guidelines for appointment of statutory central auditors

Rbi guidelines for appointment of statutory central auditors

fine and penalties as per Value Added Tax, 2052 Nepal.pdf

fine and penalties as per Value Added Tax, 2052 Nepal.pdf

More from mystartupvakil.com

Companies amendment act 2017 amended sections with analysis

The Companies Amendment Act, 2017 was passed by the Rajya Sabha in December 2017 and received presidential assent in January 2018. The amendments will come into force on dates notified by the Ministry of Corporate Affairs. This article summarizes the key amendments made to section 2, which defines terms used in the Act. Some of the important changes include expanding the definition of "associate company", including cost accountants in practice in the definition of "cost accountant", and increasing the limits for paid-up capital and turnover to qualify as a small company.

Faq on gstr 3 b

Form GSTR-3B is a simplified return form introduced for July and August 2017 that requires taxpayers to report total consolidated values for supplies rather than individual invoice details. It must be filed by all taxpayers registered under GST, except those under the composition scheme, input service distributors, or non-resident taxpayers. While the original due date for July was August 20th, it has been extended to August 25th or August 28th for those claiming transitional credit. GSTR-3B provides information on outward supplies, input tax credit, and tax payments, but individual invoice details are not required. It cannot be revised after filing.

HAPPY HOLI 2015

The document provides contact information for Company Secretaries located at 268, First Floor, Business India Complex, Uday Park, New Delhi-110049. Their phone number is 011-41407878 and their email address is cs.kashifali2gmail.com.

Secretarial Audit under Companies Act 2013

‘Secretarial Audit’ is introduced by recently enacted Companies Act, 2013. It is a process to check compliances made by the Company under Corporate Law & other laws, rules, regulations, procedures etc.

Happy New Year 2015

On the road to success, the rule is, always to look ahead. May you reach your destination. May your journey be wonderful. May each and every day of yours be renewed with lots happiness, success and prosperity. Happy New Year 2015

Happy New Year 2015

On the road to success, the rule is, always to look ahead. May you reach your destination. May your journey be wonderful. May each and every day of yours be renewed with lots happiness, success and prosperity. Happy New Year 2015

Happy independence day 2014

India celebrated Independence Day on August 15, 2014. Company Secretaries, located in New Delhi, wished everyone a happy Independence Day. The company can be contacted by phone at +91 9718483209 or by email at cs.kashifali@gmail.com.

Company law settlement scheme 2014

The document announces the Company Law Settlement Scheme 2014 launched by the Ministry of Corporate Affairs, which provides defaulting companies an opportunity to file overdue annual accounts by October 15th, 2014 for reduced fees and immunity from prosecution. Eligible companies can take advantage of the scheme's benefits, which include only having to pay 25% of applicable additional fees, immunity from persecution, and directors avoiding disqualification.

IS SECRETARIAL AUDIT MANDATORY FOR FINANCIAL YEAR 2013-14?

IS SECRETARIAL AUDIT MANDATORY FOR FINANCIAL YEAR 2013-14?

A small article on Secretarial Audit as per Companies Act, 2013.

E voting procedure-companies act 2013

General meetings of companies are often held at their registered offices, making it difficult for shareholders located far away or holding minor shares to attend in person. To address this, the Companies Act 2013 introduced e-voting to allow shareholders to cast votes electronically without attending in person. E-voting does not eliminate the right to attend and vote in person but shareholders can only vote through one method. Listed companies and those with over 1,000 shareholders must provide e-voting facilities. E-voting agencies are appointed to set up online voting systems and collect and report votes to ensure transparency.

DECODING COMPANIES ACT 2013_ CHAPTER-II

Attaching a

We have started making comparative analysis of sections of Companies Act 2013 & Companies Act 1956. We will provide you the same along with relevant MCA clarification or circular issued for the particular section.

PFA our note on chapter XII.

Companies Act 2013

companies act 2013 , company act 2013, new companies act 2013, new companies act, Companies Act 2013 as publishes in official gazette.

Detail of Directors of "Little Eye" Indian Company acquired/ takeover by face...

Details of directors and shareholders of the Company acquired by Facebook Little Eye Software Labs Private Limited.

HOW TO KNOW AVAILIBLITY OF TRADE MARK

To conduct a public search of a trade mark on the Indian IP office website, one must first log into http://ipindia.nic.in and click on the "Trade Mark" tab. Then a new window will open where the user clicks on the "Public Search" tab. From there the user can search by trade mark class or name to view search results.

HOW TO KNOW AVAILIBLITY OF TARDE MARK

The document provides instructions for conducting a public search of a trade mark on the IP India website. It explains that users should log into the website, click on the "Trade Mark" tab, and then click on the "Public Search" tab to open a window where they can search for a specific trade mark by name and class. The search results will then be displayed.

Format of AOA (Article of Association) as per New Companies Act 2013

Dear All

As you all know 98 sections of the Companies Act 2013 has been implemented w.e.f. 12th Sep 2013, therefore all ROC are asking changes in AOA. I am sharing a draft form of AOA. Kindly note that there is no change in MOA you can still use the old MOA.

Format of moa new companies act 2013 ( moa as per companies act 2013 )

Format of Memorandum of Association as per New Companies Act 2013. For more please visit my blog : http://newcompaniesact2013.blogspot.in/

MOA as per companies act 2013

List of recently implemented section

list of recently implemented sections of the Companies Act, 2013 along with corresponding sections of Companies Act 1956

Draft rules for 16 chapters issued on september 7 2013 by mca(1)

This document provides draft rules for 16 chapters of the Companies Act, 2013 that were issued by the Ministry of Corporate Affairs in India for public comment. It includes definitions for key terms related to companies, rules for incorporating a One Person Company, requirements for the subscriber or member of a One Person Company to nominate another person in case of incapacity, and rules regarding related parties. The draft rules aim to provide regulations and procedures for various provisions of the Companies Act, 2013.

More from mystartupvakil.com (20)

Companies amendment act 2017 amended sections with analysis

Companies amendment act 2017 amended sections with analysis

IS SECRETARIAL AUDIT MANDATORY FOR FINANCIAL YEAR 2013-14?

IS SECRETARIAL AUDIT MANDATORY FOR FINANCIAL YEAR 2013-14?

Detail of Directors of "Little Eye" Indian Company acquired/ takeover by face...

Detail of Directors of "Little Eye" Indian Company acquired/ takeover by face...

Format of AOA (Article of Association) as per New Companies Act 2013

Format of AOA (Article of Association) as per New Companies Act 2013

Format of moa new companies act 2013 ( moa as per companies act 2013 )

Format of moa new companies act 2013 ( moa as per companies act 2013 )

Draft rules for 16 chapters issued on september 7 2013 by mca(1)

Draft rules for 16 chapters issued on september 7 2013 by mca(1)

Recently uploaded

Building Your Employer Brand with Social Media

Presented at The Global HR Summit, 6th June 2024

In this keynote, Luan Wise will provide invaluable insights to elevate your employer brand on social media platforms including LinkedIn, Facebook, Instagram, X (formerly Twitter) and TikTok. You'll learn how compelling content can authentically showcase your company culture, values, and employee experiences to support your talent acquisition and retention objectives. Additionally, you'll understand the power of employee advocacy to amplify reach and engagement – helping to position your organization as an employer of choice in today's competitive talent landscape.

Easily Verify Compliance and Security with Binance KYC

Use our simple KYC verification guide to make sure your Binance account is safe and compliant. Discover the fundamentals, appreciate the significance of KYC, and trade on one of the biggest cryptocurrency exchanges with confidence.

Best Forex Brokers Comparison in INDIA 2024

Navigating the world of forex trading can be challenging, especially for beginners. To help you make an informed decision, we have comprehensively compared the best forex brokers in India for 2024. This article, reviewed by Top Forex Brokers Review, will cover featured award winners, the best forex brokers, featured offers, the best copy trading platforms, the best forex brokers for beginners, the best MetaTrader brokers, and recently updated reviews. We will focus on FP Markets, Black Bull, EightCap, IC Markets, and Octa.

Business storytelling: key ingredients to a story

Storytelling is an incredibly valuable tool to share data and information. To get the most impact from stories there are a number of key ingredients. These are based on science and human nature. Using these elements in a story you can deliver information impactfully, ensure action and drive change.

Unveiling the Dynamic Personalities, Key Dates, and Horoscope Insights: Gemin...

Explore the fascinating world of the Gemini Zodiac Sign. Discover the unique personality traits, key dates, and horoscope insights of Gemini individuals. Learn how their sociable, communicative nature and boundless curiosity make them the dynamic explorers of the zodiac. Dive into the duality of the Gemini sign and understand their intellectual and adventurous spirit.

Top mailing list providers in the USA.pptx

Discover the top mailing list providers in the USA, offering targeted lists, segmentation, and analytics to optimize your marketing campaigns and drive engagement.

Satta Matka Dpboss Matka Guessing Kalyan Chart Indian Matka Kalyan panel Chart

Satta Matka Dpboss Matka Guessing Kalyan Chart Indian Matka Kalyan panel Chart➒➌➎➏➑➐➋➑➐➐Dpboss Matka Guessing Satta Matka Kalyan Chart Indian Matka

SATTA MATKA SATTA FAST RESULT KALYAN TOP MATKA RESULT KALYAN SATTA MATKA FAST RESULT MILAN RATAN RAJDHANI MAIN BAZAR MATKA FAST TIPS RESULT MATKA CHART JODI CHART PANEL CHART FREE FIX GAME SATTAMATKA ! MATKA MOBI SATTA 143 spboss.in TOP NO1 RESULT FULL RATE MATKA ONLINE GAME PLAY BY APP SPBOSSTaurus Zodiac Sign: Unveiling the Traits, Dates, and Horoscope Insights of th...

Dive into the steadfast world of the Taurus Zodiac Sign. Discover the grounded, stable, and logical nature of Taurus individuals, and explore their key personality traits, important dates, and horoscope insights. Learn how the determination and patience of the Taurus sign make them the rock-steady achievers and anchors of the zodiac.

Understanding User Needs and Satisfying Them

https://www.productmanagementtoday.com/frs/26903918/understanding-user-needs-and-satisfying-them

We know we want to create products which our customers find to be valuable. Whether we label it as customer-centric or product-led depends on how long we've been doing product management. There are three challenges we face when doing this. The obvious challenge is figuring out what our users need; the non-obvious challenges are in creating a shared understanding of those needs and in sensing if what we're doing is meeting those needs.

In this webinar, we won't focus on the research methods for discovering user-needs. We will focus on synthesis of the needs we discover, communication and alignment tools, and how we operationalize addressing those needs.

Industry expert Scott Sehlhorst will:

• Introduce a taxonomy for user goals with real world examples

• Present the Onion Diagram, a tool for contextualizing task-level goals

• Illustrate how customer journey maps capture activity-level and task-level goals

• Demonstrate the best approach to selection and prioritization of user-goals to address

• Highlight the crucial benchmarks, observable changes, in ensuring fulfillment of customer needs

TIMES BPO: Business Plan For Startup Industry

Starting a business is like embarking on an unpredictable adventure. It’s a journey filled with highs and lows, victories and defeats. But what if I told you that those setbacks and failures could be the very stepping stones that lead you to fortune? Let’s explore how resilience, adaptability, and strategic thinking can transform adversity into opportunity.

DearbornMusic-KatherineJasperFullSailUni

My powerpoint presentation for my Music Retail and Distribution class at Full Sail University

Anny Serafina Love - Letter of Recommendation by Kellen Harkins, MS.

This letter, written by Kellen Harkins, Course Director at Full Sail University, commends Anny Love's exemplary performance in the Video Sharing Platforms class. It highlights her dedication, willingness to challenge herself, and exceptional skills in production, editing, and marketing across various video platforms like YouTube, TikTok, and Instagram.

The latest Heat Pump Manual from Newentide

𝐔𝐧𝐯𝐞𝐢𝐥 𝐭𝐡𝐞 𝐅𝐮𝐭𝐮𝐫𝐞 𝐨𝐟 𝐄𝐧𝐞𝐫𝐠𝐲 𝐄𝐟𝐟𝐢𝐜𝐢𝐞𝐧𝐜𝐲 𝐰𝐢𝐭𝐡 𝐍𝐄𝐖𝐍𝐓𝐈𝐃𝐄’𝐬 𝐋𝐚𝐭𝐞𝐬𝐭 𝐎𝐟𝐟𝐞𝐫𝐢𝐧𝐠𝐬

Explore the details in our newly released product manual, which showcases NEWNTIDE's advanced heat pump technologies. Delve into our energy-efficient and eco-friendly solutions tailored for diverse global markets.

Creative Web Design Company in Singapore

At Techbox Square, in Singapore, we're not just creative web designers and developers, we're the driving force behind your brand identity. Contact us today.

Call8328958814 satta matka Kalyan result satta guessing

Satta Matka Kalyan Main Mumbai Fastest Results

Satta Matka ❋ Sattamatka ❋ New Mumbai Ratan Satta Matka ❋ Fast Matka ❋ Milan Market ❋ Kalyan Matka Results ❋ Satta Game ❋ Matka Game ❋ Satta Matka ❋ Kalyan Satta Matka ❋ Mumbai Main ❋ Online Matka Results ❋ Satta Matka Tips ❋ Milan Chart ❋ Satta Matka Boss❋ New Star Day ❋ Satta King ❋ Live Satta Matka Results ❋ Satta Matka Company ❋ Indian Matka ❋ Satta Matka 143❋ Kalyan Night Matka..

Organizational Change Leadership Agile Tour Geneve 2024

Organizational Change Leadership at Agile Tour Geneve 2024

How MJ Global Leads the Packaging Industry.pdf

MJ Global's success in staying ahead of the curve in the packaging industry is a testament to its dedication to innovation, sustainability, and customer-centricity. By embracing technological advancements, leading in eco-friendly solutions, collaborating with industry leaders, and adapting to evolving consumer preferences, MJ Global continues to set new standards in the packaging sector.

Dpboss Matka Guessing Satta Matta Matka Kalyan Chart Satta Matka

Dpboss Matka Guessing Satta Matta Matka Kalyan Chart Satta Matka➒➌➎➏➑➐➋➑➐➐Dpboss Matka Guessing Satta Matka Kalyan Chart Indian Matka

Dpboss Matka Guessing Satta Matta Matka Kalyan Chart Indian Matka Indian satta Matka Dpboss Matka Kalyan Chart Matka Boss otg matka Guessing Satta Recently uploaded (20)

Easily Verify Compliance and Security with Binance KYC

Easily Verify Compliance and Security with Binance KYC

Unveiling the Dynamic Personalities, Key Dates, and Horoscope Insights: Gemin...

Unveiling the Dynamic Personalities, Key Dates, and Horoscope Insights: Gemin...

Satta Matka Dpboss Matka Guessing Kalyan Chart Indian Matka Kalyan panel Chart

Satta Matka Dpboss Matka Guessing Kalyan Chart Indian Matka Kalyan panel Chart

Taurus Zodiac Sign: Unveiling the Traits, Dates, and Horoscope Insights of th...

Taurus Zodiac Sign: Unveiling the Traits, Dates, and Horoscope Insights of th...

Anny Serafina Love - Letter of Recommendation by Kellen Harkins, MS.

Anny Serafina Love - Letter of Recommendation by Kellen Harkins, MS.

Call8328958814 satta matka Kalyan result satta guessing

Call8328958814 satta matka Kalyan result satta guessing

Organizational Change Leadership Agile Tour Geneve 2024

Organizational Change Leadership Agile Tour Geneve 2024

Dpboss Matka Guessing Satta Matta Matka Kalyan Chart Satta Matka

Dpboss Matka Guessing Satta Matta Matka Kalyan Chart Satta Matka

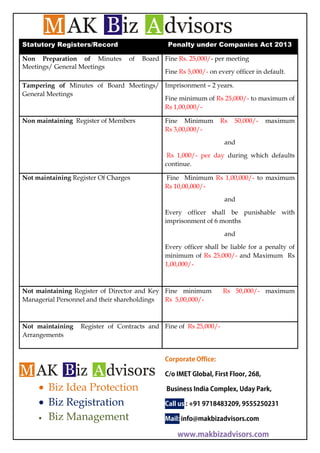

Penalty for non maintaing statutory records & registers

- 1. Statutory Registers/Record /Record Non Preparation of Minutes Meetings/ General Meetings Penalty under Companies Act 2013 of Board Fine Rs. 25,000/- per meeting Fine Rs 5,000/- on every officer in default. years. Tampering of Minutes of Board Meetings/ Imprisonment – 2 years General Meetings Fine minimum of Rs 25 25,000/- to maximum of Rs 1,00,000/Non maintaining Register of Members embers Fine Minimum Rs 3,00,000/- Rs 50,000/50 maximum nd and Rs 1,000/- per day during which defaults continue. Not maintaining Register Of Charges 00,000/- to maximum Fine Minimum Rs 1,00 Rs 10,00,000/and Every officer shall be punishable with very imprisonment of 6 months and Every officer shall be liable for a penalty of very minimum of Rs 25,000/ and Maximum Rs /1,00,000/Not maintaining Register of Director and Key Fine minimum Managerial Personnel and their s shareholdings Rs 5,00,000/Not maintaining Arrangements Rs 50 50,000/- maximum Register of Contracts a r and Fine of Rs 25,000/- Corporate Office: • Biz Idea Protection • Biz Registration • Biz Management C/o IMET Global, First Floor, 268, Business India Complex, Uday Park, Call us : +91 9718483209, 9555250231 Mail: info@makbizadvisors.com www.makbizadvisors.com