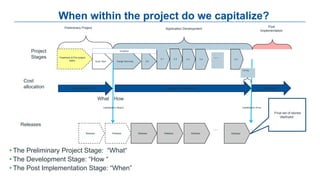

The document outlines an Agile Accounting Playbook aimed at enhancing collaboration between IT and finance to improve organizational agility and profitability through effective capitalization of software development costs. It emphasizes the need for a change in mindset, various strategies for implementing Agile accounting practices, and the potential benefits, including reduced expenses and risks. The playbook also advocates for co-creation of solutions, engaging the right stakeholders, and continuous learning to drive value creation and compliance with GAAP.

![[HCM Scrum Breakfast] Agile estimation - Story points](https://cdn.slidesharecdn.com/ss_thumbnails/storypointsestimations-160827052054-thumbnail.jpg?width=640&height=640&fit=bounds)

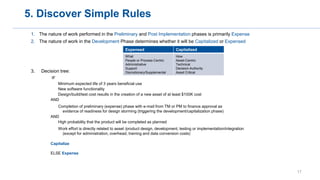

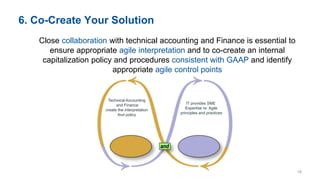

![Rick Austin - Portfolio mangement in an agile world [Agile DC]](https://cdn.slidesharecdn.com/ss_thumbnails/portfoliomangementinanagileworld-agiledc-181015223517-thumbnail.jpg?width=640&height=640&fit=bounds)