REVIEW

1. In apartnership, 3 individuals with no

business may form a partnership.

A. True

B. False

3.

REVIEW

2. What doyou call a person who takes

active part in the business of the

partnership but is not known as a

partner?

A. Dormant partner

B. Secret partner

C. Silent partner

D. Nominal partner

4.

REVIEW

3. When non-cashassets are contributed by a

partner to the partnership, the basis of

valuation is

A. at fair market value at time of contribution.

B. at fair market value a day after date of

contribution.

C. at agreed value at time of contribution.

D. at carrying amount of the asset at time of

contribution.

5.

REVIEW

4. Which ofthe following statements is

incorrect?

A. The profits of a general professional

partnership is subject to 30% income tax.

B. SEC will not allow formation of professionals

as a corporation.

C. SEC will allow professionals to form a trading

partnership.

D. As trading partnership, the profits is taxed

like a corporation at 30% of taxable income.

6.

REVIEW

5. When soleproprietorship is contributed to

the partnership, which of the following is

correct?

A. All assets and liabilities are revalued

according to agreement.

B. All assets and liabilities are revalued

according to fair market values.

C. Revaluation of assets and liabilities are

adjusted to income summary account.

D. Revaluation of assets and liabilities are

adjusted to capital account.

7.

REVIEW

6. In thecase of liquidation and the partnership assets are

insufficient to settle partnership liabilities, which of the

following statements is correct?

A. The personal assets before personal creditors of general

partner may be used to settle unpaid partnership liabilities.

B. The personal assets before personal creditors of limited

partner may be used to settle unpaid partnership liabilities.

C. The personal assets after personal creditors of general

partner may be used to settle unpaid partnership liabilities.

D. The personal assets after personal creditors of limited

partner may be used to settle unpaid partnership liabilities.

8.

REVIEW

7. A limitedpartnership is composed of

A. all general partners.

B. all limited partners.

C. all general partners and at least one

limited partner.

D. all limited partner and at least one

general partner.

9.

REVIEW

8. A partnershipwith assets P20,000,000

before financing and has 120 employees

is considered as

A. micro enterprise.

B. small enterprise.

C. medium enterprise.

D. large enterprise.

10.

REVIEW

9. Which ofthe following will not be found

in the articles of partnership?

A. Partnership name

B. Residences of the partners

C. Birthdays of the partners

D. The rights and duties of each partner.

11.

REVIEW

10. The provisionsgoverning partnership are

in:

A. Civil Code of the Philippines

B. Revised Code of Corporation of the

Philippines

C. Department of Trade and Industry

D. Securities and Exchange Commission

12.

LEARNING OBJECTIVES

1. Contrasta partner’s equity in assets from share in profits or

losses.

2. Summarize the rules for the distribution of profits or losses.

3. Explain prior period errors and interpret the effects on

partners’ share in profits or losses.

4. Identify, describe and account for the different methods of

dividing partnership profits or losses based on agreement.

5. Ascertain the effects of using original, beginning, ending

and average capitals on the partners’ share in profits or

losses.

6. Show the treatment of interest on capital, partners’ salaries

and bonus in the distribution of profits or losses.

13.

PARTNERS’ EQUITY INASSETS

CONTRASTED WITH SHARE IN PROFITS OR LOSSES

If “A is one-fourth partner,” does not always

mean that A, who has one-fourth (1/4)

equity in the net assets of the partnership,

might have smaller or larger than 1/4 share

in the partnership profits or losses. Or A, who

shares 1/4 of partnership profits or losses, has

more or less than one-fourth (1/4) equity in

the net assets of the partnership.

14.

PARTNERS’ EQUITY INASSETS

CONTRASTED WITH SHARE IN PROFITS OR LOSSES

Keep in mind, regardless of the capital

contribution of partners, they may agree on

a specific profit or loss sharing.

15.

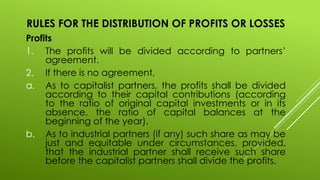

RULES FOR THEDISTRIBUTION OF PROFITS OR LOSSES

Profits

1. The profits will be divided according to partners’

agreement.

2. If there is no agreement,

a. As to capitalist partners, the profits shall be divided

according to their capital contributions (according

to the ratio of original capital investments or in its

absence, the ratio of capital balances at the

beginning of the year).

b. As to industrial partners (if any) such share as may be

just and equitable under circumstances, provided,

that the industrial partner shall receive such share

before the capitalist partners shall divide the profits.

16.

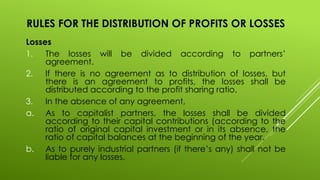

RULES FOR THEDISTRIBUTION OF PROFITS OR LOSSES

Losses

1. The losses will be divided according to partners’

agreement.

2. If there is no agreement as to distribution of losses, but

there is an agreement to profits, the losses shall be

distributed according to the profit sharing ratio.

3. In the absence of any agreement,

a. As to capitalist partners, the losses shall be divided

according to their capital contributions (according to the

ratio of original capital investment or in its absence, the

ratio of capital balances at the beginning of the year.

b. As to purely industrial partners (if there’s any) shall not be

liable for any losses.

17.

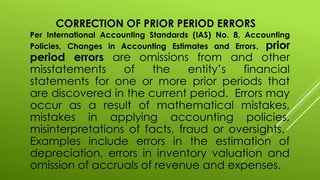

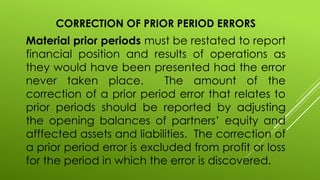

CORRECTION OF PRIORPERIOD ERRORS

Per International Accounting Standards (IAS) No. 8, Accounting

Policies, Changes in Accounting Estimates and Errors, prior

period errors are omissions from and other

misstatements of the entity’s financial

statements for one or more prior periods that

are discovered in the current period. Errors may

occur as a result of mathematical mistakes,

mistakes in applying accounting policies,

misinterpretations of facts, fraud or oversights.

Examples include errors in the estimation of

depreciation, errors in inventory valuation and

omission of accruals of revenue and expenses.

18.

CORRECTION OF PRIORPERIOD ERRORS

Material prior periods must be restated to report

financial position and results of operations as

they would have been presented had the error

never taken place. The amount of the

correction of a prior period error that relates to

prior periods should be reported by adjusting

the opening balances of partners’ equity and

afffected assets and liabilities. The correction of

a prior period error is excluded from profit or loss

for the period in which the error is discovered.

19.

DISTRIBUTION OF PROFITSOR LOSSES

BASED ON PARTNERS’ AGREEMENT

1. Equally or in other agreed ratio.

2. Based on partners’ capital contributions:

a. ratio of original capital contributions

b. ratio of capital balances at the beginning of the year

c. ratio of capital balances at the end of the year

d. Ratio of average capital balances

3. By allowing interest on partners’ capital and the balance in an

agreed ratio.

4. By allowing salaries to partners and the balance in an agreed ratio.

5. By allowing bonus to the managing partner based on profit and the

balance in an agreed ratio.

6. By allowing salaries, interest on partners’ capital, bonus to managing

partner and the balance in an agreed ratio.

20.

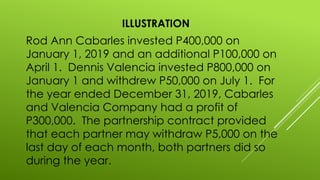

ILLUSTRATION

Rod Ann Cabarlesinvested P400,000 on

January 1, 2019 and an additional P100,000 on

April 1. Dennis Valencia invested P800,000 on

January 1 and withdrew P50,000 on July 1. For

the year ended December 31, 2019, Cabarles

and Valencia Company had a profit of

P300,000. The partnership contract provided

that each partner may withdraw P5,000 on the

last day of each month, both partners did so

during the year.

21.

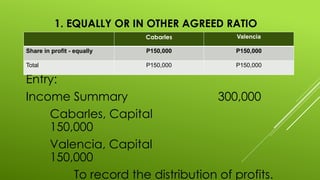

1. EQUALLY ORIN OTHER AGREED RATIO

Entry:

Income Summary 300,000

Cabarles, Capital

150,000

Valencia, Capital

150,000

To record the distribution of profits.

Cabarles Valencia

Share in profit - equally P150,000 P150,000

Total P150,000 P150,000

22.

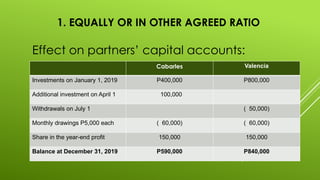

1. EQUALLY ORIN OTHER AGREED RATIO

Effect on partners’ capital accounts:

Cabarles Valencia

Investments on January 1, 2019 P400,000 P800,000

Additional investment on April 1 100,000

Withdrawals on July 1 ( 50,000)

Monthly drawings P5,000 each ( 60,000) ( 60,000)

Share in the year-end profit 150,000 150,000

Balance at December 31, 2019 P590,000 P840,000

23.

1. EQUALLY ORIN OTHER AGREED RATIO

If the partnership incurred a P300,000 loss, the

entry is:

Cabarles, Capital 150,000

Valencia, Capital 150,000

Income Summary

300,000

To record the distribution of

losses.

24.

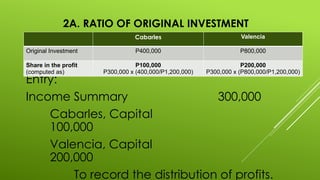

2A. RATIO OFORIGINAL INVESTMENT

Entry:

Income Summary 300,000

Cabarles, Capital

100,000

Valencia, Capital

200,000

To record the distribution of profits.

Cabarles Valencia

Original Investment P400,000 P800,000

Share in the profit

(computed as)

P100,000

P300,000 x (400,000/P1,200,000)

P200,000

P300,000 x (P800,000/P1,200,000)

25.

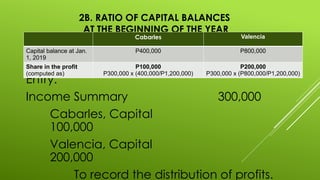

2B. RATIO OFCAPITAL BALANCES

AT THE BEGINNING OF THE YEAR

Entry:

Income Summary 300,000

Cabarles, Capital

100,000

Valencia, Capital

200,000

To record the distribution of profits.

Cabarles Valencia

Capital balance at Jan.

1, 2019

P400,000 P800,000

Share in the profit

(computed as)

P100,000

P300,000 x (400,000/P1,200,000)

P200,000

P300,000 x (P800,000/P1,200,000)

26.

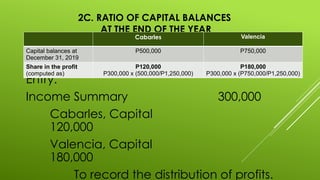

2C. RATIO OFCAPITAL BALANCES

AT THE END OF THE YEAR

Entry:

Income Summary 300,000

Cabarles, Capital

120,000

Valencia, Capital

180,000

To record the distribution of profits.

Cabarles Valencia

Capital balances at

December 31, 2019

P500,000 P750,000

Share in the profit

(computed as)

P120,000

P300,000 x (500,000/P1,250,000)

P180,000

P300,000 x (P750,000/P1,250,000)

27.

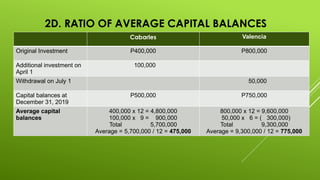

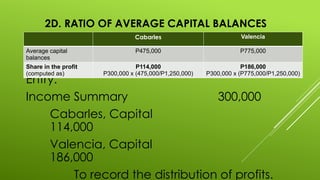

2D. RATIO OFAVERAGE CAPITAL BALANCES

Cabarles Valencia

Original Investment P400,000 P800,000

Additional investment on

April 1

100,000

Withdrawal on July 1 50,000

Capital balances at

December 31, 2019

P500,000 P750,000

Average capital

balances

400,000 x 12 = 4,800,000

100,000 x 9 = 900,000

Total 5,700,000

Average = 5,700,000 / 12 = 475,000

800,000 x 12 = 9,600,000

50,000 x 6 = ( 300,000)

Total 9,300,000

Average = 9,300,000 / 12 = 775,000

28.

2D. RATIO OFAVERAGE CAPITAL BALANCES

Entry:

Income Summary 300,000

Cabarles, Capital

114,000

Valencia, Capital

186,000

To record the distribution of profits.

Cabarles Valencia

Average capital

balances

P475,000 P775,000

Share in the profit

(computed as)

P114,000

P300,000 x (475,000/P1,250,000)

P186,000

P300,000 x (P775,000/P1,250,000)

29.

3. ALLOWING 15%INTEREST ON AVERAGE CAPITAL AND

REMAINING PROFIT IS DISTRIBUTED EQUALLY

Entry:

Income Summary 300,000

Cabarles, Capital

127,500

Valencia, Capital

172,500

To record the distribution of profits.

Share of Profit Cabarles Valencia

15% interest on capital P 71,250

P475,000 x 15% = P71,250

P116,250

P775,000 x 15% = P116,250

Remainder – equally

P300,000 – P71,250 –

P116,250 = P112,500

P 56,250

P112,500 / 2 = P56,250

P 56,250

P112,500 / 2 = P56,250

Total share in profit P127,500 P172,500

30.

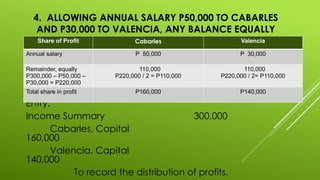

4. ALLOWING ANNUALSALARY P50,000 TO CABARLES

AND P30,000 TO VALENCIA, ANY BALANCE EQUALLY

Entry:

Income Summary 300,000

Cabarles, Capital

160,000

Valencia, Capital

140,000

To record the distribution of profits.

Share of Profit Cabarles Valencia

Annual salary P 50,000 P 30,000

Remainder, equally

P300,000 – P50,000 –

P30,000 = P220,000

110,000

P220,000 / 2 = P110,000

110,000

P220,000 / 2= P110,000

Total share in profit P160,000 P140,000

31.

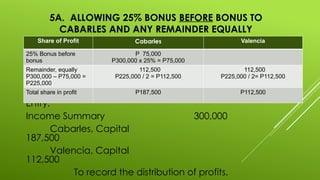

5A. ALLOWING 25%BONUS BEFORE BONUS TO

CABARLES AND ANY REMAINDER EQUALLY

Entry:

Income Summary 300,000

Cabarles, Capital

187,500

Valencia, Capital

112,500

To record the distribution of profits.

Share of Profit Cabarles Valencia

25% Bonus before

bonus

P 75,000

P300,000 x 25% = P75,000

Remainder, equally

P300,000 – P75,000 =

P225,000

112,500

P225,000 / 2 = P112,500

112,500

P225,000 / 2= P112,500

Total share in profit P187,500 P112,500

32.

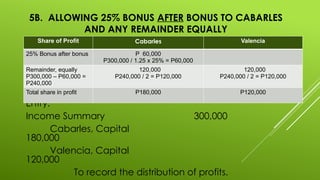

5B. ALLOWING 25%BONUS AFTER BONUS TO CABARLES

AND ANY REMAINDER EQUALLY

Entry:

Income Summary 300,000

Cabarles, Capital

180,000

Valencia, Capital

120,000

To record the distribution of profits.

Share of Profit Cabarles Valencia

25% Bonus after bonus P 60,000

P300,000 / 1.25 x 25% = P60,000

Remainder, equally

P300,000 – P60,000 =

P240,000

120,000

P240,000 / 2 = P120,000

120,000

P240,000 / 2 = P120,000

Total share in profit P180,000 P120,000

33.

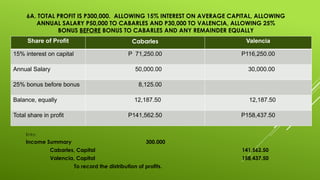

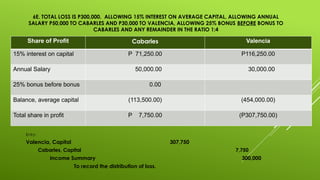

6A. TOTAL PROFITIS P300,000. ALLOWING 15% INTEREST ON AVERAGE CAPITAL, ALLOWING

ANNUAL SALARY P50,000 TO CABARLES AND P30,000 TO VALENCIA, ALLOWING 25%

BONUS BEFORE BONUS TO CABARLES AND ANY REMAINDER EQUALLY

Entry:

Income Summary 300,000

Cabarles, Capital 141,562.50

Valencia, Capital 158,437.50

To record the distribution of profits.

Share of Profit Cabarles Valencia

15% interest on capital P 71,250.00 P116,250.00

Annual Salary 50,000.00 30,000.00

25% bonus before bonus 8,125.00

Balance, equally 12,187.50 12,187.50

Total share in profit P141,562.50 P158,437.50

34.

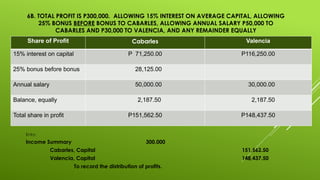

6B. TOTAL PROFITIS P300,000. ALLOWING 15% INTEREST ON AVERAGE CAPITAL, ALLOWING

25% BONUS BEFORE BONUS TO CABARLES, ALLOWING ANNUAL SALARY P50,000 TO

CABARLES AND P30,000 TO VALENCIA, AND ANY REMAINDER EQUALLY

Entry:

Income Summary 300,000

Cabarles, Capital 151,562.50

Valencia, Capital 148,437.50

To record the distribution of profits.

Share of Profit Cabarles Valencia

15% interest on capital P 71,250.00 P116,250.00

25% bonus before bonus 28,125.00

Annual salary 50,000.00 30,000.00

Balance, equally 2,187.50 2,187.50

Total share in profit P151,562.50 P148,437.50

35.

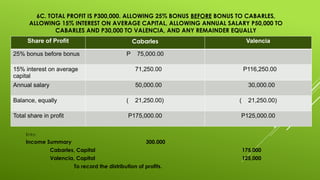

6C. TOTAL PROFITIS P300,000. ALLOWING 25% BONUS BEFORE BONUS TO CABARLES,

ALLOWING 15% INTEREST ON AVERAGE CAPITAL, ALLOWING ANNUAL SALARY P50,000 TO

CABARLES AND P30,000 TO VALENCIA, AND ANY REMAINDER EQUALLY

Entry:

Income Summary 300,000

Cabarles, Capital 175,000

Valencia, Capital 125,000

To record the distribution of profits.

Share of Profit Cabarles Valencia

25% bonus before bonus P 75,000.00

15% interest on average

capital

71,250.00 P116,250.00

Annual salary 50,000.00 30,000.00

Balance, equally ( 21,250.00) ( 21,250.00)

Total share in profit P175,000.00 P125,000.00

36.

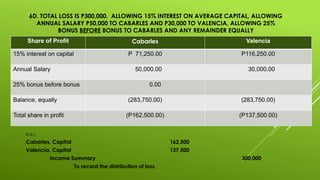

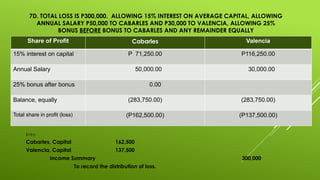

6D. TOTAL LOSSIS P300,000. ALLOWING 15% INTEREST ON AVERAGE CAPITAL, ALLOWING

ANNUAL SALARY P50,000 TO CABARLES AND P30,000 TO VALENCIA, ALLOWING 25%

BONUS BEFORE BONUS TO CABARLES AND ANY REMAINDER EQUALLY

Entry:

Cabarles, Capital 162,500

Valencia, Capital 137,500

Income Summary 300,000

To record the distribution of loss.

Share of Profit Cabarles Valencia

15% interest on capital P 71,250.00 P116,250.00

Annual Salary 50,000.00 30,000.00

25% bonus before bonus 0.00

Balance, equally (283,750.00) (283,750.00)

Total share in profit (P162,500.00) (P137,500.00)

37.

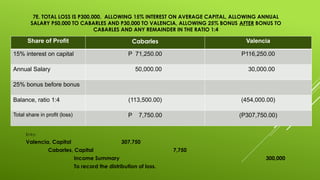

6E. TOTAL LOSSIS P300,000. ALLOWING 15% INTEREST ON AVERAGE CAPITAL, ALLOWING ANNUAL

SALARY P50,000 TO CABARLES AND P30,000 TO VALENCIA, ALLOWING 25% BONUS BEFORE BONUS TO

CABARLES AND ANY REMAINDER IN THE RATIO 1:4

Entry:

Valencia, Capital 307,750

Cabarles, Capital 7,750

Income Summary 300,000

To record the distribution of loss.

Share of Profit Cabarles Valencia

15% interest on capital P 71,250.00 P116,250.00

Annual Salary 50,000.00 30,000.00

25% bonus before bonus 0.00

Balance, average capital (113,500.00) (454,000.00)

Total share in profit P 7,750.00 (P307,750.00)

38.

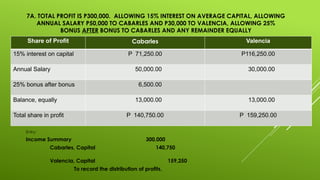

7A. TOTAL PROFITIS P300,000. ALLOWING 15% INTEREST ON AVERAGE CAPITAL, ALLOWING

ANNUAL SALARY P50,000 TO CABARLES AND P30,000 TO VALENCIA, ALLOWING 25%

BONUS AFTER BONUS TO CABARLES AND ANY REMAINDER EQUALLY

Entry:

Income Summary 300,000

Cabarles, Capital 140,750

Valencia, Capital 159,250

To record the distribution of profits.

Share of Profit Cabarles Valencia

15% interest on capital P 71,250.00 P116,250.00

Annual Salary 50,000.00 30,000.00

25% bonus after bonus 6,500.00

Balance, equally 13,000.00 13,000.00

Total share in profit P 140,750.00 P 159,250.00

39.

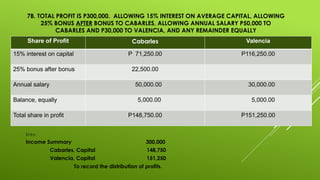

7B. TOTAL PROFITIS P300,000. ALLOWING 15% INTEREST ON AVERAGE CAPITAL, ALLOWING

25% BONUS AFTER BONUS TO CABARLES, ALLOWING ANNUAL SALARY P50,000 TO

CABARLES AND P30,000 TO VALENCIA, AND ANY REMAINDER EQUALLY

Entry:

Income Summary 300,000

Cabarles, Capital 148,750

Valencia, Capital 151,250

To record the distribution of profits.

Share of Profit Cabarles Valencia

15% interest on capital P 71,250.00 P116,250.00

25% bonus after bonus 22,500.00

Annual salary 50,000.00 30,000.00

Balance, equally 5,000.00 5,000.00

Total share in profit P148,750.00 P151,250.00

40.

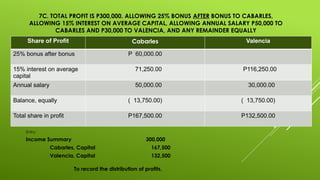

7C. TOTAL PROFITIS P300,000. ALLOWING 25% BONUS AFTER BONUS TO CABARLES,

ALLOWING 15% INTEREST ON AVERAGE CAPITAL, ALLOWING ANNUAL SALARY P50,000 TO

CABARLES AND P30,000 TO VALENCIA, AND ANY REMAINDER EQUALLY

Entry:

Income Summary 300,000

Cabarles, Capital 167,500

Valencia, Capital 132,500

To record the distribution of profits.

Share of Profit Cabarles Valencia

25% bonus after bonus P 60,000.00

15% interest on average

capital

71,250.00 P116,250.00

Annual salary 50,000.00 30,000.00

Balance, equally ( 13,750.00) ( 13,750.00)

Total share in profit P167,500.00 P132,500.00

41.

7D. TOTAL LOSSIS P300,000. ALLOWING 15% INTEREST ON AVERAGE CAPITAL, ALLOWING

ANNUAL SALARY P50,000 TO CABARLES AND P30,000 TO VALENCIA, ALLOWING 25%

BONUS BEFORE BONUS TO CABARLES AND ANY REMAINDER EQUALLY

Entry:

Cabarles, Capital 162,500

Valencia, Capital 137,500

Income Summary 300,000

To record the distribution of loss.

Share of Profit Cabarles Valencia

15% interest on capital P 71,250.00 P116,250.00

Annual Salary 50,000.00 30,000.00

25% bonus after bonus 0.00

Balance, equally (283,750.00) (283,750.00)

Total share in profit (loss) (P162,500.00) (P137,500.00)

42.

7E. TOTAL LOSSIS P300,000. ALLOWING 15% INTEREST ON AVERAGE CAPITAL, ALLOWING ANNUAL

SALARY P50,000 TO CABARLES AND P30,000 TO VALENCIA, ALLOWING 25% BONUS AFTER BONUS TO

CABARLES AND ANY REMAINDER IN THE RATIO 1:4

Entry:

Valencia, Capital 307,750

Cabarles, Capital 7,750

Income Summary 300,000

To record the distribution of loss.

Share of Profit Cabarles Valencia

15% interest on capital P 71,250.00 P116,250.00

Annual Salary 50,000.00 30,000.00

25% bonus before bonus

Balance, ratio 1:4 (113,500.00) (454,000.00)

Total share in profit (loss) P 7,750.00 (P307,750.00)

43.

What do youthink is the purpose of providing

(1) interest on capital investments, (2) salaries

to partners, and (3) bonus to managing

partner?